The global semiconductor industry is currently in a new round of upward economic cycle. The domestic semiconductor industry is influenced not only by global cycles but also by a very strong logic of domestic substitution. Although China has become the largest semiconductor consumer in the world, the self-sufficiency rate of chips is low, with only 15.9% self-sufficiency in integrated circuits in 2020, indicating significant room for domestic substitution.

On the demand side, benefiting from “Internet of Everything + domestic substitution” and the boost from new energy vehicles, chip demand has risen significantly; on the supply side, the pandemic impact and sanctions have slowed down the expansion rate. Similar to traditional cyclical industries, semiconductors also face the impossible triangle of capacity, inventory, and demand. Due to the long lead time from investment to capacity release, the gap in chips has widened.

Since the beginning of this year, major wafer fabs have announced a series of capital expenditure plans that exceeded expectations.

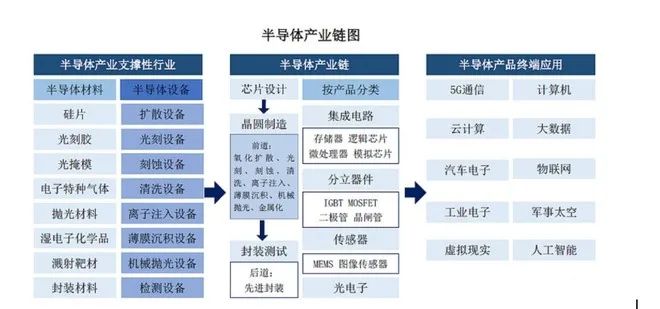

The following diagram illustrates the semiconductor industry process from materials to application terminals:

As shown in the figure: The chip industry chain mainly includes design, manufacturing, packaging, and testing three major segments and semiconductor equipment and materials two major pillar industries. This article will analyze the entire chip industry chain according to this framework.

Chip design includes tool software and design companies.

Chip manufacturing includes manufacturing plants, manufacturing equipment, materials, and auxiliary materials.

Chip packaging and testing include packaging and testing plants, packaging and testing equipment, and auxiliary materials.

To put it simply, the chip design phase is like the architectural design of real estate, wafer foundry is like construction, and packaging and testing is like turning a rough house into a finished one.

1. Chip Design

Chip design is a crucial part of the industry chain, affecting the functionality, performance, and cost of subsequent chip products, requiring strong R&D capabilities. Based on different downstream applications, it can be divided into four categories:

Integrated circuits: memory, logic chips (CPU, GPU), microprocessors (MPU), analog chips.

Discrete components (including power semiconductors): MOSFET, IGBT, diodes, thyristors.

Sensors: MEMS, image sensors.

Optoelectronic devices.

(1) Integrated Circuits

GigaDevice: A dual leader in domestic flash memory chips and MCU microcontroller design. It holds 6% of the global NOR Flash market share, ranking third globally. As a leading company in the domestic MCU microcontroller market, it sold nearly 200 million units in 2020, and its performance is expected to grow rapidly in 2021 as industrial control and other fields expand.

Beijing Junzheng: Acquired Beijing Xicheng, becoming a rare leading company in automotive storage chips in China. Beijing Xicheng holds 15% of the global automotive DRAM memory chip market, ranking second globally. Benefiting from the electrification and intelligence of automobiles, the demand for automotive storage chips in terms of quantity and capacity has increased, achieving both volume and price growth. The microprocessor chip business benefits from the explosive demand for smart terminal hardware. The company plans to raise funds for expanding automotive LED lighting chip production.

Guoke Micro: A leading representative of China’s solid-state storage chips technology, with the latest products reaching international average levels, deeply engaged in smart security monitoring chips, and actively laying out AI smart monitoring chips.

Shengbang Co.: A domestic leader in analog chips, power management chips and signal chain chips benefit from 5G, industrial drive, artificial intelligence, and automotive upgrades, with significant space for domestic substitution.

SiruiPu: A leading domestic signal chain analog chip company, highly overlapping with Shengbang Co. The company’s signal chain analog chips are a major component of 5G RF analog chips, and their overall performance has reached international standards.

Zhuoshengwei: Leading in the RF front-end field, with rapid growth in market demand driven by the development of 5G communication technology, and continuous penetration of the company’s products in client applications.

