Click the mini program to view the original research report

Core Insights

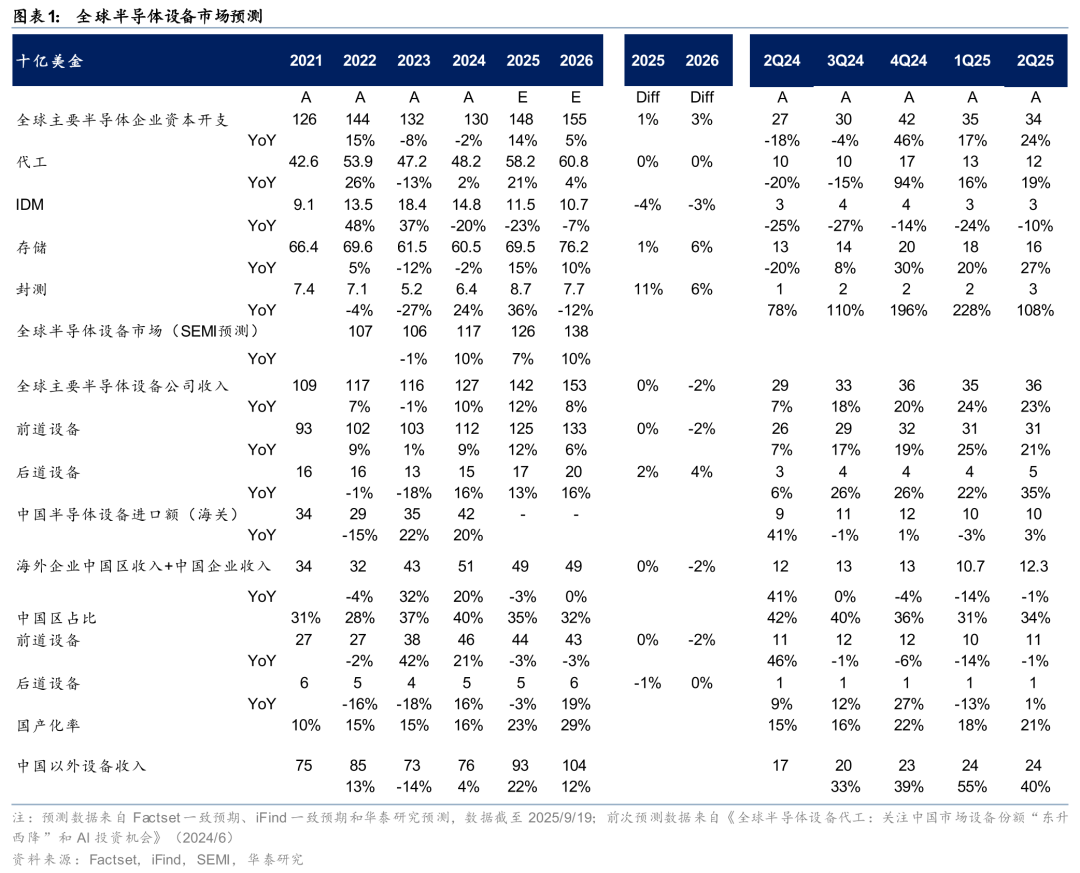

Based on statistics from the performance of 32 global semiconductor manufacturing companies and 20 equipment companies, the total revenue of global equipment companies in 2Q25 increased by24% year-on-year to34 billion USD. Among them, the overseas market is dominated by AI-related investments, with a market size growth of40% year-on-year, particularly notable in the growth of backend equipment such as testers. Affected by last year’s high base, the Chinese market saw a slight decline of1% in 1H25, showing different cyclical characteristics compared to overseas markets. Based on the analysis of the guidance from the above companies, we believe that the total semiconductor capital expenditure for 2025 will increase by14% year-on-year, reaching148 billion USD; the global equipment market size is expected to grow by12% year-on-year, reaching142 billion USD. We believe that: 1) In 2H25, the Chinese market is expected to continue an investment cycle dominated by advanced processes, and we are optimistic about the investment opportunities for local equipment companies to increase their market share. 2) The overseas market may enter a period of overall slowdown. We recommend paying attention to changes in the investment pace of major companies such as Intel and investment opportunities related to AI demand.

Chinese Market: The localization rate continues to improve, and the performance of local equipment shows differentiation

