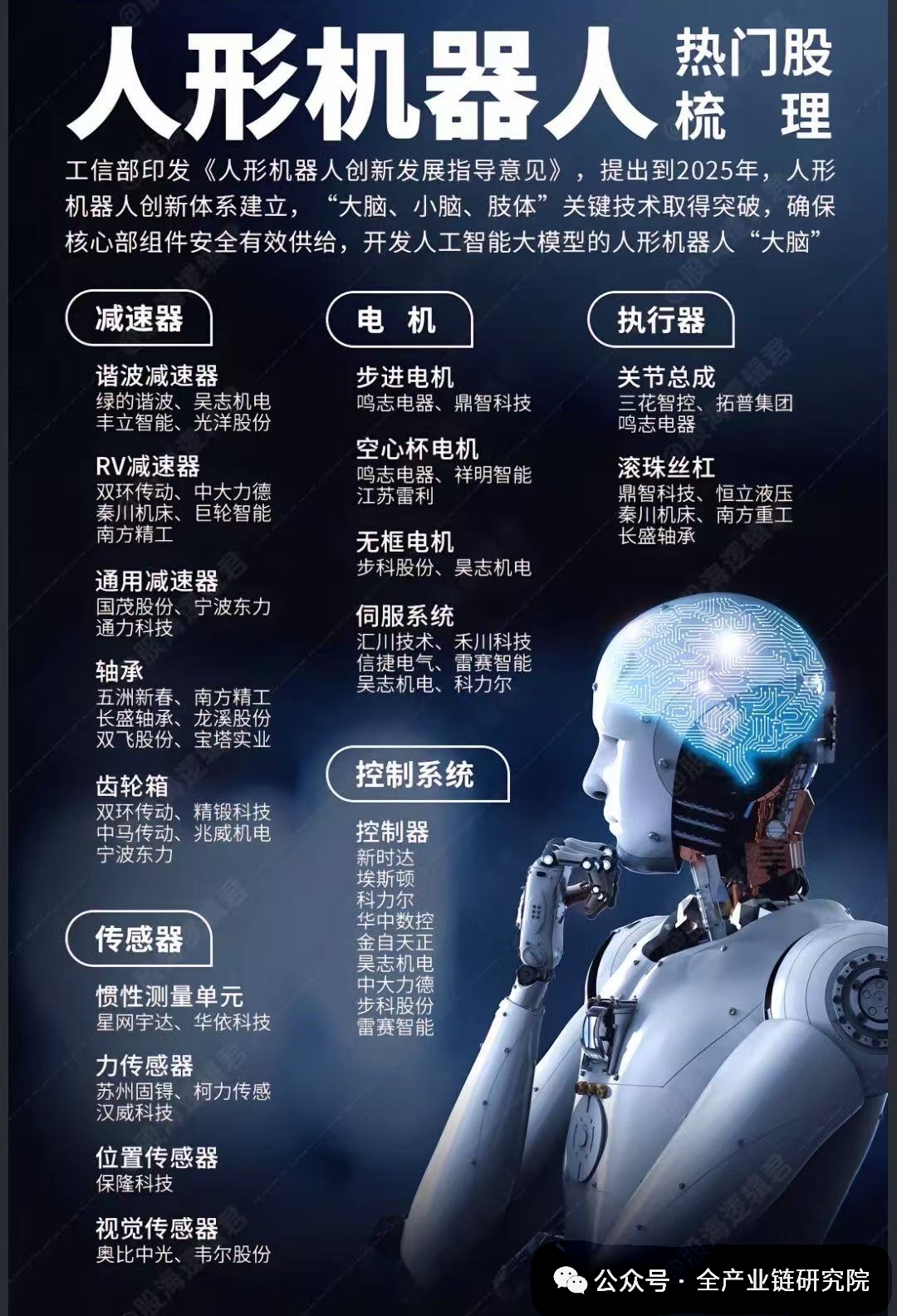

1. Analysis of Tesla Robot Core ComponentsTop Group Analysis: Top Group’s product expectations in the robotics field focus on the T2 one joint and dexterous hand. Based on a 50% market share estimate, the robot’s market value is approximately 600 – 1000 billion, and with the dexterous hand expectations, the total market value is about 1760 billion. The main business is expected to profit 3 billion by 2025, corresponding to a market value of 600 billion at a 20x PE ratio, leading to an overall market value of about 2360 billion. There is controversy in the market regarding its R&D of the dexterous hand due to the design not being finalized, but Tesla values it, and suppliers have the opportunity to obtain blueprints for production, making Top Group’s R&D probability high. The upside potential is about 82%, and the downside potential is about 54% (excluding the robot business market value). The difference with Sanhua products is minimal, but Top Group has a higher potential; after Sanhua reached a market value of 1700 billion, the T2 one business potential became more prominent.Zhejiang Rongtai Analysis: Zhejiang Rongtai’s product expectations include micro lead screws, dexterous hand motors, and potential complete hand and joint assemblies. The total market value of these businesses is approximately 740 billion, while the current robot market value is about 323 billion. The proportion of robots in the market value is high, with an upside potential of about 91% and a downside potential of about 83%. The key to future breakthroughs lies in advancing dexterous hand products and collaborating with partners to introduce the expected Tesla T2 one joint.Jiangsu Junsen and Deka Motor Analysis: Jiangsu Junsen’s business includes head modules, thoracic components, and potential dexterous hand blueprints, with a total market value target of about 1000 billion (currently over 500 billion), and the existing robot business market value is about 200 billion. Its dexterous hand R&D is slower than some manufacturers, but it has reached a strategic cooperation with partners, providing significant upward potential for the business. Deka Motor is a core target for dexterous hands, with R&D progress and certainty better than other manufacturers, and the market has already factored in many expectations. Based on a 50% sales share estimate, the market value could reach 600 – 700 billion, with the automotive business having nearly doubled potential. Since Tesla’s third-generation robot core is in the dexterous hand, Deka Motor’s dexterous hand valuation may lead the way to the extreme, then spread to other manufacturers.Xinquan Co. Recovery Logic: Xinquan Co. is a potential target for Tesla’s T1 joint, but due to slower progress than previous partners, expectations need to be discounted. Based on a 50% share, the robot business market value is about 1000 billion; at a 20% share, it is about 500 – 600 billion. The current robot business expectation is only about 120 billion (the lowest in the TR2 phase), indicating recovery potential, with future progress to be tracked.2. Analysis of Targets in Each Robot SegmentLead Screw Segment Targets: In the lead screw segment, FuDa is recommended as a recovery target. FuDa’s four-screw technology and production capacity have reached mass production levels, and the company is continuously connecting with customers and is in the testing phase. Previously, FuDa’s stock price stagnated, but it is expected to enter the T segment testing soon. Compared to other targets, FuDa has the least embedded expectations, and its marginal change direction should be monitored.Reducer Segment Targets: In the reducer segment, the cycloidal segment is the core of incremental logic, focusing on three targets: Shuanghuan Transmission, Haoneng, and Jingzhu Technology. Shuanghuan Transmission has recently performed strongly; previously, the