This article is brought to you by Semiconductor Industry Insights (ID: ICViews).

This article is brought to you by Semiconductor Industry Insights (ID: ICViews).

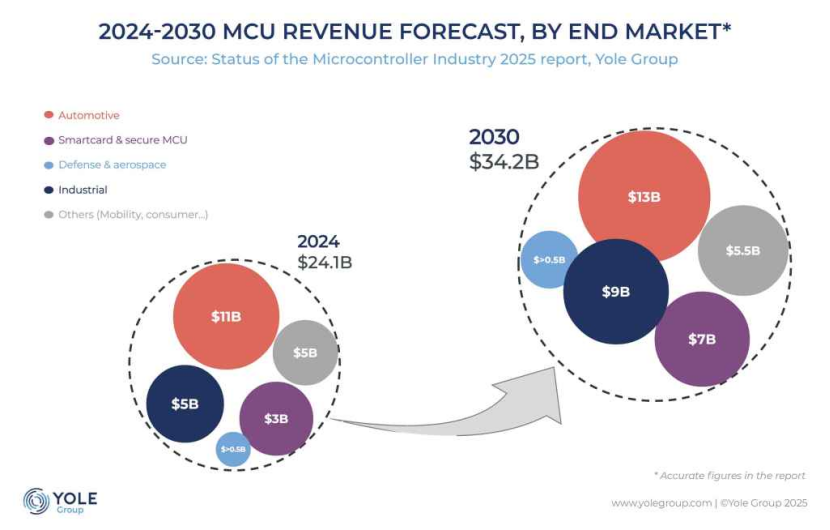

The automotive market will become the largest revenue source for MCUs.

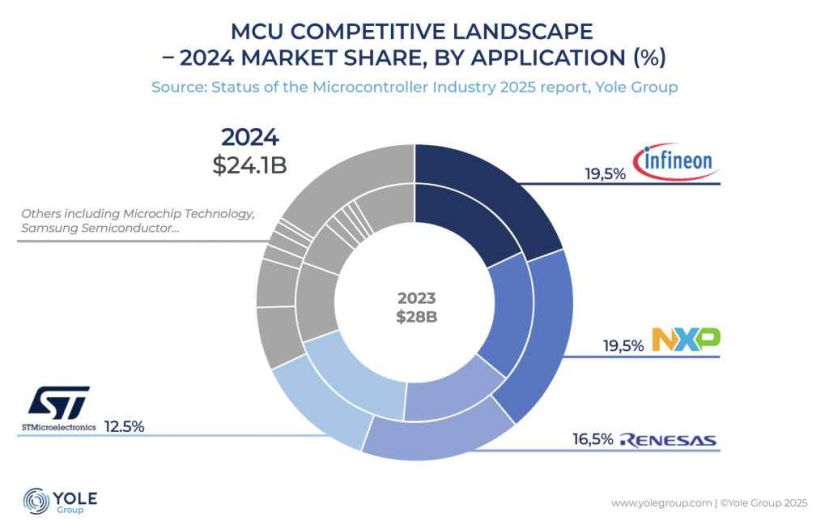

Recently, Yole Group released its annual “Microcontroller Industry Status Report,” which shows that the MCU market continues to expand into automotive, industrial, smart cards and security, defense, and consumer electronics sectors.

In the market landscape for MCUs in 2024,Infineon will have a market share of 19.5%, NXP will have a market share of 16.5%,Renesas will have a market share of 16.5%, and STMicroelectronics will have a market share of 12.5%.

The automotive industry remains the most influential category, growing at a compound annual growth rate of 3%, driven by the transition to domain and zonal control, ADAS intelligence, cybersecurity, and electrification architectures. Yole believes that while the automotive sector is a relatively small market in terms of sales, its high semiconductor output, high average selling prices, and continuous technological advancements make it a uniquely interesting market and the largest revenue source for MCUs.

The industrial and defense application sectors also show strong growth momentum, with a compound annual growth rate approaching 9%, while the smart card and security card sectors stand out with a compound annual growth rate of 13.5%, expected to reach approximately $7 billion by 2030.

Despite these advancements, the market still faces ongoing supply chain uncertainties. Geopolitical conflicts, U.S. trade restrictions, tariffs, sanctions, and government interventions create a complex environment for forecasting and production planning. Price trends peaked during the supply shortages caused by the pandemic and have now stabilized and gradually declined, rather than returning to pre-pandemic levels. By the end of 2024, the inventory reductions by original equipment manufacturers (OEMs) will also trigger a significant temporary decline.

Artificial intelligence capabilities are gradually becoming a key differentiating advantage. With the TinyML framework enabling resource-constrained processors and architectures (such as Arm’s M55/M85 or AI-accelerated RISC-V cores) to support machine learning, these architectures are increasingly being adopted by mainstream suppliers. It is expected that by 2028, AI at the MCU level will cover at least 10% of MCUs. Meanwhile, the automotive industry continues to see a growing demand for high-reliability MCUs to meet safety requirements across various systems, including steering, braking, propulsion, communication, and energy management systems, in compliance with ISO 26262 and AEC-Q100 standards.

Electrification further accelerates the adoption of MCUs (smart control units), especially in hybrid platforms that require coordination between internal combustion engines and electric power systems. Beyond power systems, consumers also expect full vehicle electrification—from digital lighting to smart seating and cockpit experiences—which will further drive the widespread application of MCUs.