Jingfeng Mingyuan: A leading company in the LED lighting driver chip market, with both technology and market leadership, achieving the highest global shipment volume. Jingfeng Mingyuan has issued six price increase notices this year due to rising raw material prices and tight production capacity.

Mingwei Electronics: Focused on LED driver business, advancing in display and lighting sectors, with leading technological research and development capabilities. Compared to Jingfeng Mingyuan, it mainly produces LED display driver chips, ranking third among display driver chip manufacturers in 2020 with a market share of 13%.

Zhonying Electronics: The company’s main products include microcontroller chips and OLED display driver chips, benefiting from increased product demand and intelligence in the downstream smart home appliance sector, with significant room for domestic substitution.

Jingjiamicro: A rare graphics processor chip stock in A-shares, mainly applied in military equipment, occupying a large market share in the domestic airborne graphics field, and expanding from military to commercial and civilian markets.

Lexin Technology: A global leader in IoT WiFi-MCU chip companies, holding the largest global market share of over 30%. Its products are mainly used in smart home, electronic consumer products, sensing devices, and industrial control, benefiting fully from the development of the downstream IoT market.

Fuhanwei: A leading designer of security chips. Originally a leading security chip company, HiSilicon was forced out of the market due to U.S. sanctions, and the company seized the opportunity during the supply chain switch of downstream customers, achieving 80% replacement of HiSilicon products. In 2020, the company achieved a market share of 60%-70% in the front-end ISP chip field. At the same time, the company, based on video processing capabilities, entered the automotive camera market, with increasing penetration and providing new growth momentum.

Allwinner Technology: An established SOC chip design company for smart terminals. (SOC, or system-on-chip, can be simply understood as integrating the system onto a single chip, which is the main product development method that the industrial sector will adopt in the future.) Its products are mainly focused on IoT, smart home, etc., with JD’s smart speaker and Xiaomi’s smart vacuum cleaner both using Allwinner’s SOC chips.

Rockchip: Focused on SOC design, with a strong emphasis on power management. The 5G terminal’s requirements for battery life have increased, leading to higher demands for power and energy management. The company’s fast-charging chips have significant optimizations compared to ordinary power management chips in terms of size, energy conversion efficiency, and heat dissipation, with performance and reliability indicators at market-leading levels.

Shanghai Beiling: Focused on consumer and industrial control chip design, targeting markets such as electric meters, mobile phones, LCD TVs, tablets, set-top boxes, and other industrial and consumer electronic products. The merger with Nanjing Weimeng aims to increase the market share of power management chips.

(2) Power Semiconductors

Xinjieneng: Specializes in the research, design, and sales of MOSFET, IGBT and other semiconductor chips and power devices. IGBT is currently the fastest-growing segment in the power device market, and the company has a complete product line, becoming a new growth driver for revenue. At the same time, the company focuses on the research and development of third-generation semiconductor power devices, actively developing power semiconductors for new energy vehicles.

(3) Sensors

Weier Shares: A domestic leader in image sensor design, ranking among the top three globally and number one domestically. In 2019, it successfully acquired two image sensor CIS design companies, OmniVision and Sipex, with design business revenue exceeding the world’s tenth largest listed chip design company.

2. Chip Manufacturing

Driven by market demand, national policies, and capital investment, the global wafer foundry industry is gradually shifting to mainland China, which has become the world’s fastest-growing wafer foundry. From 2016 to 2020, 42% of the newly commissioned wafer fabs were located in mainland China, with the rest spread across various countries worldwide.

The principle of wafer manufacturing is to create masks based on design layouts, forming templates to mass-produce integrated circuits on wafers. Chips are manufactured through repeated processes such as doping, deposition, and photolithography, ultimately achieving highly integrated complex circuits on the wafer.

(1) Manufacturing Plants

Many pure design companies are transitioning to IDM, possessing design, research and development, and production capabilities, which we categorize as manufacturing plants.

1. Integrated Circuits

SMIC: Undoubtedly the leading domestic chip foundry, with the highest technology and scale in China, representing the most advanced manufacturing level of integrated circuit domestic substitution, ranking fourth globally. After sanctions, R&D is expected to stagnate for several years, and the expansion of advanced process production capacity will also stall.

