Pengding Holdings: GlobalPCB Leader’s Breakthrough and Growth

1. Introduction

Printed Circuit Boards (PCB) are core components of the electronic information industry. Pengding Holdings (A Share Code: 002938) is a global leader in PCB, occupying an important position in the industry due to its technological, production capacity, and customer advantages. This article analyzes its operational status and potential from multiple dimensions, providing references for relevant parties.

2. Company Overview Overview

2.1Development History

In 1999, the predecessor, Fokai Precision Components (Shenzhen) Co., Ltd., was established; in 2017, it was fully transformed into a joint-stock company; in 2018, it was listed on the Shenzhen Stock Exchange. After going public, it accelerated its global layout, and by the end of 2024, it will have established production or service bases in mainland China, Taiwan, Singapore, India, Thailand, etc., forming a global network of “R&D–Production–Sales”.

2.2Organizational Structure

It adopts a “Shareholders’ Meeting–Board of Directors–Supervisory Board–Senior Management” standardized governance structure, with five specialized committees under the board of directors. The management team has clear divisions of labor, and the business layer is organized into departments based on “R&D–Procurement–Production–Sales”, with 17 subsidiaries managed uniformly through the “Subsidiary Management Measures”.

2.3Corporate Culture and Core Team

Corporate Culture: With the mission of “Developing Technology for the Benefit of Humanity, Advancing Environmental Protection for a Better Earth”, it practices the values of “Integrity, Responsibility, Innovation, Excellence, and Benefiting Others”, and promotes the “Pengding Seven Greens” concept, emphasizing R&D and employee development. In 2024, R&D investment is expected to reach 2.324 billion yuan, with a total of 2642 patents.

The core team is centered around Chairman Shen Qingfang, who has over 40 years of cross-field management experience. The average tenure of the core management team exceeds 20 years, covering multiple fields, ensuring the implementation of strategies.

3. Industry Analysis

3. Industry Analysis

3.1Industry Status

In 2024, the global PCB market value is expected to reach 73.565 billion USD (+5.8%), with China accounting for over 50%. Pengding’s revenue is expected to be 35.14 billion yuan, maintaining its position as the global leader for eight consecutive years. In terms of demand, traditional consumer electronics are recovering, while emerging fields such as AI servers and new energy vehicles are booming; technologically, high-end products such as HDI, SLP, and FPC along with technologies like fine lines and micro-holes are becoming the core of competition.

3.2Competitive Landscape

The top 30 global PCB manufacturers hold a market share of 67.6%, with intense competition among leading companies. The domestic market is divided into three tiers, with Pengding in the first tier. The industry has three major barriers to entry: technology, customers, and capital.

3.3Development Trends

In the next five years, AI will drive the demand for the entire PCB supply chain, with automotive electronics becoming the second growth curve. Global PCB companies are accelerating their production capacity layout in “China+Southeast Asia”, with Pengding’s Thailand base expected to start production in May 2025.

4. Business Analysis

4. Business Analysis

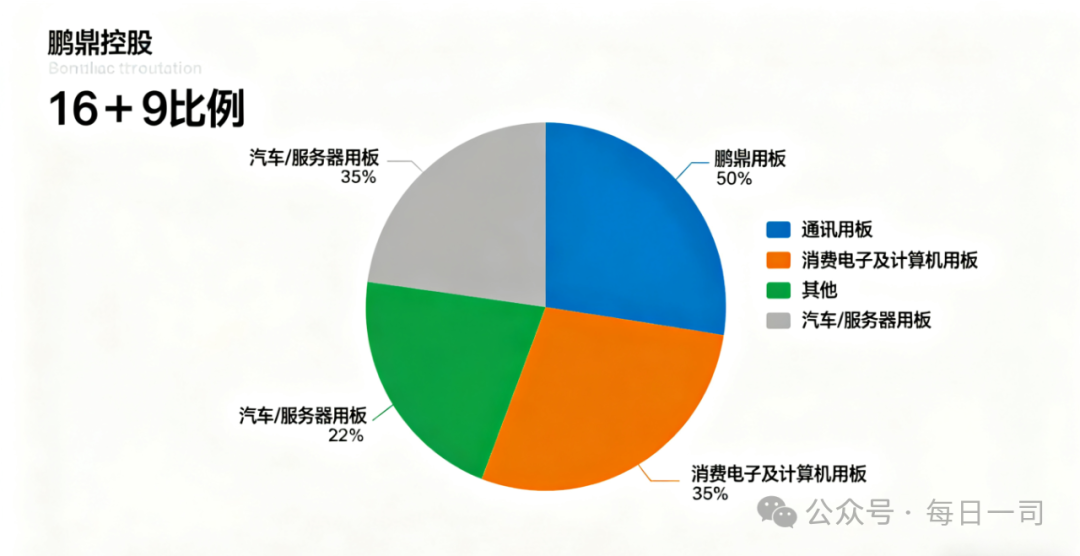

4.1Core Business Segments (2024)

Communication Boards: Revenue is expected to be 24.236 billion yuan (accounting for 68.97%), focusing on smartphones, with a global market share of over 20% in smartphone FPCs, and revenue growth of +3.08%.

