For a wealth of sensor knowledge and industry reports, please reply with the keyword 【Data Download】 in the public account dialog box to obtain some materials for viewing《100+ Professional Knowledge Materials on Sensors, There’s Always One Suitable for You~》This is👇Follow me, and remember to click the menu bar in the upper right corner•••👉Set as a Star⭐

Recently, “China’s first MEMS chip stock” Minxin Co., Ltd. released its performance report and investor relations record.

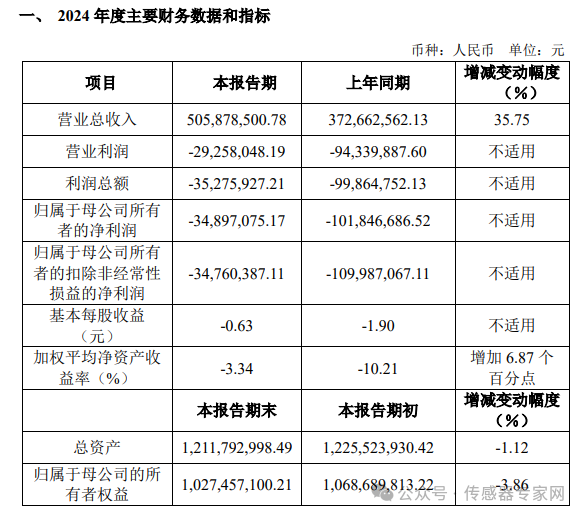

The report shows that Minxin Co., Ltd. achieved a revenue of 506 million yuan in 2024, a year-on-year surge of 35.75%. In the report, Minxin explained the reasons for the significant performance increase. Additionally, in the investor relations record, Minxin revealed its latest strategic layout and recent progress in MEMS pressure sensors and other areas. Details are as follows:

Explanation of Operating Performance and Financial Status

(1) Operating conditions, financial status, and main factors affecting operating performance during the reporting period

During the reporting period, the company achieved total operating revenue of 505.8785 million yuan, an increase of 35.75% year-on-year; achieved a net profit attributable to the parent company of -34.8971 million yuan, a decrease in loss of 66.9496 million yuan year-on-year; achieved a net profit attributable to the parent company after deducting non-recurring gains and losses of -34.7604 million yuan, a decrease in loss of 75.2267 million yuan year-on-year.

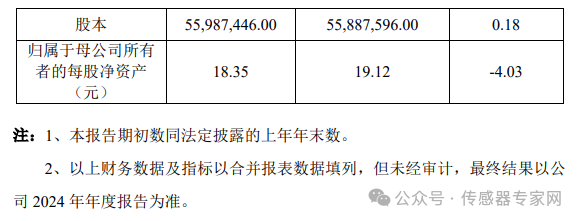

At the end of the reporting period, the company’s total assets were 1.211793 billion yuan, a decrease of 1.12% compared to the beginning of the reporting period, and the equity attributable to the parent company was 1.0274571 billion yuan, a decrease of 3.86% compared to the beginning of the reporting period.

During the reporting period, the company’s operating performance continued to improve, with the revenue for the second, third, and fourth quarters of 2024 reaching historical highs. The company has continuously focused on new products, especially the pressure product line, which has seen significant growth, effectively improving the company’s product structure and driving the continuous expansion of revenue scale.

At the same time, during the reporting period, the profitability of the company’s products improved, with the net profit loss amount significantly narrowing compared to the same period last year, achieving a quarterly turnaround in the fourth quarter of 2024. The main reasons are the substantial increase in overall sales and the improvement in the overall gross profit margin of products. Notably, the gross profit margin of products in the third and fourth quarters of 2024 reached the highest quarterly levels in nearly two years. The main reasons for the improvement in the overall gross profit margin of the company’s products are as follows:

(1) The sales proportion of high-margin new products, represented by the pressure product line, has gradually increased, raising the overall product gross margin of the company;

(2) The company’s continuous cost reduction and efficiency improvement measures have yielded good results, gradually lowering product production costs;

(3) The smooth release of production capacity from the company’s fundraising projects has led to an increase in product output, thereby generating economies of scale, gradually reducing unit costs.

(2) Main reasons for changes in relevant financial data and indicators exceeding 30%

1. During the reporting period, the company’s total operating revenue increased by 35.75%, mainly due to the company’s sustained R&D investment and market promotion in new product areas over the years, achieving significant breakthroughs in pressure products, gaining market recognition, and the revenue of the pressure product line increased significantly compared to the same period last year.