Unisoc: A dual leader in intelligent security chips and domestic specialty ICs, with “universal chips” and automotive-grade chips blooming in multiple areas. Its subsidiary Guowei Electronics has a complete product line and strong technical strength, making it a leading company in domestic specialty ICs. Subcompany Unisoc Tongxin is a leader in domestic smart card chips, with increasing market penetration. Subcompany Unisoc Tongchuang is a leading domestic civilian FPGA enterprise, breaking the monopoly of overseas oligopolies, with significant space for domestic substitution.

Fuman Electronics: Mainly engaged in LED control and driver chips, power management chips, and has integrated design and packaging capabilities. The company has made breakthroughs in core technologies for small-pitch & Mini LED control and driving, and has also achieved leading breakthroughs in fast-charging chips, with leading technical strength in China. Actively laying out the MOSFET field, it is expected to benefit fully from the domestic substitution of power semiconductors.

2. Power Semiconductors

Refers to chips that handle electricity, with the main function of converting various types of electricity into specifications required by end products. For example, after the current is output from the electric vehicle’s battery, it can drive the motor, air conditioning, and audio through different power chips.

MOSFET: A field-effect transistor. Mainly used in computer power supplies, household appliances, etc., accounting for over 40% of the global power device market.

IGBT: Applications cover a series of fields from industrial power supplies, frequency converters, new energy vehicles, new energy generation to rail transportation, and national grid.

China Resources Micro: One of the leading domestic power semiconductor IDMs, the largest in terms of operating income and the most complete product series of MOSFET manufacturers. Plans to establish Runxi Microelectronics in cooperation with the National Integrated Circuit Industry Investment Fund Phase II and Chongqing Yongwei Electronics, expected to achieve a monthly production capacity of 30,000 pieces of 12-inch mid-to-high-end power semiconductor wafers upon completion.

Star Power: A domestic leader in IGBT semiconductors, ranking seventh in the global IGBT module market, being the only domestic company in the top ten, with a significant market advantage. Transitioning from a pure design plant to IDM to ensure capacity supply, its products are primarily used in industrial control and electrical fields. Plans to raise 3.5 billion yuan to purchase lithography, developing, and etching equipment, with a design capacity of 360,000 pieces of power semiconductors, aimed at quickly launching automotive-grade SiC chips to improve the product layout in the automotive power supply market.

Silicon Micro: One of the leading domestic power semiconductor IDMs, focusing on MEMS sensors, high-voltage integrated circuits, and semiconductor power devices across three main technical directions.

Jiejie Micro: A leading company in thyristors, with product performance reaching international leading levels. Its business scope covers chip design, wafer manufacturing, and packaging testing across all business segments. In July this year, it announced plans to expand its power semiconductor 6-inch wafer and device packaging projects, with products expanding from thyristors and protective devices to IGBT modules. Additionally, the automotive-grade packaging industry project has been launched, gradually improving the industrial chain.

Yangjie Technology: A leading domestic power semiconductor IDM manufacturer with complete chip design, wafer manufacturing, and packaging testing capabilities. Leading domestic power diode, gradually extending towards MOSFET, IGBT, and third-generation semiconductor power devices. Its application fields cover power supplies, home appliances, lighting, security, instrumentation, communication, industrial control, and automotive electronics. Its products have a high application rate in the photovoltaic field, accounting for about 15% of revenue.

Wentai Technology: Acquired Anshi Semiconductor for 18.1 billion yuan, which is a global leader in power semiconductors, mainly targeting consumer electronics and automotive fields. Its main products include logic devices, discrete devices, and MOSFET devices, being a semiconductor multinational company integrating design, manufacturing, packaging, and testing. All three major businesses are globally leading, with logic devices ranking second, diodes and transistors ranking first, and automotive power MOSFET ranking second.

Liangwei Micro: A rapidly growing leading enterprise in semiconductor silicon wafers and power devices, focusing on Schottky diode chips.

San’an Optoelectronics: A domestic leader in LED chips. The first phase of the Hunan San’an Semiconductor base, with a total investment of 16 billion yuan, officially went into production this June, being the first domestic and the third global SiC IDM production line.

3. Sensors

SemiMicro: Originally named Nawei Technology, specializing in MEMS chip wafer manufacturing. In 2016, SemiMicro acquired Swedish Silex, gaining globally leading process IP, entering the MEMS pure foundry track and becoming the global leader in MEMS foundry. The company currently produces various devices such as microfluidics, micro-ultrasonic, micromirrors, and optical switches.

