Modern society is inseparable from semiconductors, from our daily-use smartphones, computers, and televisions to the spacecraft and aircraft carriers needed for national development; semiconductors are present in almost everything in our lives.Since the development of human civilization, we have experienced multiple rounds of leaps. Starting from the first industrial revolution, human civilization entered the steam age, replacing manual labor with machines; in the second industrial revolution, human civilization entered the electrical age, achieving a qualitative leap in production efficiency; and by the third industrial revolution, human civilization entered the information age, driven by semiconductor technology. It can be said that semiconductor chips are as essential as oil, a scarce resource on which the modern world relies.Many people believe that semiconductors are merely a growth industry; however, this is not the case. The semiconductor industry possesses both growth and cyclical attributes. Since 1978, the global semiconductor industry’s market size has been increasing year by year, with current global sales exceeding $500 billion. Despite over forty years of industry development, it still exhibits strong growth characteristics. However, in terms of market growth rate, there has been significant volatility over the past few decades, showing very clear cyclical attributes.Annual global semiconductor sales over the years

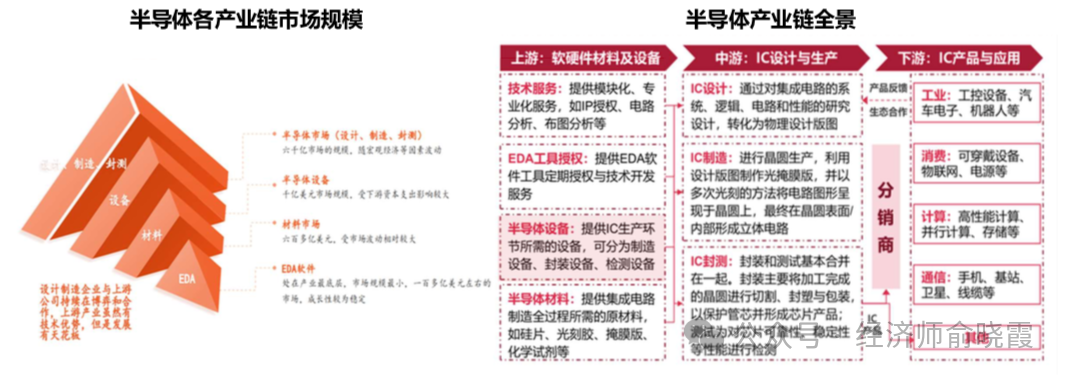

Modern society is inseparable from semiconductors, from our daily-use smartphones, computers, and televisions to the spacecraft and aircraft carriers needed for national development; semiconductors are present in almost everything in our lives.Since the development of human civilization, we have experienced multiple rounds of leaps. Starting from the first industrial revolution, human civilization entered the steam age, replacing manual labor with machines; in the second industrial revolution, human civilization entered the electrical age, achieving a qualitative leap in production efficiency; and by the third industrial revolution, human civilization entered the information age, driven by semiconductor technology. It can be said that semiconductor chips are as essential as oil, a scarce resource on which the modern world relies.Many people believe that semiconductors are merely a growth industry; however, this is not the case. The semiconductor industry possesses both growth and cyclical attributes. Since 1978, the global semiconductor industry’s market size has been increasing year by year, with current global sales exceeding $500 billion. Despite over forty years of industry development, it still exhibits strong growth characteristics. However, in terms of market growth rate, there has been significant volatility over the past few decades, showing very clear cyclical attributes.Annual global semiconductor sales over the years In summary, the semiconductor industry is characterized by a long-term upward growth trend, with cyclical changes in the medium to short term.Classic macroeconomic cycles can be divided into four types based on the duration and intrinsic driving factors:1. The Kitchin cycle driven by inventory (3-4 years)2. The Juglar cycle driven by fixed asset investment (10 years)3. The Kuznets cycle driven by real estate construction (20 years)4. The Kondratiev cycle driven by innovative technological changes (60 years)Based on this, economist Joseph Schumpeter proposed the theory of nested cycles, suggesting that the above cycles coexist, with medium, short, and long cycles nested together, working in concert.The semiconductor industry is a typical cyclical growth industry, with fluctuations in cycles arising from the combined effects of innovation cycles (long), capacity cycles (medium), and inventory cycles (short). The previous long cycles in the semiconductor