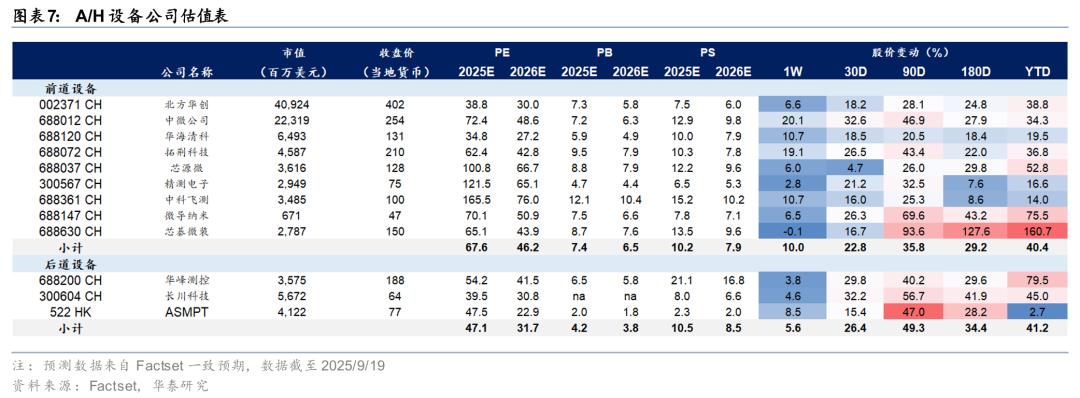

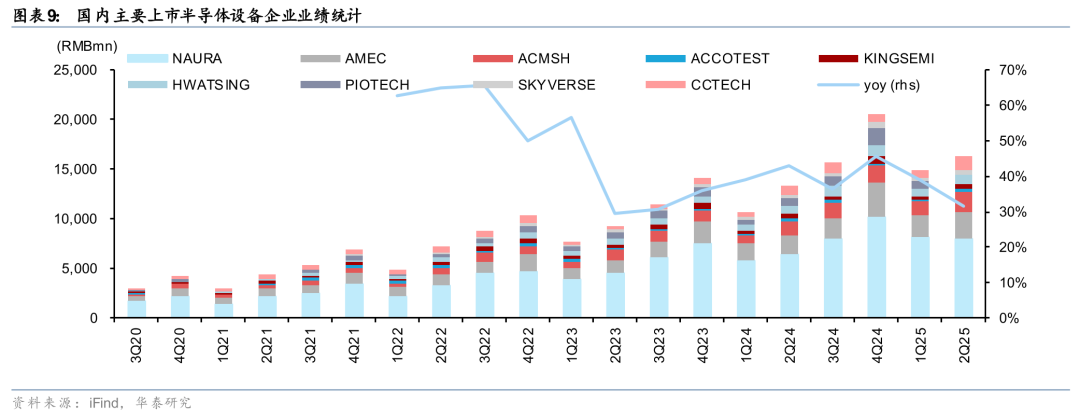

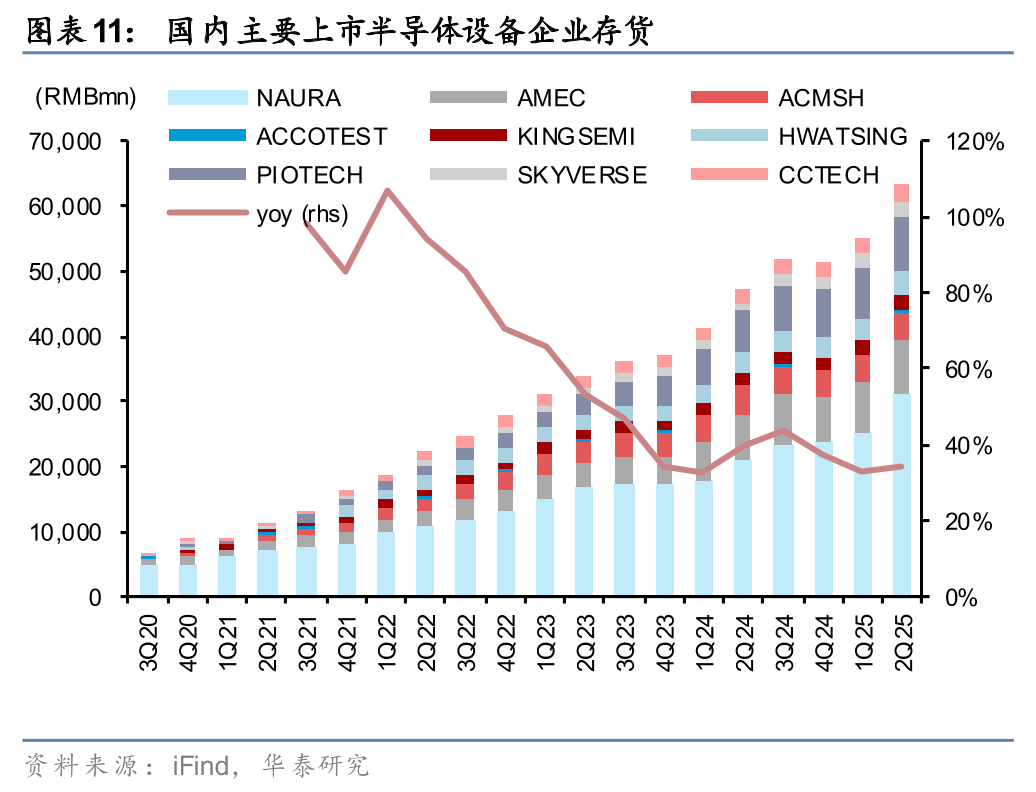

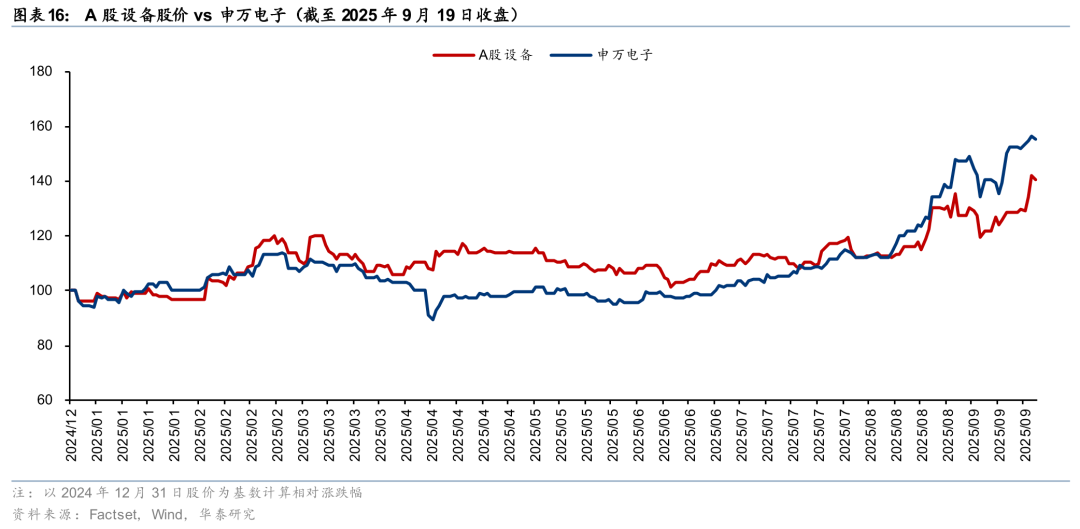

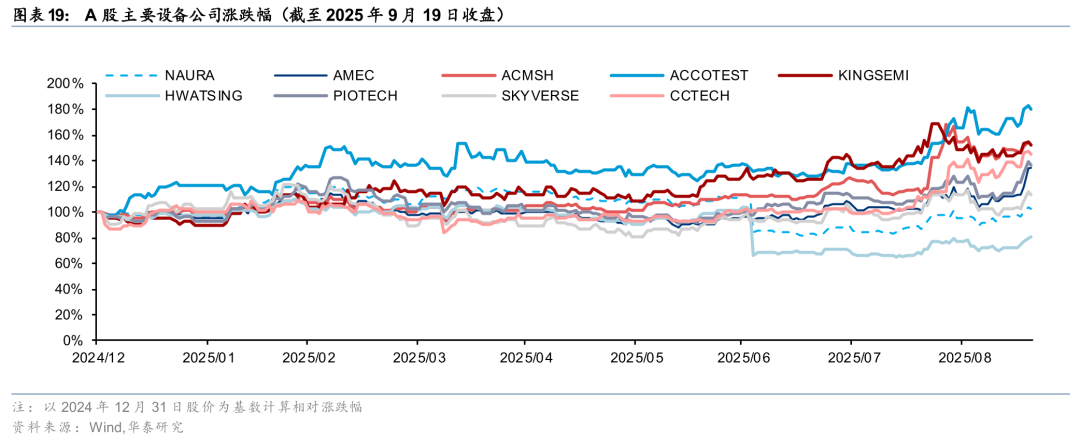

In 2Q25, the size of the Chinese equipment market slightly declined by1% year-on-year, while the localization rate of semiconductor equipment increased by6 percentage points to21%. We observed that the performance of leading local companies is differentiated; for example, the revenue and net profit attributable to the parent company of Zhongwei Company in 2Q25 increased by51.3% and46.8%, respectively, while the revenue and net profit attributable to the parent company of North Huachuang increased by22.5% and decreased by-1.6%. Since the beginning of the year, the stock prices of major A-share equipment companies have underperformed the Shenwan Electronics index. In the short term, the capital expenditure rhythm of storage and the yield of advanced logic are the main factors affecting the delivery rhythm and performance of local equipment. Looking ahead, with the continued investment in advanced logic and storage and technological breakthroughs in wafer fabs, we are optimistic about the long-term increase in the localization rate of equipment.

Overseas Market: Q2 overseas equipment market size shows steady growth, but growth drivers may weaken marginally in the second half

