Little Orange Light Network WeChat ID:ivdnet

In Vitro Diagnostics Connector (www.iivd.net),Moving Forward with Micro-light!

1What is In Vitro Diagnosis

In vitro diagnosis refers to the products and services that obtain clinical diagnostic information by testing human samples (blood, body fluids, tissues, etc.) outside the human body, thereby determining diseases or bodily functions.

In other words, in vitro diagnosis (IVD) involves taking samples such as blood, body fluids, and tissues from the human body and using in vitro testing reagents and instruments to test and verify the samples for disease prevention, diagnosis, treatment monitoring, follow-up observation, health assessment, genetic disease prediction, etc. Therefore, the core of in vitro diagnosis is the in vitro testing reagents and detection instruments.

In vitro diagnosis is a powerful tool in medical testing, providing comprehensive (biochemical information, immune information, genetic information) and multi-layered (qualitative, semi-quantitative, quantitative) test information, which becomes an important source of clinical diagnostic information.

According to statistics from Roche Diagnostics, in vitro diagnosis can influence 60% of clinical treatment plans (some reports say this figure is 80%, which is somewhat vague), but its costs account for only 2% of the total clinical treatment costs, thus in vitro diagnosis has great commercial value and practical significance.

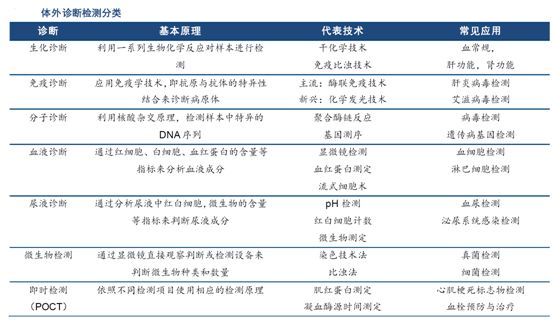

2Classification of In Vitro Diagnosis

In vitro diagnosis can be classified based on different testing principles or methods, mainly including clinical biochemical diagnosis, immunodiagnosis, molecular biology diagnosis, hematological diagnosis, microbiological diagnosis, urinalysis, coagulation diagnosis, etc. Among these, biochemical diagnosis, immunodiagnosis, and molecular biology diagnosis are the three main fields of clinical in vitro diagnosis.

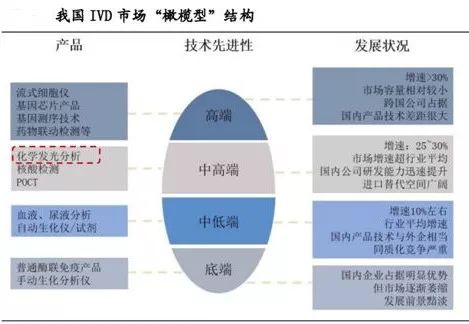

If classified by technological level, the entire IVD market can be roughly divided into three technology levels: low, medium, and high. The low-end market mainly corresponds to manual or semi-automatic ordinary enzyme-linked immunoassay products; the mid-end market can be divided into mid-low end (biochemical, blood testing, urinalysis, etc.) and mid-high end (chemiluminescent immunoassay products, fluorescent quantitative PCR molecular diagnostics, etc.); while the high-end market mainly includes flow cytometers, high-throughput gene chips, etc.

From the development trend perspective, the industry tends to continue upgrading platforms, and each technological platform upgrade often accompanies changes in the growth rate/share of segmented markets (a notable example is the replacement of ordinary enzyme immunoassays by chemiluminescent immunoassay products due to advancements in immunological technology platforms in recent years).

It is important to note that in the process of in vitro diagnosis, diagnostic instruments, reagents, and consumables are used in conjunction. In China’s in vitro diagnosis industry, reagents account for73% (2015 data).

According to the combination of reagents, in vitro diagnostic instruments can be divided into open systems and closed systems. An open system means that the diagnostic instrument can use reagents from multiple manufacturers, while a closed system requires that instruments and reagents from the same manufacturer must be used together.

From this perspective, chemiluminescence, gene chips, gene sequencing, etc. are closed systems, while others are generally open systems.

Based on different detection environments and conditions, in vitro diagnosis can also be divided into laboratory diagnosis and bedside diagnosis (Point of Care Testing, POCT). POCT refers to a method of rapid testing and obtaining results using portable analytical instruments or matching reagents at the sampling site, and has rapidly developed and been applied due to its advantages of “portability, ease of operation, and timely results”.

2. Analysis of the In Vitro Diagnosis Industry

1Overall Industry Growth

(1) Global Growth Rate

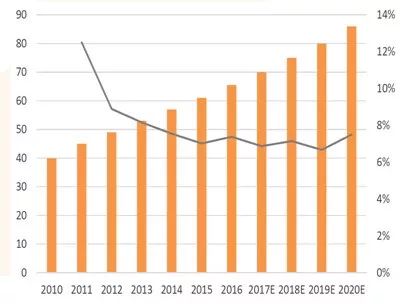

The global in vitro diagnosis industry is in a mature development stage, with the market size expected to reach 74.7 billion USD in 2020, and it is estimated that the global IVD industry will have an average annual compound growth rate of about 4-5% over the next 3-5 years.

In 2016, the global IVD industry market size was approximately 61.7 billion USD. According to Allied Market Research, the global IVD industry is expected to grow at an average annual compound growth rate of about 5% in the coming years and reach 74.7 billion USD by 2020.

With the continuous upgrading of in vitro diagnostic technology and the wave of cutting-edge scientific applications, the growing global population base, and the increasing incidence of chronic diseases and tumors, all have become driving forces for the sustained development of the global IVD market.

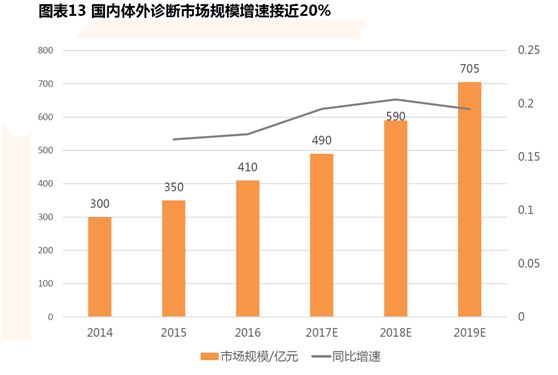

(2) Growth Rate in China

China’s in vitro diagnosis industry is currently in a rapid development stage, maintaining an annual growth rate of around 20% in recent years, with the total market size of China’s IVD market expected to be about 60 billion RMB in 2017.

Driven by factors such as a low market size base, increasing demand for medical services, and updates in testing technology, China’s IVD market is expected to maintain a growth rate that surpasses the average growth rate of the pharmaceutical industry. According to the Kalorama Information report on the “Global IVD Market (10th Edition)”, it is estimated that the compound growth rate of China’s IVD market from 2016 to 2021 will be about 15%.

(3) Development Space for China’s IVD

China’s IVD is in a growth phase of the industry. In terms of per capita diagnostic costs, it is half of the world average level and less than 15% of Japan’s. Compared to developed countries, China’s in vitro diagnosis industry is still in the early stages of development. China’s population accounts for about 1/5 of the global population, but the in vitro diagnosis market size is only 3% of the global total, indicating that it is still relatively small.

According to statistics from the China Industry Information, the per capita annual consumption of in vitro diagnostic products in China is 4.6 USD, which is only half of the global average consumption level and less than 15% of Japan’s, significantly lower than the per capita levels of developed countries. The global IVD market accounts for about 5% of the total pharmaceutical market, while China’s share is only about 1-1.5%.

2Growth of Segmented Industries

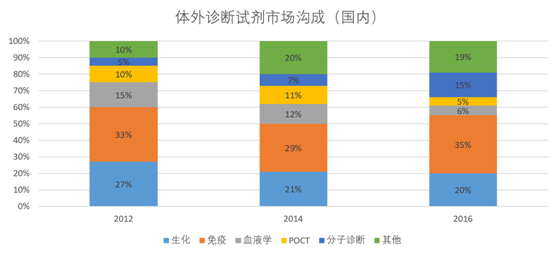

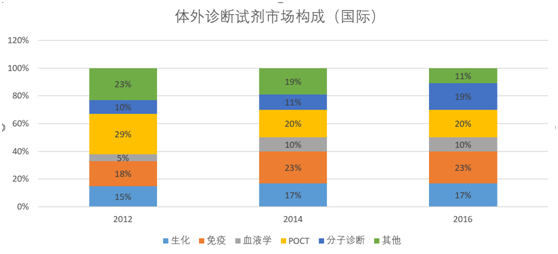

From the perspective of the structure of the in vitro diagnosis market internationally and domestically, biochemistry, immunology, and molecular diagnostics occupy the vast majority of market shares, with international figures at 59% and China at 70%. If the international market represents a mature market structure, does it mean that the market share of biochemical diagnostics in China’s in vitro diagnosis market is stable or shrinking (market share does not represent scale), while the market share of immunological diagnostics will shrink due to the rapid development of other diagnostics like molecular and POCT?

As mentioned earlier, China’s in vitro diagnosis market will maintain a 15% compound growth rate over the next 3-5 years. The following will focus on analyzing the segmented structure and development speed of China’s IVD market to answer the above questions.

(1) Question 1: Is there still development momentum in China’s biochemical diagnostic market? How is market competition? Where are the opportunities for domestic manufacturers?

First, we must ask whether biochemical diagnostics will be eliminated. The answer is no, as the results from practice (the results of development in Europe and America) have shown.

Logically, although different diagnostic methods in the market have their advantages and disadvantages in technology, the hospital’s laboratory or physical examination center will comprehensively consider the adaptability of the diagnostic methods, including requirements for accuracy, efficiency, price, etc.

For example, some biochemical diagnostic projects are tested using chemiluminescent immunoassays, resulting in more accurate and reliable results, while some projects are more suitable for biochemical diagnostic methods. In routine projects like blood glucose, blood lipids, cholesterol, enzymes, etc., biochemical diagnostics play an irreplaceable role. Using chemiluminescent methods may complicate the process, requiring a series of preliminary preparations to clean samples and eliminate interference factors.

Moreover, immunological testing often has higher costs and longer durations, generally requiring 15-20 minutes. In contrast, biochemical diagnostics usually take around 10 minutes, with faster projects yielding results in 2-3 minutes.

Currently, biochemical diagnostics are technologically mature and cost-effective, primarily focusing on glucose and non-protein-based indicators, gradually phasing out other areas while maintaining a high market share in grassroots markets. The terminal pricing is the lowest among several types of tests, but due to low costs, it remains the highest margin variety for both hospitals and product suppliers, exceeding 80%.

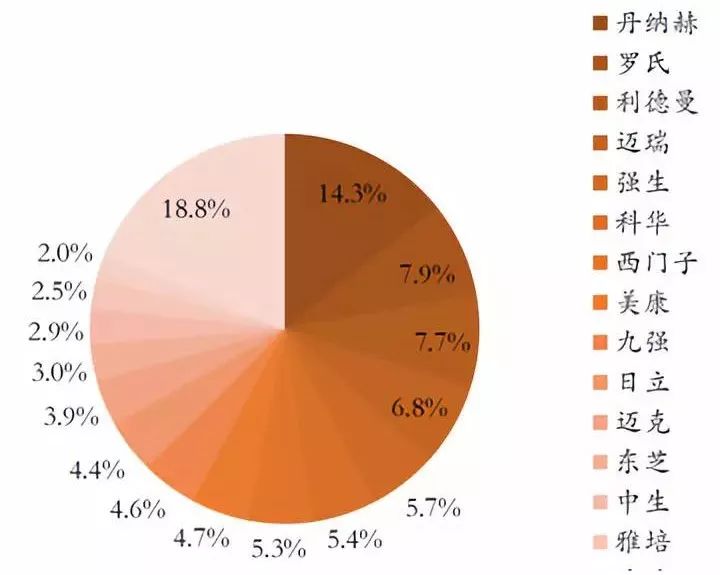

Secondly, from the perspective of market share, the international market is highly concentrated, while China’s market is relatively fragmented. The four major international giants Roche, Beckman, Siemens, and Johnson & Johnson occupy over 80% of the international market share due to their first-mover advantage, while the top five manufacturers in China account for 42%, indicating a relatively fragmented market.

Additionally, the growth rate of biochemical diagnostics in China is slowing, with the industry expected to maintain a growth rate of around 7% over the next 3-5 years, indicating fierce competition. Regarding domestic substitution, imported instruments dominate the high-end domestic market, while domestic brand reagents account for over two-thirds.

Due to the low technical requirements for producing biochemical diagnostic reagents, they have become an entry point for many companies into the in vitro diagnosis field. However, domestic products still have a significant gap in terms of detection accuracy and stability compared to imported products, especially in high-end markets such as tertiary hospitals, which are basically monopolized by foreign giants. The five major diagnostic giants occupy 42.40% of the domestic biochemical market, while domestic products gradually replace imported products in the mid-low end market due to significant price advantages.

From the perspective of the openness of instruments and reagents, in biochemical diagnostics, both closed and open systems coexist, primarily because biochemical diagnostic technology is very mature, and the requirements for using instruments and matching reagents are relatively low.

Open systems can achieve high detection accuracy after calibration of instruments and reagents, essentially meeting clinical testing needs. Many domestic tertiary hospitals often purchase imported instruments and use domestic reagents to reduce costs, so import manufacturers meet domestic market demand, and many of their biochemical instruments are also open systems.

Currently, open systems account for 70%, while the remaining 30% are high-end foreign brands. However, from a trend perspective, many foreign brands are setting up factories in China and collaborating with local companies to reduce costs, leading to a long-term trend toward the closure of instruments and reagents, which will impact domestic reagent manufacturers.

From the perspective of the development trend of biochemical diagnostics, the main competition is in the existing market, and the trend is toward increased market concentration.

Currently, biochemical diagnostic reagents have basically completed import substitution, with domestic market share reaching 70%, but high-end instruments are still dominated by foreign investment, with domestic market share of instruments being less than 10%.

However, as the localization process of foreign biochemical diagnostic leaders accelerates in China, the closure of instruments and reagents is an inevitable trend, which will squeeze domestic small and medium enterprises. To break through, they either need to develop integrated solutions for instruments and reagents or pursue mergers and acquisitions.

(Image: Market Structure of Biochemical Diagnostics)

(Image: Growth Rate of Biochemical Diagnostics)

In summary, several viewpoints on the future development of biochemical diagnostics are as follows:

(1) The industry will maintain low and steady growth (5%-6%);

(2) Integration of instruments and reagents is a future development trend;

(3) The industry has low barriers to entry, with increasing pressure from existing competition, leading to intensified industry consolidation.

Question 2: What is the status of China’s immunodiagnostic market? How can domestic products replace imports?

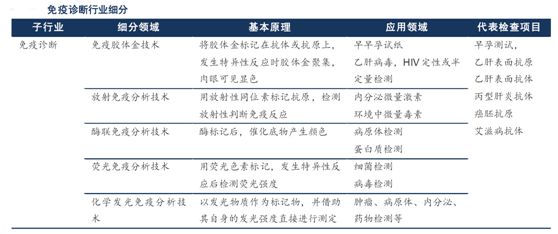

Immunodiagnostics is a diagnostic method that uses the specific immune response between antigens and antibodies to determine immune status and detect various diseases. The so-called specificity means that one antibody can only bind with one antigen, and this one-to-one relationship gives immunodiagnostics high sensitivity.

In recent years, various labeling techniques have been used to label antigens or antibodies, amplifying the process of antigen-antibody binding and expressing it through photonic or radiological signals, leading to various highly specific and sensitive immunodiagnostic methods.

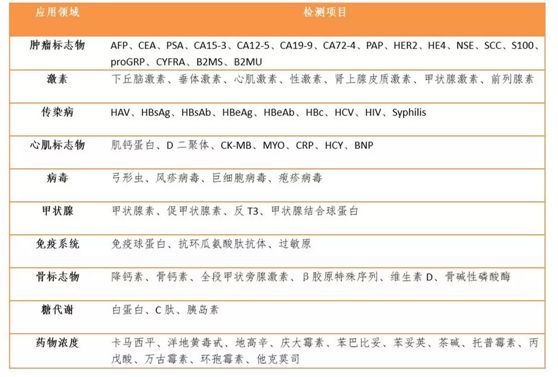

Immunodiagnostics have a much broader application field compared to biochemical diagnostics, mainly including tumors, infectious diseases, viral hepatitis, etc., as shown in the table above. The characteristics of the immunology market are as follows:

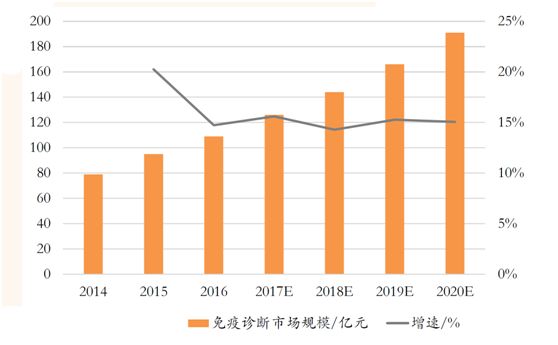

The domestic immunodiagnostic market is rapidly developing, with the market share of chemiluminescence gradually expanding. Immunodiagnostics have become the largest segmented market in China, currently accounting for about 35% of the market share. In 2010, the immunology market size was approximately 4.5 billion, and in 2016, it reached 10.9 billion, with a forecasted growth rate of 15% in the coming years.

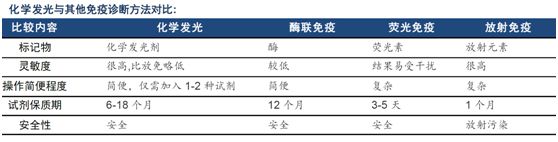

Chemiluminescent immunodiagnostics are the mainstream technology in the field of immunodiagnostics and are also the trend of international development. In recent years, chemiluminescent immunodiagnostic technology has rapidly captured a significant share of the global high-end immunodiagnostic market due to its high degree of automation, high precision in detection, and fast testing speed, becoming the mainstream in immunodiagnostics.

The main types of immunodiagnostics in China’s market are chemiluminescence and enzyme-linked reactions, with chemiluminescence accounting for over 75% (95% in foreign markets). Due to the advantages of chemiluminescence (as seen in the table below), it is expected to further replace enzyme-linked reactions.

(Immunological Response Share in China)

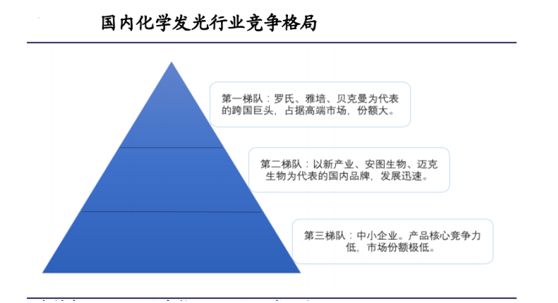

Currently, 90% of the domestic chemiluminescence market is occupied by foreign investment. From a channel perspective, tertiary hospitals are basically monopolized by imported products, while domestic chemiluminescence products primarily serve secondary hospitals and below. This is because the barriers to the chemiluminescence market are relatively high and it is a closed system, so manufacturers that can provide a rich variety of reagents have a strong competitive edge, pushing domestic leaders in chemiluminescence to develop rapidly.

The current capacity of the chemiluminescence market is around 20 billion, and with the technological iteration of the existing market and the growth of the incremental market, this capacity will further expand. The domestic chemiluminescence market is essentially monopolized by foreign giants such as Roche, Abbott, Siemens, and Beckman, with Roche holding a 47% share of the Chinese chemiluminescence market, Abbott at 26%, Beckman (Danaher) at 15%, and Siemens at about 6%, with tertiary hospitals being the main customers for these multinational giants.

Domestic tertiary hospitals, due to their high accuracy requirements, large sample volumes, and numerous testing items, have become the primary customer base for these multinational giants. Additionally, since chemiluminescence is essentially a closed system, with instruments and reagents bundled together, foreign manufacturers have earned substantial profits from the continuous sale of reagents.

In contrast, secondary hospitals and below, due to their relatively small sample sizes, find it challenging to bear the high costs of using imported instruments and reagents. Therefore, foreign giants’ chemiluminescence products have not yet entered secondary hospitals on a large scale, leaving significant market space for cost-effective domestic chemiluminescence products.

With the technological iteration of the existing market and the growth of the incremental market, the capacity for chemiluminescence will further expand; the detection items involve multiple consumer terminals, with a wide coverage area. Moreover, policies favoring graded diagnosis and regional testing centers will benefit the domestic chemiluminescence industry. Currently, foreign investment accounts for 90% of the chemiluminescence market, and domestic substitution is the direction for the development of the chemiluminescence industry.

What is the core competitiveness of domestic substitution in chemiluminescence? R&D capability + price + channels.

(1) R&D

Chemiluminescence technology has a high threshold, and the reason foreign brands dominate domestic tertiary hospitals is mainly due to the accuracy of their instruments and the completeness of their reagents, which is their core competitive advantage in R&D. However, with domestic companies placing greater emphasis on R&D, significant breakthroughs have been made in both instruments and reagents.

For example, AnTu Bio currently focuses on two models, A2000Plus and A2000, which have obtained 88 registration (filing) certificates for magnetic microparticle chemiluminescence detection products, widely applicable in infectious disease testing, tumor detection, prenatal and postnatal care testing, hormone detection, liver fibrosis testing, etc.

Currently, the company’s products have entered 4,500 terminal users, including 1,381 tertiary hospitals, accounting for 61.87% of the total number of tertiary hospitals in the country. In terms of installations, around 400 new units were added in the first half of 2018, with an estimated total of 900 new units for the entire year.

Mike Bio began with only 6 units sold in 2012, reaching about 400 units by 2015, with an expected shipment of 200-300 units in 2017. In September 2018, they launched the I300, all showing rapid growth, with widespread deployment of instruments laying a solid foundation for the continuous sales of reagents.

However, it should also be noted that in terms of chemiluminescent instruments, domestic manufacturers are limited by their technical level and overall R&D capabilities, resulting in certain performance gaps compared to foreign giants. Moreover, they mainly rely on chemiluminescent enzyme immunoassay methods, so attention should be paid to the current progress of domestic leaders.

In terms of reagents, AnTu Bio’s magnetic microparticle chemiluminescent detection reagents cover ten major areas, including infectious diseases, prenatal and postnatal care testing, tumor markers, and hypertension detection, holding 87 registration certificates and offering a complete product line.

Mike Bio had already obtained 77 certificates for chemiluminescent matching reagents at the time of its listing in 2015, with another 27 currently under review, ensuring a rich variety of detection reagents that strongly support performance growth.

In 2012, Mike Bio’s overall revenue from chemiluminescent products was 1.482 million, reaching 160 million in 2015, a 111-fold increase over three years. Although the growth rate of instruments is slower than that of reagents, the bundling of reagents driven by instrument sales and the rich variety of reagents have both contributed to a 33% year-on-year increase in reagent sales in 2017.

KeHua Bio currently has 191 reagent and instrument products, ranking among the top in the domestic market share. Among them, 67 reagent and instrument products have passed the EU CE certification, and chemiluminescence is expected to become a new strong growth point.

(2) Price

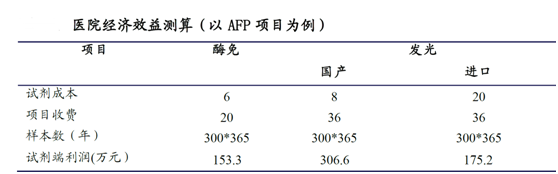

Under the same conditions, the economic effect of using domestic reagents in hospitals is much greater than that of imported ones. Taking a certain secondary hospital in Fujian as an example, if they need to purchase a chemiluminescent instrument for tumor markers (using AFP and hepatitis B HBsAg prices as examples), the daily sample volume is 300.

The price of domestic reagents is around 30% of that of imported reagents, with the cost of a single chemiluminescent reagent reaction being 8 RMB, while the cost of a single enzyme immunoassay reagent is 20 RMB. The list price for chemiluminescence is 36 RMB, while for enzyme immunoassay, it is 20 RMB. The hospital’s reagent profit can be calculated as follows:

Since the instruments are introduced into hospitals through a leasing model, hospitals only need to calculate the reagent costs. The above calculation shows that if this hospital substitutes enzyme immunoassays with chemiluminescence, it not only upgrades the testing technology and optimizes the test results but also achieves better economic benefits. In the chemiluminescent projects, the economic benefits of domestic products compared to imports are significant, with a single project potentially yielding an additional profit of hundreds of thousands.

(3) Channel Mergers and Acquisitions

From 2009 to 2012, the overall sales model of the industry was mainly traditional sales, with manufacturers focusing on single product sales gradually entering the laboratory departments. Both instruments and reagents were distributed through agents or partially through direct sales by manufacturers.

From 2012 to 2015, the industry gradually shifted to a small investment model, where agents earned profits from consumables through upfront or minimal payments for instruments. From 2014 to 2017, the industry sales model underwent significant changes, leading to the emergence of a new marketing model called collective procurement services.

The construction, procurement, after-sales, and value-added services of laboratory departments are outsourced to manufacturers, achieving the goals of cost reduction and efficiency improvement for laboratory departments. This will be the primary sales model in the future.

Therefore, the emergence of the collective procurement model will change the channel ecology of the IVD industry, requiring strong companies with rich products to not only obtain long-term contracts with laboratory departments through their own channels but also to quickly integrate and acquire to gain advantages for rapid future development.

In general, the viewpoints on the future development of chemiluminescence are as follows:

(1) Chemiluminescence is the largest segment in the IVD industry, and with rapid domestic substitution, maintaining a growth rate of 20% over the next 3-5 years is not a problem.

(2) Companies with strong R&D capabilities, rich products, and fast channel expansion will quickly stand out.

Source: Chenghong Finance | Author: Compound Interest Knife

– End –

Guess You Like Previous Selections ▼

1. In Vitro Diagnostic Reagents Enter the