(2) Materials and Auxiliaries

The semiconductor manufacturing process is quite complex, with advanced processes requiring over 500 steps, necessitating a large number of materials. Therefore, semiconductor materials are also the most subdivided field in the entire industry chain, with high technical and capital barriers.

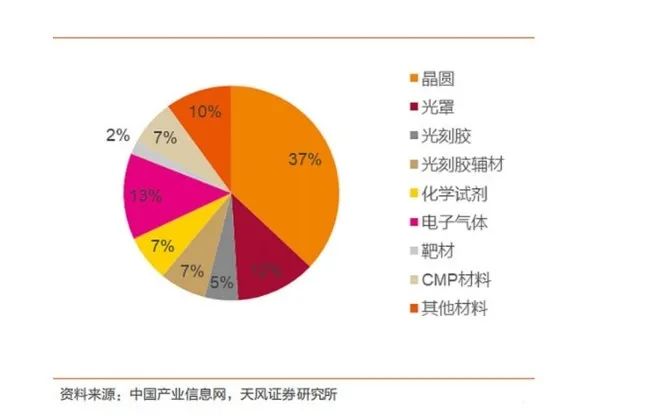

Among them, silicon wafers (substrates) account for the highest value, exceeding 1/3, followed by special electronic gases accounting for 13%, photomasks, photoresists, and auxiliary materials each accounting for about 12%, with other materials accounting for less than 10%.

Classification of semiconductor material cost ratios:

1. Silicon Wafers

Silicon wafers are the most important raw material in integrated circuit manufacturing, with the largest market scale. Currently, over 50% of global silicon material production capacity is concentrated in Japan, with the top five manufacturers accounting for over 90%. The largest domestic manufacturer is Shanghai Silicon Industry.

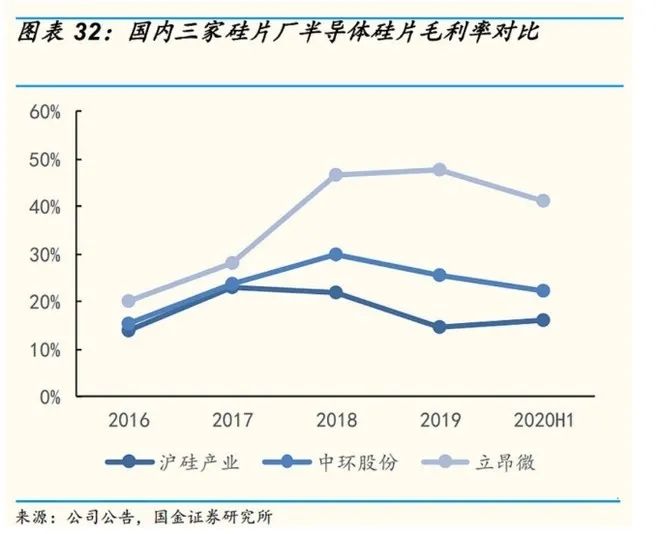

Shanghai Silicon Industry: A pure semiconductor silicon wafer company with leading domestic production capacity and technology. It was the first to achieve large-scale production of 300mm silicon wafers, breaking the deadlock of zero domestic production of large wafers, but the utilization rate is low, and it has not yet achieved scale effects. Due to high depreciation costs, the gross profit margin of 300mm silicon wafers is -34.82%, the lowest among the three domestic silicon wafer manufacturers, and it has not yet achieved profitability.

Zhonghuan Shares: Zhonghuan focuses on photovoltaic silicon wafers, accounting for nearly 90%, while semiconductor silicon wafers only account for 7% of total revenue. Although the scale is not large, Zhonghuan’s semiconductor silicon wafer production capacity is rapidly improving. The 12-inch capacity for 2020 is 70,000 wafers/month, and from 2021 to 2023, production is expected to continue to increase, with capacity expected to exceed 600,000 wafers/month. The photovoltaic and new energy layout can achieve synergy, and the future release of large silicon wafer capacity has significant premium space for leading companies.

Liangwei Micro: Liangwei Micro’s silicon wafer products are smaller in size and have integrated advantages in polishing wafers, epitaxial wafers, and power devices, resulting in the highest gross margin exceeding 40%. The 12-inch wafer production capacity of 150,000 wafers/month is expected to be completed by the end of this year. In addition to semiconductor wafers, it also has power devices and RF chip business.