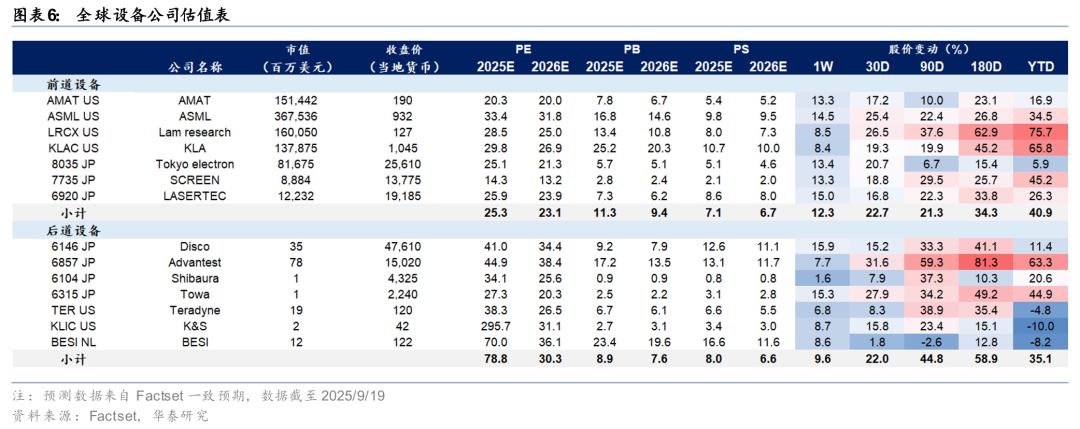

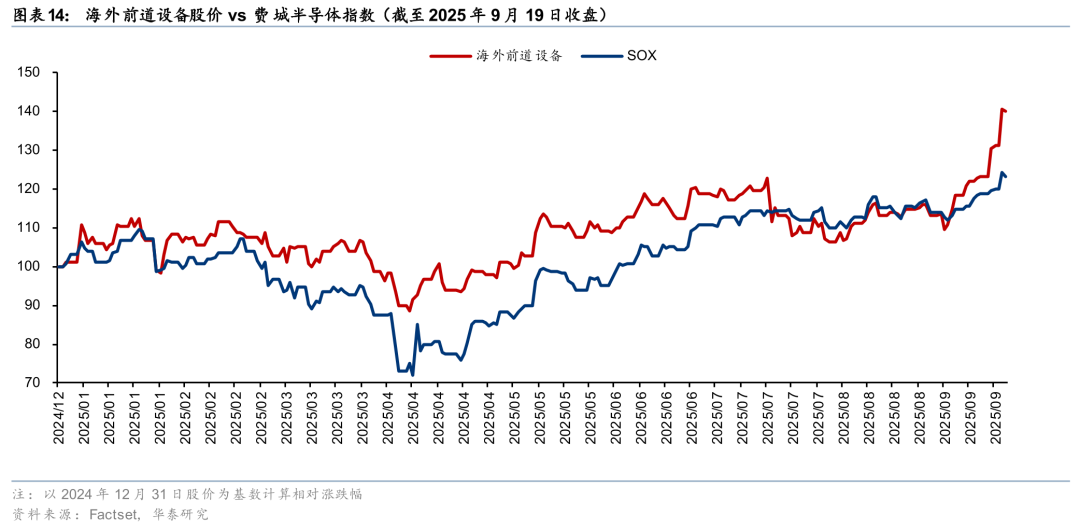

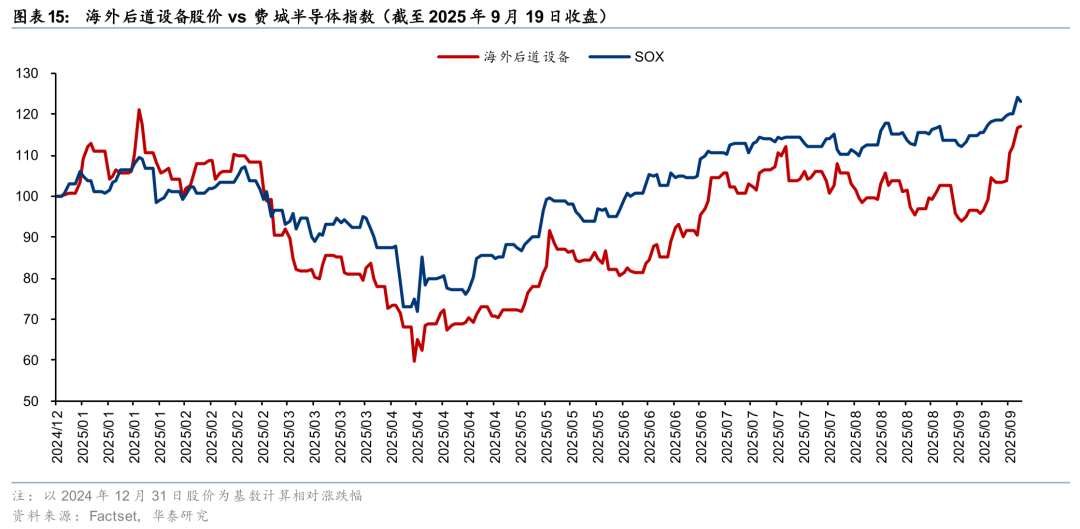

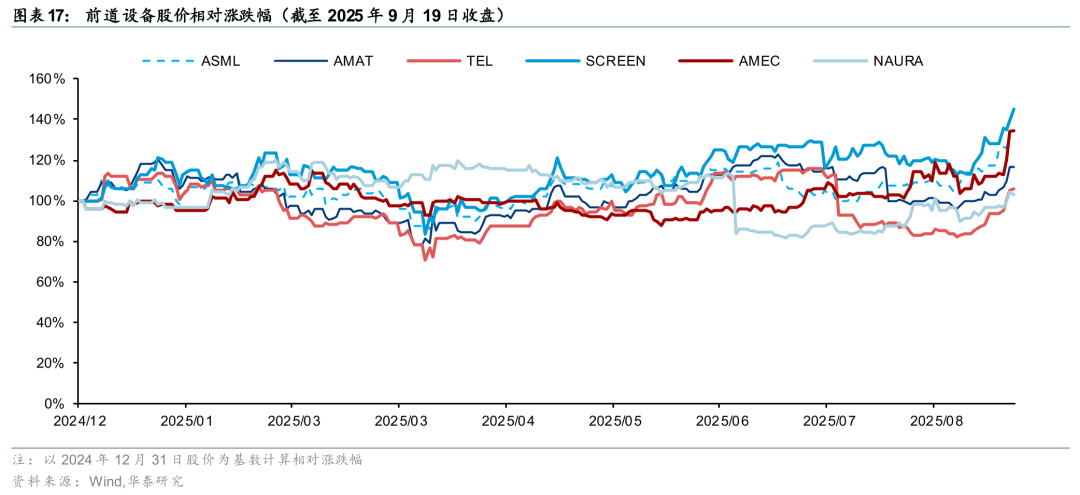

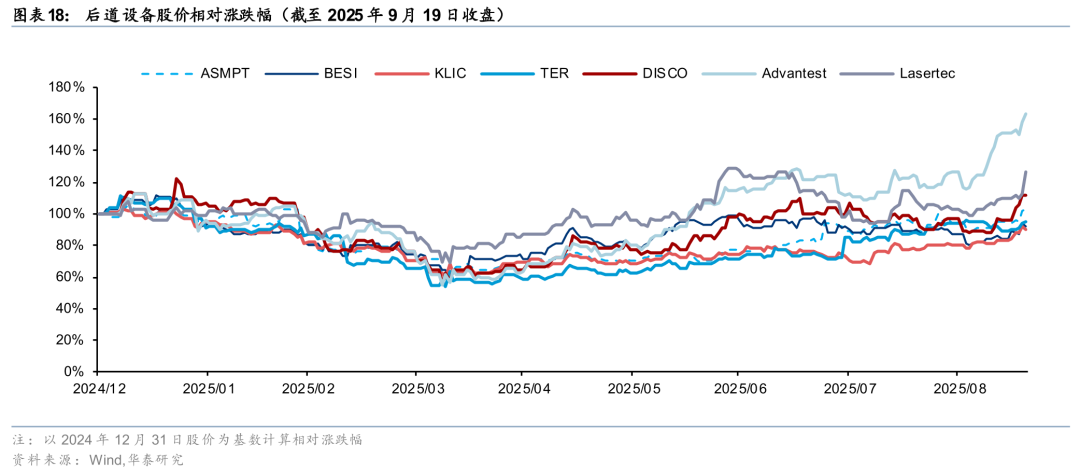

In 2Q25, the overseas market continued to be driven by AI demand, with major global equipment companies achieving approximately40% year-on-year growth in markets outside of China. However, at the same time, AMAT pointed out in its earnings call that due to market concentration and the timing of wafer fab construction, the demand from leading customers presents a non-linear pattern. This has led to longer decision-making times for customer orders, thereby reducing the company’s short-term visibility; Advantest noted in its earnings call that despite stronger-than-expected performance in the first quarter, it raised its full-year guidance for FY2025, while expecting a temporary digestion period in the second half of FY2025 due to the timing of the next-generation equipment transition, with growth expected to accelerate again in FY2026. We are optimistic about the sustainability of AI investments in the long term, but looking ahead to the second half, factors such as the 232 tariffs may lead customers to be more cautious in placing orders, and the timing of the launch of next-generation AI chips remains uncertain, which may result in a period of “window” for overseas equipment demand.

2026 Outlook: Optimistic about structural opportunities related to AI demand and the expansion of advanced logic in China

We expect global semiconductor equipment revenue to grow by8% year-on-year in 2026, reaching153 billion USD, with the Chinese market size at49 billion USD, nearly flat year-on-year. Looking ahead to 2026, we believe that: 1) Overseas, AI-related advanced logic and storage will continue to be the main drivers of capital expenditure. According to consensus estimates from Factset, TSMC, Samsung, and SK Hynix are expected to see capital expenditure growth rates of8%/6%/9% in 2026. Intel and Samsung may become key variables; we recommend paying attention to whether Intel can accelerate investment in its 14A node after receiving funding support from the CHIPS Act, and whether Samsung can gain more customer trust after securing Tesla’s AI chip orders. 