Consumer Electronics and Computer Boards: Revenue is expected to be 9.754 billion yuan (accounting for 27.76%), covering tablets, laptops, etc., with revenue growth of +22.30%, and AI-related products accounting for over 45% of the total.

Automotive/Server Boards and Others: Revenue is expected to be 1.025 billion yuan (accounting for 2.92%), involving automotive radar boards and AI server boards, with revenue growth of +90.34%, the fastest growth rate.

4.2Business Model and Strategy

Model: Customized production (rapid prototyping + bulk delivery, with a capacity utilization rate of over 90%), direct sales (the top five customers account for 91.23%), and centralized procurement (the top five suppliers account for 29.29%).

Strategy: Product upgrades (focusing on high value-added products), market expansion (extending from consumer electronics to multiple fields), and technological R&D (focusing on “new materials, new processes, new equipment”).

5. Financial Analysis

5.1Historical Financial Data (2021-2024, unit: billion yuan)

|

Indicator |

2024 Year |

2023 Year |

2022 Year |

2021 Year |

2024 Year-on-Year Growth Rate |

|

Total Revenue |

35.14 |

32.066 |

36.211 |

33.310 |

9.59% |

|

Net Profit Attributable to Shareholders |

3.620 |

3.287 |

5.012 |

3.317 |

10.14% |

|

Net Cash Flow from Operating Activities |

7.082 |

7.969 |

10.957 |

— |

-11.12% |

|

In 2024, revenue and profit are expected to recover, with good cash flow quality. |

|

|

|

|

|

5.2Financial Indicators (2024)

Profitability: Gross margin 20.76% (2.26 percentage points higher than the industry), net margin 10.30%, and weighted ROE 11.73% (1.63 percentage points higher than the industry).

Operational Capability: Days sales outstanding 62, inventory turnover days 42, total asset turnover 0.81 times, all better than the industry average.

Debt Repayment Ability: Debt-to-asset ratio 27.44% (low in the industry), current ratio 2.11, quick ratio 1.80, and cash and cash equivalents 13.497 billion yuan, indicating sufficient debt repayment ability.

5.3Financial Outlook (2025)

Expected revenue is between 39.3-40.4 billion (+12%-15%), gross margin 21%-22%, net margin 10.5%-11%, and net cash flow from operating activities 7.5-8.0 billion, with attention needed on consumer electronics demand and raw material price risks.

6. Market Performance

6.1Stock Price and Valuation

6.1Stock Price and Valuation

In 2024, the stock price fluctuated and rebounded, closing at 32.6 yuan at the end of the year (+26.1%), outperforming the market. The dynamic PE at year-end was 21.5 times, static PE was 18.8 times, lower than peers, with a PEG of 2.24 (lower than the industry average of 2.8), indicating a margin of safety in valuation.

6.2Shareholder Structure

The controlling shareholder, Zhendin Holdings, holds a total of 71.88% of the shares, indicating stable equity; institutional holdings account for 15.3% (+3.2 percentage points), with a decrease in the number of shareholders and an increase in share concentration.

6.3Market Value Management

In 2024, the company established a “Market Value Management System”, with high dividends (dividend rate of 64%), strengthening investor communication, and establishing a market value monitoring mechanism to maintain company value.

7. Risks and Challenges

7. Risks and Challenges

Industry and Market: Fluctuations in consumer electronics demand, high customer concentration (the largest customer accounts for 81.94%), and intensified industry competition.

Operations and Management: Fluctuations in raw material prices, risks in capacity construction ramp-up, and overseas operations (exchange rate, policy) risks.

Technology and Policy: Risks of technological iteration, international trade policy risks, and environmental policy risks.

8. Conclusion and Recommendations

8.1Conclusion

Pengding’s industry position is solid, with AI terminals, automotive electronics, and AI server PCBs becoming growth engines; the financials are robust, with strong risk resistance; despite risks, the strategic layout has development potential.

8.2Recommendations

For the company: Accelerate customer and business diversification, optimize capacity and supply chain, and strengthen R&D and environmental investment.

For investors: Pay long-term attention to the growth rate of AI products and the progress of production capacity in Thailand, and invest during dips; short-term focus on orders during the consumer electronics peak season and raw material prices, seizing opportunities while being cautious of risks and diversifying investments.

Risk Warning: Consumer electronics demand may fall short of expectations, and rising prices of raw materials such as copper foil may impact profits.