2. Special Electronic Gases

Electronic special gases are required in nearly every step of semiconductor production, and they largely determine the final product’s performance. The variety of gases used is extensive, and the quality requirements are high, making them known as the “blood” of semiconductor manufacturing. Although the domestic substitution rate is still low, the speed of domestic substitution is relatively fast.

Nanda Optoelectronics: Its independently developed hydrogen-based gases phosphine and arsine are among the two types of electronic special gases with the highest technical barriers, breaking foreign technical blockades and monopolies. It has not only continuously increased its market share in the LED industry but has also rapidly achieved product import substitution in the integrated circuit industry, gaining high recognition from a wide range of customers, currently holding more than 75% of the domestic market share. Meanwhile, the company’s MO source products have achieved domestic import substitution and are a major global producer of MO sources. MO source series products are core raw materials for preparing LEDs, next-generation solar cells, phase-change memory, semiconductor lasers, RF integrated circuit chips, etc.

Huate Gas: The company has achieved large-scale production of 20 imported substitute products. Special gases have also passed the product certification of ASML, the world’s largest photolithography machine supplier, and supply to first-tier companies such as SMIC and Hua Hong Semiconductor.

Yake Technology: A platform-type enterprise in semiconductor materials, similar to Northern Huachuang in the equipment sector. Its business includes semiconductor chemical materials, electronic special gases, and photoresists. Its products cover core links such as semiconductor films, photolithography, deposition, etching, and cleaning. Precursors and SOD break the overseas monopoly. In 2020, it acquired LG Chem’s colored photoresist, gaining mature technology and mass production capabilities for colored photoresists and TFT photoresists, effectively filling the gap in domestic colored photoresist production.

3. Photoresists

Photoresist technology has high barriers and high value, making it known as the “pearl” among semiconductor materials. The high-end photoresist market is mainly dominated by Japanese companies, with the most widely used KrF photoresists and ArF photoresists having a domestic substitution rate of less than 5% and significant room for imported substitutes.

Huamao Technology: Mainly engaged in airbag materials, entering the semiconductor photoresist industry through holding 29% of Xuzhou Bokan’s equity. Xuzhou Bokan’s photoresist monomer business accounts for 5% of the global market share and has stored 80% of the global photoresist monomer product technology, becoming the only high-end photoresist monomer material research and development and mass production enterprise in China. It has successfully developed over 10 series of high-end photoresist products, with significant integrated advantages in semiconductor photoresists.

Tongcheng New Materials: Mainly engaged in special rubber additives, entering the semiconductor photoresist market through holding Beijing Kehua. Beijing Kehua is the only Chinese photoresist company listed among the top eight global photoresist companies, and also the highest-grossing photoresist company in China. The domestic substitution of i-line products is mainly contributed by Beijing Kehua, which is also the only local photoresist company capable of supplying KrF photoresists in bulk to 8-inch and 12-inch customers, with products reaching world-class standards, entering the supply chains of domestic manufacturers such as SMIC, Changjiang Storage, and Hua Hong Semiconductor.

Jingrui Shares: Jingrui’s products include ultra-pure high-purity reagents, photoresists, functional materials, lithium battery materials, and basic chemical materials.

In the photoresist field, the subsidiary Suzhou Ruihong is a pioneer in the domestic photoresist field, producing photoresists for 30 years, with product technology levels and sales at the leading position in China. The i-line photoresist has obtained supply orders from SMIC Tianjin and Yangjie Technology; the high-end KrF (248nm) photoresist has completed pilot testing and established a pilot demonstration line.

Nanda Optoelectronics: The company has successfully self-developed the first ArF photoresist product in China, passing customer certification twice. The company has currently built a 25-ton production line (5 tons dry and 20 tons wet), and under the trend of photoresist domestication, the photoresist business will drive the company’s performance into new growth space.

4. CMP Polishing Materials

CMP polishing materials and target materials have the highest degree of domestic substitution, with some products’ technical standards reaching world-class levels, and local companies have achieved bulk supply.

Polishing liquids and polishing pads are the main materials for CMP polishing, classified as high-value consumables with high profit margins, long certification times, strong customer stickiness, and relatively good competitive landscapes. In terms of product value, polishing liquids are higher, accounting for 49% of total material costs, while polishing pads account for 33%, with other materials totaling less than 20%.

