Oracle’s stock surged by36%, with a market value increase of1.78 trillion yuan. This astonishing performance not only shocked global investors but also revealed thatthe competition for AI computing power is shifting from general computing to dedicated chips.

On Wednesday, Eastern Time, American tech giant Oracle signed a massive computing power procurement contract withOpenAI, becoming one of the largest cloud contracts in global tech history.

Behind this major deal, an unstoppable trend is forming: driven by the U.S.-led large-scaleAI infrastructure investment and the accelerated construction of data centers by global tech giants, the global demand forAI computing power is continuously surging.

1.Oracle Ignites Market, New Opportunities for the Computing Power Industry

The details of the collaboration between Oracle andOpenAI are astonishing.OpenAI will procure4.5 gigawatts (GW) of computing power from Oracle (Note: Market rumors, currently no official source). This is equivalent to1/4 of the total current data center capacity in the U.S., or about4 million households’ annual electricity consumption.

This order directly positions Oracle as a core infrastructure provider forAI model training and provides long-term growth assurance for its cloud infrastructure business (OCI).

The company expectsOCI to maintain high double-digit growth, showcasing the enormous growth potential of theAI computing power market.

2.Why Does AI Computing Power NeedASICs?

AI computing power has always had two technical paths: one is the general path represented by NVIDIA’sGPUs, suitable for general high-performance computing; the other is the dedicated path represented byASICs custom chips.

GPUs excel at handling large-scale parallel computing tasks, but they face memory wall issues when processing large-scale matrix multiplications. In contrast,ASICs can solve this problem, and once mass-produced,ASICs will have a better cost-performance ratio.

Broadcom’s latest financial report fully demonstrates the strong demand forASIC chips. In the third quarter of fiscal year 2025, the company achieved revenue of15.952 billion USD, a year-on-year increase of22%, withAI business revenue reaching5.2 billion, a year-on-year increase of63%.

3.The Three Camps of the ASIC Ecosystem

Currently, the ASIC field has formed three major camps: first is the self-research faction represented by Google, which is one of the largestASIC designers and users globally. Its next-generationTPU Ironwood has seen a performance leap, competing with NVIDIA’sB200 series chips.

Secondly, there are solution providers represented by Broadcom, which has launched a new generation of high-speed switching chipsTomahawk6 (102TB), which can reduce the network architecture from three layers to two layers under the same computing cluster scale, significantly reducing latency and power consumption.

Finally, NVIDIA itself is transforming. In the face of competition from Google’sTPUs and otherASICs, NVIDIA has also begun to launch inference-specific chips, expanding from a “training leader” to a “dual leader in training and inference”.

4.The Rise of ASICs Brings Industrial Opportunities

The rapid development ofASICs is driving innovation and growth across multiple industrial chain links. Optical modules are iterating to800G and1.6T, with Lightcounting predicting a global optical module market CAGR of 22% from 2024 to 2029, exceeding37 billion USD by 2029.

OCS (Optical Circuit Switch) has become a new solution for large-scale data centers. Compared to electrical switches,OCS does not require optical-electrical signal conversion and corresponding data packet processing, significantly reducing latency and power consumption.

There is a surge in demand for high-end materials, asAI servers are shifting to56+ layer high-density boards, with materials upgrading fromM8 toM9, increasing the value of a single rack by30%.

Liquid cooling technology, as a key path to reduce data center energy consumption, is rapidly penetrating the market. AsAI computing power density continues to rise, traditional air cooling can no longer meet heat dissipation needs, and liquid cooling is becoming a standard rather than an option.

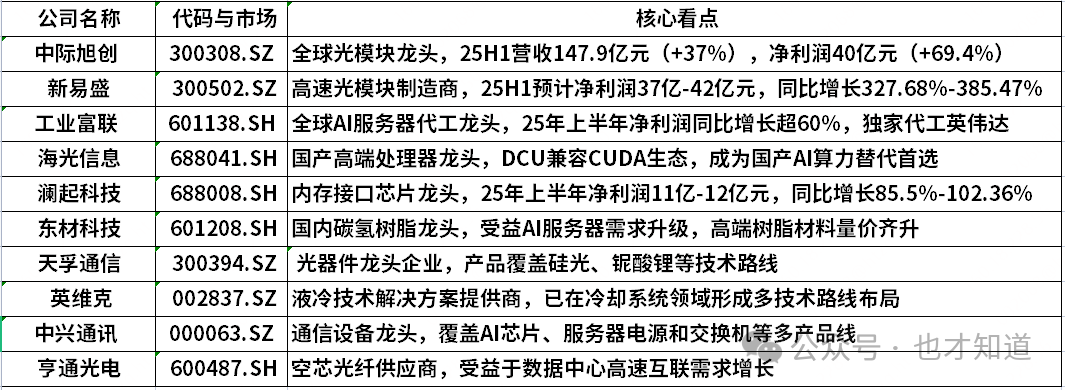

5.Overview of Related Listed Companies

Below is an overview of listed companies related toAI computing power andASICs in the A-share and Hong Kong stock markets:

6.Investment Logic and Risk Warning

The second phase of AI computing power development is opening, characterized by a shift from “general” to “dedicated” (GPU -> ASIC), and from “hardware computing power” to “ecosystem + efficiency” (CUDA ecosystem vs TPU and other open ecosystems).

Investment opportunities are also shifting from “single core” to “full industrial chain diffusion” (from chip design to materials, packaging, cooling, connectivity, etc.).

It is important to note that investing in the AI computing power field also carries certain risks: AI development may not meet expectations, industry competition may intensify, Sino-U.S. trade frictions may have impacts, and capacity construction may not meet expectations.

Investors should focus on companies with strong technical capabilities, that have entered the global supply chain system, and possess rapid response and adaptation capabilities.

As AI applications extend from training to inference scenarios, the market space forASIC chips is expected to continue to expand.

Broadcom’s CEO, Chen Fuyang, pointed out that customer investments inAI semiconductors will drive AI revenue to accelerate to6.2 billion in the fourth quarter, with full-year revenue expected to reach17.4 billion.

In this shifting market, by2028, the shipment ofASICs is expected to exceed that ofGPUs. Companies that have laid out theASIC industrial chain in advance will gain an advantage in the second half of this computing power battle.

#AI computing power #ASIC chips # optical modules # liquid cooling technology #PCB #AI servers # data centers # investment strategy

AI servers are igniting high-end copper foil demand, and domestic alternatives are timely!

Technology leads the liquidity bull market, can AI + the main line continue?

Explosive buying of 6.4 billion! Behind the surge in Chemical ETF (159870) shares, funding sentiment is quietly changing.

“Risk Warning” The information regarding listed companies in this article is based on publicly available data analysis, aimed at providing readers with reference dimensions, and does not constitute any form of investment advice or trading basis. The market carries risks, and investment requires caution. The views expressed in this article only represent the logic of information organization, and the historical performance of individual stocks does not represent future trends. Readers should make prudent decisions based on their risk tolerance and consult professional institutions if necessary.