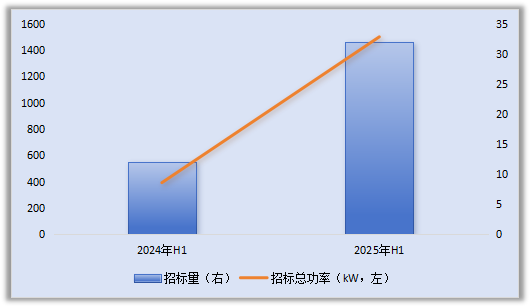

With the end of the first demonstration period for fuel cell vehicles, the hydrogen energy industry chain has officially entered a new development model driven by policy guidance and technological innovation. The fuel cell stack, represented by perfluorosulfonic acid proton exchange membrane fuel cells, is making breakthroughs in the critical temperature range of 90-100 degrees Celsius for wide-temperature fuel cell development. During this period of unclear policy and critical technological research and development, the performance of different technological paths in the fuel cell market has shown significant differences: in the first half of this year, the production and sales of fuel cell vehicles were 1,364 and 1,373 units respectively, both down by half year-on-year; while the SOC/SOEC (hereinafter referred to as “SOC”) market saw a substantial increase in both order volume and installed capacity.【DT New Energy】 database shows that the SOC market experienced explosive growth in the first half of this year, with over 30 equipment bidding projects and a total power reaching the megawatt level, already exceeding the total for the entire year of 2024. Renewable Hydrogen1. Overall Situation: 32 new SOC bids in the first half of 2025, total power reaching megawatt levelNumber of projects increased by 167% year-on-year.According to the plan, the domestic energy consumption dual control policy will shift from the 14th Five-Year Plan to a dual control system for carbon emissions. As the national hydrogen energy industry demonstration synchronously enters the next stage, higher performance and higher technological content have become the core vocabulary of hydrogen energy development. Consequently, governments, enterprises, and research institutions have increased their research and demonstration efforts on SOC. 【DT New Energy】 database shows that in the first half of 2025, 32 new SOC bidding projects were added nationwide, a year-on-year increase of 167%. According to the trends in the hydrogen energy industry, various projects are mainly concentrated in the second half of the year, and it is expected that this year’s SOC bidding volume will achieve significant growth compared to last year. Total power surged by 282%, with the largest project reaching the megawatt level. With the continuous advancement of SOC demonstrations in recent years, SOC products have also completed the first stage of technical verification. More and more enterprises have passed the small-scale and pilot testing stages, leading to a significant increase in the power of single projects. Statistics show that the total installed power of newly added SOC bidding projects nationwide in the first half of this year reached 1.5 MW, a year-on-year increase of 282%, with a single project from China General Nuclear Power Group reaching 1.1 MW.Chart 1 Overall Situation of SOC Bidding in H1 2024 and H1 2025 Source: DT Database, DT New Energy MappingPower and other downstream applications and related parties have become the main force in bidding. From the perspective of bidding units, unlike previous years where universities dominated, in the first half of this year, enterprises in downstream applications such as power and shipping, along with their research institutes, have become one of the main forces in bidding. This also indirectly indicates that the SOC industry chain, after years of technical verification, has entered a new stage of industrial development.

Source: DT Database, DT New Energy MappingPower and other downstream applications and related parties have become the main force in bidding. From the perspective of bidding units, unlike previous years where universities dominated, in the first half of this year, enterprises in downstream applications such as power and shipping, along with their research institutes, have become one of the main forces in bidding. This also indirectly indicates that the SOC industry chain, after years of technical verification, has entered a new stage of industrial development.