Anji Technology: A domestic leader in polishing liquids, currently having no competitors in the domestic market. Its market share exceeds 20%, second only to Cabot. The technical content of polishing liquids is very high, and due to their specificity, after binding with major customers, future growth rates are also guaranteed.

Dinglong Shares: A domestic leader in polishing pads, primarily producing printing and copying consumables, has begun to layout semiconductor materials in recent years, with polishing pads starting to ramp up last year. It has become a supplier to Changjiang Storage and continues to increase supply to SMIC.

5. High-Purity Wet Electronic Chemicals

Ultra-pure high-purity reagents refer to chemical reagents with a main component purity higher than 99.99%, mainly used in chip cleaning, etching, and other manufacturing fields.

Jianghuai Micro: A domestic leader in wet electronic chemicals, breaking the barriers set by foreign companies and gradually achieving domestic substitution in the mid-to-low-end market. Its ultra-pure high-purity reagents and supporting reagents for photoresists can provide a full range of wet electronic chemicals for flat-panel displays, semiconductors, photovoltaic, and other fields.

Jingrui Shares: Ultra-pure high-purity reagents account for 20% of its revenue. Its main products, such as ultra-pure hydrogen peroxide, ultra-pure ammonia, and the under-construction high-purity sulfuric acid, have reached G5 levels, while other high-purity chemicals generally range from G3 to G4 levels.

6. Target Materials

Jiangfeng Electronics: The domestic leader in high-purity sputtering target materials, currently capable of mass production of tantalum, copper, titanium, and aluminum target materials for 90-7nm semiconductor chips, with tantalum target materials already in mass production for TSMC’s 7nm chips, and products for the 5nm technology node entering the verification stage.

(3) Manufacturing Equipment

The semiconductor boom cycle follows the pattern of “equipment leading, manufacturing relay, materials in short supply”. Mainland China has welcomed an investment boom, significantly increasing the demand for semiconductor equipment. In the first half of this year, the year-on-year shipment volume of semiconductor equipment increased by 50% compared to last year, with equipment manufacturers overwhelmed with orders.

Due to the high technical barriers and long development cycles of semiconductor equipment, it is one of the most critical links in the entire industry. Therefore, to achieve self-control in China’s semiconductor industry chain, semiconductor equipment is crucial.

Semiconductor equipment has high value content, accounting for 75-80% of wafer fab construction investment. Currently, the self-manufacturing rate of semiconductor equipment in China is still low, with a domestic substitution rate of about 16% in 2020. However, in some areas, domestic manufacturers have broken the blank and are continuously catching up in technology.

North Huachuang: The absolute leader in domestic semiconductor equipment with strong platform attributes. Large scale; strong R&D strength belongs to the first tier in China; leading market share, with a 7% market share in etching equipment. A rich product line covering thermal processing, etching, thin film deposition (PVD, CVD), cleaning, etc. Silicon wafer equipment – thermal processing equipment – photolithography equipment – etching equipment – ion implantation equipment – thin film deposition equipment – polishing equipment – cleaning equipment – testing equipment.

Changchuan Technology: The company primarily engages in the R&D, production, and sales of integrated circuit-specific equipment, a high-tech enterprise and software company dedicated to enhancing the technical level of China’s integrated circuit equipment and actively promoting the upgrade of the integrated circuit equipment industry.

1. Silicon Wafer Equipment

Silicon wafer manufacturing is the first step in chip production, with single crystal silicon growth furnaces being the main semiconductor equipment for producing single crystal silicon.

Jingsheng Electromechanical: A domestic leader in crystalline silicon growth equipment, spanning both semiconductor and photovoltaic industries, holding the largest share in the domestic high-end market. The technology is advanced, achieving multiple technological breakthroughs in large silicon wafers. It has also expanded into slicing, polishing, and epitaxial equipment, completing technology certification. It has even launched third-generation silicon carbide semiconductor equipment, which has been delivered to customers.

2. Thermal Processing Equipment

Thermal processing equipment refers to high-temperature furnaces, mainly used for the oxidation, diffusion, and annealing processes of silicon wafers. The suppliers are mainly foreign manufacturers, with the domestic leader being North Huachuang, which has mature product lines in various sub-fields of thermal processing equipment, and its market share is increasing year by year. North Huachuang’s thermal processing equipment accounts for over 30% of Changjiang Storage.

3. Photolithography Equipment

Photolithography is the process of transferring the designed circuit pattern from the photomask to the photoresist on the wafer surface, facilitating subsequent processes such as etching and ion implantation to realize the designed circuit. Photolithography is the core link in wafer production, including photolithography machines and coating and developing equipment.

Photolithography machines are the most technically challenging equipment in wafer processing, with the market dominated by Dutch company ASML. Currently, the main domestic companies capable of producing photolithography machines are Shanghai Microelectronics.

Xinyuan Micro: The leading company in the coating and developing machine industry, successfully breaking the monopoly of foreign manufacturers and becoming the only domestic manufacturer. Its products have passed the process verification of downstream wafer factories, with a market share of 5%. In recent years, the company has also begun to enter the wet cleaning equipment field, competing with companies like Shengmei Technology, Zhichun Technology, and North Huachuang.

4. Etching Equipment

Etching equipment is second only to photolithography equipment in wafer factory equipment expenditure, and there are more etching devices, with a higher replacement ratio. Currently, China’s etching equipment is relatively advanced.

China Micro: The leading enterprise in etching equipment, with its dielectric etching machine having entered the 5nm process, with technology nearing world-class standards and a domestic market share of 13%.

North Huachuang: The technology node has reached 28nm, with a 7% market share in etching equipment.

5. Ion Implantation Equipment

After etching the silicon wafer, some special impurity ions need to be implanted into the silicon substrate, which is done by ion implantation machines. There are few domestic targets for ion implantation, with only Kaishitong and Zhongke Xinxin.

Wanye Enterprise: The company primarily engages in real estate business, acquiring Kaishitong in 2018 to enter the semiconductor ion implantation equipment market. Its products have entered the production line verification stage, and last year it received orders for four machines.

6. Thin Film Deposition Equipment

The thin film deposition process is divided into physical vapor deposition (PVD), chemical vapor deposition (CVD), and epitaxy.

North Huachuang’s PVD equipment has already been used in 28nm production lines, with significant progress made in 14nm process equipment, with a domestic substitution rate of about 30%.

7. Polishing Equipment

In the later stages of wafer manufacturing, polishing machines are used to flatten the surface of silicon wafers.

The leading company in this field is Huahai Qingke, with advanced technology, holding a total market share of 20%. Its IPO application has been approved by the Shanghai Stock Exchange listing committee and will be listed on the Sci-Tech Innovation Board.

8. Cleaning Equipment

Cleaning equipment currently has the highest domestic substitution rate, reaching 20%. With the extension and complexity of the process, each chip requires at least over 200 cleaning steps during the entire manufacturing process.

Shengmei Technology, which is applying for an IPO on the Sci-Tech Innovation Board, has been deeply engaged in semiconductor cleaning equipment for over ten years, holding the highest market share among domestic companies, with its products entering the supply chains of SMIC, Changjiang Storage, and SK Hynix.

Shengmei Technology: The leading company in semiconductor cleaning equipment, with a technological advantage leading the industry. It occupies 80% of the domestic market share, while the remaining 20% is shared by North Huachuang, Xinyuan Micro, and Zhichun Technology.

Zhichun Technology: The company currently has sufficient orders for wet cleaning equipment, with production plans extending to 2022. Its equipment can achieve full coverage of 28nm wet processes, meeting the requirements of most domestic wafer fabs, with single wafer cleaning equipment expected to be delivered in bulk in the second half of the year.

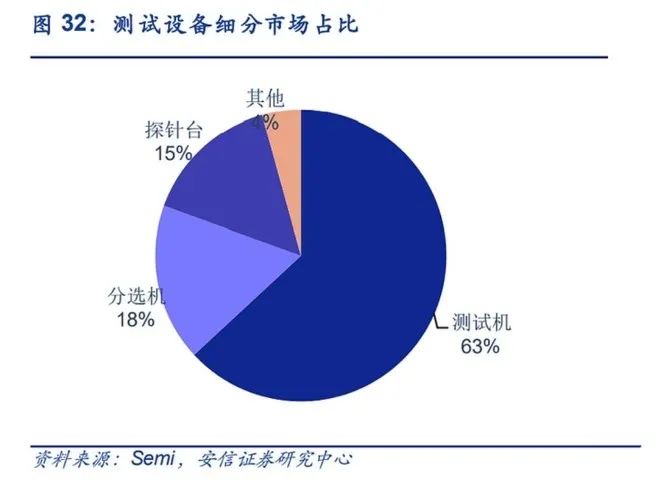

9. Testing Equipment

Testing equipment is mainly used to detect chip performance and defects, spanning each major process in semiconductor manufacturing, categorized into front-end testing and back-end testing equipment based on different stages.

