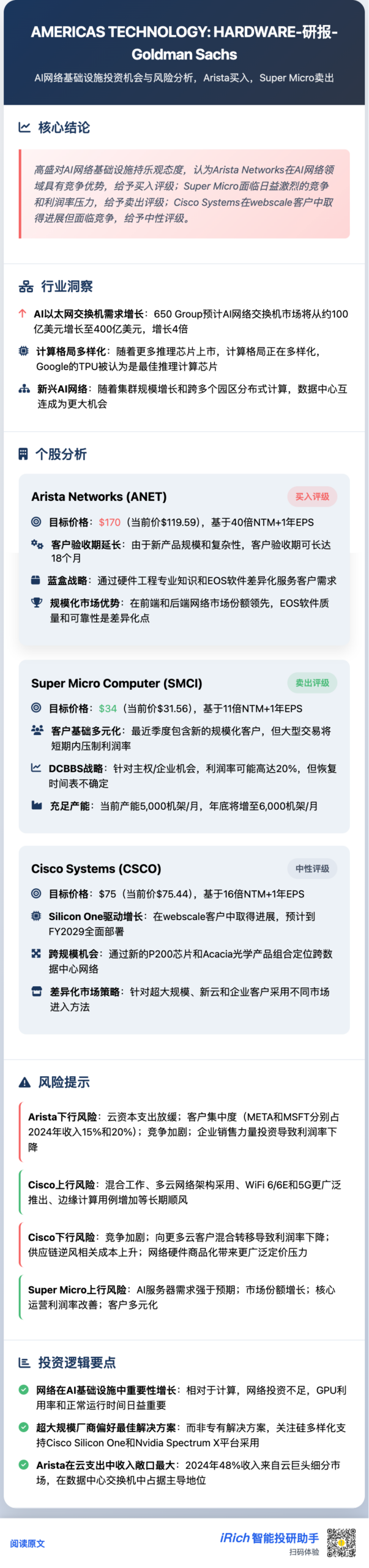

On November 20, 2025, Goldman Sachs held a hardware investor bus tour in California, engaging in in-depth discussions with the management teams of Arista Networks, Supermicro, 650 Group, and Cisco Systems. This research revealed significant trends in network-side investments within AI infrastructure, providing key guidance for hardware investment directions.

Core Conclusion of the Research: Network Investments Reach a Turning Point

As the scale of AI clusters expands and the demand for distributed computing grows, the lagging situation of network investments relative to computing investments is changing. The Goldman Sachs team is increasingly optimistic about network-side opportunities in AI infrastructure, especially considering the growing importance of GPU utilization and uptime.The AI network switch market is expected to grow from approximately $10 billion to $40 billion, showing a fourfold expansion potential. This growth is driven by front-end networks, back-end horizontal scaling, vertical scaling, and cross-scale network demands.

In-Depth Stock Analysis

Arista Networks (Buy Rating, Target Price $170)

Extended Customer Acceptance Cycle Reflects Product Complexity

- The acceptance period for new systems has extended to 18 months, leading to an increase in deferred revenue.

- Certification for the network spine layer is more complex than for the underlying switches.

- The company adopts a conservative revenue recognition policy, ensuring that revenue is recognized only after all contractual functionalities are delivered.

Blue Box Strategy Meets Customer Customization Needs

- Expertise in hardware engineering, diagnostic software, and supply chain capabilities constitute core advantages.

- The underlying network can run alternative operating systems such as SONIC or FBOSS.

- High-end systems (e.g., 7800R series) only support proprietary EOS systems.

Significant Advantages in Vertical Scaling Market

- Leads the front-end and back-end network markets.

- Possesses a deep talent pool in engineering.

- Rich experience in co-development with clients like Meta.

Key Risks: Slowdown in cloud capital expenditures, customer concentration (Meta and Microsoft account for 35% of 2024 revenue), competition from white box switches.

Supermicro (Sell Rating, Target Price $34)

Continued Increase in Scale Customers

- New scale customers (contributing over 10% of revenue) emerged in the latest quarter.

- Winning the GB300 megascale project relied not only on price but also on product engineering differentiation.

- Recent profit margins are under pressure due to manufacturing process efficiency issues and pricing pressure from large customers.

DCBBS Strategy Enhances Profit Margins

- Demand from sovereign and enterprise customers drives an increase in service and software add-on rates.

- Collaborating with U.S. federal entities to expand opportunities for sovereign customers.

- DCBBS product margins can reach 20%.

Ample Capacity Supports Demand

- Current monthly capacity is 5,000 racks, expected to increase to 6,000 racks by year-end.

- The Malaysia factory is primarily responsible for the production of “building block” servers.

Key Risks: Intensifying competition in the AI server market, product commoditization pressure, strong competition from Dell and Cisco in the enterprise market.

Cisco Systems (Neutral Rating, Target Price $75)

Silicon One Chip Drives Growth in Network Scale Customers

- Participating in supplier diversification strategies as an alternative silicon platform.

- Single ASIC supports both switching and routing, offering greater programmability.

- Full deployment of Silicon One is expected by fiscal year 2029.

Significant Cross-Scale Expansion Opportunities

- The new P200 chip features deep buffering and integrated security controls.

- Meets related optical module demands through the Acacia product portfolio.

- Unlike traditional DCI networks, focuses on back-end AI network cross-data center expansion.

Differentiated Market Strategy

- For hyperscale customers: Offers flexible consumption models for components or complete systems.

- For new cloud customers: Focuses on technical collaboration and system coordination.

- For enterprise customers: Leverages a network of certified engineers and trust advantages.

Key Risks: Ongoing loss of market share, structural changes in cloud customer base suppressing profit margins, pricing pressure from hardware commoditization.

Industry Trend Insights

Evolution of Network Architecture

650 Group points out that as cluster scales expand and computing becomes distributed across multiple buildings, data center interconnect becomes an important opportunity. Cisco and Arista have launched deep buffering routers and the 800G R4 series products to address this trend.

Diversification of Computing Landscape

In addition to GPUs, the inference chip market is showing a trend towards diversification:

- Google TPU has become the preferred choice for inference workloads due to multi-generation cost optimization.

- OpenAI’s custom chip plan has been described as “ambitious.”

- Apple may adopt custom ASICs similar to Google TPU.

Conclusion

Based on this research, AI infrastructure investment is shifting from the computing side to the network side, with structural growth opportunities emerging in the Ethernet switch market. Arista is in the most favorable position due to its technological advantages and customer relationships, while Cisco seeks breakthroughs through its chip strategy, and Supermicro faces intensified competition and margin pressures.In light of the turning point in network-side investments, it is recommended to focus on network equipment suppliers with high technical barriers and solid customer relationships, while remaining vigilant against the risks of product homogenization.