★

Welcome to bookmark Guoke Hard Technology

★

Japan has long dominated the semiconductor industry with its equipment and materials. In 2019, a ban nearly choked South Korea’s semiconductor industry, involving materials such as high-purity hydrogen fluoride, fluorinated polyimide, and photoresist. It wasn’t until a few months ago that both parties reached a reconciliation.

What makes high-purity hydrogen fluoride stand alongside photoresist? It is a type of wet electronic chemical, similar to electronic gases, serving as the “blood” of semiconductor products; without it, chips cannot be produced.

This article is the twenty-sixth in the “domestic substitution” series planned by Guoke Hard Technology, focusing on wet electronic chemicals. In this article, you will learn about: which wet electronic chemicals are used in semiconductor production, their special requirements, the current development status domestically and internationally, and the future of domestic development.

Author: Fu Bin

Editor: Li Tuo

Planning: Guoke Hard Technology

The Aristocrats of Liquids, Surrounded by Barriers

In the industry, wet electronic chemicals are known by various names; internationally, they are referred to as process chemicals, while domestically they are called “electronic-grade reagents” or “ultra-pure chemical reagents”.

In wafer manufacturing materials, 14% is spent on wet electronic chemicals, which are used for cleaning, etching, and wafer cleaning, determining the final yield, electrical performance, and reliability.

For example, after the photolithography process, the etching process requires specific etching liquids to chemically react with the thin film; after etching, stripping liquids are needed to dissolve the unexposed parts of the photoresist; throughout the production process, contamination from dust, particles, metals, or ionic conductive pollutants is inevitable, and cleaning liquids can remove these impurities. In metallization processes, copper plating solutions are essential chemicals for copper interconnection processes.

In addition to integrated circuits, flat panel displays and solar cells also rely on wet electronic chemicals. Due to their strong functionality and high added value, they are widely regarded as a crucial lever for driving the industry.

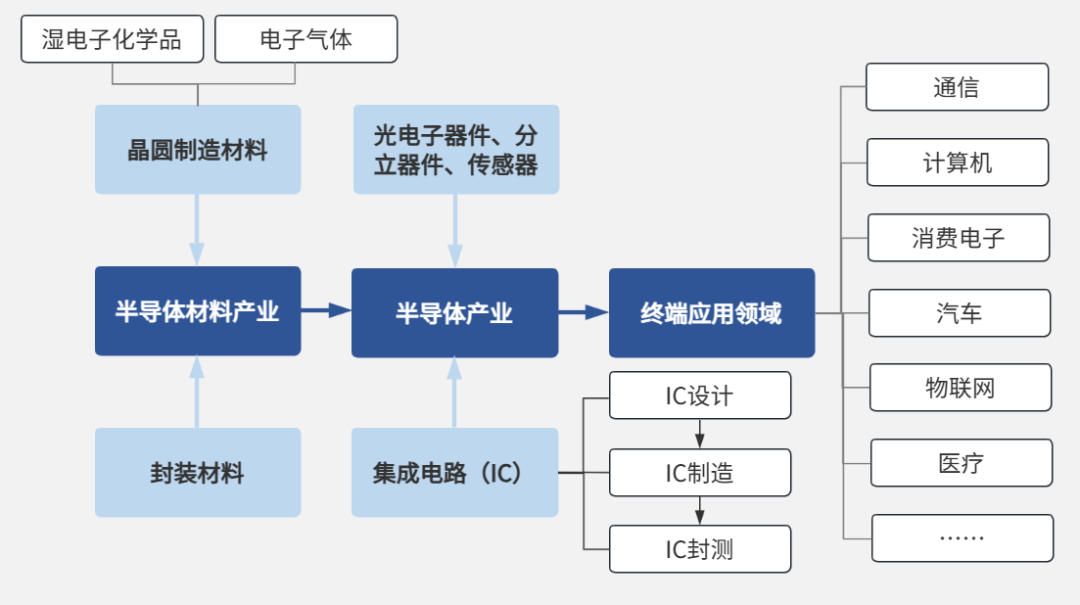

Materials are a crucial support for the semiconductor industry

Strictly speaking, any liquid, paste, or viscous substance used in the semiconductor production process is considered a wet electronic chemical, but the term generally refers specifically to ultra-high-purity reagents.

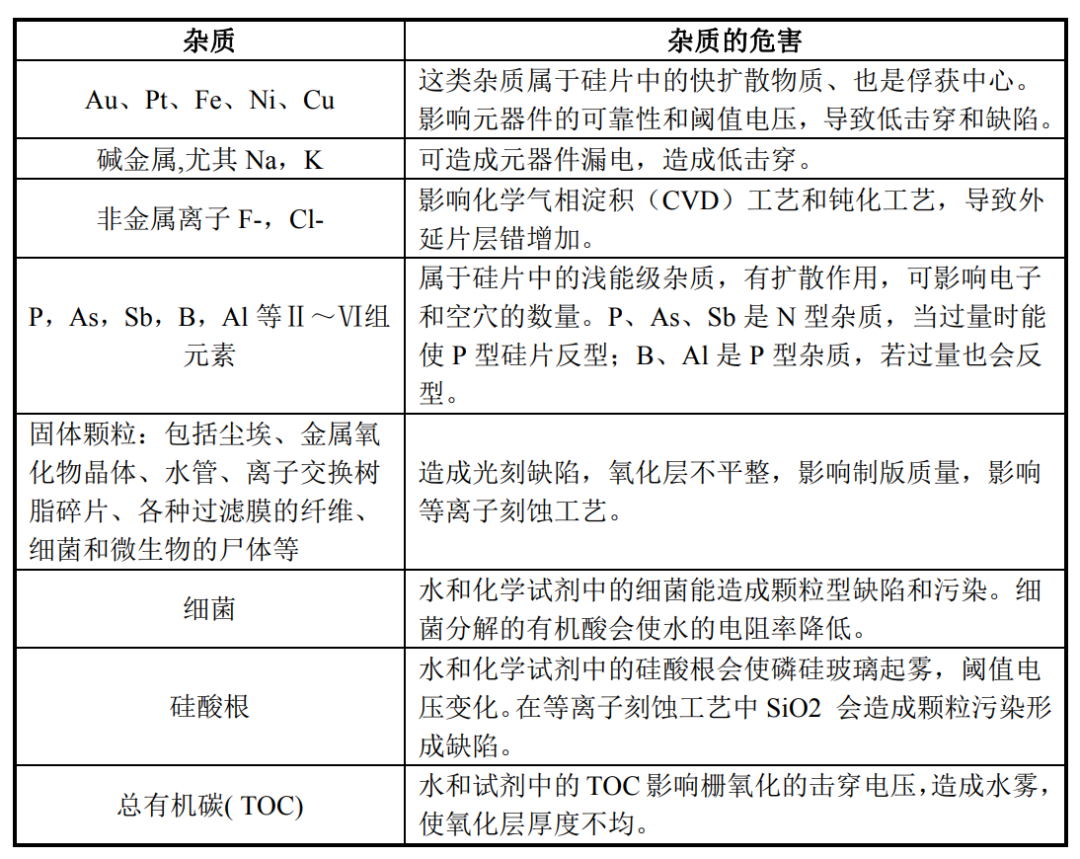

Chip manufacturing cannot tolerate even a grain of sand; metal ions and non-metallic ion impurities such as boron, silicon, arsenic, phosphorus, sulfur, chlorine, and organic carbon in wet electronic chemicals can directly affect the 3D structure of chips.

Impurities harm integrated circuits

Wet chemicals used in the semiconductor industry are known as the aristocrats of chemicals, with the highest purity requirements.

