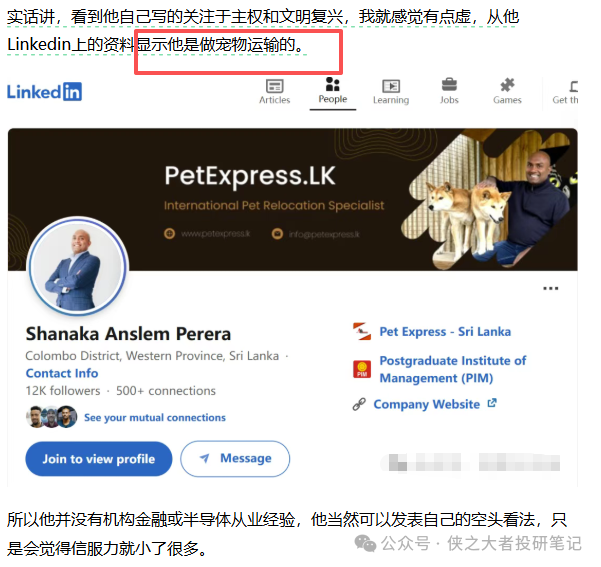

1. Let’s start with a piece of news that was quite popular yesterday – NVIDIA’s financial fraud:A lengthy article on X (formerly Twitter) about an AI Ponzi scheme went viral, with a sensational tone and apocalyptic predictions, typical of the narrative surrounding the bursting of the AI bubble. This tweet quickly gained traction, currently receiving 21,000 likes and 3.02 million views.However, there are still many exaggerations and selective interpretations, describing the normal characteristics of a high-growth tech industry as a “Ponzi scheme.”Author’s Identity: In the U.S. stock market, the consequences of financial fraud are well-known; you can search it on Baidu. The points he questions do not stem from actual business practices. Many senior financial analysts on Wall Street have not identified these issues, yet they are being questioned by an outsider, and the article is widely shared… (This actually tells us one thing: to go viral, one must seize trending topics and produce seemingly professional outputs, regardless of their accuracy, as long as there is traffic.)For example:1) The author claims that accounts receivable increased from 46 days to 53 days, but NVIDIA’s CFO stated in the earnings call that it was actually one day less than the previous quarter… (Given the significant increase in revenue compared to last year, a few days delay in accounts receivable is within a reasonable range, so the author is clearly exaggerating and deliberately concealing the CFO’s latest statement.)

In the U.S. stock market, the consequences of financial fraud are well-known; you can search it on Baidu. The points he questions do not stem from actual business practices. Many senior financial analysts on Wall Street have not identified these issues, yet they are being questioned by an outsider, and the article is widely shared… (This actually tells us one thing: to go viral, one must seize trending topics and produce seemingly professional outputs, regardless of their accuracy, as long as there is traffic.)For example:1) The author claims that accounts receivable increased from 46 days to 53 days, but NVIDIA’s CFO stated in the earnings call that it was actually one day less than the previous quarter… (Given the significant increase in revenue compared to last year, a few days delay in accounts receivable is within a reasonable range, so the author is clearly exaggerating and deliberately concealing the CFO’s latest statement.)

2) The author’s main point is the increase in inventory and the decrease in rental prices for the H100.

First, regarding the increase in inventory, it is primarily to support the ramp-up of production for the Blackwell architecture. Jensen Huang has stated that demand for Blackwell is extremely strong, with orders far exceeding supply capacity.

Quoting Jensen Huang’s exact words:If our quarterly performance is poor, that would be evidence of an AI bubble. If our quarterly performance is excellent, we are fueling the AI bubble. The company is in a lose-lose situation.NVIDIA’s financial report is indeed outstanding, with no issues; it seems everyone has become accustomed to it, numb to it, so meeting or exceeding expectations is now considered normal…

2. Objective Analysis: NVIDIA’s decline is certainly influenced by Google’s TPU chips.From a narrative perspective, people might speculate whether more manufacturers will use their own AISC chips, which is absurd. TSMC’s capacity is already fully booked, where would they find the opportunity to set up their own production lines? There are too many issues with the supply chain, etc. Not every company is like Google, with its own R&D capabilities.The key point is: Google continues to purchase NVIDIA cards in large quantities.Tech stocks in the U.S. are all declining; the fundamental issue is still the liquidity problem in the U.S. stock market and the impact of interest rate cuts.

2. Objective Analysis: NVIDIA’s decline is certainly influenced by Google’s TPU chips.From a narrative perspective, people might speculate whether more manufacturers will use their own AISC chips, which is absurd. TSMC’s capacity is already fully booked, where would they find the opportunity to set up their own production lines? There are too many issues with the supply chain, etc. Not every company is like Google, with its own R&D capabilities.The key point is: Google continues to purchase NVIDIA cards in large quantities.Tech stocks in the U.S. are all declining; the fundamental issue is still the liquidity problem in the U.S. stock market and the impact of interest rate cuts. 3. The most important point: Many friends ask whether NVIDIA’s continued decline will affect AI hardware in the A-share market.

3. The most important point: Many friends ask whether NVIDIA’s continued decline will affect AI hardware in the A-share market.

First, this assumption is not valid; secondly, the correlation between NVIDIA’s rise and fall and the rise and fall of AI hardware in the A-share market is not significant,in the short term there is certainly an emotional impact.

However, it is important to remember that in the long term, the essence of what affects stock price fluctuations is whether the profits and market value created by the company are reasonable; this is what determines stock price increases.The future profits multiplied by the price-earnings ratio > current market value indicates undervaluation; otherwise, it indicates overvaluation.

These AI hardware companies are not rising because they bought NVIDIA stocks; when NVIDIA rises, they rise; when NVIDIA falls, they fall.

In other words, just because macro factors like U.S. stock market liquidity lead to NVIDIA’s stock price decline, does that mean these AI hardware companies will stop shipping or stop generating profits???

NVIDIA will not lack revenue or orders for the next five years; as mentioned before, NVIDIA’s revenue ceiling is constrained by TSMC’s insufficient capacity. There has always been a supply-demand imbalance.

Moreover, Shenghong Technology has increased tenfold in over a year,and Zhongji Xuchuang has increased eightfold,while NVIDIA has only increased 30% this year, so do you think there is a necessary correlation???

Should NVIDIA, a multi-trillion-dollar company, increase tenfold for them to increase tenfold? Not necessary!

If a company earned 100 million last year, and hypothetically earns 1 billion next year, its stock price can increase significantly.

In other words, as long as they can share a piece of the pie from NVIDIA’s business and generate their own profits, they can see significant increases, rather than needing NVIDIA’s stock price to rise significantly for them to rise. If you still have this kind of thinking, you should consider closing your account.