LAIKA

2025/09/16

Steadily entering the breakeven harvest period.

Author | Gong Yan

Editor | G3007

Recently, AI has become the focal point of performance growth in the second quarter reports of major technology and internet companies. For instance, in the financial reports of Tencent, Alibaba, Baidu, Kuaishou, Meituan, etc., the frequency of AI mentions has significantly increased, with AI businesses contributing to revenue growth or efficiency improvements, leading to a surge in stock prices.

However, apart from these large companies, some usually low-profile firms have emerged as dark horses in the AI race, thanks to their steady and flexible approach. For example, on the evening of September 11, Cheetah Mobile (CMCM.US) released its Q2 2025 financial report before the US stock market opened. This company, which proposed “All in AI” even earlier than Baidu, achieved its best quarterly performance since 2021, with operational results nearing breakeven, demonstrating significant effects from its AI strategic transformation.

The market tests a company’s ability for stable operation and long-term growth in two main aspects:

First, even in the face of transformation adjustments, whether there will be significant fluctuations in current financial indicators that impact the business fundamentals. This forms the basis for stable performance today.

Second, when facing changes in the era, whether the company has the courage and ability to quickly adjust, repurposing previous R&D investments into new businesses, opening up new growth ceilings. This represents the company’s future profitability.

From these two dimensions, Cheetah Mobile’s financial report can be considered commendable. The company’s gross margin has increased for the sixth consecutive quarter, with AI revenue accounting for nearly 50%. Cheetah Mobile’s Chairman and CEO Fu Sheng stated at the earnings release that the biggest challenge in the industry lies in the return on investment (ROI). Regardless of how hot the market is, the key to successful commercialization lies in completing tasks at low cost and high reliability. The emergence of large models has injected new vitality into the industry, but achieving profitability still requires focusing on suitable scenarios to drive efficient implementation with reasonable investments.

Fu Sheng indicated that the company plans to launch more products next year, continuing the path of “focusing on scenarios and balancing investments.” Management hopes that the robotics business can quickly achieve independent profitability, thereby pushing Cheetah Mobile into a larger scale of profitability.

After the earnings disclosure, Cheetah Mobile’s stock price surged by 18.6% in a single day, with the short covering ratio reaching a nearly four-year high. We believe the company is in the early stages of a “Davis double play” with “AI empowerment, upward revenue slope + robotics operation focusing on scenarios,” and looking ahead, the company’s valuation still has significant room for recovery.

01

Strategic Transformation Solidifies Growth Trend

Breakeven Approaching Harvest Period

In recent years, with the explosive growth of AI technology and applications, global tech companies have been reinvesting in AI, even adjusting their strategic transformations to sacrifice short-term revenue and profits, leading to current performance pressures.In contrast, Cheetah Mobile’s quarterly report shows that several core financial indicators continue to maintain positive growth, with performance becoming increasingly stable.

