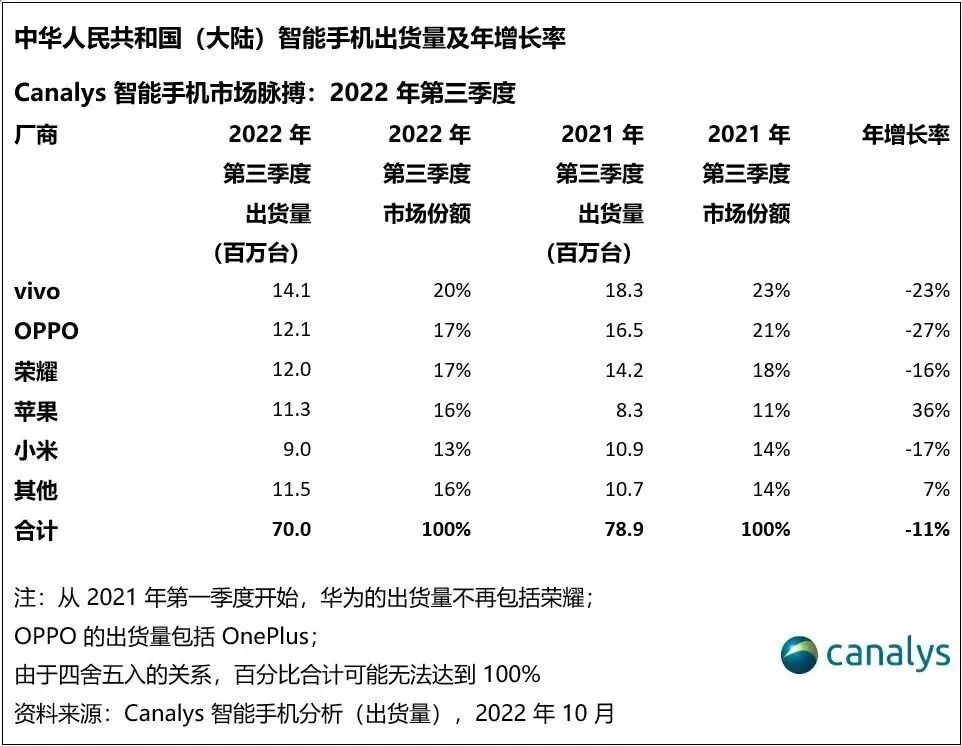

This year’s chip market can be summarized in one word: “divergence”.Taking the smartphone market in consumer electronics as an example, on one side, domestic smartphone manufacturers are clearing inventory, while on the other side, Apple is the only brand among the top five global smartphone brands to experience year-on-year growth.

This year’s chip market can be summarized in one word: “divergence”.Taking the smartphone market in consumer electronics as an example, on one side, domestic smartphone manufacturers are clearing inventory, while on the other side, Apple is the only brand among the top five global smartphone brands to experience year-on-year growth. Even within Apple, smartphone sales are diverging. The iPhone 14 series shows a polarized sales pattern, with the high-end Pro versions sold out, while the budget iPhone 14 has seen significant price cuts in the market, and the order cut ratio for Apple A15 and A16 chips is as high as 40-50%.On one hand, mid-to-low-end television prices are approaching “bargain prices”, while on the other hand, high-end television prices continue to rise. Samsung’s market share in the high-end television segment, priced over $2500 (approximately 17389 RMB), has increased to 51.1%, with a 37.5% share in the ultra-large television market of 75 inches and above.Additionally, there is a divergence in consumer electronics chips, with low-end volume chips and high-end chips showing different market trends; divergence between consumer electronics chips and automotive, industrial chips; and divergence between domestic and foreign trade…After the market cools down, divergence can be seen everywhere, and behind this divergence is the invisible hand’s scrutiny, reflection, and intervention after the market frenzy.

Even within Apple, smartphone sales are diverging. The iPhone 14 series shows a polarized sales pattern, with the high-end Pro versions sold out, while the budget iPhone 14 has seen significant price cuts in the market, and the order cut ratio for Apple A15 and A16 chips is as high as 40-50%.On one hand, mid-to-low-end television prices are approaching “bargain prices”, while on the other hand, high-end television prices continue to rise. Samsung’s market share in the high-end television segment, priced over $2500 (approximately 17389 RMB), has increased to 51.1%, with a 37.5% share in the ultra-large television market of 75 inches and above.Additionally, there is a divergence in consumer electronics chips, with low-end volume chips and high-end chips showing different market trends; divergence between consumer electronics chips and automotive, industrial chips; and divergence between domestic and foreign trade…After the market cools down, divergence can be seen everywhere, and behind this divergence is the invisible hand’s scrutiny, reflection, and intervention after the market frenzy.