Renewable Hydrogen2. Product Type Situation: EC and FC “Dual Pillars”, Initial Coordination Effect of the Industry

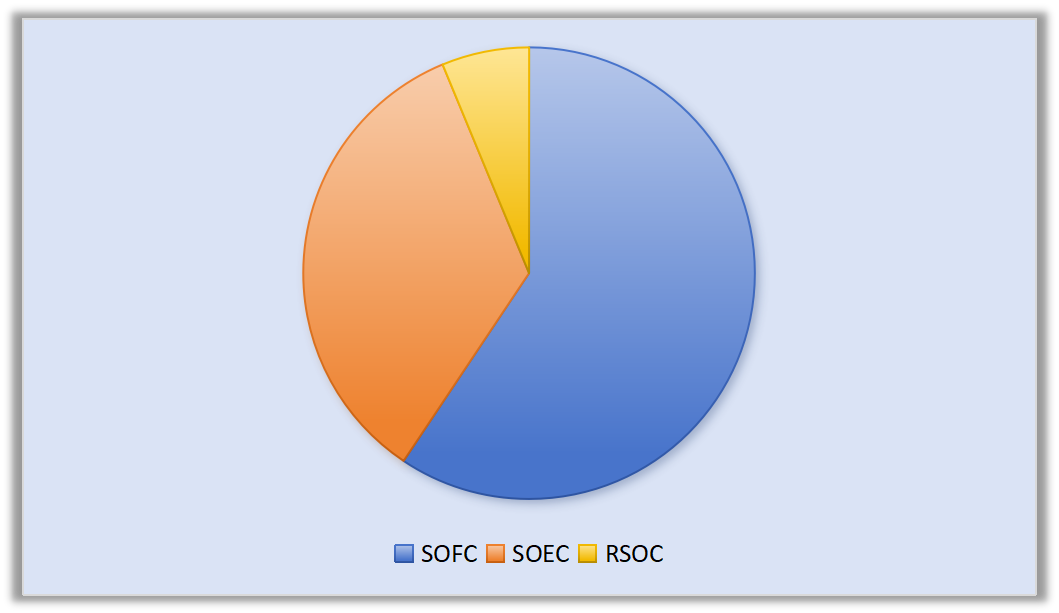

Significant growth in SOEC project numbers.Among the 32 new bidding projects in the first half of the year, the proportions of SOFC, SOEC, and RSOC were 60%, 34%, and 6% respectively, with SOEC showing significant growth, initially presenting a situation of “dual pillars” with SOFC. On the other hand, as more downstream application enterprises became the main force in bidding in the first half of the year, the system procurement volume also increased significantly. Chart 2 Equipment Classification of SOC Bidding Projects in H1 2025 Source: DT Database, DT New Energy MappingIncrease in projects using methanol, ammonia, and other fuels.With the promotion of numerous green ammonia and green methanol projects in recent years, the research and demonstration of related industry chains have significantly increased. Taking the SOFC projects bid in the first half of the year as an example, in addition to conventional hydrogen and gas as project fuels, there has been a significant increase in projects using methanol and ammonia as fuels. Companies such as Zhejiang Hydrogen Bond Technology Co., Ltd. (hereinafter referred to as “Hydrogen Bond Technology”) have won related projects, and the synergistic effect of the entire hydrogen energy industry is beginning to emerge. Due to the strong adaptability of SOFC to fuels, it is expected that future projects using ammonia and methanol as fuels will further increase, with Geely Sichuan College also conducting related demonstrations.

Source: DT Database, DT New Energy MappingIncrease in projects using methanol, ammonia, and other fuels.With the promotion of numerous green ammonia and green methanol projects in recent years, the research and demonstration of related industry chains have significantly increased. Taking the SOFC projects bid in the first half of the year as an example, in addition to conventional hydrogen and gas as project fuels, there has been a significant increase in projects using methanol and ammonia as fuels. Companies such as Zhejiang Hydrogen Bond Technology Co., Ltd. (hereinafter referred to as “Hydrogen Bond Technology”) have won related projects, and the synergistic effect of the entire hydrogen energy industry is beginning to emerge. Due to the strong adaptability of SOFC to fuels, it is expected that future projects using ammonia and methanol as fuels will further increase, with Geely Sichuan College also conducting related demonstrations.