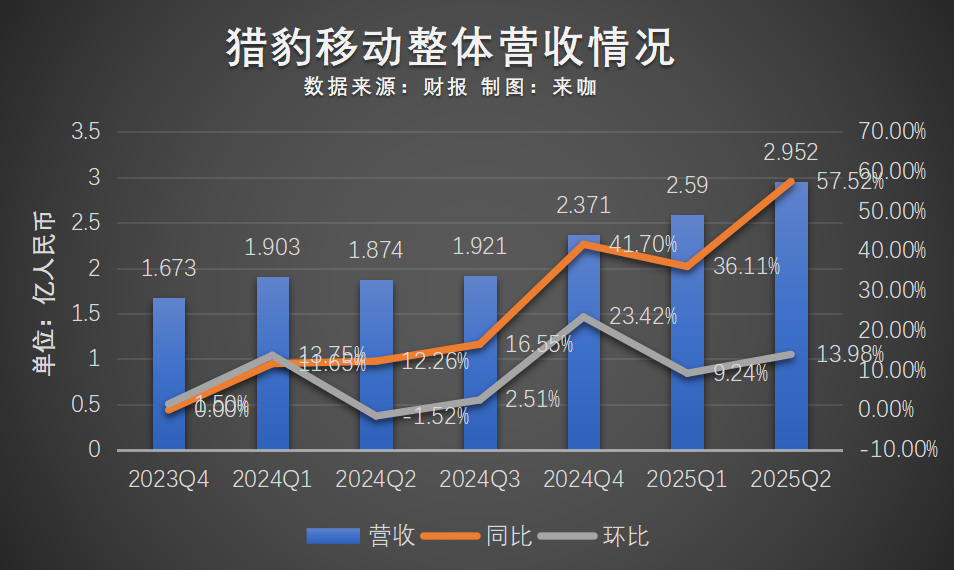

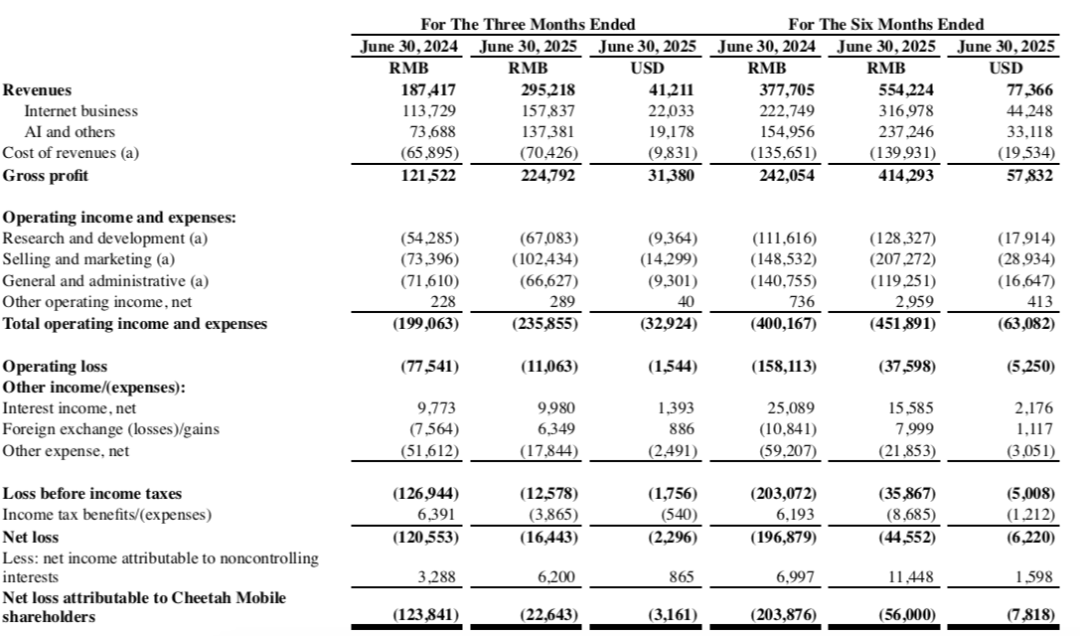

First, looking at revenue. The revenue side has experienced rapid growth for four consecutive quarters. In Q2 2025, revenue reached 295 million yuan (up 57.5% YoY, up 14.0% QoQ), with growth accelerating by 4.74 percentage points from Q1 (from 9.24% to 13.98%), significantly outperforming the 21% revenue growth average in China’s service robot industry, and also higher than the 15-20% compound growth rate in the SaaS sector.