industry were driven by PCs & servers and smartphones & mobile internet. From 2001 to 2010, the growth of the global semiconductor industry was primarily driven by the proliferation of the internet and laptops; from 2010 to 2020, the industry’s growth was mainly fueled by advancements in communication technology and the iterative upgrades of smartphones. After experiencing two consecutive decades of technological innovation cycles, the laptop and smartphone markets are now largely saturated. The industry is eagerly awaiting the next growth driver. When potential directions emerge, related concept valuations will rapidly increase, as evidenced by the significant performance in the AI market in the first half of 2023.The capacity cycle in the semiconductor industry generally lasts about 4 years, dominated by the supply side, characterized by a capacity cycle driven by capital expenditure. It typically takes about 2 years for a semiconductor production line to go from construction to mass production, and wafer manufacturing capacity usually takes 2-4 years from planning to implementation. Due to the lagging nature of capacity release, it cannot keep pace with changes in downstream demand, leading to supply-demand mismatches.For example, in 2020, due to the pandemic, semiconductor wafer fabs halted operations, while at the same time, the stay-at-home economy and new energy vehicles continued to surge, exacerbating the supply-demand gap and resulting in a “chip shortage”. As the industry cycle turned upward, wafer fabs began to increase capital expenditure and procure semiconductor equipment for expansion. However, in the second half of 2021, demand fell back, and by the fourth quarter of 2022, the supply-demand balance reversed, leading to oversupply. Wafer fabs began to cut capital expenditure and reduce semiconductor equipment purchases, leading to a clearing of capacity.Just as the capacity release during the expansion phase takes about 2 years, the effects of reduced capital expenditure cannot be immediately reflected but will manifest in the next upward phase of the cycle. This cycle repeats itself, characterizing the semiconductor capacity cycle.The inventory cycle in the semiconductor industry is demand-driven, lasting about 2-3 years. To observe short-term changes in industry prosperity, one primarily looks at demand and inventory. This cycle is determined by changes in the supply-demand relationship and self-regulation, including phases of active inventory replenishment, passive inventory replenishment, active destocking, and passive destocking.Until the semiconductor industry enters a downward cycle, when downstream demand is poor, it enters the passive inventory replenishment phase; subsequently, companies reduce production and begin to lower prices to clear inventory, entering the active destocking phase. Once inventory is cleared, when downstream demand surges again, a new inventory cycle will begin.For the semiconductor industry, medium to long cycles determine the overall direction of fluctuations, while the inventory cycle amplifies short-term volatility. Of course, for domestic semiconductors, long-cycle influences also include domestic substitution.So, where do semiconductor cycles come from?First, semiconductors have a very large industrial chain, making synchronization between various links difficult.From the production perspective, the semiconductor industry is mainly divided into three stages: design, manufacturing, and packaging/testing. While this may seem simple, the high-tech nature of the industry means that the materials, equipment, and processes required in each stage are exceptionally complex, leading to many sub-industries. Each sub-industry has different production difficulties and capital investments, making it challenging to synchronize production cycles, resulting in frequent supply-demand mismatches.