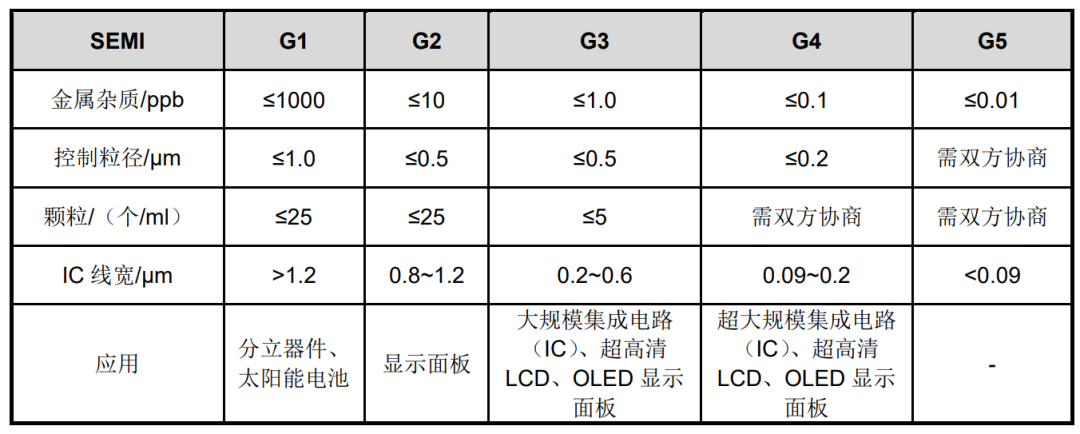

Globally, the SEMI international standard is followed regarding purity, which is classified into five grades based on metal impurities, particle size control, and particle count, with G5 being the highest grade. Different grades are suitable for different applications. For instance, solar photovoltaics generally require only G1 level, display panels and LEDs typically require G2~G3 levels, while semiconductors correspond to G4~G5, with the highest technical barriers.

SEMI international standard grades for wet electronic chemicals

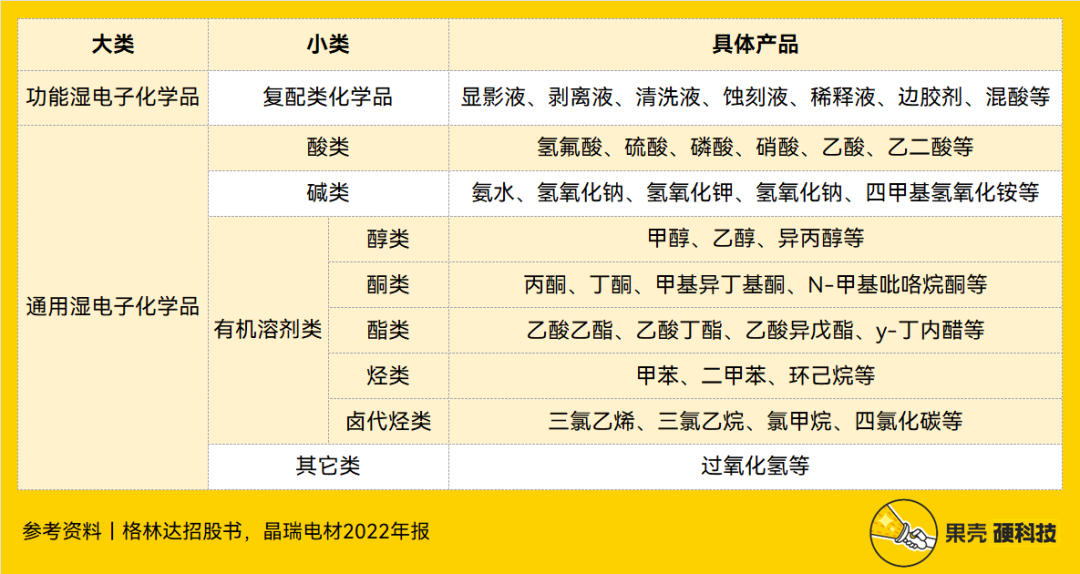

There are many varieties of wet electronic chemicals for integrated circuits, which can be divided into two main categories based on composition and process: general wet chemicals and functional wet chemicals:

-

General wet electronic chemicals are liquid chemicals used extensively in manufacturing processes, typically single-component, single-function chemicals, such as hydrofluoric acid, sulfuric acid, nitric acid, phosphoric acid, hydrochloric acid, hydrogen peroxide, sodium hydroxide, and potassium hydroxide;

-

Functional wet electronic chemicals are blended chemicals that meet the needs of specific manufacturing processes, such as developing solutions, stripping solutions, etching solutions, diluents, and cleaning solutions, involving processes like photolithography, etching, ion implantation, and CMP.

Classification and specific products of wet electronic chemicals, table by Guoke Hard TechnologyReferences: Glinda’s prospectus, Jingrui Electronics 2022 annual report

Classification and specific products of wet electronic chemicals, table by Guoke Hard TechnologyReferences: Glinda’s prospectus, Jingrui Electronics 2022 annual report

Specifically, among general chemicals, the consumption of sulfuric acid, hydrofluoric acid, nitric acid, phosphoric acid, hydrochloric acid, hydrogen peroxide, ammonia, and isopropanol is particularly large, while in functional chemicals, the consumption of diluents, developing solutions, etching solutions, stripping solutions, buffered oxide etchants (BOE), cleaning solutions, and plating solutions increases with process complexity.

For chips, the more advanced the process technology, the greater the use of wet electronic chemicals. SEMI statistics show that the total process steps will increase from 400 for 28nm to over 1200 for 5nm, further driving the demand for wet electronic chemicals.