01

Behind the Divergence in Consumer ElectronicsThe current semiconductor cyclical downturn in consumer electronics, dominated by smartphones, personal computers, and various audio and video devices, is most pronounced. While there is a downturn, divergence exists, with the most obvious manifestation being price.Chips with high circulation are dropping in price in the spot market, such as DDIC, MCU, PMIC, and memory chips, experiencing drastic price cuts and avalanche-like declines… Chip prices are gradually returning to normal from last year’s irrational levels.Chips with lower volume but higher value are still increasing in price.CPUs— Intel’s new prices will take effect on October 2 this year, with desktop and laptop processors seeing price increases of 10-20%. Intel aims to capture more market share and increase its average selling price (ASP) through this strategy.SoCs— Qualcomm and Marvell have also announced price increases, with Qualcomm’s new contract prices rising by 4%, and orders due for delivery in January 2023 will see price increases of nearly 10%. Marvell’s products will also see a 10% price increase starting January 1, 2023.Compared to Wi-Fi 5 and Wi-Fi 4 SoCs, Wi-Fi 6 SoCs have relatively stable prices due to strong demand, with suppliers like Realtek and Qualcomm unable to meet all order demands, while Broadcom’s networking chip prices will increase by 6%-8% starting January 2023.High-end 5G basebandchip growth is evident, with Strategy Analytics reporting a 40% year-on-year increase in revenue from 5G baseband chips in Q2 2022, a 16% increase in shipment volume, and a combination of high-end and premium 5G chips increasing ASP. Despite a weak market environment, the report suggests that baseband suppliers need to exercise pricing principles due to rising foundry costs, implying that prices can still rise.High-end chips do not constitute a large proportion of the entire consumer chip category, while the large-volume consumer chips are all falling, leading to a chaotic overall performance in consumer chips amidst headwinds.A similar divergence is occurring in the chip spot market, where domestic chip trade is particularly sluggish, with demand on hold, and salespeople are eager to clear inventory, competing on price and service, resulting in continuous price declines for many chips. In contrast, foreign trade has not seen a sharp reduction in order volume; it has merely returned to pre-pandemic norms, with consistent demand and less emphasis on social connections and relationships.Market pessimism has led to some consumer chips experiencing price increases in the “headwind” scenario, primarily because overall demand has dropped to a point where it cannot get worse, and price increases are used to boost revenue. However, most consumer chips, such as DDIC, MCU, PMIC, and memory chips circulating in the market, continue to decline in price due to sharply reduced demand.The market reflects that low-priced, high-volume chips are dropping in price, while low-volume, high-priced chips are increasing in price; overall, chip demand has decreased.

