A complete framework covering portfolio construction, optimization, and risk management.

🌟 Project Highlights:

-

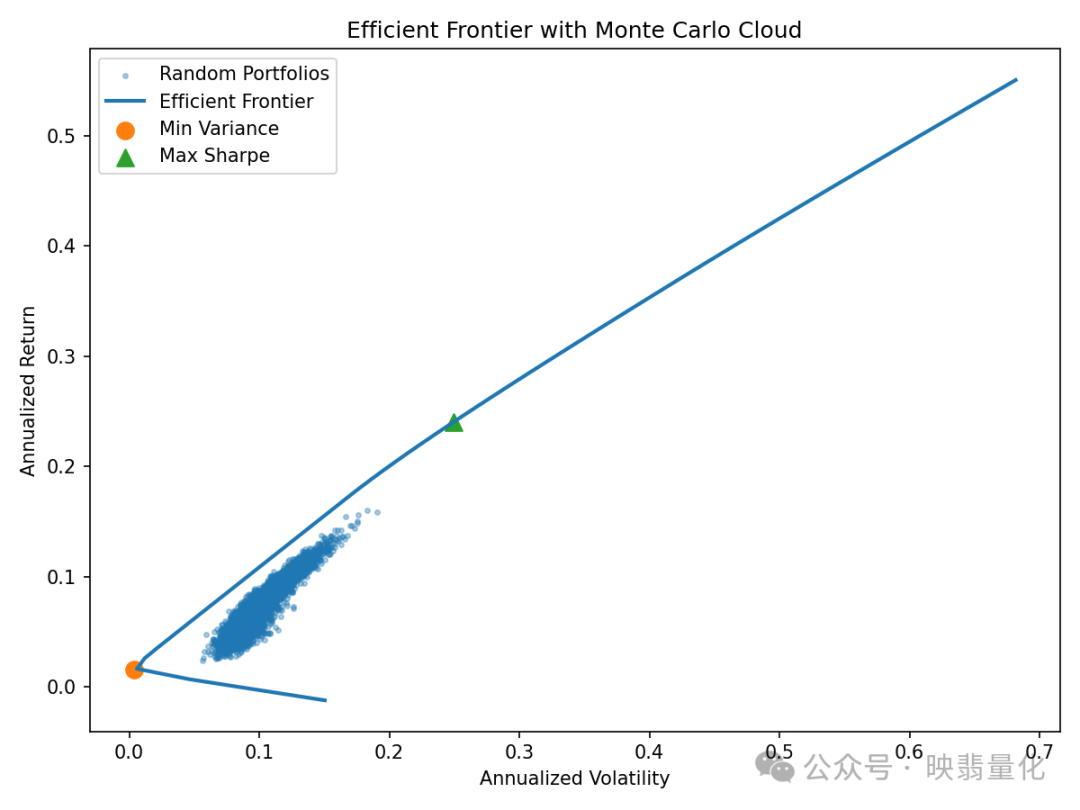

Mean-Variance Optimization (MVO): Constructing the efficient frontier and optimal portfolios.

-

Monte Carlo Simulation: Generating thousands of random portfolios to visually demonstrate the return-risk trade-off.

-

Risk Model: Risk parity allocation combined with the Black–Litterman framework incorporating investor views.

-

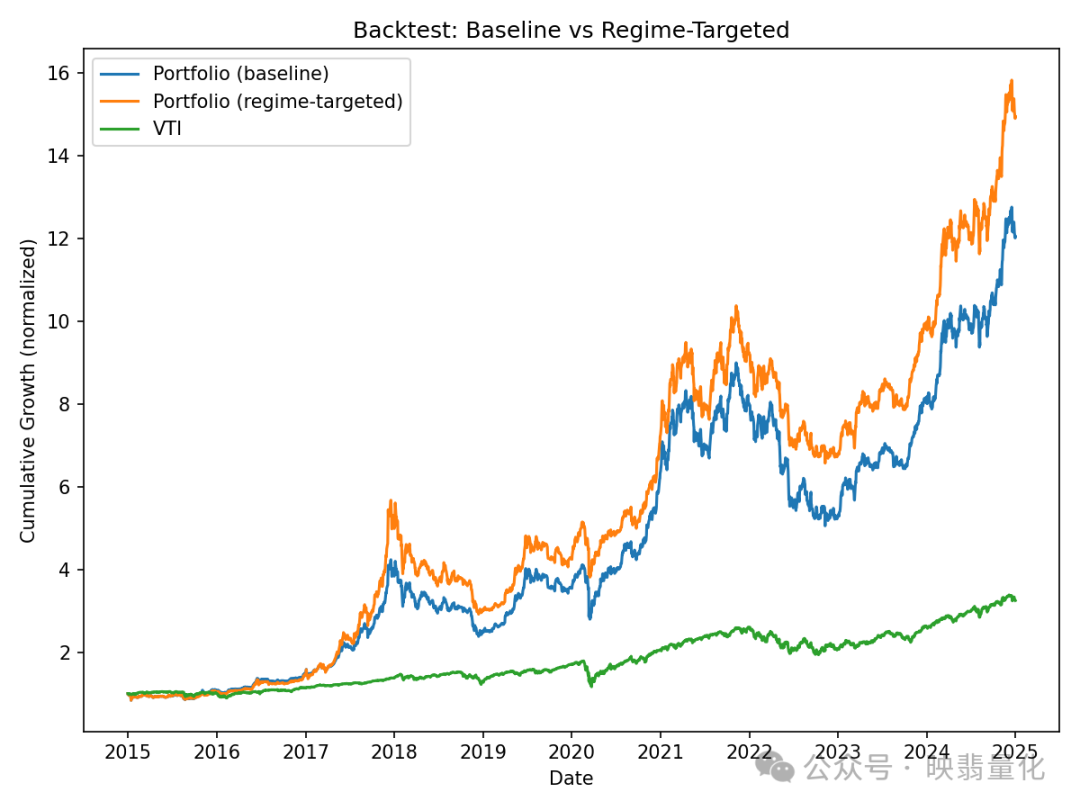

Backtesting: Adaptive scaling based on market conditions (bull, bear, and sideways markets).

📈 Core Conclusions:

-

The maximum Sharpe ratio portfolio consistently outperforms simple benchmarks.

-

Risk parity significantly reduces drawdowns through balanced exposure.

-

The Black–Litterman model integrates market equilibrium with personal insights, enhancing allocation flexibility.

🔗 The complete project (including code and charts) is open-sourced:👉https://github.com/anemer-astro/portfolio-optimization