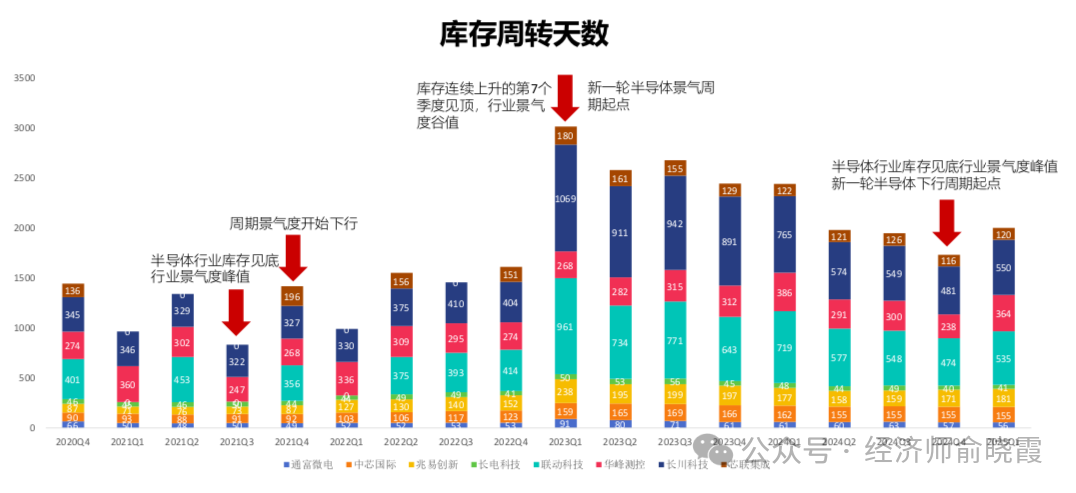

In summary, the semiconductor industry is characterized by a long-term upward growth trend, with cyclical changes in the medium to short term.Classic macroeconomic cycles can be divided into four types based on the duration and intrinsic driving factors:1. The Kitchin cycle driven by inventory (3-4 years)2. The Juglar cycle driven by fixed asset investment (10 years)3. The Kuznets cycle driven by real estate construction (20 years)4. The Kondratiev cycle driven by innovative technological changes (60 years)Based on this, economist Joseph Schumpeter proposed the theory of nested cycles, suggesting that the above cycles coexist, with medium, short, and long cycles nested together, working in concert.The semiconductor industry is a typical cyclical growth industry, with fluctuations in cycles arising from the combined effects of innovation cycles (long), capacity cycles (medium), and inventory cycles (short). The previous long cycles in the semiconductor industry were driven by PCs & servers and smartphones & mobile internet. From 2001 to 2010, the growth of the global semiconductor industry was primarily driven by the proliferation of the internet and laptops; from 2010 to 2020, the industry’s growth was mainly fueled by advancements in communication technology and the iterative upgrades of smartphones. After experiencing two consecutive decades of technological innovation cycles, the laptop and smartphone markets are now largely saturated. The industry is eagerly awaiting the next growth driver. When potential directions emerge, related concept valuations will rapidly increase, as evidenced by the significant performance in the AI market in the first half of 2023.The capacity cycle in the semiconductor industry generally lasts about 4 years, dominated by the supply side, characterized by a capacity cycle driven by capital expenditure. It typically takes about 2 years for a semiconductor production line to go from construction to mass production, and wafer manufacturing capacity usually takes 2-4 years from planning to implementation. Due to the lagging nature of capacity release, it cannot keep pace with changes in downstream demand, leading to supply-demand mismatches.For example, in 2020, due to the pandemic, semiconductor wafer fabs halted operations, while at the same time, the stay-at-home economy and new energy vehicles continued to surge, exacerbating the supply-demand gap and resulting in a “chip shortage”. As the industry cycle turned upward, wafer fabs began to increase capital expenditure and procure semiconductor equipment for expansion. However, in the second half of 2021, demand fell back, and by the fourth quarter of 2022, the supply-demand balance reversed, leading to oversupply. Wafer fabs began to cut capital expenditure and reduce semiconductor equipment purchases, leading to a clearing of capacity.Just as the capacity release during the expansion phase takes about 2 years, the effects of reduced capital expenditure cannot be immediately reflected but will manifest in the next upward phase of the cycle. This cycle repeats itself, characterizing the semiconductor capacity cycle.The inventory cycle in the semiconductor industry is demand-driven, lasting about 2-3 years. To observe short-term changes in industry prosperity, one primarily looks at demand and inventory. This cycle is determined by changes in the supply-demand relationship and self-regulation, including phases of active inventory replenishment, passive inventory replenishment, active destocking, and passive destocking.Until the semiconductor industry enters a downward cycle, when downstream demand is poor, it enters the passive inventory replenishment