Front-end testing equipment is mainly used in the wafer processing stage, belonging to quality testing, with higher barriers. Currently, domestic companies have weaker competitiveness, with a domestic substitution rate of less than 5%, at the stage of technological and product breakthroughs.

Precision Testing: Focused on semiconductor front-end testing equipment while also laying out back-end equipment to form a comprehensive coverage of the semiconductor testing field. Its automatic testing equipment has achieved basic domestication and has received bulk repeat orders from first-tier domestic customers.

Saiteng Shares: Deeply engaged in automated assembly and automated testing equipment, entering the semiconductor testing equipment field through the acquisition of Japanese Optima. Optima has a mature product line in wafer defect detection equipment, and this technology reserve is scarce in China, thus seizing the developmental opportunity.

3. Chip Packaging and Testing

China, benefiting from cheap labor, initially undertook semiconductor packaging and testing businesses that require a large labor force and lower technical requirements. Currently, the overall chip packaging and testing in mainland China has reached international advanced levels, with a relatively complete industrial chain (packaging and testing plants, equipment, materials).

(1) Packaging and Testing Equipment

The back-end testing equipment of detection equipment is mainly used in the packaging and testing stage after wafer processing, mainly for electrical testing.

The equipment is mainly divided into testers (ATE), sorters, and probe stations, with testers having the largest market and higher value. With the expansion plans of the three major packaging and testing manufacturers, there will be a direct increase in demand for domestic back-end testing equipment.

Changchuan Technology: A comprehensive leader in domestic semiconductor testing equipment, mainly focusing on sorters, with testers as a supplement, laying out multiple tracks. Its products are competitive, with major performance indicators reaching domestic leading levels, close to advanced foreign technology levels.

Huafeng Measurement and Control: The leading company in testing machine equipment, capable of achieving domestic substitution. Its technology is domestically leading, approaching world-class levels, entering the supply chain of packaging and testing leaders. Testing machines have a high value proportion in semiconductor testing equipment, with Huafeng Measurement and Control achieving an 80% gross profit margin, leading peers and showing strong profitability. However, it is also constrained by a single track, limiting growth speed.

(2) Packaging and Testing Materials

Kangqiang Electronics: The domestic leader in semiconductor packaging materials, being the largest lead frame production enterprise in China.

(3) Packaging and Testing Plants

China is a major packaging and testing country, possessing the “three giants of packaging and testing”—Changdian Technology, Tongfu Microelectronics, and Huatian Technology, all of which have announced their respective expansion plans.

Changdian Technology: The leading domestic packaging and testing company, ranking third globally with a market share of 14.4%. The company is advancing in high-end packaging technology alongside the international first tier, further developing advanced packaging technologies such as SiP, wafer-level, and 2.5D/3D after acquiring Xingke Jintong, achieving large-scale production far exceeding traditional packaging in terms of output and sales.

Tongfu Microelectronics: The sixth global packaging and testing plant, with a market share of 7%. It focuses on a major customer strategy, long-term laying out advanced packaging technologies for memory and microprocessor products. Recently, it developed the first domestic SiP power module packaging technology, which can be applied to various base stations and network power supplies, including 5G, and has achieved mass production.

Huatian Technology: Through self-construction and acquisitions, it owns multiple domestic and foreign factories, with a comprehensive layout in low-end, mid-end, and high-end.

E Course Network (www.eecourse.com) is a professional integrated circuit education platform under Moore Elite, dedicated to cultivating high-quality integrated circuit professionals for the semiconductor industry for six years. The platform is oriented towards the job demands of integrated circuit companies, providing a training platform that aligns with the corporate environment, rapidly training students to meet corporate needs through online and offline training.

E Course Network has a mature training platform, a complete course system, and a strong faculty, planning a high-quality course system of 168 courses for China’s semiconductor industry, covering the entire integrated circuit industry chain, and has four offline training bases. So far, it has deeply trained a total of 15,367 people, directly supplying 4,476 professionals to the industry. It has established deep cooperative relationships with 143 universities and held 240 corporate-specific IC training sessions.