–

Today marks the 3343th day of our journey together.

Today’s Article from Danrenxing ↓↓↓

Today’s Article from Danrenxing ↓↓↓

01

Recently, the launch of Xiaomi’s self-developed 3nm Xuanjie chip has garnered significant attention in the chip industry.

Many are concerned about the development of Chinese chips: Will Xiaomi face U.S. sanctions? What is the status of Huawei’s chips?

In fact, just last week, the chip industry, especially China’s high-end chips, experienced significant changes and opportunities.

On May 13, the U.S. Department of Commerce suddenly revoked the “AI Diffusion Rules” proposed by the previous Biden administration, lifting export restrictions on high-end chips.

However, at the same time, it issued a stern warning to global manufacturers using Huawei’s Ascend chips: if they continue to use the Ascend 910 or 310 series chips, they will face hefty fines, and responsible individuals could face up to 20 years in prison.

On the surface, it seems that the U.S. has relaxed export restrictions on high-end chips, but it has separately warned global companies against using Huawei’s Ascend chips.

Is this truly a relaxation, or not? What kind of Chinese companies and chips will not be sanctioned by the U.S.?

We will examine this from the perspective of national and corporate competition, looking at different competitive logics.

02

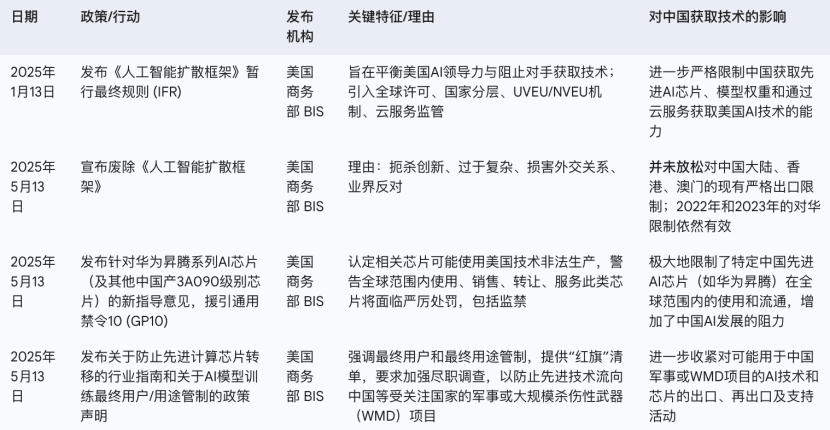

On January 13 of this year, before the Biden administration transitioned, the final interim rules for the “AI Diffusion Framework” were released.

This framework has three key mechanisms.

The first is the global licensing requirement for the export of the most advanced chips, computing devices, related AI technologies, and specific closed AI models, along with regulation of cloud service access.

The second is the classification of global countries into three categories. The first category is the whitelist, including allies like Japan, the UK, and Australia, which can receive advanced chips and AI products without quantity restrictions or approval.

The second category is the blacklist, which includes 23 countries and regions, including China and Russia, that are prohibited from receiving exports.

The third category is the middle category, which includes other countries that require special authorization for exports.

The third mechanism requires U.S. companies and trusted entities, such as TSMC and ASML, to build data centers and manufacture chips anywhere outside the blacklist.

However, they must keep 50% of AI computing power and data center infrastructure in the U.S., with at least 75% retained in the U.S. and whitelist countries, and no more than 7% in any other single country.

The “AI Diffusion Rules” issued by the Biden administration cover a wide range and extend from hardware to corporate technology, services, investment, and export.

Essentially, the U.S. aims to use administrative means to establish market access barriers, creating an AI industry and chip supply chain ecosystem led by itself.

The U.S. places extreme importance on AI and semiconductors, and its primary target is China’s AI and chip industry.

From the goals of this rule, the U.S. attitude towards competition is not about enlarging the pie and sharing benefits, even if it means taking the largest share.

Rather, it is a complete zero-sum game, with no room for easing; the U.S. would rather see technology stagnate and businesses fail than lose its so-called lead.

It’s like a rainy day: the U.S. holds an umbrella while watching others get soaked; if others want to make their own umbrellas, the U.S. would rather not use its umbrella than let others have theirs.

03

So, why did the U.S. suddenly cancel this rule? Did Trump suddenly become benevolent?

In fact, the implementation of this rule is very complex, affecting many countries and regions, and has faced strong dissatisfaction from U.S. companies, as it not only impacts their business but also incurs additional costs to comply with regulatory requirements.

This is somewhat similar to the recent U.S.-China tariff conflict: the U.S. had a well-thought-out plan, imposing high tariffs and blocking transshipment trade from surrounding countries, only to find itself unable to bear the consequences first.

NVIDIA CEO Jensen Huang stated, “Four years ago, NVIDIA had a 95% market share in China, but today it is only 50%, with the rest being local technology. Even without NVIDIA, they would still use a lot of domestic technology.”

Previously, NVIDIA launched a performance-reduced version of the H20 chip for the Chinese market to comply with export control regulations, resulting in a $5.5 billion asset write-down.

Mainland China is NVIDIA’s fourth-largest market, with revenue in the China region reaching $17.108 billion in 2024, a year-on-year increase of 66%.

Of course, if we include Singapore, this small country of 6 million people accounts for 20% of NVIDIA’s revenue, even surpassing that of mainland China, making Singapore a significant transshipment trade channel for China. The mainland market is extremely important for NVIDIA and is growing rapidly.