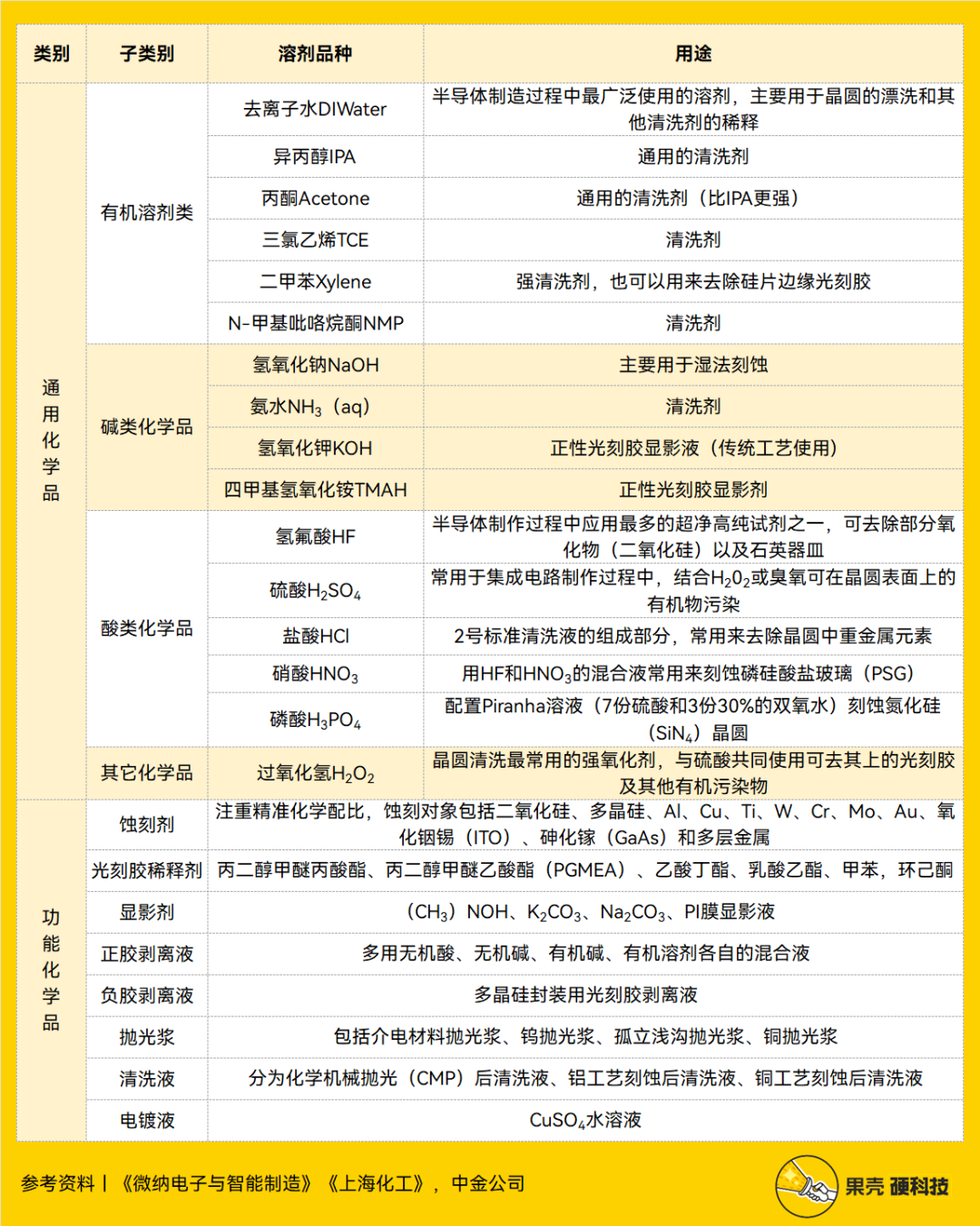

Common electronic-grade chemicals and their uses, table by Guoke Hard TechnologyReferences: Micro-nano electronics and intelligent manufacturing, Shanghai Chemical, Zhongjin Company

Common electronic-grade chemicals and their uses, table by Guoke Hard TechnologyReferences: Micro-nano electronics and intelligent manufacturing, Shanghai Chemical, Zhongjin Company

Of course, not only must the liquid itself be pure, but the packaging, transportation, and usage processes must also be sufficiently clean. It can be said that every link in wet electronic chemicals has technical barriers:

-

Raw material purification: Raw materials are key to preparing high-purity wet electronic chemicals. Efficient purification requires investment in the selection of purifying agents, improvement of process parameters, and optimization of purification systems;

-

Purification: The focus of purifying wet electronic chemicals is not on content but on removing harmful metal ions and particle content. Purification methods mainly include distillation and precision fractionation, ion exchange, molecular sieve separation, gas absorption, and ultra-clean filtration, with each purification technology having its strengths;

-

Blending: The ratio and formulation are key, much like mixing seasonings; not only is experience important, but it must also meet taste preferences. Additionally, the temperature, pressure, flow rate, ratio, and exhaust volume during the blending process are closely related to the blending results;

-

By-product utilization: Most wet electronic chemical production processes generate a large number of by-products. For example, barium fluorosilicate produced during the purification of electronic-grade hydrofluoric acid can be directly sold after multiple washings and drying, so the development of by-product utilization is a focus for production enterprises;

-

Testing: The contamination of wet electronic chemicals during chip manufacturing determines the lifeline of enterprises. As chips enter the nanometer level, the requirements for metal and non-metal impurity content have reached the 10-12 level. Traditional trace element detection methods such as GF-AAS and ICP-OES have been eliminated, and the commonly used analytical testing methods are ICP-MS and ICP-MS/MS ion chromatography. Currently, foreign analytical systems include ESI in the USA, IAS in Japan, and JinZhaoYi in Taiwan, while domestic systems include Hangzhou PuYu Technology;

-

Packaging and transportation: Wet electronic chemicals are mostly flammable, explosive, and highly corrosive hazardous materials. During transportation, they must not leak or become contaminated. The most widely used packaging materials are high-density polyethylene (HDPE), polytetrafluoroethylene, and perfluoroalkoxy copolymers (PFA), with different chemical packaging requirements varying accordingly;

-

Recycling: The discharge of waste liquids in chip production is significant, and most of these waste liquids are biologically toxic and pollute the environment. Recycling not only has environmental significance but can also reduce the consumption of chemicals by enterprises. So far, wet electronic chemicals are mostly used for cleaning and drying, and the impurity content after use is not high, with most impurity types being known, allowing for targeted removal of impurities for reuse, thus reducing enterprise costs.

From Domestic Substitution to Prosperity

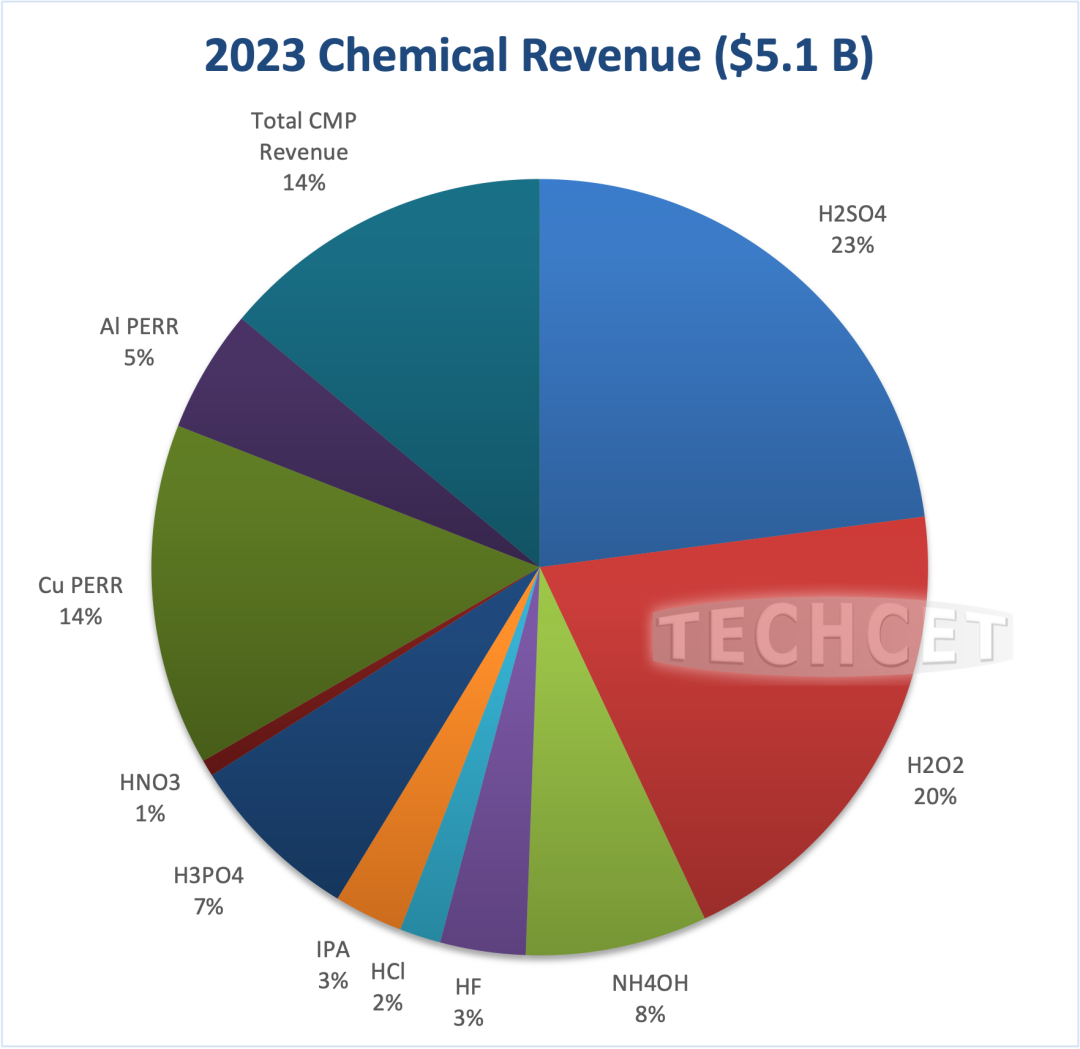

The customer base for wet electronic chemicals used in integrated circuits is relatively specialized, but there is also a certain market scale. According to data from the China Electronic Materials Industry Association and TECHCET, the global market size for wet chemicals used in integrated circuits is expected to grow from $5.69 billion in 2022 to $6.38 billion by 2025. Due to a decrease in downstream chip demand, the global market size is expected to reach $5.1 billion in 2023, slightly down year-on-year, with China’s overall market size projected to grow to $1.027 billion by 2025.

