On June 2, news from Nikkei reported that with the slowdown in the electric vehicle market and the continuous increase in production by Chinese silicon carbide (SiC) manufacturers, the silicon carbide market is facing oversupply and price declines. This has led the Japanese semiconductor giant Renesas Electronics to potentially abandon the production of silicon carbide power semiconductors for electric vehicles.

It was reported that the original plan was to start production of automotive silicon carbide power semiconductors at the Takasaki factory in early 2025, but Renesas has now disbanded the silicon carbide team at the Takasaki factory. In addition to abandoning the production of automotive silicon carbide power semiconductors, Renesas has also revised its production plans for silicon-based power semiconductors.

The main reason Renesas is abandoning the production of automotive silicon carbide power semiconductors is due to the end of subsidies in Europe, which has led to electric vehicle sales growth falling short of expectations. Meanwhile, Chinese companies have increased production of silicon carbide power semiconductors, resulting in market oversupply and continuous price declines for silicon carbide power semiconductors.

It is noteworthy that the world’s largest silicon carbide manufacturer, Wolfspeed, is facing a debt crisis of up to $6.5 billion due to intensified market competition and ongoing massive losses, and is preparing to file for bankruptcy reorganization. Last November, Wolfspeed announced a 20% workforce reduction and the closure of multiple sites and factories. This further reflects the fierce competition in the silicon carbide market.

According to the research firm Fuji Economic, the market size of silicon carbide power semiconductors is expected to grow by 18% year-on-year to 391 billion yen in 2024, which is lower than the previous estimate of 491.5 billion yen made in February 2024.

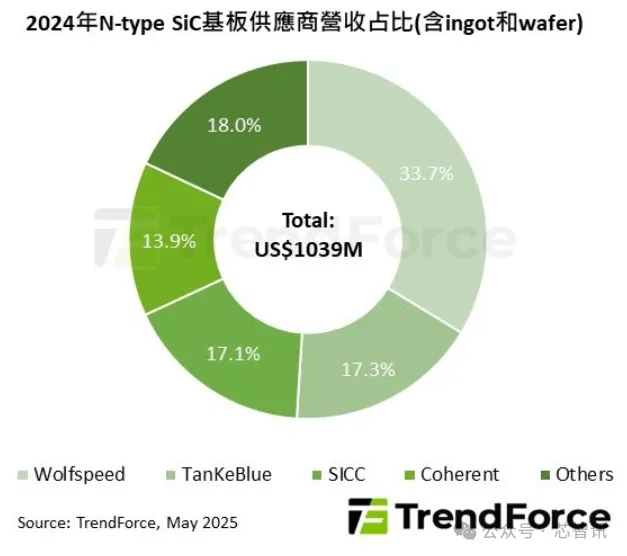

The latest report from market research firm TrendForce also shows that due to weakened demand in the automotive and industrial sectors in 2024, the global shipment growth of silicon carbide substrates is slowing down. At the same time, due to intensified market competition, product prices have dropped significantly, leading to a 9% year-on-year decline in revenue for the global N-type (conductive type) SiC substrate industry, amounting to $1.04 billion in 2024.

Previous data indicated that due to the continuous expansion of silicon carbide production capacity in China, the price decline of silicon carbide substrates is far outpacing the speed of market expansion. In the second half of 2024, the price of 6-inch silicon carbide substrates has fallen below $500, approaching the production cost line, which is a drop of over 90% compared to prices in 2022.

From the current market landscape of silicon carbide substrates, despite facing significant operational challenges in recent years, the American silicon carbide substrate giant Wolfspeed still maintains the top position, with a market share of 33.7% in 2024. However, Chinese manufacturers TanKeBlue and SICC have developed rapidly in recent years, continuously increasing their market shares, ranking second and third with market shares of 17.3% and 17.1%, respectively. TanKeBlue is the largest supplier of silicon carbide substrates in the domestic power semiconductor market, while SICC holds a leading position in the 8-inch silicon carbide wafer market. Additionally, Xiamen Silan Microelectronics, a subsidiary of Silan Micro, and the joint venture Anifa Semiconductor between STMicroelectronics and Sanan Optoelectronics are also vigorously developing 8-inch silicon carbide.

According to TrendForce’s forecast, entering 2025, the silicon carbide market will continue to face dual pressures of weak demand and oversupply.

However, from a long-term trend perspective, as the costs of silicon carbide substrates and silicon carbide devices continue to decrease, the applications of silicon carbide will become more widespread in the future.

Editor: Chip Intelligence – Wandering Sword

Previous Exciting ArticlesSynopsys CEO Sends Internal Letter: New US Regulations Will Affect All Chinese Customers!Yin Zhiyao from Zhongwei Company: Will Continue to Focus on High-End, Filling Weak Links, Not Afraid of Competitor Pressure!Has the US Requested to Cut Off EDA Supplies to China? Synopsys and Cadence Stocks PlummetTest Results Released: Qualcomm’s 5G Baseband Performance Outshines Apple’s C1Has the US Requested Three Major EDA Companies to Cut Off Supplies to China? No Notifications Received in ChinaThree Years of Losses Exceed 800 Million! Silicon Carbide IDM Giant Basic Semiconductor Files for Hong Kong Stock ExchangeBenchmarking RTX4060! Lishan Technology’s 6nm High-Performance GPU Successfully Lights Up: Has Secured Hundreds of Millions in Pre-Orders!Not Arm CSS Custom! What Exactly Did Xiaomi’s Xuanjie O1 Self-Develop?Huawei and MediaTek Patent Lawsuit Jurisdiction Dispute, Supreme Court Makes Final Decision!Xiaomi’s 13.5 Billion Burnt on “Xuanjie” Dual Chip, Is It Enough to Be “Hard”?Jensen Huang Criticizes US AI Chip Restriction Policies, NVIDIA’s Market Share in China Has Dropped to 50%!Wolfspeed to File for Bankruptcy, Stock Price Plummets Over 70%!US Global Ban on Chinese AI Chips! China Responds: Enforcers Will Violate the “Anti-Foreign Sanctions Law”Malaysia’s Sovereign AI Project Launched: Chinese AI Chips + DeepSeek Become Core Support!

For industry communication and cooperation, please add WeChat: icsmart01Chip Intelligence Official Communication Group: 221807116