An End-to-End Python Portfolio Optimization Open Source Project

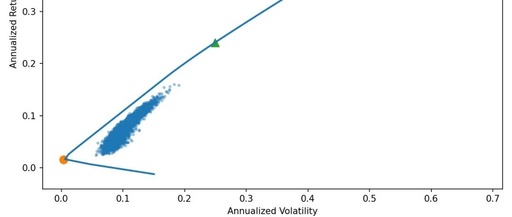

A complete framework covering portfolio construction, optimization, and risk management. 🌟 Project Highlights: Mean-Variance Optimization (MVO): Constructing the efficient frontier and optimal portfolios. Monte Carlo Simulation: Generating thousands of random portfolios to visually demonstrate the return-risk trade-off. Risk Model: Risk parity allocation combined with the Black–Litterman framework incorporating investor views. Backtesting: Adaptive scaling based on … Read more