market did not price it reasonably due to split issues, and its current certainty is considered to have been underestimated, with an estimated overall robot market value of about 700 billion at a 50% share, with about 70% upside potential. Haoneng is in a stagnation phase, with a strong position in the domestic chain, and previous expectations regarding Tesla have been digested in the current pullback, requiring tracking of its progress with Tesla. Jingzhu Technology’s market value includes expectations for providing samples to Tesla, with products launched and connected with domestic companies, seen as a dark horse target. Although certainty is weaker, the market value space is large, making it a potential recovery target for Shuanghuan Transmission.Motor Segment Targets: In the motor segment, Weichuang Electric has performed well due to multiple marginal changes, with products covering frameless torque motors and dexterous hand motors, connecting with Tesla in various aspects. Based on a 50% market value estimate, its robot business target market value is 400 – 500 billion, while the current total market value is only 160 billion, indicating a potential doubling upside and a 60% downside, with a high risk-reward ratio. Xinzhi Group has a good layout in the overseas Tesla robot, domestic Huawei robot, and Xindong Era robot fields, with a high option content in its market value, requiring attention to its certainty progress.Sensor and Lightweight Segments: In the sensor segment, the market tends to overestimate valuation premiums, and better targets need to have marginal changes from 0 to 1, such as Baolong. Baolong is engaged in sensor business and has recently laid out in the robotics field, with global capabilities, and will have high valuation elasticity when connecting with Tesla. The lightweight segment has seen many recent changes; although materials like PEEK have low value, certainty is currently more important. PEEK material-related targets are no longer scarce; Aikedi, due to its factory in Mexico, close cooperation with Tesla, and acquisition of small parts, has a low robot premium and is a target with marginal changes in the structural components of Tesla’s supply chain.Rotary Encoder Segment Targets: In the rotary encoder segment, Yapu Co. is a key target, with its main product being rotary encoders, gradually replacing magnetic encoders and having advantages in anti-interference capability. From the perspective of product quantity and value, the replacement of magnetic encoders by rotary encoders is an inflation logic that is expected to give rise to leading companies. Yapu itself has 500 – 600 million in profit support, with upward market value elasticity, and an estimated upside potential of about 70 – 80%, with only a 20% downside, making the current odds quite favorable. A conference call will be held later to report in detail on its core technology and changes.3. Recommended Directions and Rhythm for the Robot SectorCore Recommended Directions: The robot sector is recommended on three levels: first, Tier one segment, focusing on the control height of Deka Motor, then deducing the incremental elasticity of other companies; second, Tier two segment, recommending Weichuang Electric motors and Yapu; third, dark horse targets, including Jinzong Co. (PEEK materials, supported before and after thoracic positioning, for small Fusa and PEEK material recovery), Guangyang Co. (domestic chain business, expanding product categories towards actuators), and Xinyuan Zhuomei (optimistic about the trend of American alloy industry, with robot and vehicle terminal volume increasing, strong performance support).Catalytic Rhythm Suggestions: In terms of rhythm, the Tesla robot sector has continuous catalysts from factory audits to finalization. Currently, quantity and technology are gradually converging, and it is recommended to pay attention to sector opportunities.