phase; subsequently, companies reduce production and begin to lower prices to clear inventory, entering the active destocking phase. Once inventory is cleared, when downstream demand surges again, a new inventory cycle will begin.For the semiconductor industry, medium to long cycles determine the overall direction of fluctuations, while the inventory cycle amplifies short-term volatility. Of course, for domestic semiconductors, long-cycle influences also include domestic substitution.So, where do semiconductor cycles come from?First, semiconductors have a very large industrial chain, making synchronization between various links difficult.From the production perspective, the semiconductor industry is mainly divided into three stages: design, manufacturing, and packaging/testing. While this may seem simple, the high-tech nature of the industry means that the materials, equipment, and processes required in each stage are exceptionally complex, leading to many sub-industries. Each sub-industry has different production difficulties and capital investments, making it challenging to synchronize production cycles, resulting in frequent supply-demand mismatches. Secondly, the semiconductor industry is a global collaborative industry.Currently, no single country or company can take the entire semiconductor industry chain (including materials and equipment) away. Each link has a high technical barrier, and breaking through all of them is as difficult as climbing to the sky.Therefore, to manufacture a chip, one might first seek design from NVIDIA in the United States, then manufacturing from TSMC in Taiwan, and finally packaging and testing from Amkor in the United States. This leads to cycle misalignment due to low synergy, differences in company capabilities, transportation efficiency, and other issues.So how should one invest in semiconductors?First, it is essential to have a clear understanding of the cycle position of the industry. As mentioned earlier, the semiconductor cycle can be broken down into three nested cycles: the innovation cycle, the capacity cycle, and the inventory cycle. We can approach this from these three aspects to determine the current cycle position.Every super cycle in the semiconductor industry is driven by the emergence of disruptive innovations. Such technological advancements are often accompanied by the birth of killer applications, creating massive demand. For example, the launch of the iPhone 4 triggered a wave of smartphones and mobile internet, leading to a super cycle in the semiconductor industry lasting a decade.Similarly, ChatGPT and DeepSeek became global phenomena overnight. Although the downstream application scenarios for AI remain somewhat vague, if this indeed marks the beginning of a new super cycle, we are still in the early stages.If the innovation cycle represents the growth potential of semiconductors, then the capacity cycle reflects the manufacturing attributes of the semiconductor industry. The capacity cycle represents changes on the supply side; when supply is low and downstream demand begins to rise, it is an opportune time for investment.For the capacity cycle, we can track indicators such as wafer manufacturing capacity, wafer fab capacity utilization, capital expenditure, semiconductor equipment sales, orders on hand at wafer fabs, and the speed of capacity ramp-up to locate the stage of the capacity cycle.As for inventory, it is closer to the downstream demand side and more reflective of changes in demand. An important indicator for determining the semiconductor cycle position is the inventory levels of chip companies. When inventory rises, it is a strong signal of a downward cycle. Conversely, when inventory decreases, it indicates a recovery in demand. Additionally, we can assess the strength of downstream demand and the specific position of the inventory cycle through metrics such as inventory turnover days, inventory levels, semiconductor sales, and chip prices.

