Click the “blue text” above to follow for more exciting content.

This article contains a total of 789 words, and it takes about 2 minutes to read.

The global FPGA market can be roughly divided into three categories based on process technology:

1) >90nm, including 0.25/0.22 μm, 0.18/0.15 μm, and 0.13 μm, mainly used for high-reliability aerospace applications;

2) 20-90 nm, including 20/22 nm, 28 nm, 40/45 nm, 55/60/65 nm, and 90 nm. Among these, the defense & aerospace (A&D) sector has demand for 28-90 nm FPGAs, the automotive market mainly focuses on 28-65 nm FPGAs, consumer electronics commonly use 28nm or 45nm FPGAs, and telecommunications primarily use 28nm FPGAs on the air interface;

3) ≤16nm, including 16 nm, 14 nm, 10 nm, and 7 nm. Among these, 14/16nm FPGAs are mainly applied in baseband units and wired networks in the telecommunications field, laser radar in the automotive sector, security and instrumentation in industrial applications, as well as in medical imaging, ASIC verification, multimedia & broadcasting, and intensive visual processing and communication scenarios in defense & aerospace. Currently, 7nm FPGAs are mainly used in data center acceleration computing.

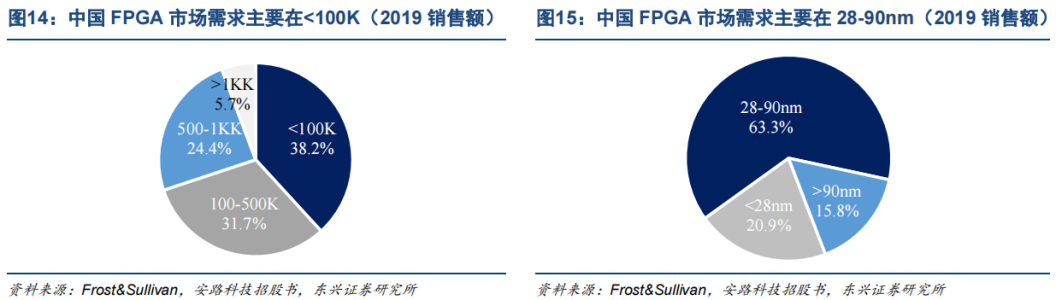

At present, the mainstream demand for FPGAs in China is mostly concentrated in the mature market with a process technology of 28nm-90nm and a logic unit count of less than 500K. According to Frost & Sullivan data, in 2019, based on sales revenue, FPGAs with less than 100K logic units accounted for 38.2% of the market share, FPGAs with 100K-500K logic units accounted for 31.7%, and FPGAs with less than 500K in total accounted for nearly 70% of the market. In terms of process technology, over 60% of the market is for 28-90nm FPGAs. For domestic manufacturers, 28nm is the market that needs to be captured the most.

Nevertheless, the global FPGA process is transitioning to 16nm, as the 16nm process is considered essential for gaining a competitive advantage in the next 5-10 years. The advantages of 14/16nm FPGAs lie in their ability to achieve larger capacity and higher performance at the same power consumption, or smaller power consumption and size at the same capacity. We see that the global FPGA market is migrating towards 16nm and more advanced processes. Marketsandmarkets predicts that by 2028, the market share of 20-90nm FPGAs will decrease from 49% in 2019 to 46%, while the share of ≤16nm FPGAs will increase from 36% to 44%, with a six-year compound growth rate of 17%, higher than the 10% for 20-90nm FPGAs.

Risk Warning:This content only represents the analysis, speculation, and judgment of the research team, and is published here solely for the purpose of conveying information, not as a basis for specific investment targets. Investment carries risks; please proceed with caution!Copyright Statement:This content is copyrighted by the original party or author. If reproduced, please indicate the source and author, retain the original title and ensure the integrity of the article content, and bear legal responsibilities for copyright and other issues.

END