In terms of key chemical categories, sulfuric acid, hydrogen peroxide, Cu PERR (post-etch cleaning agent), and CMP polishing liquids are the top four wet electronic chemicals used globally in 2023, accounting for 23%, 20%, 14%, and 14%, respectively, followed by ammonia, phosphoric acid, AI PERR (post-etch cleaning agent), hydrofluoric acid, isopropanol, hydrochloric acid, and nitric acid.

Market segmentation of wet electronic chemicals

Market segmentation of wet electronic chemicals

One generation of products, one generation of materials; wet electronic chemicals have high technical barriers, require significant investment, and undergo rapid updates. Moreover, China started decades later than foreign countries, making it challenging to compete in the market.

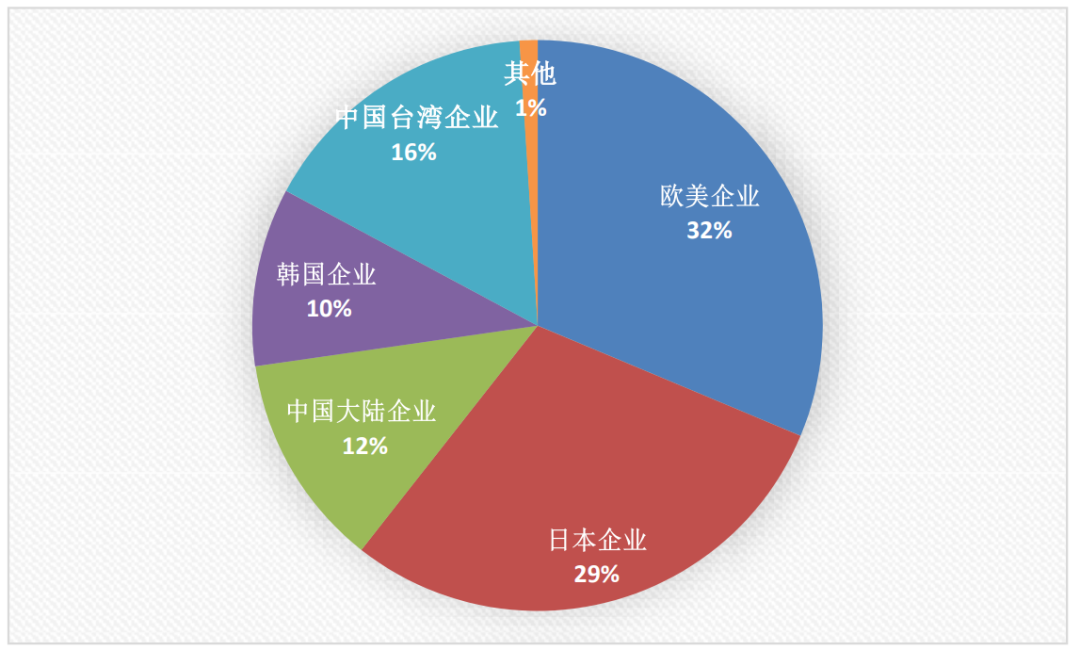

Currently, major manufacturers from Europe, America, Japan, and South Korea occupy over 70% of the global wet electronic chemical market, with a relatively stable structure. Data shows that Europe and America account for about 32% of the global market share, Japan accounts for 29%, while mainland China only accounts for 12%.

Specifically, domestic products are mainly concentrated in low-end products in fields such as solar cells, where the technical barriers are low and competition is fierce; in mid-range products, there is mutual competition between China and South Korea in flat panel displays and semiconductors; while high-end products are dominated by Germany, the USA, and Japan.

Global market structure of wet chemicals in 2021 (by sales)

Global market structure of wet chemicals in 2021 (by sales)

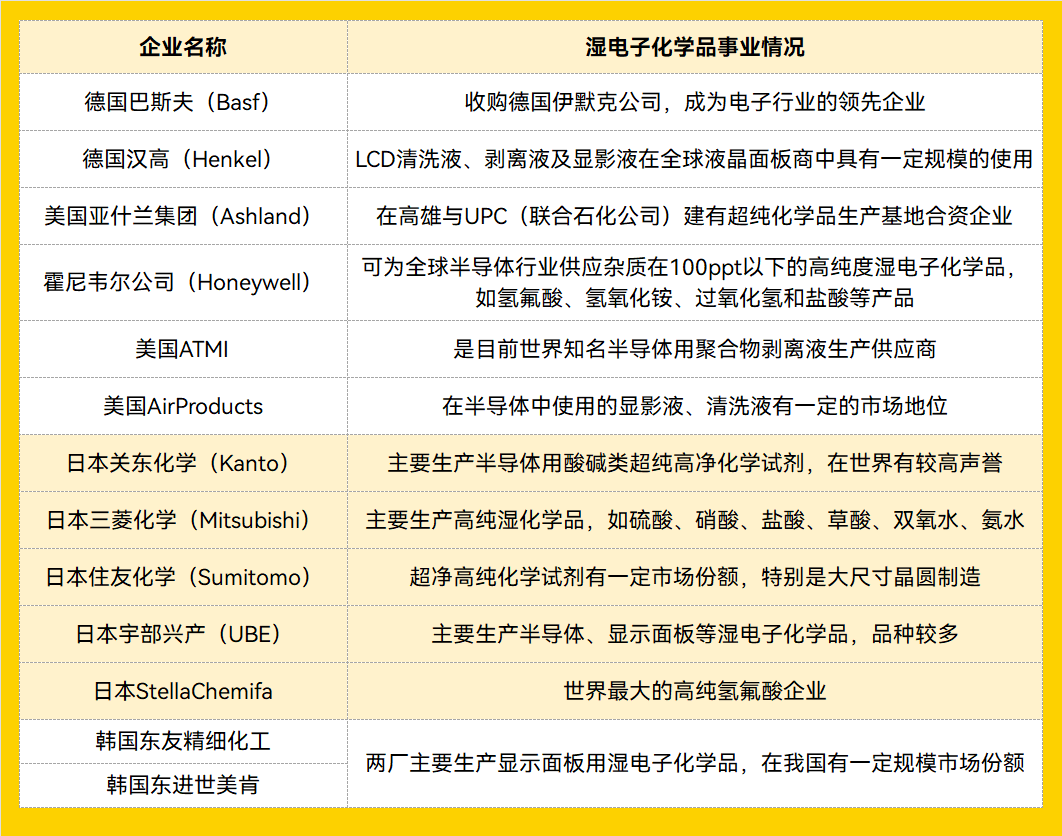

Established chemical companies in Europe and America generally have product grades above G4, maintaining pace with the development of the semiconductor chip manufacturing industry. Representative companies include BASF from Germany, E. Merck from Germany, Ashland from the USA, Arch Chemicals from the USA, Honeywell from the USA, Mallinckrodt Baker from the USA, Avantor Performance Materials from the USA, and ATMI from the USA.

Japan’s industrial development, although later than that of Europe and America, has progressed rapidly, and its process technology level is now basically on par with that of European and American companies. Representative companies include Kanto Chemical, Mitsubishi Chemical, Kyoto Chemical, Japan Synthetic Rubber, Sumitomo Chemical, Wako Pure Chemical Industries, Ube Industries, and Stella-Chemifa.

South Korea and Taiwan are also rapidly developing in wet electronic chemicals, with their production technologies and process levels now competitive in high-end fields. Representative companies include Dongwoo Fine-Chem from South Korea, Dongjin Semichem from South Korea, Dongying Chemical from Taiwan, and Lian Shi Electronics Chemical from Taiwan.

International representative companies in wet electronic chemicals

International representative companies in wet electronic chemicals

China’s wet electronic chemicals have made certain breakthroughs, initially forming an industrial scale in general chemicals, but in ultra-high-purity reagents, both quality and quantity are still insufficient to meet the needs of the electronics industry. In 2019, mainland Chinese companies accounted for only 9% of the ultra-pure chemical market supply.