Renewable Hydrogen3. Application Fields Further Diversified

Increase in marine and hydrogen-electric coupling projects.With the initial completion of technical verification in the industry, major stakeholders are beginning to promote the application demonstration of SOC equipment in various terminals. For example, in the first half of the year, the China Shipbuilding Research and Design Center released a marine SOFC system project, with Huazhong University of Science and Technology and others participating in the R&D work of this project. In addition, enterprises related to power energy, such as Guangdong Power Grid Co., Ltd. Guangzhou Power Supply Bureau, China General Nuclear Power Research Institute Co., Ltd., and Beijing Jingneng Digital Technology Co., Ltd., have released bids for SOC products for hydrogen-electric coupling. With the advancement of new power systems and increased investment in distribution networks, projects such as hydrogen-electric coupling are expected to further increase. The exploratory spirit of enterprises deserves attention from the government and other sectors. Based on the bidding project situation in the first half of the year, major enterprises and research institutions have shown a strong exploratory spirit in the demonstration of SOC, whether in product technology scaling or downstream applications. The domestic industry is promoting the process from “0 to 1”. For example, in the first half of the year, Hydrogen Bond Technology made significant progress in exploring diversified applications, achieving breakthroughs in fixed power generation systems in the field and mobile power generation systems for vehicles and ships.

Renewable Hydrogen4. Winning Enterprises Situation: Xi’an Rare Institute ranks first, Proton Power and Yijing Energy rank first in installed capacity

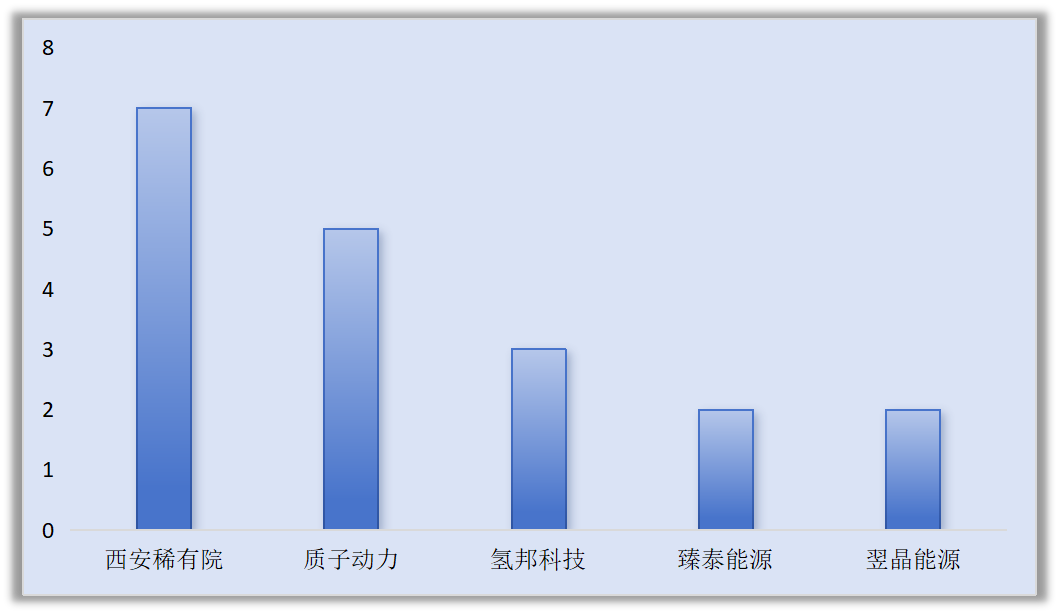

13 enterprises won bids, with an increase in enterprises going abroad.As of the date of publication, many projects have not yet announced the winning situation. A total of 13 enterprises have won bids. Since the data released this time only counts the newly added bidding projects domestically, according to enterprise feedback, the situation of enterprises exporting has significantly increased. For instance, Yijing Energy has three overseas projects in the first half of this year, with the highest single project exceeding 100 kW. In the past, new energy sectors such as photovoltaics and lithium batteries have experienced a transition from technology import to technology export, and the future of hydrogen energy in China is expected to follow this process. Xi’an Rare Institute ranks first in quantity.From the announced winning project situation, Xi’an Rare Institute ranks first, Proton Power ranks second, and Hydrogen Bond Technology ranks third. Chart 3 Top 5 Enterprises in the Number of Winning SOC Bidding Projects in H1 2025 Source: DT Database, DT New Energy Mapping

