On July 19, 2025, China announced the full launch of the Yarlung Tsangpo River downstream hydropower project, with a total investment of approximately 1.2 trillion yuan. The project plans to construct five cascade power stations (with the Motuo Power Station as the core), with a total installed capacity of 60 to 70 million kilowatts, equivalent to three Three Gorges projects (Three Gorges installed capacity is 22.5 million kilowatts), and an annual power generation of about 300 billion kilowatt-hours, which can meet the annual electricity needs of 300 million people, making it a century project.

This super project will provide a long-term, stable, and large-scale incremental market for civil explosives, cement, and steel enterprises in the region near Tibet for over a decade. Leading companies and those capable of supplying plateau engineering materials will significantly benefit. During the construction of the five giant cascade power stations (especially the core Motuo Power Station) and supporting dams, tunnels, roads, and camps, civil explosive materials will face a continuous massive demand due to the large-scale rock excavation (such as tunnel excavation, dam foundation treatment, and road construction); cement consumption will reach astronomical figures, especially special cements that meet the requirements of low temperature, early strength, and high durability in plateau conditions, which will be widely used in dam body pouring, tunnel lining, and grouting projects; at the same time, steel (rebar, steel plates, section steel) will be used extensively in dams, power plants, pressure steel pipes, gates, large steel structures, and construction support structures.

In addition to the significant opportunities in raw materials, up to 70% of the electricity from the Yajiang hydropower station group (approximately 42 to 49 million kilowatts) needs to be transmitted over 2000 to 3000 kilometers to the load centers in central and eastern China, which determines that the construction of a large-scale UHV transmission network is the core key to realizing the project’s value. Faced with such a massive and ultra-long-distance power transmission, ±800kV UHVDC (Ultra High Voltage Direct Current) transmission has become the only economically feasible technical solution, and it is expected that at least 4 to 6 strategic UHVDC corridors will need to be newly built (such as Southeast Tibet – Guangdong-Hong Kong-Macao, Southeast Tibet – Central China, Southeast Tibet – East China, etc.). The construction in the high-altitude, complex geological, and ecologically sensitive environment of the Qinghai-Tibet Plateau may cost as much as 30 to 50 billion yuan per line, with total investment possibly reaching 120 to 300 billion yuan, involving high-end equipment (converter valves, transformers), high-strength materials (special conductors, tower steel), and extremely complex construction.

This also brings world-class technical challenges, such as high-altitude insulation, repeated icing, strong earthquakes, complex terrain crossing, and stability issues of receiving end power grids with multiple DC feeds, which will drive related technological innovations. From planning and design, equipment manufacturing, engineering construction to material supply and later operation and maintenance, the entire UHV industry chain (covering design institutes, equipment manufacturers like NARI/XJ Electric/Xi’an Electric, engineering bureaus like PowerChina/China Energy Construction, and material suppliers) will usher in a new round of high prosperity cycle. The construction of these strategic corridors will greatly enhance the national “West-to-East Power Transmission” capability, reshape the power grid pattern, and effectively guarantee the supply of clean energy in central and eastern China, becoming a core support for national energy security and achieving carbon neutrality goals. Currently, there are two power equipment theme indices in the A-share market, and here is a detailed comparison:

| Dimension | CSI Power Grid Equipment Index (931994) | Hang Seng A-share Power Grid Equipment Index (HSCAUPG) |

|---|---|---|

| Index Overview | The CSI Power Grid Equipment Theme Index selects 80 listed companies involved in the UHV industry, smart grid construction, and other fields, reflecting the overall performance of securities of listed companies in the power grid equipment theme. |

The Hang Seng A-share Power Grid Equipment Index consists of up to 100 listed companies related to power grid equipment in Shanghai and Shenzhen, reflecting the performance of mainland listed companies related to power grid equipment. |

| Investment Direction | UHV, smart grid, power transmission equipment, new energy access technology | Power transmission, distribution systems, smart grid technology services, integrating “source-grid-load-storage” |

| Top Ten Weighted Stocks |

State Grid NARI (13.06%), TBEA (8.75%), Sifang Electric (6.59%), Zhongtian Technology (5.73%), Hengtong Optic-Electric (4.38%), Orient Cables (3.10%), Chint Electric (3.08%), Hongfa Technology (2.83%), Trina Solar (2.57%), Samsung Medical (2.30%) |