2) SMIC and Hua Hong have recently raised funds, and Changxin has initiated listing guidance. We are optimistic about the continued investment in advanced logic and storage in China in 2026, and we expect the localization rate of domestic equipment companies in the Chinese market to increase by6 percentage points to29% year-on-year.

Risk Warning: Risks of trade friction, risks of semiconductor cycle downturn, limitations of calculations and available data. The content related to unlisted companies or uncovered stocks in this research report is a compilation of objective public information and does not represent our research team’s recommendation or coverage of these companies or stocks.

Main Text

Global Semiconductor Equipment Market Review and Forecast

Based on the analysis of the performance of 32 global semiconductor manufacturing companies and 20 equipment companies in 2Q25 and the consensus expectations for the 2025 market, we expect global semiconductor equipment company revenue to reach 142 billion USD in 2025, a year-on-year increase of 12%. We expect global semiconductor equipment revenue to grow by 8% year-on-year in 2026, reaching 153 billion USD, with the Chinese market size at 49 billion USD, nearly flat year-on-year. The localization rate of domestic equipment companies in the Chinese market is expected to increase by 7/6 percentage points year-on-year to 23%/29% in 2025E/2026E. Looking ahead to 2H25 and 2026, we are optimistic about the following three major investment opportunities: 1) Continued optimism for AI-driven advanced logic capital expenditure in 2026, with TSMC likely to continue leading, and Intel and Samsung as major variables; 2) Continued investment in advanced logic in China in 2026 and local-for-local demand; 3) The trend of “East Rising, West Falling” in the semiconductor equipment market continues, with optimism for the localization rate of equipment in the storage sector to increase first. For a detailed analysis of related industry chain companies, please refer to the original research report.

