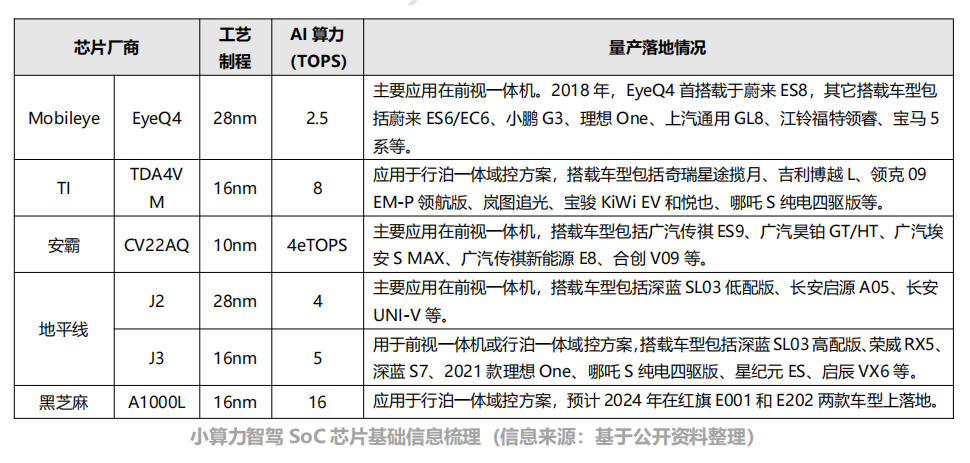

Generally, different vehicle models from car manufacturers have different market positions, which determine the price range of the models. Different price models also exhibit varying sensitivity to the pricing of functional configurations. Regarding smart driving feature configurations, there are different levels of demand for the main control SoC chips based on the market positioning of the models (different price tiers).Currently, based on the varying AI computing power requirements of different levels of smart driving solutions, smart driving SoC chips can be roughly categorized into three types: low-power SoC chips (2.5~20 TOPS), mid-power SoC chips (20~80 TOPS), and high-power SoC chips (≥100 TOPS).1 Market Demand1) Low-Power SoC ChipsLow-power SoC chips typically have an AI computing power ranging from 2.5 to 20 TOPS, and the primary product forms supported are front-view integrated machines or distributed driving or parking controller solutions, characterized by a pursuit of high cost-performance ratio; in terms of functionality, they mainly provide basic L0~L2 level assisted driving features, with some models possibly offering high-speed NOA functionality, generally priced between 100,000 to 150,000 yuan.Currently, L2 and below ADAS functions have entered a rapid growth phase, with front-view integrated machines accounting for about 75% of the ADAS market share, remaining the main product form in the current ADAS market. Low-power SoC chips still have a broad market space in the future. 2) Mid-Power SoC ChipsMid-power SoC chips typically have an AI computing power ranging from 20 to 80 TOPS, and the primary product forms supported are lightweight integrated driving and parking domain controller solutions; in terms of functionality, they promote features such as “easy to use” high-speed NOA, urban memory NOA, and memory parking, with some models possibly offering urban NOA functionality, generally priced between 150,000 to 250,000 yuan.Overall, the mid-power SoC chip market is a result of the rapid iteration and upgrading of chips. Nvidia’s Xavier was initially a high-power SoC chip in the smart driving market, but with the emergence of Nvidia’s next-generation chip Orin, as well as subsequent high-power chips like Horizon’s J5 and Ambarella’s CV3-AD, simply pursuing high computing power for some mid-range models does not guarantee their competitiveness in the market, but rather may lead to a loss of cost-performance advantage. Thus, chips of the same level as Xavier have “downgraded” from the high-power SoC chip market to the mid-power SoC chip market.

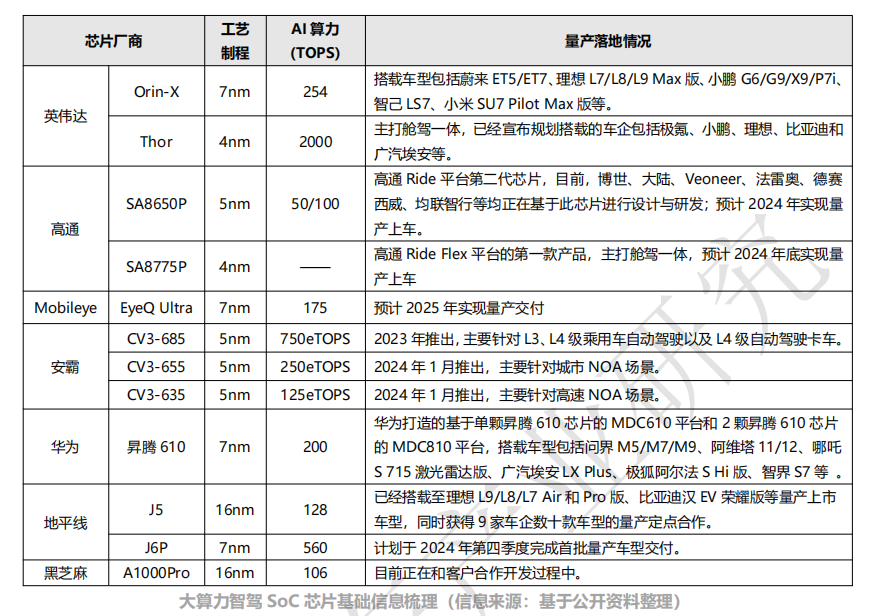

2) Mid-Power SoC ChipsMid-power SoC chips typically have an AI computing power ranging from 20 to 80 TOPS, and the primary product forms supported are lightweight integrated driving and parking domain controller solutions; in terms of functionality, they promote features such as “easy to use” high-speed NOA, urban memory NOA, and memory parking, with some models possibly offering urban NOA functionality, generally priced between 150,000 to 250,000 yuan.Overall, the mid-power SoC chip market is a result of the rapid iteration and upgrading of chips. Nvidia’s Xavier was initially a high-power SoC chip in the smart driving market, but with the emergence of Nvidia’s next-generation chip Orin, as well as subsequent high-power chips like Horizon’s J5 and Ambarella’s CV3-AD, simply pursuing high computing power for some mid-range models does not guarantee their competitiveness in the market, but rather may lead to a loss of cost-performance advantage. Thus, chips of the same level as Xavier have “downgraded” from the high-power SoC chip market to the mid-power SoC chip market. 3) High-Power SoC ChipsHigh-power SoC chips typically have an AI computing power of 100 TOPS and above, with the primary product forms supported being high-end integrated driving and parking domain controller solutions, and even cabin driving integrated solutions; in terms of functionality, they promote features such as “easy to use” urban NOA, AVP, and other L2+ level functionalities, with some models considering hardware embedding to achieve L3 and higher-level autonomous driving functions, generally priced above 250,000 yuan.In the development process toward high-level smart driving functionalities, new algorithms (Transformer + BEV + OCC) and more advanced vehicle EE architectures (centralized computing + regional control) are required, which all necessitate higher computing power SoC chips as the “foundation” to support.

3) High-Power SoC ChipsHigh-power SoC chips typically have an AI computing power of 100 TOPS and above, with the primary product forms supported being high-end integrated driving and parking domain controller solutions, and even cabin driving integrated solutions; in terms of functionality, they promote features such as “easy to use” urban NOA, AVP, and other L2+ level functionalities, with some models considering hardware embedding to achieve L3 and higher-level autonomous driving functions, generally priced above 250,000 yuan.In the development process toward high-level smart driving functionalities, new algorithms (Transformer + BEV + OCC) and more advanced vehicle EE architectures (centralized computing + regional control) are required, which all necessitate higher computing power SoC chips as the “foundation” to support. 2 Market StructureFrom the perspective of market size, according to data from ICV, the global smart driving SoC market size in 2022 was 3.295 billion US dollars, with the Chinese market size reaching 1.505 billion US dollars, accounting for 45.68% of the global market. It is estimated that by 2024, the global smart driving SoC market size is expected to exceed 10 billion US dollars, and by 2027, it is projected to reach 28.306 billion US dollars, with a compound annual growth rate of 43.11%.According to statistics from the Gaishi Automotive Research Institute, in 2023, the number of passenger cars (excluding imports and exports) in the Chinese market equipped with smart driving domain controllers reached 1.839 million sets, a year-on-year increase of about 70%, with an installation rate of about 8.7%.Additionally, in the ranking of smart driving domain control chip installations in the Chinese market in 2023:

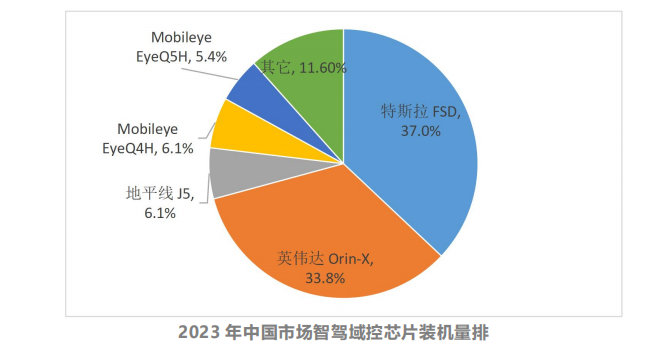

2 Market StructureFrom the perspective of market size, according to data from ICV, the global smart driving SoC market size in 2022 was 3.295 billion US dollars, with the Chinese market size reaching 1.505 billion US dollars, accounting for 45.68% of the global market. It is estimated that by 2024, the global smart driving SoC market size is expected to exceed 10 billion US dollars, and by 2027, it is projected to reach 28.306 billion US dollars, with a compound annual growth rate of 43.11%.According to statistics from the Gaishi Automotive Research Institute, in 2023, the number of passenger cars (excluding imports and exports) in the Chinese market equipped with smart driving domain controllers reached 1.839 million sets, a year-on-year increase of about 70%, with an installation rate of about 8.7%.Additionally, in the ranking of smart driving domain control chip installations in the Chinese market in 2023:

- The first place is Tesla’s FSD chip, with a shipment of about 1.208 million units, accounting for 37%;

- The second place is Nvidia’s Orin-X chip, with a shipment of 1.095 million units, accounting for 33.5%;

- The third place is Horizon’s Journey 5 chip, with a shipment of 200,000 units, accounting for 6.1%;

- The fourth place is Mobileye’s EyeQ4H chip, with a shipment comparable to J5, also around 200,000 units, accounting for 6.1%; the fifth place is Mobileye’s EyeQ5H chip, with a shipment of 174,000 units, accounting for 5.4%.

From the overall industry structure, currently, the market share of domestic smart driving SoC chips is still at a disadvantage. In 2023, foreign chip solutions account for a large proportion, totaling over 80%. Among them, Tesla’s FSD and Nvidia’s Orin-X alone capture over 70% of the market share. The FSD chip is self-developed and used by Tesla, with each vehicle equipped with 2 FSD chips.The Nvidia Orin-X chip is installed in many models, covering dozens of models from various manufacturers such as NIO, Xpeng, Li Auto, Zhiji, and Xiaomi.Among domestic smart driving SoC chips, the one with the largest shipment is the Journey 5 chip, which reached a shipment of 200,000 units in 2023, primarily equipped in the Li Auto L7/L8 Air and Pro versions and L9 Pro version; additionally, in February 2024, the J5 chip will go into mass production on the BYD Han EV Glory Edition.However, the smart driving SoC market structure has not yet stabilized, and domestic chip manufacturers have their advantages, still having opportunities to catch up. For example, compared to foreign chip manufacturers, domestic chip manufacturers have stronger local service capabilities, allowing them to quickly adapt to changes in local car manufacturers’ needs; additionally, the impact of geopolitics has also accelerated the pace of domestic chip replacement to some extent.

Source: Architect Technical Alliance

Welcome all angel round and A round enterprises from the entire automotive industry chain (including the power battery industry chain) to join the group (which will be recommended to over 1,000 automotive investors from top institutions);There are communication groups for leaders of innovative technology companies, as well as dozens of groups related to the automotive industry, automotive semiconductors, key components, new energy vehicles, smart connected vehicles, aftermarket, automotive investment, autonomous driving, vehicle networking, etc. Please scan the administrator’s WeChat to join the group (Please indicate your company name)