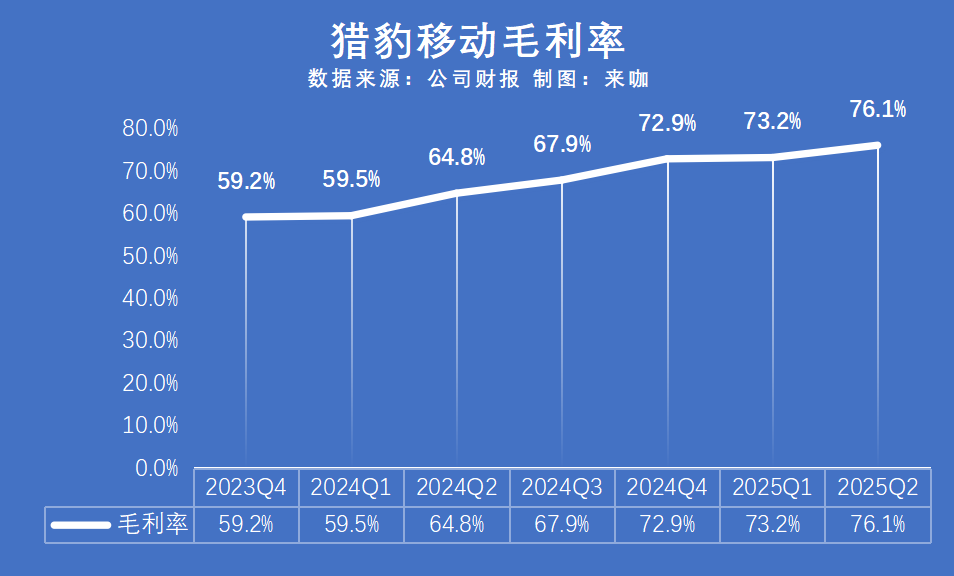

The company’s business operates on two tracks, with internet business generating 158 million yuan (up 38.8% YoY), and subscription revenue exceeding 60%; AI and robotics generated 137 million yuan (up 86.4% YoY), accounting for 46.5%. From a structural health perspective, the company is also performing excellently, with a comprehensive gross margin of 76.1%, significantly higher than the industry average, validating the premium capability of the company’s “AI + hardware + systems + services” integrated model.

This quarter, the company’s profitability inflection point appeared, with Cheetah Mobile’s Non-GAAP operating loss of 2.1 million yuan, a year-on-year decrease of 96.7% and a quarter-on-quarter decrease of 85.5%. Excluding stock-based compensation, the main business achieved breakeven.

Looking at the revenue structure over the past few quarters, it is clear that Cheetah Mobile is gradually transitioning from a revenue model heavily reliant on internet business to a diversified revenue structure with both internet and AI businesses operating in parallel. In the first half of this year, the revenue proportions of internet and AI businesses were 57.2% and 42.8%, respectively, making the two-legged approach more stable.

Additionally, the company maintains good financial health, with strong cash reserves and long-term investments providing a lasting safety net for long-term business development.

In terms of operating cash flow, after turning positive in 2023, Q2 achieved operating cash flow of 361.7 million yuan, demonstrating the company’s strong cash generation capability.

Notably, Cheetah Mobile also has long-term investments of 791.2 million yuan (110.5 million USD), including investments in several AI and robotics-related companies, which have potential for revaluation in the future.

As of June 30, the company had cash and cash equivalents of 2.0196 billion yuan (281.9 million USD), and as of the time of writing, the company’s market value was 242 million USD, with a cash market value ratio of 1.16×. The market value is lower than the company’s book cash, meaning that with a market value of 242 million USD, one can buy 281.9 million USD in cash assets, with the remaining profitable business being essentially free.

Based on the latest data from the past 12 months, Cheetah’s internet segment achieved operating profits of approximately 87 million yuan. Referring to the Hang Seng Index PE of approximately 12.6×, it can be valued at about 1.1 billion yuan; AI and other businesses generated approximately 370 million yuan in revenue over the past 12 months, and if valued at a 5-10× PS multiple in the robotics industry, it could yield 1.85-3.7 billion yuan; combined with the stable cash and investments on the books of approximately 2.73 billion yuan, the SOTP total valuation indicates the company’s reasonable market value range is approximately 5.7-7.5 billion yuan (approximately 810-1,070 million USD), indicating that the company is significantly undervalued.

