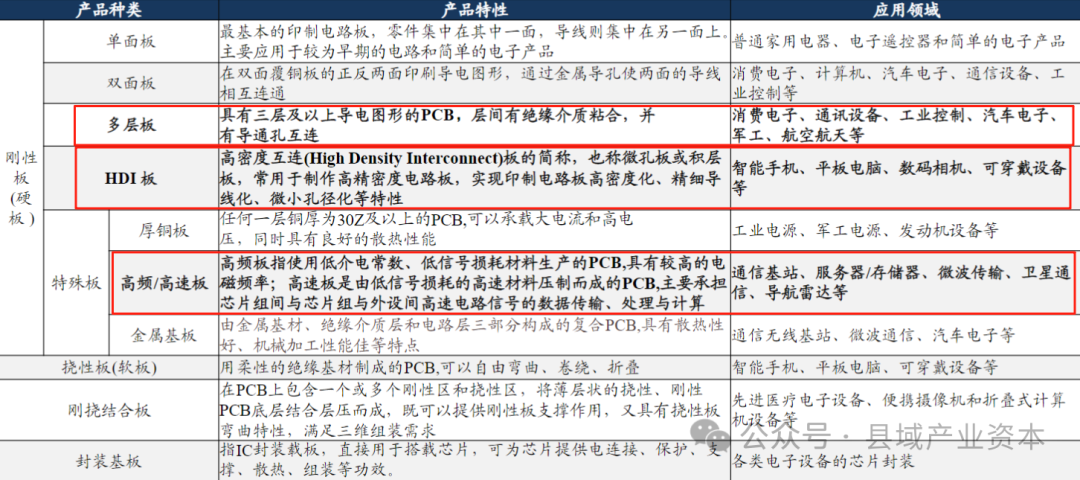

PCB Classification

The PCB industry is showing a significant trend of product structure upgrading. Depending on the manufacturing process and application scenarios, PCBs can be classified into categories such as double-sided boards, HDI boards, high-frequency and high-speed boards, flexible boards (soft boards), and packaging substrates. Among these, HDI, high-frequency/high-speed boards, and multilayer boards are becoming the core growth areas of this industry cycle.

1) HDI boards possess technical characteristics such as high-density wiring and micro-hole diameters, primarily used in high-end consumer electronics like smartphones, wearables, and tablets. HDI boards have become a key interconnection structure in AI servers; for example, in the Nvidia GB200 architecture, both the Compute Tray (OAM module) and the Switch Tray widely use multi-tier HDI boards to support high-density, high-speed signal connections. In simple terms, HDI boards are mainly used in high-end consumer electronics and automotive electronics.

2) High-frequency/high-speed boards meet the requirements for high-speed and high-frequency signal transmission in devices such as servers, switches, and communication base stations, playing a crucial role in the construction of data centers and edge computing nodes. The technical barriers and unit prices are significantly higher than traditional rigid boards; in simple terms, high-frequency/high-speed boards are mainly used in communication base stations.

3) Multilayer boards (≥18 layers) have become a key structure in AI server motherboards and high-performance computing modules due to their support for complex wiring and high power management, showing explosive growth potential. In simple terms: 18+ layer multilayer boards are mainly used in AI servers and high-speed switches.

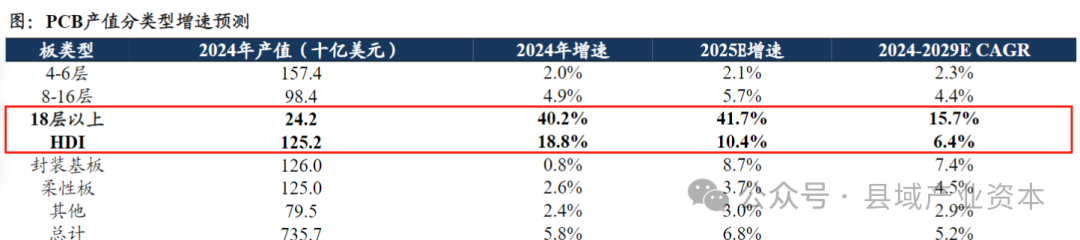

18 layer multilayer boards and HDI boards are about to explode in demand.

Multilayer boards with more than 18 layers and HDI boards are becoming the core beneficiary categories. According to Prismark’s forecast: by 2025, the output value of multilayer boards with more than 18 layers is expected to grow by 41.7% year-on-year, while HDI boards will grow by 10.4%; from 2024 to 2029, they will maintain high growth rates of 15.7% and 6.4%, respectively.

From the perspective of PCB product structure, based on output value as a statistical measure, it is expected that 4-6 layer multilayer boards will still account for the largest share of global PCB types by 2025, with an expected output value growth of +2% year-on-year to $16.069 billion. Benefiting from the increased demand for AI computing power, related PCB product specifications are undergoing significant upgrades, which will drive rapid growth in the output value of multilayer boards with more than 18 layers and HDI boards, with year-on-year growth rates expected to reach 41.7% and 10.4%, respectively, by 2025.

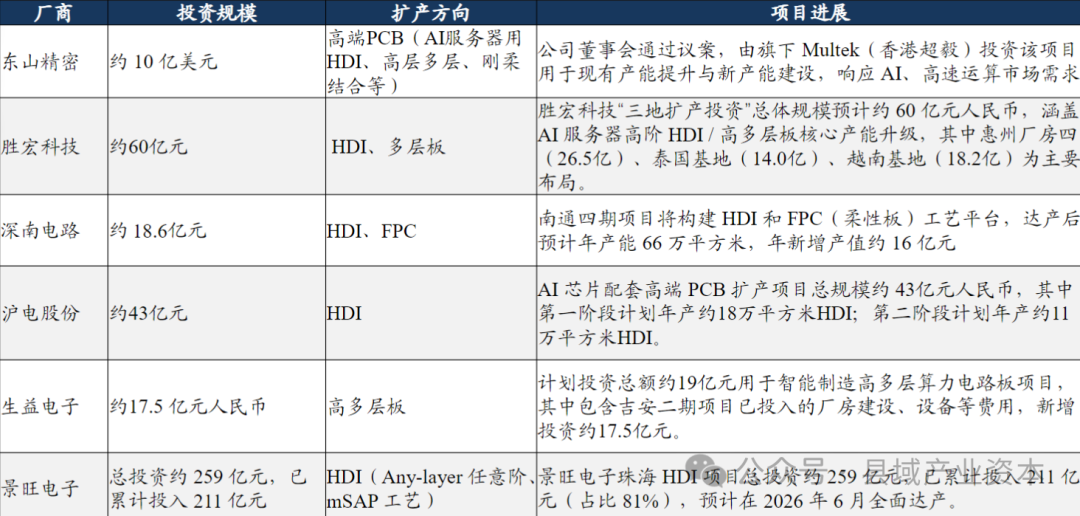

Domestic manufacturers are actively laying out high-end PCBs.

Mainstream domestic PCB manufacturers are accelerating capacity expansion around high-end HDI and high-layer multilayer boards, focusing on high-performance application scenarios such as AI servers and intelligent computing centers. Companies like Dongshan Precision, Shenghong Technology, Shenzhen Circuit, Huadian Co., Shunyi Electronics, and Jingwang Electronics are all advancing high-end PCB investment projects aimed at AI, indicating a clear trend towards high-end development in the industry.

Follow me to focus on the development of the technology industry and explore the technology industry in China!

Follow me to focus on the development of the technology industry and explore the technology industry in China!