New Yisheng (13.40%), State Grid NARI (9.34%), TBEA (6.54%), Sifang Electric (5.43%), Zhongtian Technology (5.04%), Hengtong Optic-Electric (3.61%), Hongfa Technology (3.12%), Orient Cables (2.72%), Trina Solar (2.26%), Longxin Group (2.11%) |

| Industry Distribution |

Transmission and transformation equipment (45%), cables and accessories (30%), smart meters/distribution automation (15%), new energy access (10%) |

Power transmission systems (35%), distribution equipment (25%), smart grid technology (20%), industrial robots/optical electronics (20%) (Note: RBICS requires more than 40% of revenue to come from power grid equipment) |

| Policy Impact |

2025 new mandatory green electricity consumption ratio for steel/cement/polycrystalline silicon industries, acceleration of UHV Phase III project (15.3% investment growth in 2025) |

Driven by the “New Power System Action Plan (2024-2027)”, the national hub data center green electricity ratio requirement is 80% |

| Impact of Yajiang Hydropower Station |

UHV external delivery equipment (State Grid NARI/Zhongtian Technology/Baobian Electric), supporting power grid construction (expected new orders in 2025 +20%) |

High voltage DC equipment manufacturers (TBEA/Sifang Electric), smart scheduling systems (Longxin Group) |

| Future Growth Points |

1. Concentrated release of UHV tenders (2025H2 ±800kV projects); 2. Intelligent transformation of distribution networks (rural power grid accounts for 52.5%); 3. Supporting power grid construction for Yajiang hydropower station. |

1. Maturity of power trading/virtual power plant business models; 2. Chinese companies going abroad (Southeast Asia power grid upgrades); 3. AI computing power investment driving high-speed power equipment. |

| Risk Points |

Fluctuations in raw material prices (high levels of copper/aluminum/steel), new energy installation not meeting expectations (2024 utilization hours declining) |

Intensifying industry competition (component gross margin dropping to 0.02 yuan/W), technology substitution risks (hydrogen energy/storage diverting investment) |