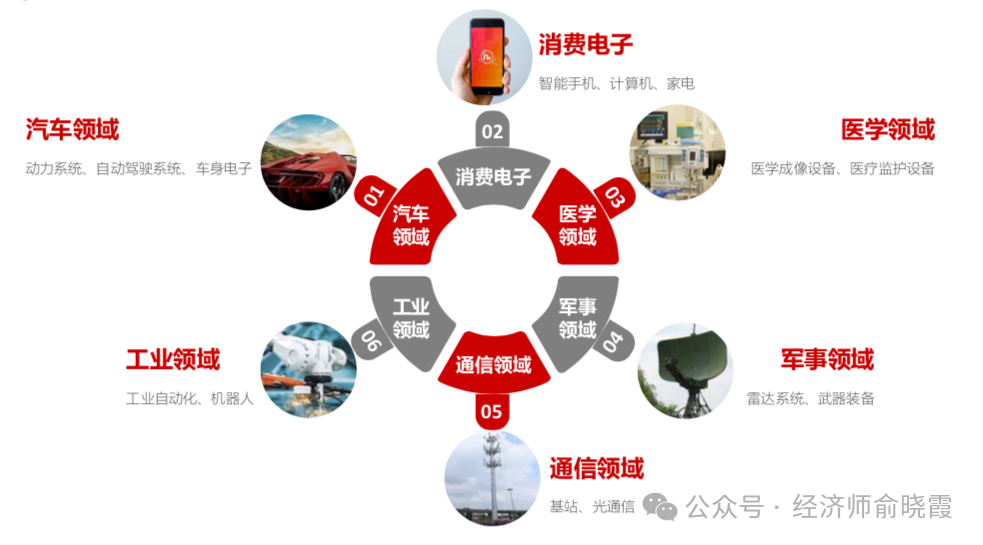

Secondly, the semiconductor industry is a global collaborative industry.Currently, no single country or company can take the entire semiconductor industry chain (including materials and equipment) away. Each link has a high technical barrier, and breaking through all of them is as difficult as climbing to the sky.Therefore, to manufacture a chip, one might first seek design from NVIDIA in the United States, then manufacturing from TSMC in Taiwan, and finally packaging and testing from Amkor in the United States. This leads to cycle misalignment due to low synergy, differences in company capabilities, transportation efficiency, and other issues.So how should one invest in semiconductors?First, it is essential to have a clear understanding of the cycle position of the industry. As mentioned earlier, the semiconductor cycle can be broken down into three nested cycles: the innovation cycle, the capacity cycle, and the inventory cycle. We can approach this from these three aspects to determine the current cycle position.Every super cycle in the semiconductor industry is driven by the emergence of disruptive innovations. Such technological advancements are often accompanied by the birth of killer applications, creating massive demand. For example, the launch of the iPhone 4 triggered a wave of smartphones and mobile internet, leading to a super cycle in the semiconductor industry lasting a decade.Similarly, ChatGPT and DeepSeek became global phenomena overnight. Although the downstream application scenarios for AI remain somewhat vague, if this indeed marks the beginning of a new super cycle, we are still in the early stages.If the innovation cycle represents the growth potential of semiconductors, then the capacity cycle reflects the manufacturing attributes of the semiconductor industry. The capacity cycle represents changes on the supply side; when supply is low and downstream demand begins to rise, it is an opportune time for investment.For the capacity cycle, we can track indicators such as wafer manufacturing capacity, wafer fab capacity utilization, capital expenditure, semiconductor equipment sales, orders on hand at wafer fabs, and the speed of capacity ramp-up to locate the stage of the capacity cycle.As for inventory, it is closer to the downstream demand side and more reflective of changes in demand. An important indicator for determining the semiconductor cycle position is the inventory levels of chip companies. When inventory rises, it is a strong signal of a downward cycle. Conversely, when inventory decreases, it indicates a recovery in demand. Additionally, we can assess the strength of downstream demand and the specific position of the inventory cycle through metrics such as inventory turnover days, inventory levels, semiconductor sales, and chip prices. In summary, we can analyze the innovation cycle, capacity cycle, and inventory cycle, and combine industry-related indicators to mutually verify which stage the industry is currently in.The semiconductor industry has widespread downstream applications, involving communications, computers, consumer electronics, automotive, and industrial sectors. In recent years, the semiconductor market has been driven by alternating demands from downstream terminal markets such as 5G, automotive electronics, and AI computing power. Due to varying levels of prosperity across different sub-sectors, there is also significant structural differentiation within the semiconductor industry.