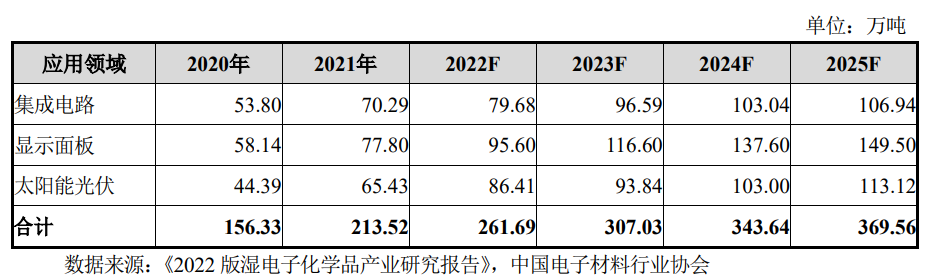

Data shows that in 2022, China’s overall demand for wet electronic chemicals grew to 2.6169 million tons, up from 2.1352 million tons the previous year, and it is expected that demand will reach 3.0703 million tons in 2023. The demand for integrated circuits, display panels, and photovoltaic industries is expected to be 965,900 tons, 1,166,000 tons, and 938,400 tons, respectively. By 2025, domestic demand is projected to increase to 3.7 million tons, with demand for integrated circuits, display panels, and photovoltaic industries expected to be 1,069,400 tons, 1,495,000 tons, and 1,131,200 tons, respectively.

Demand and market are not equivalent; the higher-end the product, the greater its value. In 2021, China’s wet electronic chemical market size was 13.78 billion yuan, with the market sizes for integrated circuits, display panels, and photovoltaic industries being 5.2 billion yuan, 6.2 billion yuan, and 1.7 billion yuan, accounting for 40%, 47%, and 13%, respectively. It is expected that from 2022 to 2028, the domestic market size will grow from 16.39 billion yuan to 30.17 billion yuan.

Demand scale of China’s three major application markets for wet electronic chemicals

Currently, the overall domestic localization rate of wet electronic chemicals is about 35%, while the localization rate for wet electronic chemicals used in integrated circuits is about 23%. Among them, the localization rate for high-end semiconductor-required hydrofluoric acid is about 30%, nitric acid is about 50%, hydrochloric acid is about 20%, sulfuric acid is about 10%, ammonia is about 40%, and hydrogen peroxide is about 70%. Products like NMP and tetramethylammonium hydroxide still have no applications in high-end fields.

That said, China has made rapid progress, achieving full domestic substitution in integrated circuits, flat panel displays, and solar cells. In other words, there are at least usable products in every field.

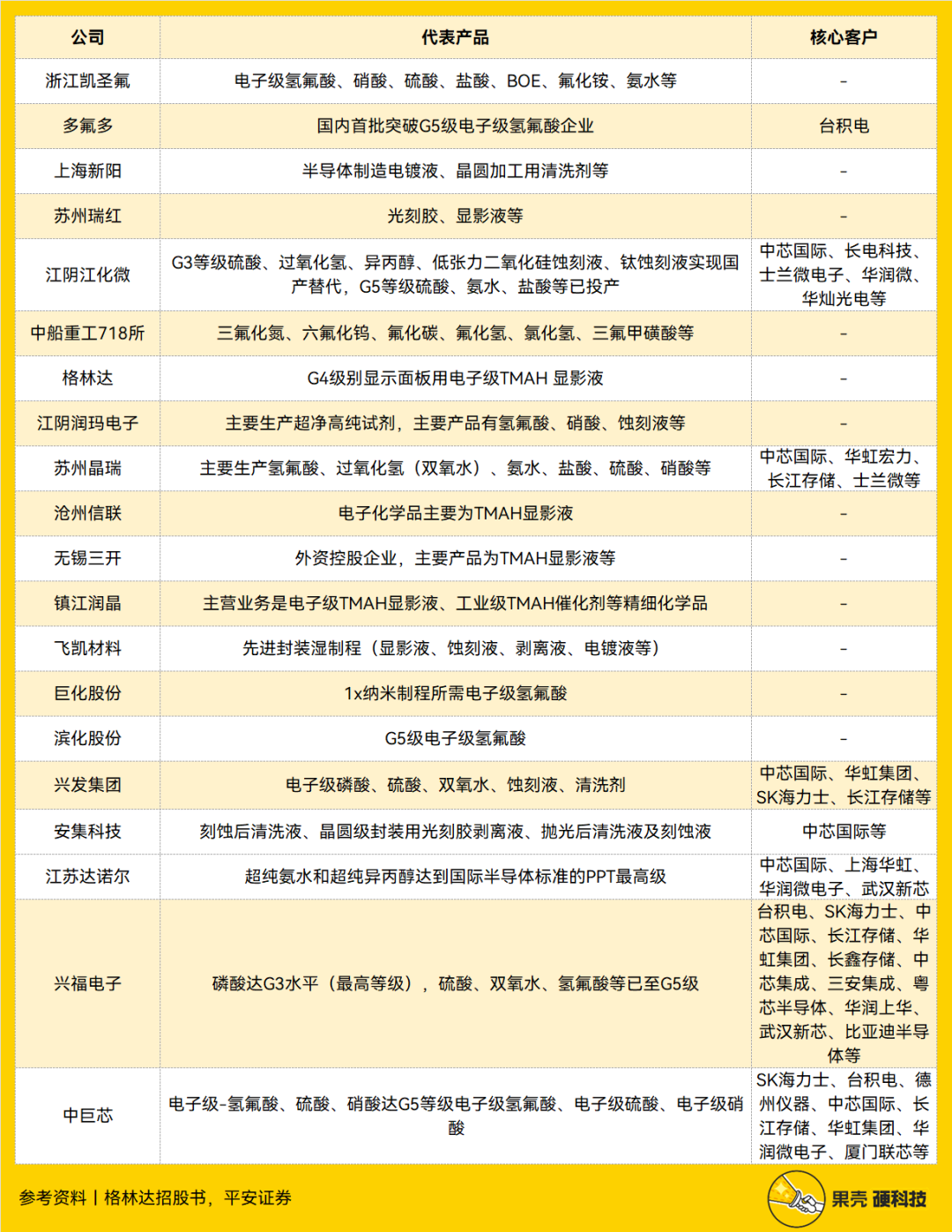

So far, there are over 40 domestic companies engaged in the research and production of wet chemicals, categorized into specialized suppliers of wet electronic chemicals, electronic materials platform companies, and large chemical enterprises. These include Jiangyin Jianghua Microelectronics, Jiangyin Runma Electronics, Jiangsu Aisen, Zhejiang Kaisheng Fluorine, Jingrui Electronics, Hangzhou Glinda, Hubei Xingfu Electronics, Zhongju Semiconductor Technology, Duofu Duo, Anji Micro, Shanghai Xinyang, Cangzhou Xinlian, Wuxi Sankai, and Zhenjiang Runjing, with clients including TSMC, SMIC, Changjiang Electronics, China Resources Micro, and Silan Micro.

Specifically, electronic-grade nitric acid, hydrofluoric acid, and phosphoric acid have made significant breakthroughs and have entered the international supply chain, while electronic-grade sulfuric acid, hydrochloric acid, ammonia, and hydrogen peroxide have achieved partial batch applications domestically. For example, Jianghua Micro’s electronic-grade hydrofluoric acid/sulfuric acid/nitric acid, Hubei Xingfu’s electronic-grade phosphoric acid/sulfuric acid/silicon etching solution/aluminum etching solution, Jingrui Electronics and Suzhou Jingrui’s electronic-grade hydrogen peroxide, Shanghai Xinyang’s electronic-grade sulfuric acid/copper plating solution/copper post-etch cleaning solution, and Anji Micro’s copper polishing post-cleaning solution have been applied in mass production on 8-inch integrated circuit production lines, while wet electronic chemicals for wafer manufacturing at 12-inch nodes above 28nm have seen limited application, mostly in system certification stages, and those below 28nm are in laboratory research and small-scale development stages.