02

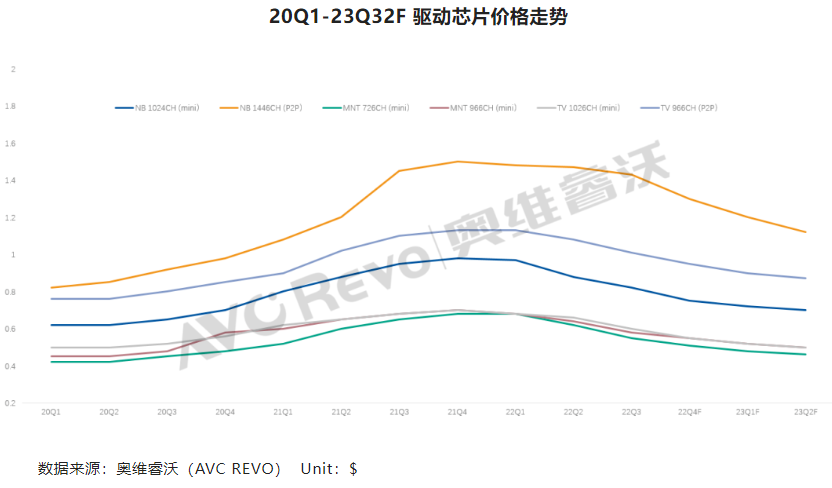

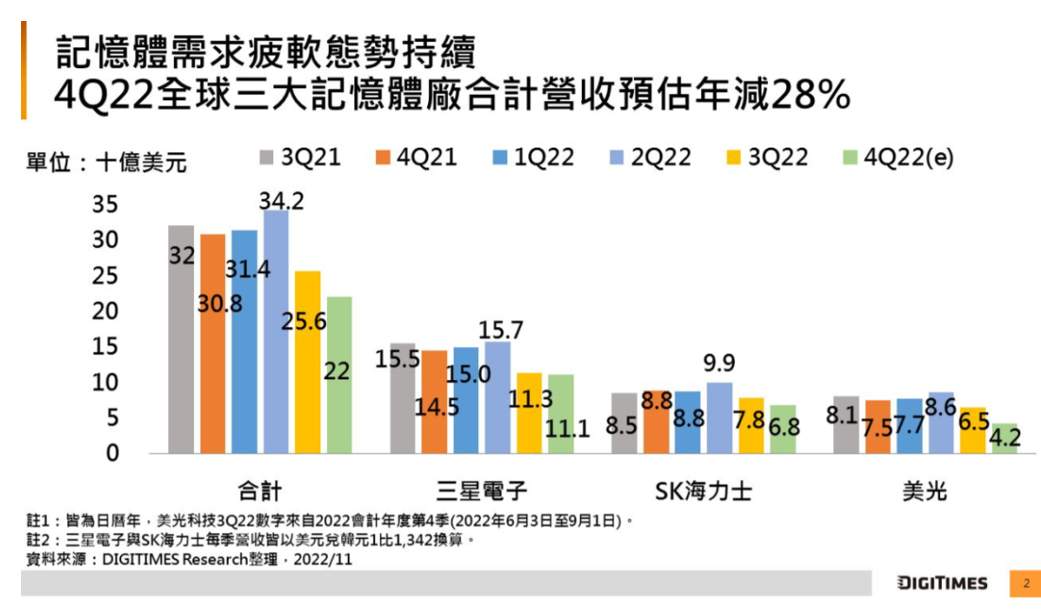

Overall Decline of Consumer ChipsAutomotive and Industrial Control Chips Remain StrongChips can be categorized based on different application markets into two types: consumer chips, which are primarily high-volume and widely circulated, such as display chips used in everything from 8K televisions to smartphones; and chips used in automotive and industrial applications, which must meet specific standards and parameters, have lower usage but higher unit value, such as automotive MCUs.The current chip market shows a decline in consumer chips, but strength in automotive and industrial sectors.Let’s first look at the high-volume chips: DDIC (Display Driver IC), passive components, analog chips, and memory chips.The panel display driver IC industry is the first to feel the consumer downturn, with panel prices having dropped for 15 consecutive months from the second half of 2021 to October this year, with mainstream panel prices nearly halving, putting pressure on DDIC prices. According to AVC Revo data, DDIC prices fell by 5%-10% in Q3 this year, and this price decline cycle is expected to continue. The overall consumer electronics market is struggling, but in niche markets, Mini LED screens are collectively gaining traction, with LED driver IC manufacturers actively developing Mini LED driver chips, such as the automotive driver ICs from Novatek, which have significantly outperformed their consumer product lines. Passive componentshave high shipment volumes, with global MLCC leader Murata serving clients including iPhone, Samsung, and mainland Chinese smartphone brands, playing a pivotal role in the smartphone and consumer electronics industries. Murata has repeatedly lowered its global smartphone production forecast for this fiscal year, with President Nakajima warning that demand for smartphones in the Greater China region is unlikely to show signs of recovery this year, and even next year’s sales are expected to continue the downward trend. Samsung Electro-Mechanics, the second-largest MLCC manufacturer globally, has seen its MLCC factory’s operating rate in the Philippines drop to 40%. However, in the automotive and industrial sectors, manufacturers’ high-end product orders remain stable, and a new industry cycle is expected to begin.It is said that analog chips are more resilient than digital chips, but this year, even analog chips related to consumer electronics cannot escape the severe downturn. The market price of consumer analog chips is returning to normal, and high-end analog chips are beginning to reflect weak demand. Texas Instruments, a leader in analog chips, has seen demand from consumer electronics (24%) weaken, and its largest downstream application (41%) in the industrial sector is also experiencing weak demand. However, in the automotive-grade analog chip sector, Texas Instruments reported a strong Q3 automotive market, with revenue growth of about 10%.Memory chipsare perhaps the least favored in the semiconductor market. WSTS reports that the segment with the largest decline in market share, accounting for over 20%, is memory chips, which are expected to decrease by 17% compared to 2022, dragging down the overall growth of the semiconductor market. In Q3 this year, contract prices for DRAM and NAND flash fell by 15% and 28%, respectively, and these two types of chips are expected to continue to decline in price in Q4 and throughout next year.Samsung Electronics has stated that it has high inventory levels of mobile storage chips and is working to reduce inventory. Global memory chip manufacturers are facing a dual decline in volume and price, and are navigating through the winter by cutting costs and reducing production capacity. At the same time, memory chip giants are increasingly focusing on the automotive market, launching corresponding automotive storage chips, with Micron estimating that the DRAM and NAND required for fully autonomous vehicles is 30 to 100 times that of non-autonomous vehicles.

Passive componentshave high shipment volumes, with global MLCC leader Murata serving clients including iPhone, Samsung, and mainland Chinese smartphone brands, playing a pivotal role in the smartphone and consumer electronics industries. Murata has repeatedly lowered its global smartphone production forecast for this fiscal year, with President Nakajima warning that demand for smartphones in the Greater China region is unlikely to show signs of recovery this year, and even next year’s sales are expected to continue the downward trend. Samsung Electro-Mechanics, the second-largest MLCC manufacturer globally, has seen its MLCC factory’s operating rate in the Philippines drop to 40%. However, in the automotive and industrial sectors, manufacturers’ high-end product orders remain stable, and a new industry cycle is expected to begin.It is said that analog chips are more resilient than digital chips, but this year, even analog chips related to consumer electronics cannot escape the severe downturn. The market price of consumer analog chips is returning to normal, and high-end analog chips are beginning to reflect weak demand. Texas Instruments, a leader in analog chips, has seen demand from consumer electronics (24%) weaken, and its largest downstream application (41%) in the industrial sector is also experiencing weak demand. However, in the automotive-grade analog chip sector, Texas Instruments reported a strong Q3 automotive market, with revenue growth of about 10%.Memory chipsare perhaps the least favored in the semiconductor market. WSTS reports that the segment with the largest decline in market share, accounting for over 20%, is memory chips, which are expected to decrease by 17% compared to 2022, dragging down the overall growth of the semiconductor market. In Q3 this year, contract prices for DRAM and NAND flash fell by 15% and 28%, respectively, and these two types of chips are expected to continue to decline in price in Q4 and throughout next year.Samsung Electronics has stated that it has high inventory levels of mobile storage chips and is working to reduce inventory. Global memory chip manufacturers are facing a dual decline in volume and price, and are navigating through the winter by cutting costs and reducing production capacity. At the same time, memory chip giants are increasingly focusing on the automotive market, launching corresponding automotive storage chips, with Micron estimating that the DRAM and NAND required for fully autonomous vehicles is 30 to 100 times that of non-autonomous vehicles. The above image shows that revenue for memory chip giants Samsung, SK Hynix, and Micron has been continuously declining since Q2 this year, with a projected year-on-year revenue decrease of 28% by Q4.Next, let’s look at the performance of MCUs, CIS (CMOS Image Sensors), and networking chips.In 2020, consumer electronics accounted for the highest proportion (26%) among the five major application areas of MCU products in China. Last year, during the chip shortage, leading consumer MCUs such as ST, TI, NXP, and Microchip saw their prices skyrocket, but this year, prices in the spot market have experienced a “collapse”. Some MCUs have dropped from hundreds to double digits in just three months, with declines exceeding 50%, gradually returning to normal prices.In contrast, automotive MCUs still have room for price increases. According to Sigmaintell’s statistics and forecasts, in Q4 2022, automotive MCU prices are expected to increase by 2%-5% depending on the degree of material shortages for different models. The demand for automotive MCUs is expected to rise significantly in 2023 due to the continued growth of new energy vehicles, making it difficult for automotive MCU prices to decline in the short term.

The above image shows that revenue for memory chip giants Samsung, SK Hynix, and Micron has been continuously declining since Q2 this year, with a projected year-on-year revenue decrease of 28% by Q4.Next, let’s look at the performance of MCUs, CIS (CMOS Image Sensors), and networking chips.In 2020, consumer electronics accounted for the highest proportion (26%) among the five major application areas of MCU products in China. Last year, during the chip shortage, leading consumer MCUs such as ST, TI, NXP, and Microchip saw their prices skyrocket, but this year, prices in the spot market have experienced a “collapse”. Some MCUs have dropped from hundreds to double digits in just three months, with declines exceeding 50%, gradually returning to normal prices.In contrast, automotive MCUs still have room for price increases. According to Sigmaintell’s statistics and forecasts, in Q4 2022, automotive MCU prices are expected to increase by 2%-5% depending on the degree of material shortages for different models. The demand for automotive MCUs is expected to rise significantly in 2023 due to the continued growth of new energy vehicles, making it difficult for automotive MCU prices to decline in the short term. CIShas been the largest product category in the optoelectronic semiconductor market over the past 20 years (accounting for 40% of annual sales), but the CIS market is currently experiencing its first decline in 13 years. Analyst Ming-Chi Kuo stated earlier this year that the top five CIS suppliers for Chinese Android brands have total inventories exceeding 550 million units. Related chip company Weir shares reported a 16.01% year-on-year decline in revenue in Q3 2022, with net profit down 38.92%. Sunny Optical’s revenue in the first half of the year fell 14% year-on-year, with net profit down 49.5%, and the shipment volume of mobile camera lenses decreased by 9.1% year-on-year.Automotive CIS is a key focus for chip companies in the future, with Weir shares reporting significant growth in sales revenue from the automotive market in the first half of this year, with the automotive business’s share of image sensors increasing from 14% at the end of 2021 to 22%, continuing to maintain a rapid growth trend.Networking chipsmainly include applications for 5G mobile networks, wireless networks WiFi 6, broadband, switches, etc. Last year, networking chips faced severe shortages, but now manufacturers are actively reducing inventory. Industry insiders in first-line IC channels have stated that inventory clearance is expected to return to normal by the end of Q2 2023, with some distributors also bearing the inventory of chip manufacturers, reducing average gross margins. Networking chip manufacturer Realtek’s revenue in November dropped to approximately 7.296 billion yuan, a month-on-month decrease of 9.81% and a year-on-year decrease of 20.57%, due to ongoing adjustments in PC inventory, with monthly revenue hitting a nearly 21-month low.However, automotive and industrial control-related networking chips are thriving, with automotive chip giant NXP reporting the fastest growth in total revenue in Q3, with automotive, industrial, and IoT businesses growing by 24% and 17% year-on-year, respectively.Whether it is DDIC, passive components, analog chips, memory chips, or MCUs, CIS, networking chips, all show a trend of continuous price declines for high-volume consumer chips, while low-volume automotive and industrial control chips exhibit price increases.Due to these various reasons, there have been continuous reports of traditional foundries closing down this year, with factories producing headphones, small appliances, and other products being both created and abandoned by the market.

CIShas been the largest product category in the optoelectronic semiconductor market over the past 20 years (accounting for 40% of annual sales), but the CIS market is currently experiencing its first decline in 13 years. Analyst Ming-Chi Kuo stated earlier this year that the top five CIS suppliers for Chinese Android brands have total inventories exceeding 550 million units. Related chip company Weir shares reported a 16.01% year-on-year decline in revenue in Q3 2022, with net profit down 38.92%. Sunny Optical’s revenue in the first half of the year fell 14% year-on-year, with net profit down 49.5%, and the shipment volume of mobile camera lenses decreased by 9.1% year-on-year.Automotive CIS is a key focus for chip companies in the future, with Weir shares reporting significant growth in sales revenue from the automotive market in the first half of this year, with the automotive business’s share of image sensors increasing from 14% at the end of 2021 to 22%, continuing to maintain a rapid growth trend.Networking chipsmainly include applications for 5G mobile networks, wireless networks WiFi 6, broadband, switches, etc. Last year, networking chips faced severe shortages, but now manufacturers are actively reducing inventory. Industry insiders in first-line IC channels have stated that inventory clearance is expected to return to normal by the end of Q2 2023, with some distributors also bearing the inventory of chip manufacturers, reducing average gross margins. Networking chip manufacturer Realtek’s revenue in November dropped to approximately 7.296 billion yuan, a month-on-month decrease of 9.81% and a year-on-year decrease of 20.57%, due to ongoing adjustments in PC inventory, with monthly revenue hitting a nearly 21-month low.However, automotive and industrial control-related networking chips are thriving, with automotive chip giant NXP reporting the fastest growth in total revenue in Q3, with automotive, industrial, and IoT businesses growing by 24% and 17% year-on-year, respectively.Whether it is DDIC, passive components, analog chips, memory chips, or MCUs, CIS, networking chips, all show a trend of continuous price declines for high-volume consumer chips, while low-volume automotive and industrial control chips exhibit price increases.Due to these various reasons, there have been continuous reports of traditional foundries closing down this year, with factories producing headphones, small appliances, and other products being both created and abandoned by the market.