02

Steady and Determined Transformation

“Differentiated Advantage in Robotics” Becomes a Rare Asset

As a leading global AI company, Cheetah Mobile primarily encompasses traditional internet business (mainly tool products) and service robotics business. However, reviewing Cheetah Mobile’s development, “steady and flexible response” has become the keyword for its cross-cycle growth.

In the fifth year of the company’s strategic shift, Cheetah Mobile’s revenue/gross profit/cash flow continues to rise, losses have significantly narrowed, and the cash market value ratio is 1.16×, indicating that Cheetah Mobile is entering the “AI harvest period.”

For example, during the PC era, Cheetah built a “three-stage rocket system” with its browser, Kingsoft Antivirus, and URL navigation to achieve profitability; then in the mobile internet era, it transformed into an overseas internet company, launching Cheetah Clean Master, Cheetah Security Master, and mobile system managers, transitioning from tool products to content; with the development of AI technology, the company began gradually transforming into an AI company in 2016 and consolidated with Orion Star in 2023.

Cheetah Mobile has completed these three technological leaps from PC to mobile to AI, achieving commercialization from zero to one. This round of review not only validates that the “management’s forward-looking judgment + strong execution capability” has been internalized into the company’s “cross-cycle algorithm,” but also confirms the company’s ability to transform industry beta into its own alpha.

This leap brings uniqueness to Cheetah Mobile’s strategic development in AI. Cheetah Mobile is the only technology company in China with large model capabilities and self-developed robots, creating a competitive barrier that makes it a relatively rare investment target in the AI robotics sector.

Compared to companies that only focus on hardware or large models, Cheetah Mobile’s approach to AI robotics combines hardware, software, and scenarios, achieving dual synergy between technology and client-side through integrating large model capabilities with robotics business.

The large model acts as the “brain” of the robot, significantly enhancing the robot’s intelligence level. Cheetah Mobile directly applies the technical experience of large models to robotic devices, such as the company’s self-developed AgentOS robot system, which significantly enhances the robot’s ability to understand intentions and plan tasks, achieving a differentiated advantage in voice-interactive robots.

Moreover, in channel management, Cheetah Mobile emphasizes the customer perspective, ensuring refined operations in product quality, pre-sales support, and after-sales response, focusing on core application scenarios such as exhibitions, elderly care, medical care, and education, allowing robots to truly land in commercial scenarios and achieve effective resource reuse, driving stable growth in the robotics business.

Data shows that since the launch of the Orion Star intelligent service robot in 2018, the cumulative total shipment of Orion Star service robots has exceeded 60,000 units, with total service instances exceeding 550 million, covering more than 60 countries and regions worldwide.

03

Favorable Industry Trends + Explosive Demand

Multiple Revenue Curves “Snowballing” Effect

This year, the robotics industry is accelerating its iteration and experiencing an unprecedented capital boom, with financing scales significantly increasing, opening up a new trillion-dollar market track.

From the perspective of overall industry development and commercialization, Cheetah’s future growth in the AI robotics sector will mainly come from two aspects:

First, as the market scale of robotics expands, Cheetah Mobile, leveraging its established leading advantage, is expected to capture more market share through product expansion, channel enhancement, and brand improvement in a market with relatively low concentration.

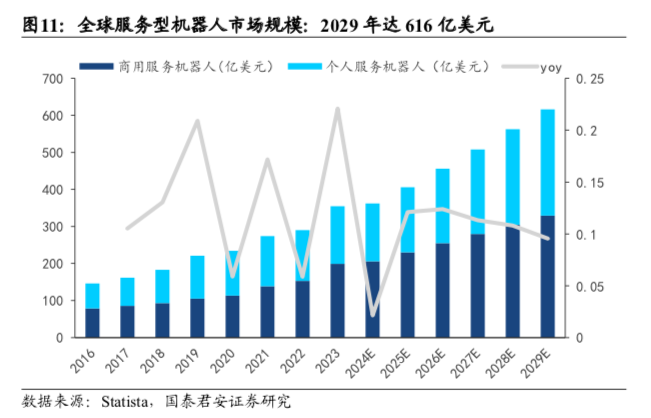

According to Statista, the global service robot market is expected to reach 36.2 billion USD in 2024 and 61.6 billion USD by 2029, with a five-year CAGR of 11.2%. Continuous upgrades in robotics technology, decreasing prices, and increasing willingness of downstream customers to pay are accelerating the rapid growth of the service robot market.