Incomplete statistics of domestic wet electronic chemical manufacturers, table by Guoke Hard TechnologyReferences: Glinda’s prospectus, Ping An Securities

Incomplete statistics of domestic wet electronic chemical manufacturers, table by Guoke Hard TechnologyReferences: Glinda’s prospectus, Ping An Securities

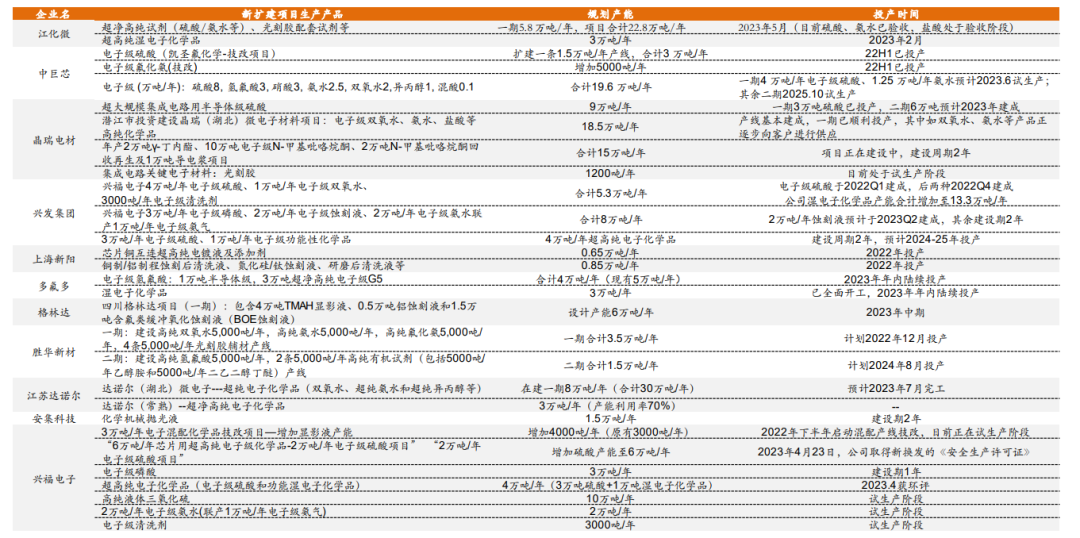

In recent years, driven by the demand for domestic substitution and the semiconductor trade war between China and Japan, the production of wet electronic chemicals in China has been continuously increasing. From 2016 to 2022, production increased from 240,000 tons to 800,000 tons, with a year-on-year growth of 23.1% in 2022 alone. Moreover, by 2025, there will be a large amount of new production capacity.

Planned new production capacity for wet electronic chemicals from 2022 to 2025

Planned new production capacity for wet electronic chemicals from 2022 to 2025

Domestic substitution is just the first step taken at this stage; moving towards prosperity still faces challenges: domestic products are relatively singular, lacking leading enterprises with high market shares across multiple varieties; although some companies have made breakthroughs in multiple product varieties, flagship products remain limited, especially in advanced processes where gaps are evident.

To Make Money, Follow the Industry Chain

Making wet electronic chemicals is not easy, and making money from them is even harder.

From the financial reports of various domestic companies, the overall gross margin fluctuates between 20% and 50%, with functional wet electronic chemicals having a gross margin between 30% and 60%, while high-end products can reach 70%, and general wet electronic chemicals fluctuate between 5% and 30%.

In contrast, the high technical barriers, significant R&D investment, and long R&D cycles associated with wet electronic chemicals mean that global chemical manufacturers are cautious about expansion. A report from SIA noted that some chip factories in the USA experience supply shortages of wet electronic chemicals almost every year.

International leading enterprises are mostly versatile in the materials field; by producing a variety of products, they can avoid cyclical risks while forming industry chains and networks to maximize the value of raw materials, intermediates, by-products, etc. This can be glimpsed in patents.

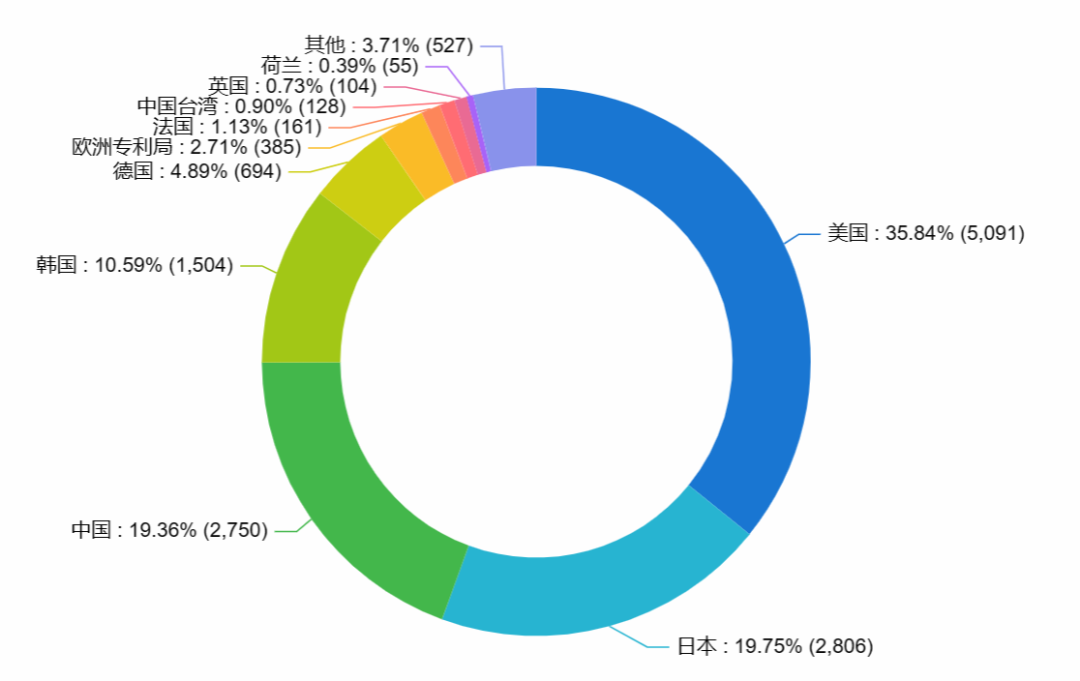

Searching for both semiconductor and wet electronic chemicals as keywords on Zhihuiya reveals that there are 19,421 patents across 170 countries/regions, with a total patent value of $1.313 billion. Among them, the USA ranks first in application volume, accounting for 35.84% of global patents related to wet electronic chemicals, followed by Japan, China, South Korea, and Europe, accounting for 19.75%, 19.36%, 10.59%, and 7.6% of the total, respectively. It is important to emphasize that domestically, there is a lack of patents going abroad, while the situation for patents from the USA and Japan going abroad is relatively good.