03

Good Times for Upstream Wafer Factories Are OverWith a large number of chips dropping in price, the chip design industry is cutting orders to minimize losses, even at a loss. The wave of order cuts from end-users and chip design companies is ultimately transmitted to wafer foundries.The production capacity of consumer chips is concentrated in 8-inch wafers, which have been significantly impacted by drastic order cuts from downstream television, PC, and smartphone manufacturers, leading to a decline in capacity utilization rates for 8-inch wafer factories in the second half of this year. The demand for DDIC continues to be revised downward without improvement, and related SoCs, CIS, and PMIC chips are also adjusting inventory and reducing wafer foundry orders.According to Sigmaintell’s research data, starting from Q2 2022, wafer foundry capacity utilization rates began to decline due to order cuts from downstream customers. Due to the relatively simple product structure, 8-inch wafer factories are more affected than 12-inch wafer factories. TrendForce predicts that in Q4, the revenue growth of most of the top ten wafer foundry companies will converge or decline, marking the end of the previous two years of quarterly growth in the wafer foundry industry.Reports from Taiwan media indicate that in Q1 2023, revenue for TSMC, the largest chip foundry, is expected to decline by 10%-15% quarter-on-quarter, primarily due to a significant reduction in new orders in the first half of the year. Additionally, according to Taiwan media DIGITIMES, TSMC’s overall capacity utilization rate for 45nm to 3nm processes is expected to drop to around 75% in the first half of 2023.World Advanced and Powerchip’s capacity utilization rates fell to around 90% in Q3 2022, and a similar decline is expected in Q4 2022. SMIC’s smartphone business share has significantly declined compared to the same period last year, and its revenue is expected to decrease by 13%-15% quarter-on-quarter in Q4 this year. In South Korea, wafer factory operating rates have sharply dropped to 80% starting in Q4, and are expected to decline further in the first half of 2023.Declining capacity utilization rates are followed by waves of layoffs.To cut costs, GlobalFoundries, the fourth largest foundry globally and the largest in the U.S., announced plans to lay off nearly 800 employees globally in December, accounting for 5.7% of its 14,000 global workforce. Hundreds of employees at chip manufacturer Intel will lose their jobs next month, and factory workers globally are being offered unpaid leave options.

04

ConclusionThe market’s feedback is always lagging. During last year’s most frenzied market conditions, many consumer electronics products had already seen a decline in sales. From the decline in consumer electronics sales to foundries closing down, to the chip spot market offloading, and finally to the performance decline of some chip manufacturers, the order cuts have reached upstream wafer foundries.After several long months, the “pass-the-parcel” game of chip industry inventory seems to be coming to an end, with market divergence showing both scarcity and abundance, while upstream wafer foundries ultimately cannot withstand the tide, and alarms have been sounded.Divergence is like the market actively seeking to preserve the genuine while discarding the false. The true demand is like rocks by the sea, present when the tide is high, and still visible when the tide recedes, only more prominent.

Contact Chip Superwoman Hua Jie on WeChat

Let’s discuss the chip market

Recommended Reading:

▶ TI, NXP, ADI, and others in November chip market: Who is raising prices? Who is reducing inventory?

▶ Price drop of 2500 yuan in one month! Identification of popular chip part numbers from TI, ST, NXP

▶ After three years of growth, how will the semiconductor industry recover from the downturn?

▶ We haven’t connected everything in the chip industry yet, but we have connected to vehicles first

▶ The fire of semiconductor order cuts, layoffs, and bankruptcies is spreading

Click to view past content

↓↓↓