In summary, we can analyze the innovation cycle, capacity cycle, and inventory cycle, and combine industry-related indicators to mutually verify which stage the industry is currently in.The semiconductor industry has widespread downstream applications, involving communications, computers, consumer electronics, automotive, and industrial sectors. In recent years, the semiconductor market has been driven by alternating demands from downstream terminal markets such as 5G, automotive electronics, and AI computing power. Due to varying levels of prosperity across different sub-sectors, there is also significant structural differentiation within the semiconductor industry. Since 2021, the lack of technological innovation in smartphones has dampened replacement demand, leading to longer replacement cycles and a continuous decline in smartphone shipments, which has also negatively impacted the consumer electronics sector.However, in stark contrast to the sluggish consumer electronics market, automotive-grade chips and power semiconductors related to photovoltaics have surged, driven by strong demand from the new energy market, with remarkable growth in related sub-sectors, significantly outperforming industry indices. The AI market in 2023 has been particularly notable, with U.S. companies like NVIDIA and AMD leading the Philadelphia Semiconductor Index to new highs, while the A-share semiconductor index has shown significant polarization.Therefore, when investing in semiconductors, it is crucial not only to pay attention to the overall prosperity of the industry but also to focus on the increasingly pronounced structural differentiation within the industry, making the exploration of alpha returns in sub-sectors particularly important.For the domestic semiconductor industry, domestic substitution is also an important long-term growth logic that cannot be ignored.Since 2018, the U.S. has progressively intensified sanctions against China’s semiconductor industry, gradually extending technology blockades to upstream sectors, affecting critical areas such as EDA, materials, and equipment.In this context, the importance of self-sufficiency in semiconductors is self-evident. Both policy support and downstream support for the domestic supply chain are continuously strengthening, and the process of domestic industrialization is rapidly advancing.Although the domestic semiconductor industry started late, its development speed in recent years has surpassed previous years. For instance, in the semiconductor equipment sector, revenue for domestic semiconductor equipment companies has increased from $5.65 billion in 2018 to $38.32 billion in 2023, with the localization rate rising from 6.16% to 18.25%. From January to November 2023, major domestic wafer fabs secured a total of 875 equipment contracts, with the proportion of domestic semiconductor equipment contracts reaching 47%.The high entry barriers for semiconductor equipment are not only due to technological levels. Changing suppliers poses significant potential risks for wafer fabs, such as stability of production lines, yield loss, raw material waste, and order losses, making it unlikely to consider other suppliers unless absolutely necessary.For domestic semiconductor equipment manufacturers, without orders or feedback from customers, there is no capacity to continue investing in R&D or product performance iterations, leading to a downward spiral of falling behind.The wave of domestic substitution began in 2019, and after years of effort, it has enabled the domestic semiconductor industry to achieve a breakthrough from 0 to 1, opening up markets for Chinese semiconductor companies. However, it is also important to recognize that while the localization process in the mid to low-end sectors is progressing rapidly, high-end sectors still require time to break through.

Since 2021, the lack of technological innovation in smartphones has dampened replacement demand, leading to longer replacement cycles and a continuous decline in smartphone shipments, which has also negatively impacted the consumer electronics sector.However, in stark contrast to the sluggish consumer electronics market, automotive-grade chips and power semiconductors related to photovoltaics have surged, driven by strong demand from the new energy market, with remarkable growth in related sub-sectors, significantly outperforming industry indices. The AI market in 2023 has been particularly notable, with U.S. companies like NVIDIA and AMD leading the Philadelphia Semiconductor Index to new highs, while the A-share semiconductor index has shown significant polarization.Therefore, when investing in semiconductors, it is crucial not only to pay attention to the overall prosperity of the industry but also to focus on the increasingly pronounced structural differentiation within the industry, making the exploration of alpha returns in sub-sectors particularly important.For the domestic semiconductor industry, domestic substitution is also an important long-term growth logic that cannot be ignored.Since 2018, the U.S. has progressively intensified sanctions against China’s semiconductor industry, gradually extending technology blockades to upstream sectors, affecting critical areas such as EDA, materials, and equipment.In this context, the importance of self-sufficiency in semiconductors is self-evident. Both policy support and downstream support for the domestic supply chain are continuously strengthening, and the process of domestic industrialization is rapidly advancing.Although the domestic semiconductor industry started late, its development speed in recent years has surpassed previous years. For instance, in the semiconductor equipment sector, revenue for domestic semiconductor equipment companies has increased from $5.65 billion in 2018 to $38.32 billion in 2023, with the localization rate rising from 6.16% to 18.25%. From January to November 2023, major domestic wafer fabs secured a total of 875 equipment contracts, with the proportion of domestic semiconductor equipment contracts reaching 47%.The high entry barriers for semiconductor equipment are not only due to technological levels. Changing suppliers poses significant potential risks for wafer fabs, such as stability of production lines, yield loss, raw material waste, and order losses, making it unlikely to consider other suppliers unless absolutely necessary.For domestic semiconductor equipment manufacturers, without orders or feedback from customers, there is no capacity to continue investing in R&D or product performance iterations, leading to a downward spiral of falling behind.The wave of domestic substitution began in 2019, and after years of effort, it has enabled the domestic semiconductor industry to achieve a breakthrough from 0 to 1, opening up markets for Chinese semiconductor companies. However, it is also important to recognize that while the localization process in the mid to low-end sectors is progressing rapidly, high-end sectors still require time to break through.