Ranking of countries/regions for the source of wet electronic chemicals technology

Ranking of countries/regions for the source of wet electronic chemicals technology

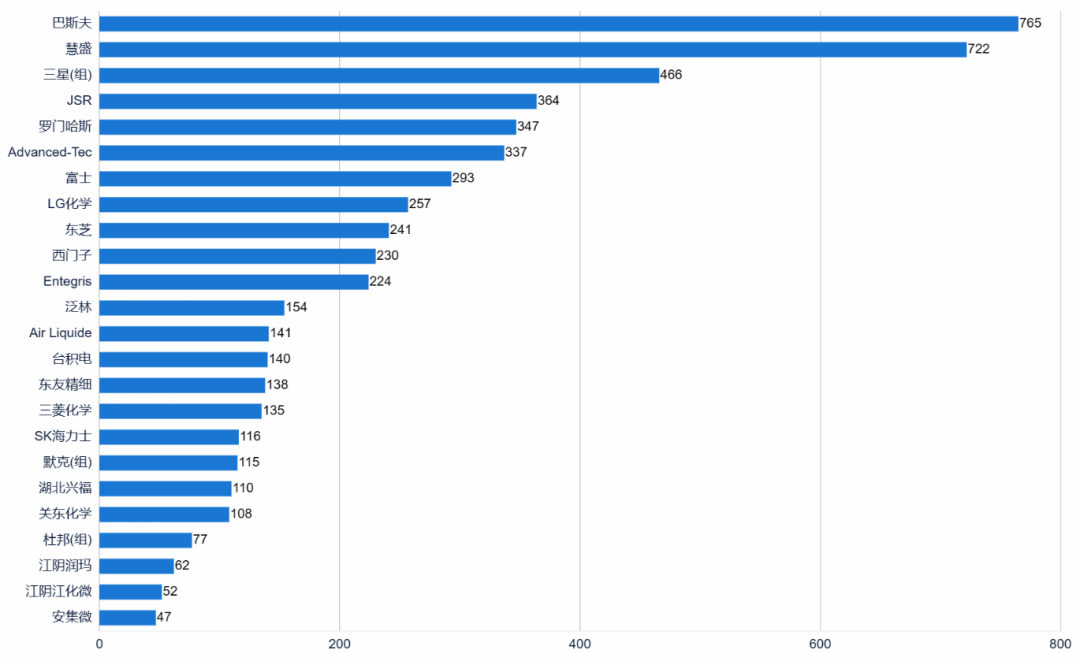

Leading companies in the patent front are mostly large comprehensive chemical enterprises, including BASF from Germany, LG Chem from South Korea, Fuji from Japan, Sumitomo Chemical from Japan, and DuPont from the USA. In contrast, domestic companies like Hubei Xingfu, Jiangyin Runma, and Jiangyin Jianghua Microelectronics are also continuously catching up with foreign companies in terms of patent numbers.

Analysis of typical applicants for wet electronic chemicals, source: Zhihuiya

Fluorinated electronic gases, wet electronic chemicals, and photoresists are three major materials in semiconductors, sharing similar industrial logic.

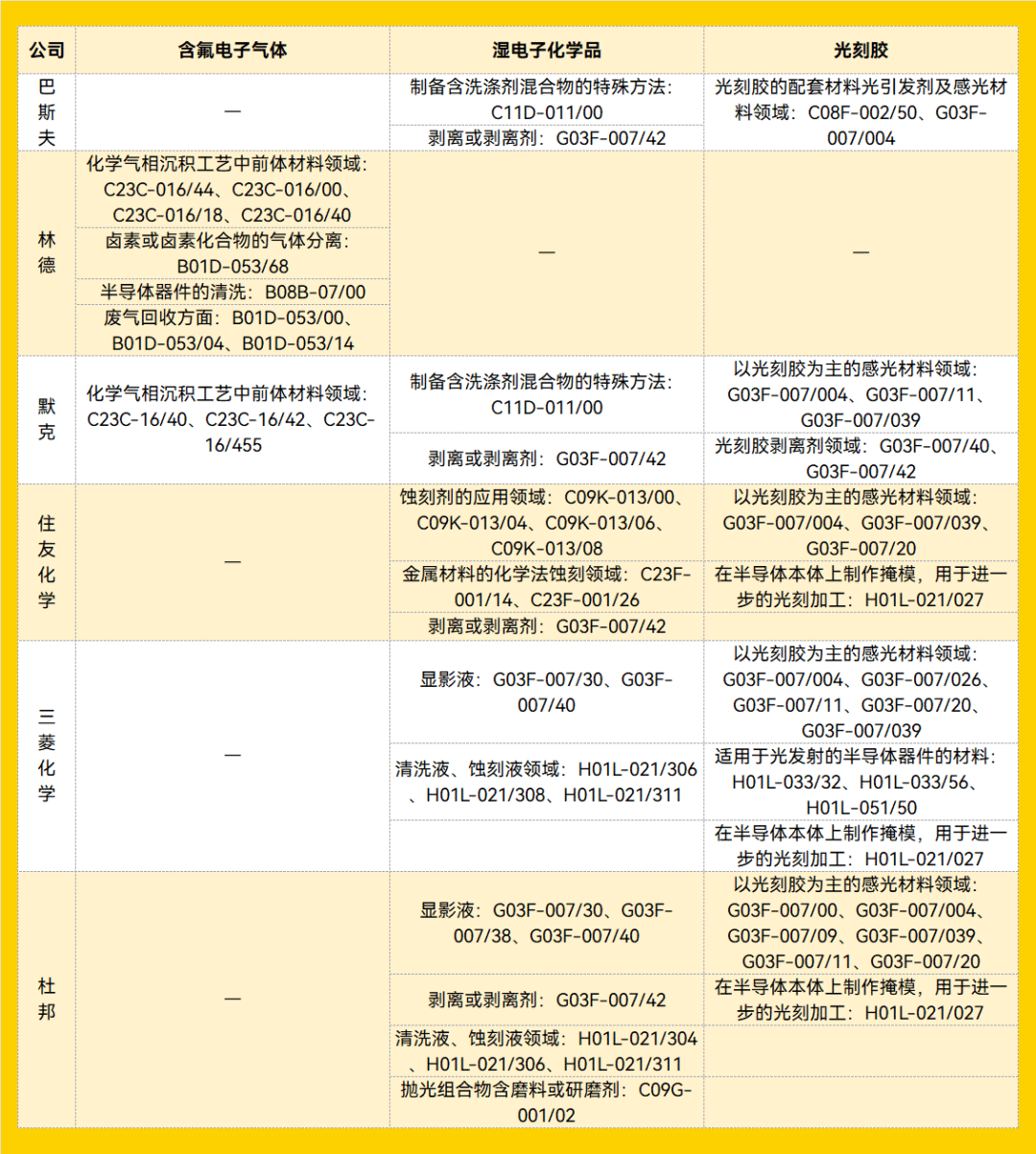

Looking at the layout of six global leading companies, including BASF from Germany, Linde from Germany, Merck from Germany, Sumitomo Chemical from Japan, and Mitsubishi Chemical from Japan, five of them are involved in both wet electronic chemicals and photoresists, covering related patents in stripping, cleaning, developing, and polishing.

Comparison of leading companies’ technology layout in segmented fields of electronic chemicals based on patents

Comparison of leading companies’ technology layout in segmented fields of electronic chemicals based on patents

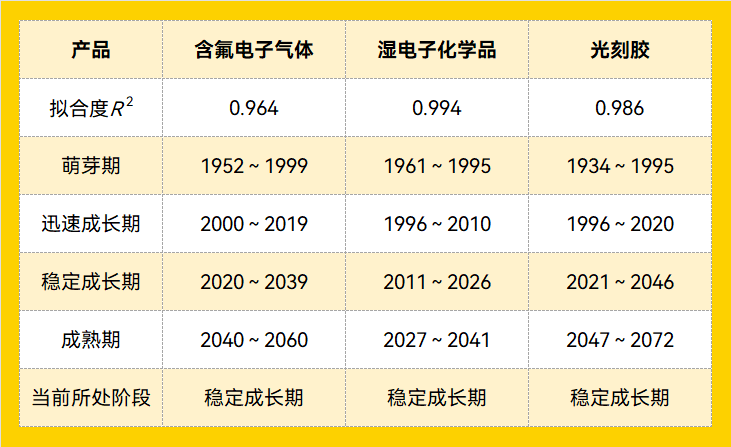

Becoming a leader is not an overnight process. Wet electronic chemicals were first applied in the 1960s, and the international market has undergone multiple rounds of reshuffling and consolidation. Currently, the global wet electronic chemical market is in a stable growth phase, expected to enter a mature phase in 5 to 20 years.

Calculated technology maturity based on patent data

The development of the business model in the chemical reagent industry in leading countries mainly goes through three stages: the first stage is to achieve self-production and self-marketing; the second stage is to develop towards supporting equipment, reagents, and services, achieving a full product line supply; the third stage is to cultivate R&D and marketing networks, with the industry beginning to form alliances or mergers and acquisitions, rapidly increasing market concentration.