2. During the reporting period, the company’s operating profit, total profit, and net profit attributable to the parent company decreased by losses of 65.0818 million yuan, 64.5888 million yuan, and 66.9496 million yuan year-on-year, respectively. The company’s net profit loss amount significantly narrowed compared to the same period last year, mainly due to the substantial increase in overall sales and the improvement in the overall gross profit margin of the company’s products.

3. During the reporting period, the net profit attributable to the parent company after deducting non-recurring gains and losses decreased by a loss of 75.2267 million yuan, earnings per share increased by 1.27 yuan/share, and the weighted average return on net assets increased by 6.87 percentage points. The main reason is the significant decrease in net profit attributable to the parent company year-on-year.

1. We see that the company announced its performance report, and the company should have achieved quarterly profitability in the fourth quarter. Which sectors are mainly growing?

Answer: In 2024, all three major product lines of the company have seen varying degrees of growth. The main acoustic products have seen rapid shipment growth, and the newly added high-margin products have also performed well. In other areas, medical, automotive, and IMU sectors are also gradually starting to receive orders. Throughout 2024, the company’s profit losses are gradually narrowing. As a company with MEMS full industry chain R&D capabilities and rare multi-category MEMS product R&D and production capabilities in China, we have been committed to building a comprehensive MEMS enterprise. After previous accumulation, products from multiple product lines have gradually entered the introduction and mass production stages in their respective market fields. 2024 is a year of comprehensive recovery for the company.

2. What is the current downstream proportion of acoustic products? Who are the main customers?

Answer: In the acoustic product line, mobile phones and headphones account for nearly 60% of the shipment volume of acoustic sensors. Other applications are concentrated in smart home devices, laptops, wearable devices, etc. The customers for mobile phones and headphones are mainly brand manufacturers and ODM manufacturers, with some being white-label customers.

3. Will the launch of AI and other products require upgrades for the company’s silicon microphone products? Will the value increase?

Answer: Through communication with top domestic mobile phone manufacturers and AI product-related manufacturers, we understand that they have a clear demand for silicon microphones with higher signal-to-noise ratios. Therefore, we already have corresponding products, and we are waiting for downstream to switch plans. New products will bring price increases, and the average value of products will also see a considerable increase.

4. There are many companies making silicon microphones in China; is the competition quite fierce?

Answer: Currently, the top ten MEMS companies globally have relatively single MEMS product lines, and the same is true domestically. This is where Minxin differs from these companies. We have always hoped to build the company into a platform-type company, continuously committed to multi-product line layout. Additionally, Minxin started with chip design and possesses its own technical processes in all links, making it one of the few full industry chain enterprises in China. Self-developed chips have already been supplied to brand customers, and domestically, Minxin is leading in competition across all links.

5. What is the current supply situation of the barometer products? Will this product have applications in other fields?

Answer: Currently, the company has two barometer products shipped to brand customers, which are used in wearable devices. In the second half of the year, they are expected to be introduced in high-end mobile phones. In addition, the product samples for overseas wearable customers are also undergoing successful testing, and shipments are expected to gradually begin in the second half of this year.

6. What is the current penetration rate and gross margin situation of the micro differential pressure products?

Answer: Currently, the micro differential pressure products are still ramping up quickly, and we are also upgrading the products and gradually increasing the share of high-end products. Additionally, we will improve gross margins through cost reduction and product structure adjustments.

What do you think of this article? Feel free to leave comments and discuss below this content on the Sensor Expert Network public account, or engage in discussions in China’s largest sensor community: Sensor Exchange Circle.

What do you think of this article? Feel free to leave comments and share!

Share and click to view, let more people understand the dynamics of the Chinese sensor industry!

Starred content = content you care about, according to the recommendation principles of public accounts, if you do not set the Sensor Expert Network public account homepage 【as a star】, you will not be able to receive the latest information in the sensor industry in a timely manner!

Source: Sensor and IoT Industry Alliance, Sensor Expert NetworkDisclaimer: The content of this article reflects the author’s personal views and does not represent the views or positions of the Sensor Expert Network. If there are any infringements or other matters, please contact via WeChat: MM380702. For more opinions, everyone is welcome to leave comments.If you have submission or interview needs, please send an email to:[email protected].