Yole believes that the expansion of artificial intelligence, vehicle electrification, and the shift towards domain and zonal architectures are reshaping the MCU landscape. Coupled with geopolitical pressures and supply chain restructuring, these factors present both risks and opportunities for global suppliers.

MCU Giants: Financial Reports Comparison

MCU Giants: Financial Reports Comparison

Infineon’s fiscal report for 2025 shows that the company achieved revenue of €14.662 billion, a slight decline of 2% year-on-year. Despite the decline in sales and profits, CEO Jochen Hanebeck believes the company’s performance meets expectations: “In 2025, our performance was affected by multiple factors including macroeconomic slowdown and geopolitical issues. Customers will be more cautious in 2026, providing only short-term demand orders, and we expect moderate growth in the coming year.”

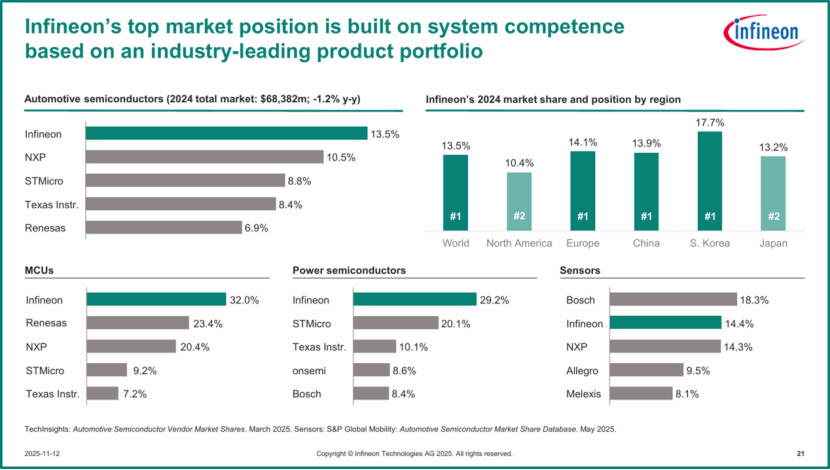

Infineon’s report shows that it holds an undisputed leading position in the automotive semiconductor sector, with a global market share of 13.5%, surpassing NXP, STMicroelectronics, Texas Instruments, and Renesas Electronics.

In terms of segments, Infineon holds nearly one-third of the automotive microcontroller MCU market share, with a 29.2% share in the power semiconductor sector, significantly ahead of competitors. In the sensor field, it ranks second, only behind Bosch of Germany.

Despite the decline in sales and profits, CEO Jochen Hanebeck still believes the company’s performance meets expectations: “In 2025, our performance was affected by multiple factors including macroeconomic slowdown and geopolitical issues. Customers will be more cautious in 2026, providing only short-term demand orders, and we expect moderate growth in the coming year.”

STMicroelectronics reported net revenue of $3.19 billion in the third quarter, with a gross margin of 33.2%; operating profit of $180 million, which includes $37 million in asset impairment, restructuring costs, and other related exit costs; net profit of $237 million.

NXP reported total revenue of $3.173 billion in the third quarter of 2025, a year-on-year decline of 2% and a quarter-on-quarter increase of 8%; core automotive business grew by 6% quarter-on-quarter, ending five consecutive quarters of decline.

In the third quarter of 2025, NXP’s revenue reached $3.173 billion, slightly above the market expectation of $3.16 billion, demonstrating resilience in the automotive and industrial IoT chip markets. Although overall revenue declined by 2% year-on-year, it rebounded by 8% quarter-on-quarter, with a gross margin maintained at around 57%, and GAAP net profit of $631 million, a quarter-on-quarter increase of 42%. The automotive business once again became the core of performance this quarter, contributing revenue of $1.837 billion, accounting for nearly 60% of total revenue, with a quarter-on-quarter increase of 6% and year-on-year flat.

The U.S. has increased tariffs on automotive and parts imports, prompting automakers to accelerate local production, which has driven demand for automotive MCUs, power management, in-vehicle networking, and smart driving-related chips, benefiting significantly from the new round of automotive electronics structural upgrades in North America and Europe.

*Disclaimer: This article is the original work of the author. The content reflects their personal views, and our reposting is solely for sharing and discussion purposes, not representing our endorsement or agreement. If there are any objections, please contact us.

The “2025 AI PC Industry Research Report” has been released

To help players across the hardware, software, model, and terminal layers in the PC field better understand the current state and future trends of the AI PC industry, Semiconductor Industry Insights has released the “2025 AI PC Industry Research Report.”The report mainly analyzes the macro environment of the AI PC industry, the AI PC industry chain, user research analysis, product evaluations, and future development trends.The AI PC user research covers first-tier cities in China such as Beijing, Shanghai, and Shenzhen, collecting over a thousand valid samples from end users and store sales personnel. The research includes user demographics, awareness of AI PCs, product feature preferences, and judgments on future industry development trends.The AI PC product evaluations focus on Lenovo ThinkPad X9 14 (Intel) and Lenovo Xiaoxin Pro16c AKP10 (AMD), analyzing dimensions including comparisons of different quantization sizes of the same model, comparisons of different parameter scale models of the same model, and comparisons of different inference devices on the same machine.

Report acquisition:1.

Report price: printed version 599 yuan/copy

2.Purchase method: Please scan the code to fill out the report purchase intention form

3.Report inquiries:

WeChat IDicviews2 orJoy8432211

Report directory: