For the report, please contact customer service or scan the code to obtain more reports.

1. Microdisplay technology drives incremental market growth, with a compound annual growth rate expected to exceed 20%

The popularity of consumer electronics such as televisions, IT products, and smartphones has led to significant advancements in display technology. However, with rapid capacity expansion and faster generational shifts, the traditional consumer electronics display sector has entered a phase of stock competition. Meanwhile, emerging application fields represented by VR and AR are rapidly rising, leading to a surge in demand for high-resolution, small-sized, low-power near-eye display technologies. Coupled with the rapid development of the semiconductor industry, microdisplay technology is gradually being pushed to the forefront of future development, forming an incremental market.

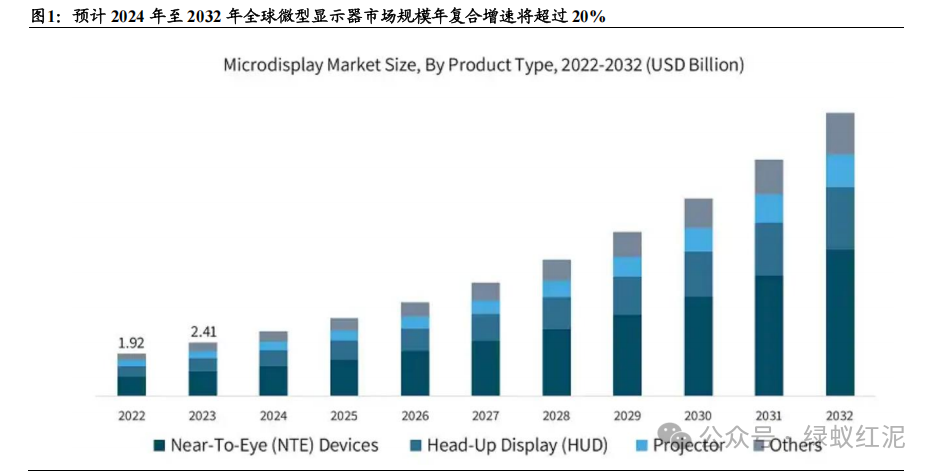

The principle of microdisplay lies in the combination of semiconductor processes and display technology. According to GMI data, the market size in 2023 is projected to be $2.41 billion, with a compound annual growth rate expected to exceed 20% from 2024 to 2032. Among these, the near-eye (NTE) device segment occupies the largest market share, accounting for over 45% of revenue. This category of products is widely used in AR/VR headsets, electronic viewfinders, smart glasses, helmet displays, etc. Due to their high pixel density, low power consumption, and backlight-free design, they are favored in scenarios requiring immersive experiences and portable use. Particularly in fields such as gaming, remote collaboration, education, and military tactical information display, near-eye displays have become the core visual interaction method, driving numerous enterprises and capital into this sector. Head-up displays (HUD) represent the second-largest segment. Currently, many automotive manufacturers are integrating OLED microdisplay HUDs into mid-to-high-end models, along with AR-assisted driving and night vision systems, creating new user interaction interfaces.

2. Different microdisplay technologies have their own advantages and disadvantages, with overlapping application scenarios often leading to competition

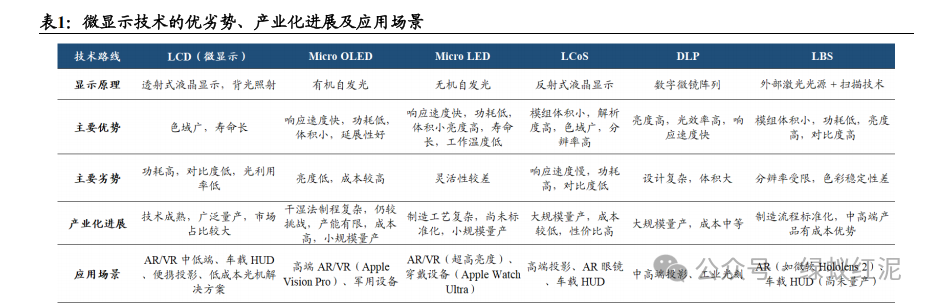

From a technical perspective, we categorize microdisplay technologies into two types: one type includes technologies such as LCD, Micro OLED, and Micro LED, which are based on self-emission or transmission/projection principles, primarily dominated by panel manufacturers; the other type includes technologies such as LCoS, DLP, and LBS, which are based on reflection or scanning principles for projection, mainly provided by chip manufacturers or optical device manufacturers.

Although these two types of microdisplay technologies differ in core principles and leading manufacturers, there is significant overlap and competition in several cutting-edge application fields.

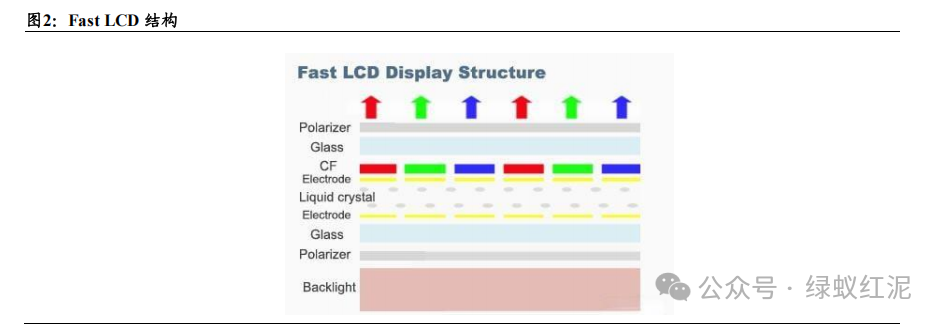

2.1. Fast LCD combined with Mini LED backlighting significantly enhances the application effectiveness of LCD in the microdisplay field

LCD (Liquid Crystal Display) manufacturing technology is mature and cost-effective, widely used not only in large screens but also in the microdisplay field. As near-eye display devices pursue higher response speeds and refresh rates, LCD microdisplay technology is continuously being optimized. For instance, Fast LCD technology employs new liquid crystal materials (ferroelectric liquid crystal materials) and ultra-fast driving technology to effectively enhance refresh rates while maintaining high production stability and yield, balancing performance and cost-effectiveness. When combined with Mini LED backlighting technology, it can significantly improve the display performance of Fast LCD. For example, in VR headsets, the cost ratios for Fast-LCD (Fresnel lens, mid-range configuration), Fast-LCD (Pancake lens, mid-range configuration), Fast-LCD (Mini LED backlight + Pancake lens, high-end configuration), and Micro OLED (Pancake lens, high-end configuration) are approximately 1:2.3:2.9:4.5.

2.2. Micro OLED is in the early stages of rapid development, with uncertainties in its technical path

OLED is the third generation of display technology developed after LCD, with its core relying on activating organic semiconductors and luminescent materials through an electric field to achieve light emission, distinguishing it from LCD which requires backlighting. Micro OLED operates on principles similar to OLED, also based on organic light-emitting diodes, capable of independent light emission per pixel, providing high contrast, wide color gamut, and fast response. The difference is that Micro OLED integrates CMOS technology, using single-crystal silicon substrates instead of traditional glass substrates, and integrates the driving circuit onto the substrate, significantly reducing the screen’s volume and weight. By applying semiconductor technology, Micro OLED can reduce pixel spacing to a few micrometers, greatly enhancing the pixel density of microdisplays.

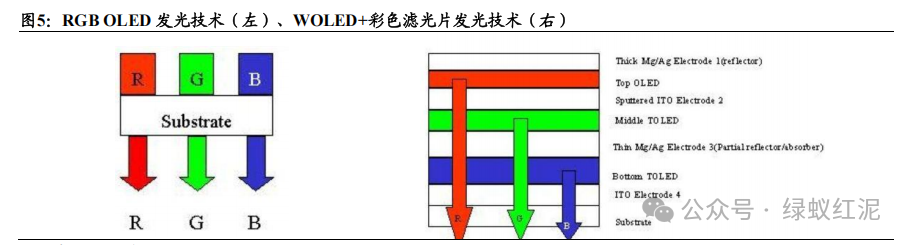

In traditional AMOLED manufacturing processes, there are mainly two types: one represented by LG that uses WOLED (White OLED) technology, where the light-emitting layer emits white light, which is then filtered through color filters to emit different colors, primarily used in medium to large panels such as televisions; while other manufacturers, including Samsung and domestic panel manufacturers, mainly adopt RGB OLED technology, which uses FMM precision metal optical masks for deposition, allowing pixel points to emit red, green, and blue primary colors, which are then combined to produce other colors, primarily used in small to medium panels such as smartphones.

RGB OLED offers extreme color accuracy, high contrast, and high pixel density, resulting in superior display performance. However, due to the extremely small pixels of Micro OLED, the more precise FMM and deposition equipment required for the RGB technology route (with the main market supplier being Sunic) are scarce. Therefore, the mainstream light-emitting solution for Micro OLED currently relies on the first type, WOLED + color filters, but the color filters reduce light transmittance, making brightness the main drawback of this solution.

2.3. Mass transfer technology is the biggest bottleneck facing the commercialization of Micro LED

Micro OLED has become the preferred choice for near-eye devices due to its ultra-high PPI, high technological maturity, and low power consumption. However, OLED organic materials are prone to degradation and have limited lifespan, while Micro LED performs better in durability, brightness, contrast, and flexible splicing, effectively addressing the main shortcomings of Micro OLED, and is regarded as the ultimate future display technology.

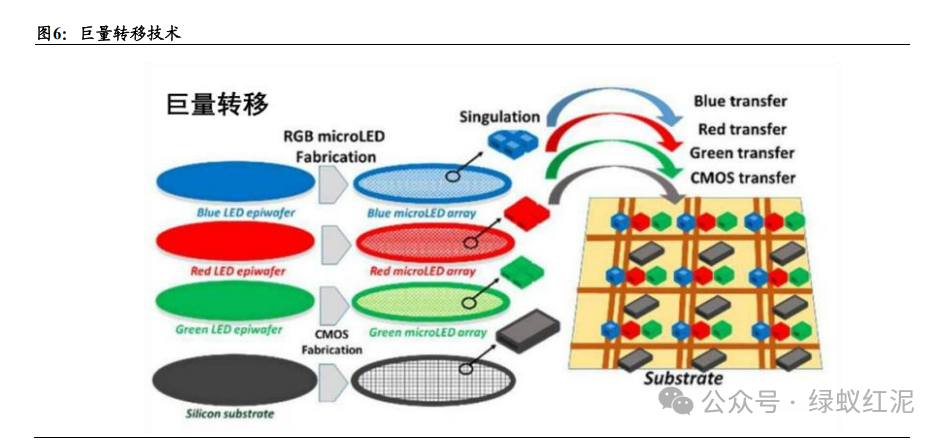

Micro-LED can essentially be seen as scaling down LED devices by hundreds to thousands of times, allowing for the integration of more and smaller Micro-LEDs within the same area of a chip. The industrial bottleneck for achieving Micro-LED lies in the “mass transfer” technology.

The core logic of mass transfer technology is to use specific equipment and processes to pick and transfer red (R), green (G), and blue (B) micron-scale Micro LED chips from the native substrate (or intermediate carrier) to the designated pixel positions on the target driving backplane (such as TFT or CMOS) with extremely high speed and precision, ultimately completing the bonding.

2.4. LCoS technology has high maturity and has achieved mass production in AR/VR, HUD, and other markets

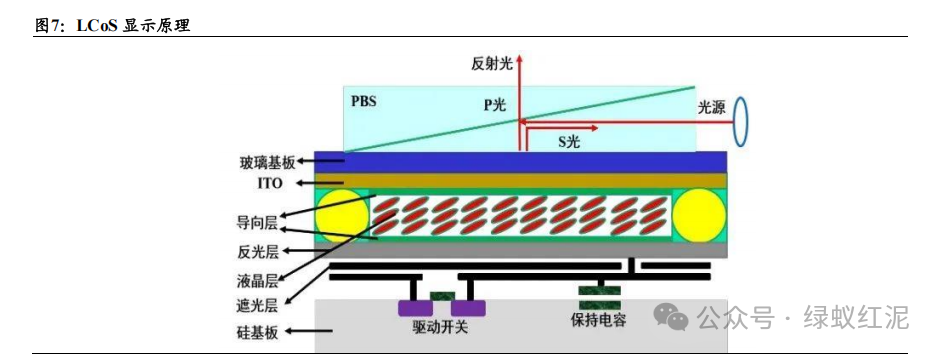

In addition to Fast LCD, LCoS (Liquid Crystal on Silicon) has also become one of the important technological directions in the microdisplay field. LCoS is a new reflective display technology that organically combines LCD with CMOS integrated circuits, using single-crystal silicon as the substrate to integrate driving circuits and other components, and modulating light through a liquid crystal layer to present images, offering high resolution, high contrast, and low power consumption advantages. It is widely used in HUD, projection, AR/VR, etc., such as the 2K automotive-grade LCoS AR-HUD equipped in the AITO M9, and Meta’s upcoming consumer-grade AR glasses—Meta Celeste.

2.5. DLP is primarily applied in the projector market

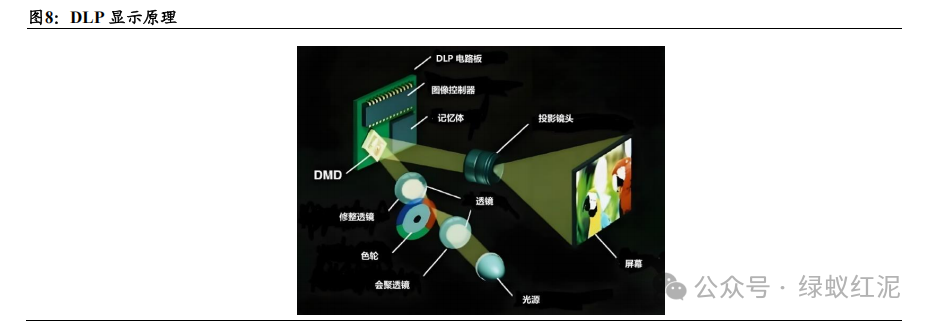

DLP (Digital Light Processing) is a display technology developed by Texas Instruments in 1987 based on micro-electromechanical systems (MEMS), where the core controls light reflection to generate images through digital micromirror devices (DMD).

The DLP system consists of DMD (digital micromirror device), DLP display control chips, and PMIC power management chips, with the DMD chip being the core of the DLP system, composed of a matrix of micromirrors, each of which can represent one or more pixels on the display. When incident light is projected onto the micromirrors, they tilt under the drive of digital signals; micromirrors in the projection state reflect light onto the screen, while those in the off state absorb light, with the DMD chip generating images through the switching of these two states.

DLP technology occupies a dominant position in high-end projection and industrial fields due to its high reliability, extreme contrast, and fast response. With advancements in laser light sources and MEMS technology, DLP is expanding from traditional displays into emerging fields such as AR and 3D printing, and may further break application boundaries through smaller pixel sizes and AI-driven light control technologies in the future.

2.6. LBS combines advantages such as small size, high efficiency, high color gamut, and high contrast

LBS (Laser Beam Scanning) uses RGB lasers as the light source, paired with MEMS for scanning imaging. It combines advantages such as small size, high efficiency, high color gamut, and high contrast, making it highly favored in AR/VR glasses and automotive AR-HUD, both of which have stringent requirements for size, brightness, and power consumption.

3. LCD/Micro OLED/Micro LED are the mainstream technology routes in the VR and AR markets

Near-eye displays essentially render light field information to the human eye through display devices placed within the non-foveal distance of the eye, thereby reconstructing virtual scenes in front of the eyes. The core includes two important elements: microdisplay devices and optical devices. Among the microdisplay devices, various technologies such as LCD/Micro OLED/Micro LED/LCoS/DLP/LBS are flourishing, but from the perspective of the downstream VR/AR market, LCD/Micro OLED/Micro LED remain the mainstream.

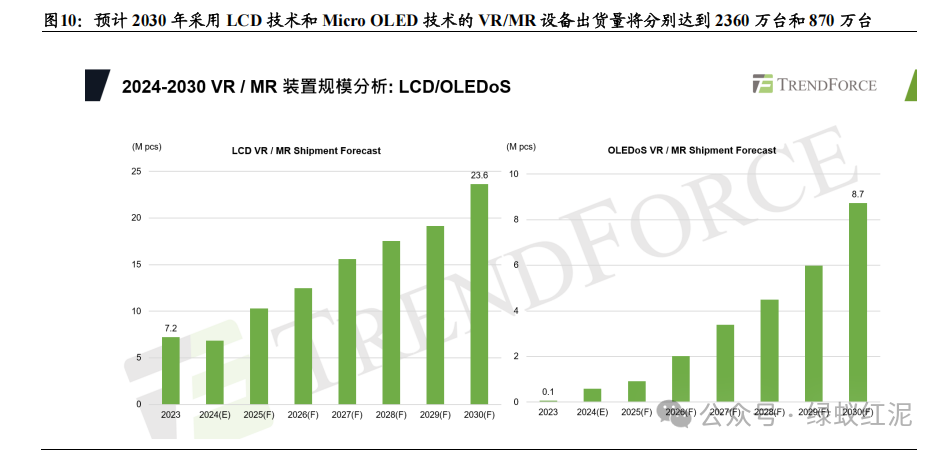

From the perspective of VR products, LCD technology offers better cost-effectiveness and currently holds a dominant position, while Micro OLED technology has established its place in the high-end VR market driven by Apple, with increasing investments and layouts from domestic and foreign manufacturers in the Micro OLED field, leading to more VR products featuring Micro OLED technology in the future. However, despite the short-term impact of Micro OLED technology products on LCD technology, in the long run, VR products using LCD technology still possess strong competitiveness in the mid-to-low-end market. Trend Force estimates that by 2030, the shipment volumes of VR/MR devices using LCD technology and Micro OLED technology will reach 23.6 million units and 8.7 million units, respectively.

4. Key companies in the microdisplay field domestically and internationally

(1) Samsung, South Korea: Micro OLED, Micro LED

In May 2023, Samsung acquired the Micro OLED microdisplay company eMagin for $218 million, accelerating its layout in Micro OLED. eMagin, established in 1996, primarily develops RGB Micro OLED solutions, serving world-class customers in military, consumer, medical, and industrial markets in the fields of AR/VR and near-eye displays, and is also a supplier to the U.S. military. Since 2001, eMagin’s Micro OLED displays have been and will continue to be used in AR/VR devices, aircraft helmets, head-up display systems, thermal imagers, night vision goggles, future weapon systems, and various other applications.

By 2025, Samsung Electronics plans to transfer its silicon-based Micro LED development capabilities to Samsung Display while completely shutting down its LED business. This decision marks a significant strategic adjustment for Samsung Electronics in the display technology field, accelerating its entry into the Micro LED and AR display sectors.

(2) LGD, South Korea: Micro OLED

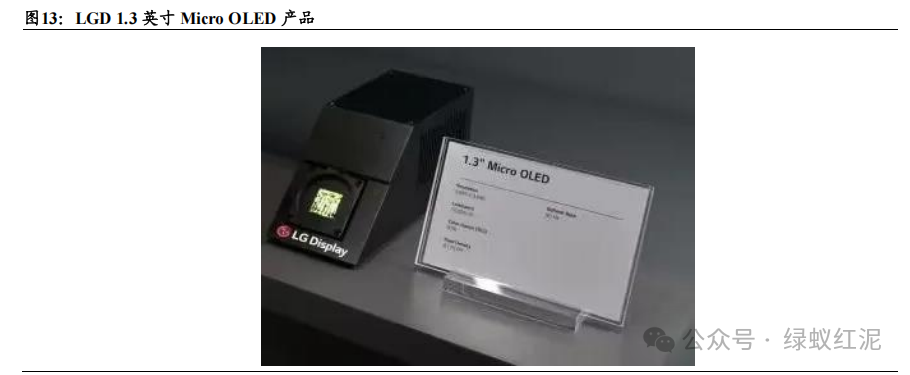

At the 2024 SID exhibition, LG Display’s 1.3-inch OLED display, boasting over 10,000 nits of ultra-high brightness and 4,000 ppi resolution, won the “Best Paper of the Year” award. However, at the 2025 SID and K-Display exhibitions, LG Display’s OLED displays did not appear; instead, LG Display focused on showcasing its fourth-generation OLED panels and large-size automotive displays, emphasizing a strategy focused on commercial products. This indicates that LG Display may stop or reduce investments in silicon-based white OLED (W-OLEDoS).

(3) Sony Semiconductor, Japan: LCoS, Micro OLED

Sony occupies an important position in the LCoS industry with its advanced SXRD (Silicon X-tal Reflective Display) technology. This technology features high resolution, high contrast, and low power consumption, commonly used in Sony’s 4K home projectors and professional cinemas. Sony’s LCoS chips also have high pixel density and compact size advantages, suitable for various advanced imaging and display applications.

(4) JVC, Japan: LCoS

JVC has been involved in LCoS research and development since the mid-1990s and is one of the earliest manufacturers to invest in LCoS technology development, independently developing the D-ILA direct drive image light source amplifier chip. In addition to projectors, the company has also expanded into emerging markets such as AR/VR devices and automotive HUD using LCoS technology.

(5) Kopin, USA: LCoS, Micro OLED, Micro LED

Kopin, established in 1984, is a supplier focused on providing specialized optical systems and high-performance microdisplays for defense, enterprise, consumer electronics, and medical fields. Its products include AMLCD, LCoS, Micro OLED, Micro LED microdisplays, display modules, eyepiece components, image projection modules, automotive and head-mounted display systems, as well as various optical devices and low-power ASIC chips, widely used in defense, enterprise, industrial, and consumer sectors. In August 2025, Kopin reached a strategic investment agreement totaling $15 million with Theon, a globally renowned manufacturer of thermal imaging and night vision systems, to accelerate key technology research and development, expand into the European and NATO defense markets, and strengthen the company’s balance sheet.

(6) SMD, USA: LCoS

Silicon Micro Display (SMD) is a company focused on LCoS microdisplay technology, established in the USA in 2009, developing high-performance microdisplays and related driving technologies for the AR/VR industry. SMD can adjust resolution, optical interfaces, and driving circuits according to customer needs, with products known for high contrast, low power consumption, and compact size, widely used in projectors, helmet displays, and automotive head-up displays, especially suitable for high-end applications with strict requirements for display quality and system integration. Its LCoS microdisplays use advanced color sequential front-lit technology, achieving brightness of up to 400K nits while maintaining a typical power consumption of only 300 milliwatts, providing excellent display performance even under high ambient light conditions.

(7) Texas Instruments, USA: DLP

As a pioneer of DLP technology, Texas Instruments employs a silicon-based DMD (digital micromirror device) array, characterized by high resolution, ultra-fast switching capabilities, and excellent optical efficiency, holding a near-monopoly position in the global DMD market.

(8) BOE: LCD, Micro OLED, Micro LED

Applications such as VR/AR and HUD are important carriers for BOE to implement its “Screen IoT” strategy, and BOE has made in-depth layouts in this regard. Specifically, Beijing BOE Creative Technology Co., Ltd. was established in 2022, with BOE holding 79.3% of the shares, operating the B20 production line, which is a G6 LTPS/LTPO TFT-LCD production line with a total investment of 29 billion, designed to produce 50K/M, mainly manufacturing VR/Mini LED direct display products.

(9) TCL Huaxing Optoelectronics: LCD, Micro LED

Wuhan Huaxing Optoelectronics Technology Co., Ltd. was established in 2014, with TCL Huaxing Optoelectronics holding 98.2% of the shares, mainly operating the t5 production line, which has a total investment of 15 billion, using Mini/Micro LED, LTPO, LTPS, touch screen, and other technologies to produce high-end flagship displays for automotive, laptops, tablets, and VR.

(10) Huike: Micro LED

On May 24, 2025, the Shunqing District People’s Government signed a project agreement with Huike Co., Ltd. in Nanchong City (Chengdu) for a new MLED display chip base project, with a total investment of approximately 10 billion, designed for a monthly production capacity of 1 million pieces. The project will be built in three phases, with the first phase designed for a monthly production capacity of 150,000 pieces, mainly producing full-color MLED display chips. Since 2024, Huike has increased its investment in MLED, exceeding 30 billion by May 2025.

(11) Shiya Technology: Micro OLED

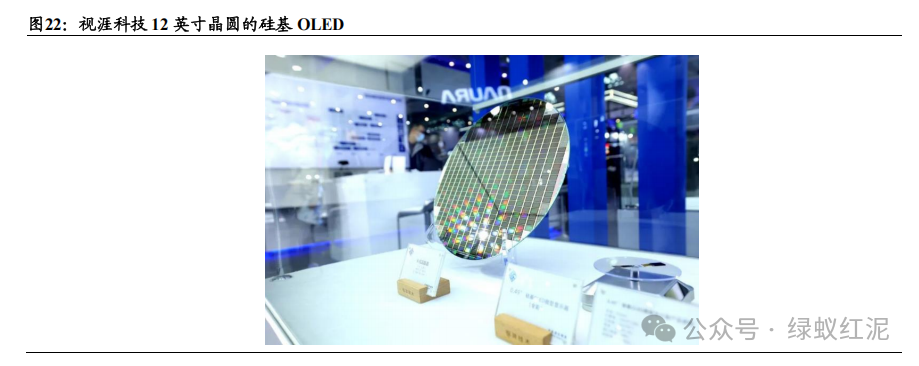

Shiya Technology, established in 2016, is a primary supplier for Apple’s Vision Pro and has submitted an IPO application to the Science and Technology Innovation Board. According to its prospectus, the company has achieved mass production of the world’s first 12-inch silicon-based OLED production line and is one of the few innovative enterprises globally with full-stack self-research capabilities in silicon-based OLED “display chips + microdisplays + optical system solutions.”

(12) Nanjing Guozhao Optoelectronics: Micro OLED

Founded in 2019, Nanjing Guozhao Optoelectronics is a national high-tech enterprise controlled by the 55th Research Institute of China Electronics Technology Group Corporation, focusing on the research and industrialization of silicon-based OLED microdisplay devices and overall solutions. The company is the only domestic unit with both chip design and device manufacturing processes, currently having an 8-inch production line with an annual capacity of 500,000 pieces, and the 12-inch production line to be put into production in 2025 will increase the annual capacity to 2 million pieces, meeting 15% of global market demand.

(13) Yunnan Northern Aolede Optoelectronics: Micro OLED

Founded in 2008, Yunnan Northern Aolede Optoelectronics is a leading domestic Micro OLED enterprise and the second globally, after the U.S. eMagin company, to achieve mass production of various specifications of active OLED microdisplays. The company has successfully developed various specifications of 800×600 (SVGA) and 1280×1024 (SXGA) resolution active OLED microdisplays based on 0.18μm silicon-based CMOS driving technology, combined with efficient top-emission technology and multi-layer thin-film sealing technology. In 2017, it established a joint venture with BOE to develop silicon-based OLED projects.

(14) Nanjing Xinshi Yuan: LCoS, Micro OLED, Micro LED

Founded in 2017, the company’s main products include silicon-based LCoS microdisplay chips, silicon-based OLED microdisplay chips, silicon-based Micro LED microdisplay chips, and spatial light modulators, widely used in AR/VR/MR glasses, automotive HUD, head-mounted displays, optical communications, optical computing, 3D printing, and other emerging fields.

(15) Sitang Technology: Micro LED

The company provides one-stop technology solutions for Micro LED for AR/XR, wearable devices, and flat displays. Since 2018, it has been conducting pilot tests for Micro LED, and in 2022, it established the first phase of its production line in Xiamen, officially starting production in June 2024, providing a capacity of 6 million Micro LED microdisplay chips, having completed Series B financing.

(16) Himax Technologies, Taiwan: LCoS

Himax Technologies, Inc. (NASDAQ: HIMX) is an IC design company focused on image display processing technology, established in 2001 and headquartered in Tainan, Taiwan. The company has long held a leading position in the LCoS technology field, with products successfully applied in Google Glass, hearing-impaired AR glasses, industrial augmented reality head-mounted wearable devices, and AR desktop gaming devices. In May 2024, Himax launched its latest phase-modulated LCoS for AR holographic automotive displays, achieving brighter and higher contrast image quality while simultaneously displaying multiple focal plane images, with lower power consumption, lower cost, and smaller form factor. At CES 2025, the company will showcase its next-generation self-developed ultra-bright 400Knits color sequential front-lit LCoS microdisplay solution.