Looking ahead to capital expenditure in 2025, we expect global major semiconductor companies’ capital expenditure to increase by14%/+5% year-on-year in 2025E/2026E, with the forecast values for 2025/2026 being+1%/+2% compared to the 2025/6 forecast, among which capital expenditure for companies outside mainland China is expected to increase by17%/+6% year-on-year. We believe that AI demand and the return of manufacturing to the U.S. will continue to be the main drivers of overseas expansion. We expect capital expenditure for major semiconductor manufacturing listed companies in China to decrease by-8%/-6% year-on-year in 2025E/2026E. We believe that: 1) Demand from traditional consumer electronics, automotive, and industrial control sectors has not yet shown significant recovery, and overall demand remains weak; 2) The rapid development of AI in China, represented by DeepSeek, and the accelerated expansion of advanced processes in domestic wafer fabs present structural opportunities. Looking ahead, tariff policies are accelerating the trend of “parallel development” in the Sino-U.S. semiconductor industry chain, with repeated capacity construction in both countries to meet local-for-local demand, and we are optimistic about leading wafer fabs that can benefit from the capacity construction in both countries.

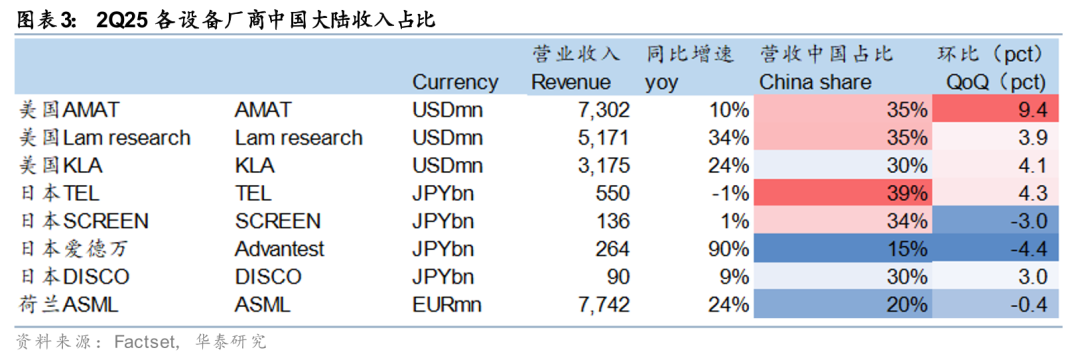

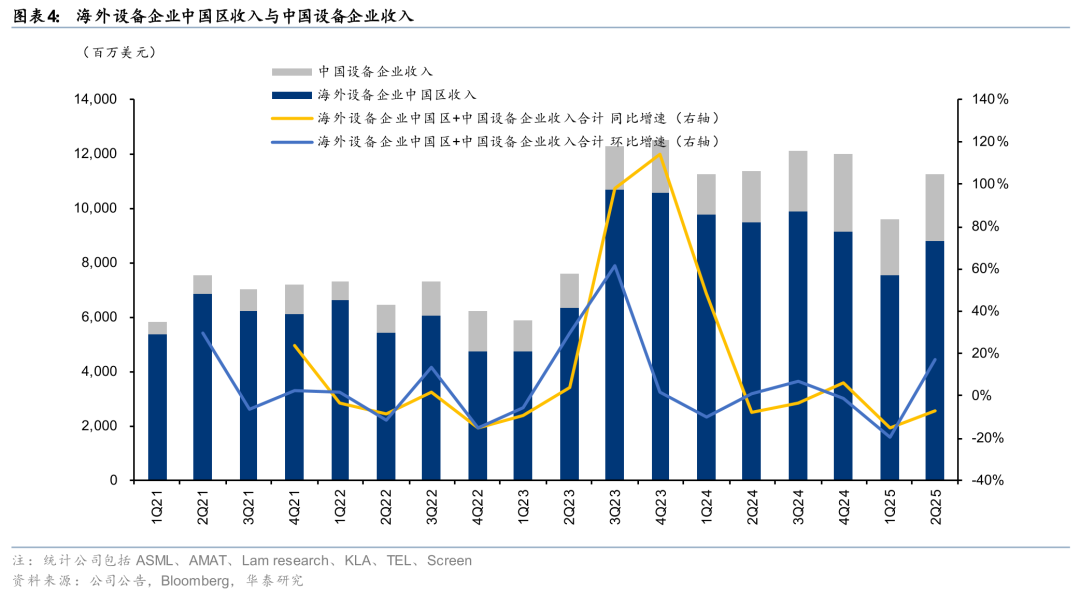

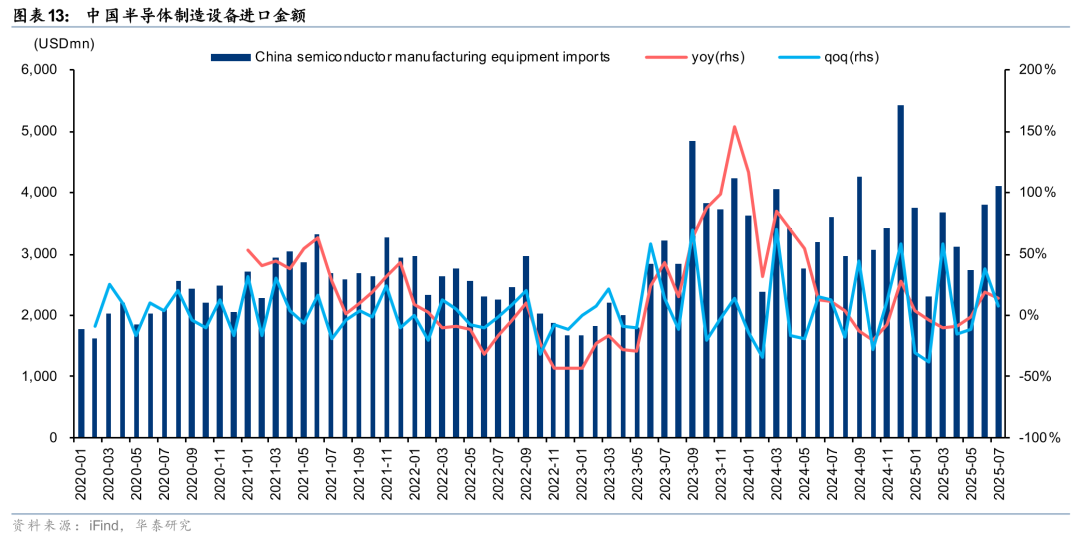

Based on statistics from 10 domestic semiconductor manufacturers and 22 domestic and overseas equipment companies’ revenue in China, we observe that: 1) The revenue share of local equipment companies continues to rise. In 2Q25, the total revenue of semiconductor equipment companies in China and overseas was 12.3 billion USD, a year-on-year decrease of 1%, among which the revenue of major listed equipment companies in mainland China maintained a high growth of 32% year-on-year, with a localization rate reaching 21%, an increase of 6 percentage points year-on-year. Looking ahead to the whole year, we are optimistic about the accelerated introduction of domestic equipment in mature production lines, expecting the localization rate to reach 23% for the year; 2) For overseas companies, in 2Q25, the revenue share of major front-end equipment companies in the Chinese market was 48%/16%/20% for the U.S./Japan/China, with year-on-year changes of +5/-3/+5 percentage points. Under the repeated tariff policies and U.S. restrictions, we are optimistic about the potential for increasing market share of domestic equipment.

We are optimistic about the increase in market share of semiconductor equipment companies in mainland China

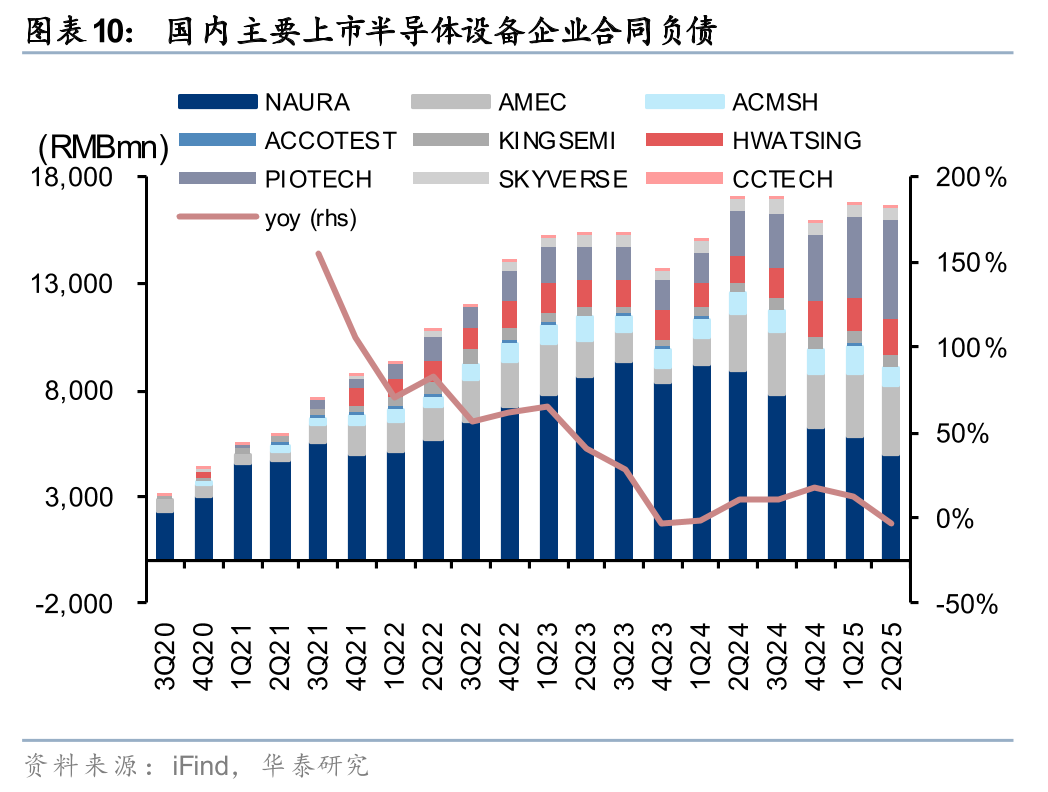

Over the past three years, under the influence of overseas semiconductor export restrictions, domestic equipment has transitioned from trial use to large-scale application. Looking back at 2Q25, we observed steady growth in domestic equipment revenue, with the total revenue of major listed equipment companies in China increasing by 32% year-on-year, and the localization rate (calculated as the proportion of domestic major equipment revenue to global equipment revenue in China) increasing by 6 percentage points to 21%. Looking ahead, according to Huatai’s forecast and iFind’s consensus expectations, the revenue of major domestic equipment companies is expected to grow by 29% year-on-year in 2025, with the localization rate expected to increase by 7 percentage points to 23%. Looking ahead to 2025, we are optimistic that 1) Chinese equipment companies and customers will achieve technological breakthroughs through joint R&D in advanced process logic, HBM, and 3D NAND high-performance storage chips; 2) Large-scale procurement of overseas equipment by wafer fabs may come to an end, and we are optimistic about the demand for domestic equipment and the maintenance needs of domestic equipment parts and materials companies in 2025.

Appendix: Global and Chinese Semiconductor Equipment Market Review

Risk Warning

Risk of trade friction:If the risk of Sino-U.S. trade friction escalates, it may cause sustained shocks to the global semiconductor supply, potentially leading to performance risks for manufacturers falling short of expectations.

Risk of semiconductor cycle downturn:The semiconductor industry is cyclical; if end demand falls short of expectations and supply chain inventories remain high, there is a risk that the semiconductor industry may enter a downturn cycle.

Limitations of calculations and available data:This article uses typical semiconductor companies for market size calculations and does not use data from all companies, thus there are risks of limitations in calculations and data.

The content related to unlisted companies or uncovered stocks in this research report is a compilation of objective public information and does not represent our research team’s recommendation or coverage of these companies or stocks.

Related Research Reports

Research Report: “2H25 Semiconductor Equipment: Overseas Temporarily Faces a Window Period, China’s Market ‘East Rising, West Falling’ May Accelerate” September 21, 2025

Huang Leping Analyst S0570521050001 | AUZ066

Chen Xudong Analyst S0570521070004 | BPH392

Yu Keyi Analyst S0570525030001 | BVF938

Follow Us

Huatai Securities Research Institute Domestic Station (Research Portal)

https://inst.htsc.com/research

Access: Domestic institutional clients

Huatai Securities Research Institute Overseas Station

https://intl.inst.htsc.com/research

Access: U.S. and Hong Kong financial institutions clientsFor access permissions, please contact your Huatai account manager

Disclaimer

▲Swipe up to read

This public account is not a platform for publishing research reports from Huatai Securities Co., Ltd. (hereinafter referred to as “Huatai Securities”). This public account is only for reference by Huatai Securities’ research service clients in mainland China. Any other readers should evaluate the appropriateness of receiving related push content before subscribing to this public account, and if using the content contained in this public account, must seek guidance and interpretation from professional investment advisors. Huatai Securities does not consider any subscriber to this public account as a client of Huatai Securities due to the act of subscribing.

This public account forwards and excerpts parts of the content and views of research reports published by Huatai Securities to its clients. The complete investment opinion analysis should be based on the complete research report content published on the day of the report. Subscribers using only the content of this public account may misunderstand the content due to a lack of understanding of the complete report or lack of related interpretation. For complete content, please refer to the complete report published by Huatai Securities.

The content of this public account is based on information that Huatai Securities believes to be reliable, but Huatai Securities makes no guarantees regarding the accuracy, completeness, or timeliness of such information, nor does it make definitive judgments about the rise or fall of securities prices or market trends. The opinions, assessments, and forecasts contained in this public account only reflect the views and judgments on the day of publication. At different times, Huatai Securities may issue research reports that are inconsistent with the opinions, assessments, and forecasts contained in this public account.

Under no circumstances does the information or opinions expressed in this public account constitute investment advice to any person. Subscribers should not rely solely on the content of this subscription account to replace their independent judgment, should make their own investment decisions, and bear their own investment risks. Subscribers using this material may misunderstand the content due to a lack of interpretation services, which may lead to investment losses. Huatai Securities and the authors bear no legal responsibility for any consequences arising from reliance on or use of the content of this public account.

The copyright of this public account is solely owned by Huatai Securities. Without the written permission of Huatai Securities, no organization or individual may infringe the copyright of all content published in this public account in any form, including reproduction, copying, publication, citation, or redistribution to others. If any infringement causes any direct or indirect loss to Huatai Securities, Huatai Securities reserves the right to pursue all legal responsibilities. Huatai Securities has been approved by the China Securities Regulatory Commission for “Securities Investment Consulting” business qualifications, with operating license number: 91320000704041011J.