Data from the National Bureau of Statistics shows that from January to June 2025, China’s service robot production was approximately 8.8245 million units, a year-on-year increase of 25.5%. With the aging population and rising labor costs, the rigid demand for service robots in elderly care, rehabilitation training, and other fields continues to grow. Additionally, consumer demand for intelligent living experiences is expanding the market for household service robots, with rapid increases in the penetration of robot products with cleaning, security, education, and other multifunctional capabilities. In the future, service robots will extend into more segmented fields, meeting differentiated needs through modular design and personalized services, with significant growth potential in the industry expected to be further released.

In July of this year, Cheetah Mobile strategically acquired the lightweight collaborative robot company UFACTORY, which specializes in “lightweight + easy deployment” and is one of the few companies in the industry that focuses on overseas markets and has achieved profitability. At the Q2 earnings meeting, Fu Sheng stated that UFACTORY’s annual revenue has reached tens of millions of yuan while maintaining a high profit margin.

The acquisition of UFACTORY is strategically significant for Cheetah, as it enriches the product matrix of the company’s AI robots. The wheeled robots are now enhanced with mechanical arms, capable of meeting more functional needs and comprehensively covering multiple scenarios, such as hotel conference reception, restaurants, and factory logistics parks. Additionally, in terms of sales channels, Cheetah Mobile can combine UFACTORY’s advantages with Orion Star’s distribution network and over 100 global partners, allowing the robotics business to expand its sales scale globally.

With policy support and market demand resonating, the long-term positive trend of the service robot industry is clear, and Cheetah Mobile’s advantage lies in its integrated AI robots and comprehensive global layout, which is expected to benefit from this.

Some brokerage analysts have noted that during the five-year lifecycle of a single robot, hardware, software + services, combined with the high gross margin of subsequent services and stable cash returns, can create a “sell one, lock in for years” snowball effect.

Everbright Securities further commented in its latest research report that with the completion and deepening of the UFACTORY acquisition and integration, the company’s robotics product matrix will become richer, and application scenarios will further expand; the continuous optimization of the subscription model in the internet business will contribute stable cash flow; and the deep integration of AI technology with robotics scenarios will continuously enhance product competitiveness. With multiple positive factors, the company is expected to enter a new growth cycle.

Conclusion

In the second quarter of this year, Cheetah Mobile’s AI business accounted for 46.5% of total revenue, gradually approaching the target of around 50% mentioned by Fu Sheng.

With the continuous advancement of enterprise-level strategies and large model robot applications, the proportion of its AI business is expected to further increase, and in terms of revenue structure, it is transitioning from selling products to selling services, with product development evolving from “nothing to everything,” providing intelligent products and personalized, customized service solutions, continuously moving towards the mid-to-high end of the value chain, seeking new market increments.

In the context of the AI sector generally characterized by “high investment, long cycles,” Cheetah Mobile, through its own skill strength, matches the pre-commercialization capability, making it an extremely rare “cash self-circulation + profitability about to turn positive + high industry beta” triple resonance target in the current AI sector, and the company’s growth certainty has been validated by this financial report.

– END –

Previous Highlights

Highlights

Alibaba, making a strong push | Including the Q1 2026 earnings call transcript

Meituan, waiting for a moment of opportunity? | Including the Q2 2025 earnings call transcript

Pinduoduo, leaving profits for tomorrow | Including the Q2 2025 earnings call transcript