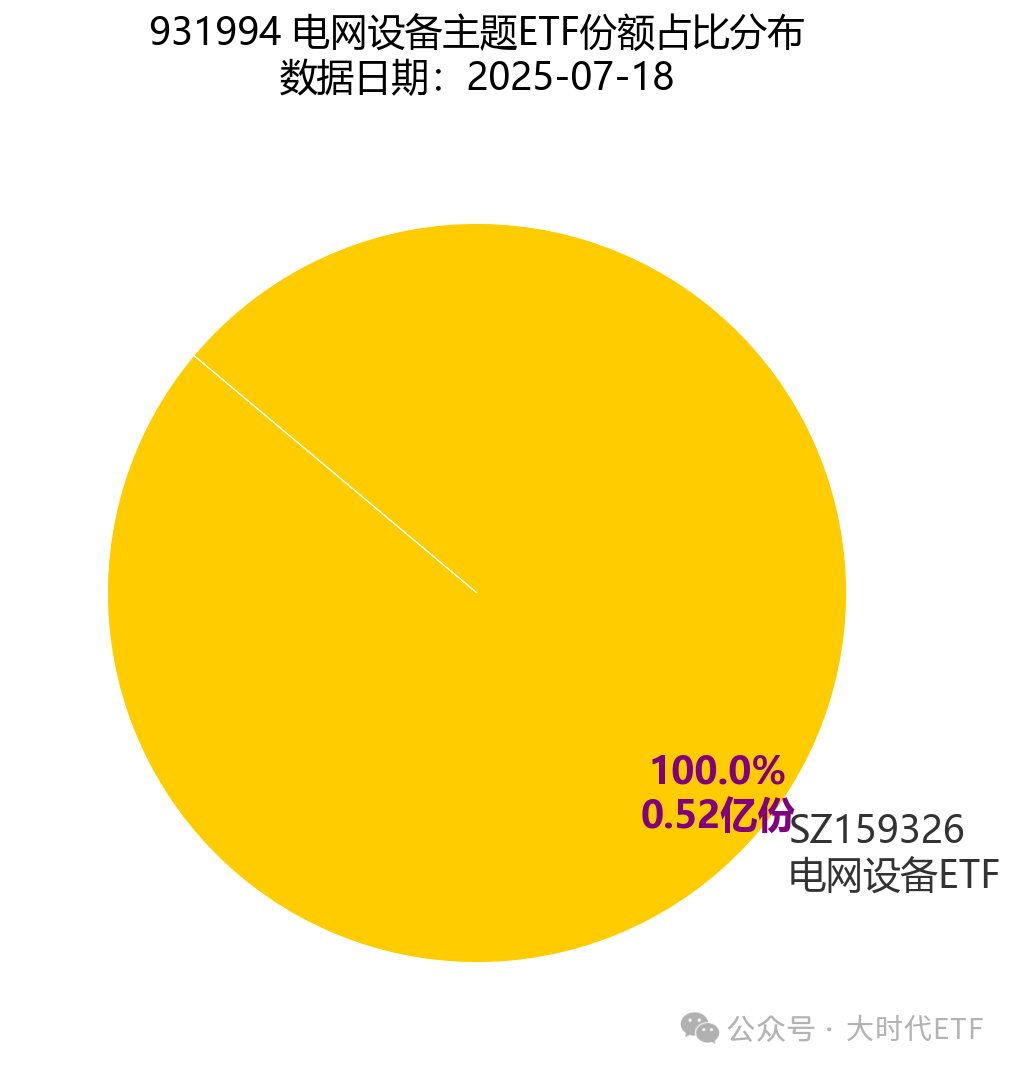

There is one ETF tracking the CSI Power Grid Equipment Index:

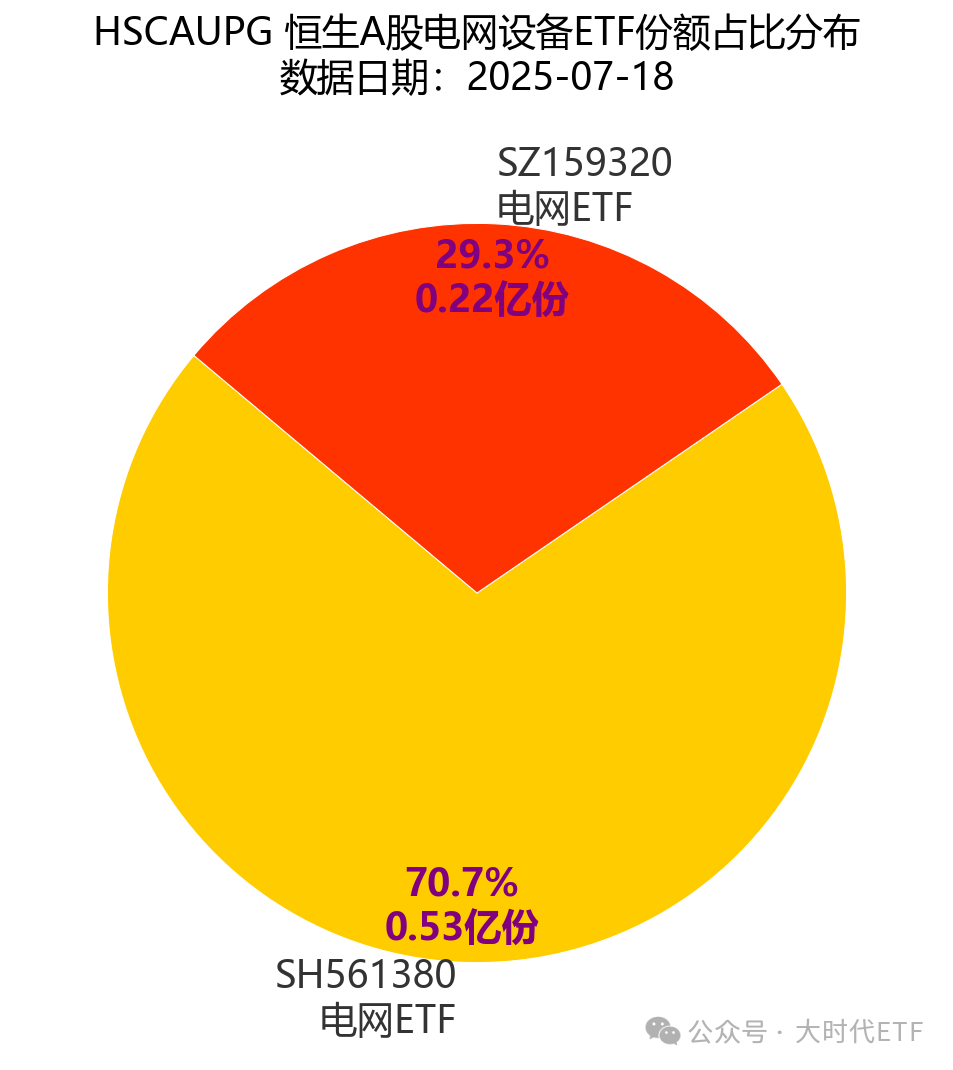

There are two ETFs tracking the Hang Seng A-share Power Grid Equipment Index, with the following scale proportions:

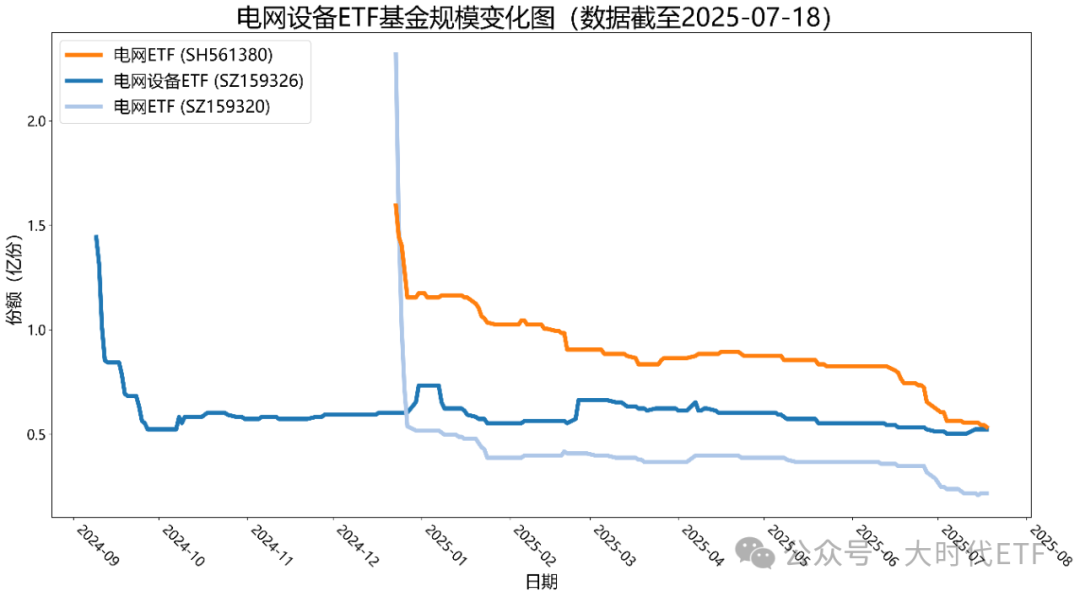

There are two ETFs tracking the Hang Seng A-share Power Grid Equipment Index, with the following scale proportions: Among these three ETFs, the largest in scale is the SH561380 Power Grid ETF, which has a scale of only 0.53 billion shares. The current market scale is completely mismatched with the huge size of the power grid, and it is expected that funds will flow in later to expand the power grid ETF.

Among these three ETFs, the largest in scale is the SH561380 Power Grid ETF, which has a scale of only 0.53 billion shares. The current market scale is completely mismatched with the huge size of the power grid, and it is expected that funds will flow in later to expand the power grid ETF.

The scale of the Yajiang hydropower station is three times that of the Three Gorges Project, which will greatly promote China to become a global leader in clean electricity. However, its development relies on grid upgrades (including UHV and smart technology) to achieve efficient power allocation. In the next decade, the core of China’s “power empire” lies not only in the enhancement of generation capacity but also in the resilience and intelligence of the power grid, marking a critical period for the explosion of demand for power grid equipment.

This public account is a non-official subscription account, purely personal scattered thoughts in a half-dream state. Under no circumstances does the content of this subscription account constitute investment advice to anyone, and I do not bear any responsibility for any losses incurred by anyone due to the use of any content contained in this subscription account.