Beyond the third stage, it is the giants’ swallowing, with increasing concentration. For example, in 2004, BASF acquired Merck’s electronic chemicals business, and in 2019, Merck completed the acquisition of Versum Materials in the USA.

Currently, China is still in the development stage, and compared to international century-old companies, it is challenging to achieve large-scale integration and mergers at this stage. Therefore, developing around the industry chain may be a good path.

On the upstream side, raw material prices and supply are the lifeline for wet electronic chemical production enterprises. Shutdowns at refineries can affect the cost and availability of isopropanol and sulfuric acid. As environmental regulations tighten, fluctuations in raw material prices also impact product output. Additionally, rising prices and restrictions on natural gas and oil used in manufacturing can also lead to increases in chemical prices.

For example, hydrofluoric acid is generally produced by adding sulfuric acid to fluorite, and 60% of the world’s annual production of 7 million tons of fluorite comes from China, leading Japan to import over 90% of its hydrofluoric acid and its main raw materials from China. Domestic companies like Duofu Duo, Xingfu Electronics, and BinHua Co., Ltd. all have G5 grade hydrofluoric acid, which not only penetrates the TSMC and SMIC supply chains but has also become a major substitute in the semiconductor trade war between China and Japan.

On the mid-to-lower stream side, the packaging and transportation costs of wet electronic chemicals, as hazardous chemicals, are extremely high. Therefore, most wet electronic chemical producers build factories around chip manufacturers.

For instance, TSMC recently announced plans to build a factory in Arizona, followed by its supplier LCY announcing plans to repackage and purify isopropanol in Arizona, and another supplier, Changchun Chemical, also plans to produce electronic-grade hydrogen peroxide and photolithography solutions based on tetramethylammonium hydroxide in Arizona.

It can be said that although there are still gaps in domestic wet electronic chemicals, the supply of upstream raw materials is abundant, providing significant advantages for domestic production enterprises. The remaining task is to navigate the industry chain and continuously increase their depth.

As the nanometer process approaches 1nm, the differences in processes among chip manufacturers are becoming more pronounced, and the demand for customized wet electronic chemicals is increasing. This may become a turning point for domestic enterprises.

References:

[1] Youyan Semiconductor Silicon Materials Co., Ltd.: Initial public offering and listing on the Science and Technology Innovation Board prospectus. 2022.11.7. http://static.sse.com.cn/disclosure/listedinfo/announcement/c/new/2022-11-07/688432_20221107_39HW.pdf

[2] Fu Xuetao. Discussion on the standard system of integrated circuit process chemicals. Information Technology and Standardization, 2013 (1): 29-32.

[3] Anji Microelectronics Technology (Shanghai) Co., Ltd. 2022 Annual Report Summary: http://static.cninfo.com.cn/finalpage/2023-04-12/1216380754.PDF

[4] Xu Zhixian, Yao Jijun, Hu Jiankun, Xia Xiaofeng, Lu Shuimiao, Mei Huadeng, Li Weidong. Current status and progress of analysis and detection technology for semiconductor industrial raw materials. Micro-nano Electronics and Intelligent Manufacturing, 2022, 4(01): 75-81.

[5] Jiangyin Jianghua Microelectronics Co., Ltd.: Initial public offering prospectus. 2017.3.23. http://static.cninfo.com.cn/finalpage/2017-03-23/1203188461.PDF

[6] Hangzhou Glinda Electronic Materials Co., Ltd.: Initial public offering prospectus. 2020.8.6. http://static.cninfo.com.cn/finalpage/2020-08-06/1208131136.PDF

[7] Jingrui Electronics Co., Ltd. 2022 Annual Report. 2023.4.26 http://static.cninfo.com.cn/finalpage/2023-04-26/1216592895.PDF

[8] Xu Zhixian, Yao Jijun, Hu Jiankun, Xia Xiaofeng, Lu Shuimiao, Mei Huadeng, Li Weidong. Current status and progress of analysis and detection technology for semiconductor industrial raw materials. Micro-nano Electronics and Intelligent Manufacturing, 2022, 4(01): 75-81.

[9] Li Wei. Production and development of wet chemicals for the microelectronics industry. Shanghai Chemical, 2004, 29(8): 32-35.

[10] Zhongjin Company: New Materials Series: The wave of domestic substitution has arrived, and China’s wet electronic chemical industry is ushering in a period of rapid development. https://research.cicc.com/frontend/recommend/detail?id=3052

[11] Zhang Xiaoxia. Analysis of key technologies for the preparation of electronic-grade hydrofluoric acid. Phosphate and Compound Fertilizer, 2021, 36(05): 27-29.

[12] TECHCET: Semiconductor Chemical Revenues Fall as Energy Prices Rise. Wet Chemical market decline follows wafer start slowdown. 2023.5.24. https://criticalmaterials.org/2023-techcet-news/#May24_2023

[13] Jiangyin Jianghua Microelectronics Co., Ltd. 2022 Annual Report. 2023.4.10: http://static.cninfo.com.cn/finalpage/2023-04-10/1216362629.PDF.

[14] Qin Yuanyuan. Current status of technology development in the etching liquid field of wet electronic chemicals. Chemical Management, 2022, (16): 95-98.

[15] Wang Haixia, Feng Yingguo, Zhong Weike. Current status of chemical development for integrated circuits in China. Modern Chemical Industry, 2018, 38(11): 1-7.

[16] Huazheng Securities: Leading enterprises in domestic wet electronic chemicals, new production capacity releases are promising. 2022.2.17. https://pdf.dfcfw.com/pdf/H3_AP202202181547737897_1.pdf?1645194731000.pdf

[17] Jin Hainian et al. The Dilemma of Great Powers: How to Break the “Choke Point” Problem. China Translation Publishing House, 2022.3

[18] Material New Media: Material New Depth | Wet electronic chemicals are booming in production and sales, and industry investment opportunities are being sorted out. 2022.9.6. https://mp.weixin.qq.com/s/RG3JHC84_cuUnur_wVAAmA

[19] Feng Li, Zhu Lei. Analysis of the current status of China’s integrated circuit materials industry development. Journal of Functional Materials and Devices, 2020, 26(03): 191-196.

[20] Ping An Securities: Riding the Wind of Demand Recovery, Walking the Path of Domestic Substitution – Nonferrous and New Materials Mid-Year Strategy Report 2023.6.13. https://pdf.dfcfw.com/pdf/H301_AP202306141590928612_1.pdf

[21] SIA: Comments of the Semiconductor Industry Association (SIA) On the CHIPS Program Office Request for Information On Implementation of the CHIPS Incentives Program. 2022.11.14. https://www.semiconductors.org/wp-content/uploads/2022/11/SIA-CPO-CHIPS-RFI-Response-11_14_22.pdf

[22] Yu Chen, Gu Fang, Lu Ying, Xiao Jiaohong, Bai Yang, Zhu Wenhan. Analysis of the development of electronic chemical technology. Fine and Specialty Chemicals, 2022, 30(01): 8-11.

[23] National New Materials Industry Development Expert Advisory Committee. China New Materials Industry Development Report (2020). Metallurgical Industry Press, 2021.10.01

[24] BASF completes acquisition of Merck’s electronic chemicals business. Integrated Circuit Applications, 2005(05): 70.

[25] PR Newswire: Merck completes acquisition of Versum Materials. 2019.10.11. https://www.prnasia.com/story/260360-1.shtml

[26] Nikkei Chinese Network: Daikin’s new technology breaks dependence on Chinese hydrogen fluoride raw materials. 2022.3.9. https://cn.nikkei.com/industry/manufacturing/47868-2022-03-09-09-05-28.html

If you are an investor, a member of a startup team, or a researcher interested in the closed-door meetings or other innovation services organized by Guoke Hard Technology, please scan the QR code below, or reply “Enterprise WeChat” in the WeChat public account backend to add our event service assistant. We will organize activities through this channel.