Source: DT Database, DT New Energy Mapping

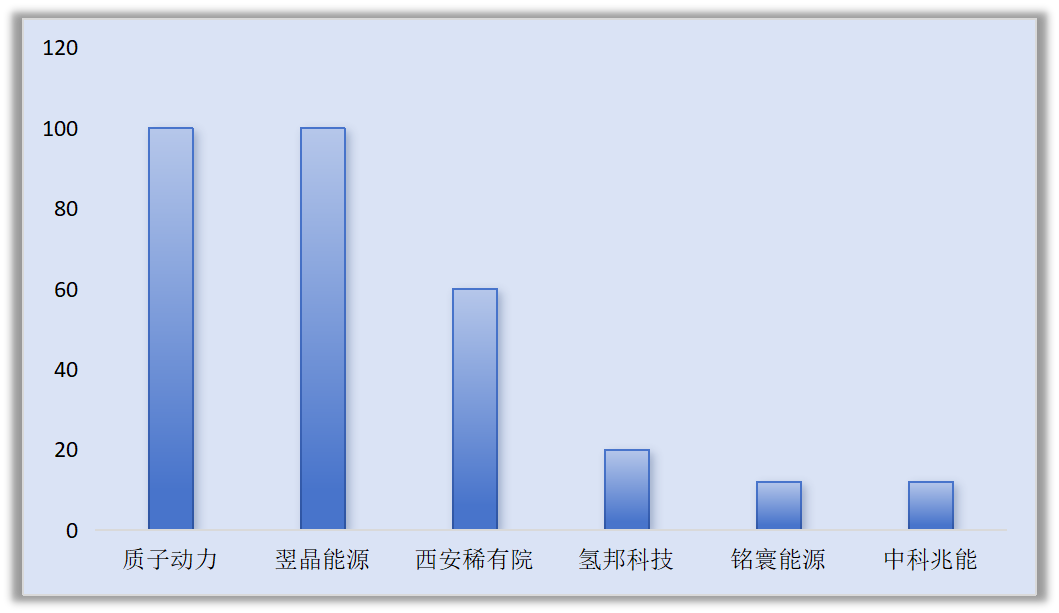

Proton Power and Yijing Energy rank first in installed capacity.From the announced winning project installation situation, Proton Power and Yijing Energy rank first in installed capacity, while Xi’an Rare Institute ranks third.

Chart 4 Top 5 Enterprises in Installed Capacity of SOC Bidding Projects in H1 2025 Source: DT Database, DT New Energy Mapping

Source: DT Database, DT New Energy Mapping

Will the China Shipbuilding Industry enter the SOEC field?It is worth mentioning that in the first half of the year, China Shipbuilding 718 Institute released a procurement for SOEC products. Currently, China Shipbuilding 718 Institute’s subsidiary, Pairui Hydrogen Energy, has laid out three technical routes: alkaline, PEM, and AEM. With the continuous development of the hydrogen energy industry, it is not surprising that the China Shipbuilding Industry enters the SOEC field.

Note:This article partially references materials from the DT database and DT New Energy. If you have any questions, please leave a message or contact us at 17306887109.

Welcome to Exchange

Focusing onSOC key technologies, materials and system integration, commercialization progress, market development, and other hot topics, gathering leading industry experts, research teams, and entrepreneurs in the SOEC/SOFC industry to discuss and exchange trends in industrial development and directions for industrialization. You are welcome to join the SOC exchange group.

Conference consultation, group exchange

Shen Fei: 13396601161 (WeChat same number)