If the rules were strictly enforced, industry analysts believe NVIDIA could lose at least $14-18 billion in revenue by 2025, which translates to over 130 billion RMB lost.

Thus, NVIDIA is leading the opposition against AI and chip restriction policies.

Huang stated, “It has been proven that the fundamental assumptions behind the initial AI and chip export restrictions are fundamentally flawed. If the U.S. wants to maintain its leading position, we need to maximize technology diffusion rather than restrict it.”

In fact, companies like NVIDIA and AMD understand this.

The U.S. restrictions have largely stimulated Chinese companies’ determination and investment in independent research and development.

Restrictions have instead provided greater motivation and more government support for Chinese companies, from establishing semiconductor industry funds to vigorously promoting DeepSeek. China is mobilizing national efforts to advance semiconductor and AI product development.

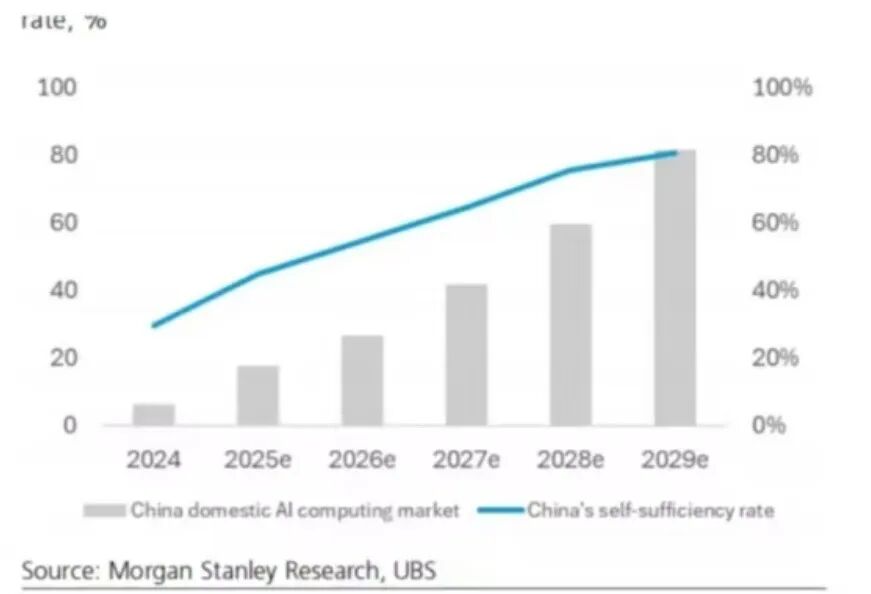

According to IDC data, by the second half of 2024, the self-sufficiency rate of chips in newly built data centers in China will reach 34%, compared to only 10% in the first half of 2023.

It is expected that by 2026, the scale of China’s AI market will reach $50 billion, and by 2029, the self-sufficiency rate of AI chips in China will reach 80%.

This represents a “dilemma of innovators” faced by U.S. companies.

If cooperation and exports are genuinely restricted, it will lead to significant market losses for companies and accelerate the pace of independent innovation among Chinese companies, ultimately undermining their own competitive advantage.

Therefore, Huang proposed the idea of “maximizing diffusion,” which is an alternative competitive strategy that aims to maintain technological leadership and rapid global market entry to outpace potential competitors.

A typical case is the Windows operating system from years ago.

Microsoft once took a tacit approach to piracy, especially turning a blind eye to end-user and small business usage, sacrificing short-term revenue for the widespread adoption of the Windows operating system globally and establishing an ecosystem lock-in, thereby cultivating user habits and establishing its market dominance.

Ultimately, Microsoft profited from software ecosystems, subsequent version sales, and corporate licensing, at which point it faced no significant competitors in the market, and users had no alternative products, achieving a de facto monopoly.

This is a competitive strategy for enterprises, leveraging product leadership and marketing offensives to quickly enter the market, cultivate user recognition and usage habits to dominate the market.

The best defense is a proactive offense, rather than retreating and closing off, thinking that if competitors cannot use my products and services, they will not develop.

04

From the perspective of market competition and enterprises, if the U.S. continues to maintain the “AI Diffusion Rules,” it would actually be beneficial for China, only further stimulating Chinese companies’ determination for self-reliance.

Conversely, if the restrictions are truly lifted as Huang suggested, it could lead to “technological dumping” and “user dependency,” reminiscent of the past victories of Windows.

Of course, the U.S. chose OR between YES and NO, abolishing the “AI Diffusion Rules,” thus preserving transshipment trade channels while still imposing strict export restrictions on China, specifically targeting high-end AI chips from Huawei with a kill order.

We believe this is a strategy of “small courtyard and high walls.”

What does this mean?

It allows for broader commercial activities without strictly controlling the business interactions and technological scope of semiconductor and AI companies.

However, the U.S. is not completely laissez-faire; it will precisely identify specific key technologies and companies (the small courtyard) and impose high-intensity restrictions (the high walls) on them.

Targeting Huawei is an example of this strategy.

The U.S. will gradually identify the “pearls” of Chinese technology and find the companies behind these technologies, then apply greater pressure at these points, using all means to cut off potential development channels and trade routes for these companies.

This also answers the question: “What kind of Chinese companies will not be sanctioned by the U.S.?”

Therefore, for many of our companies, tariff trade barriers may gradually be dismantled through long-term negotiations, but technological competition will intensify, especially in core technologies and intellectual property that are self-controllable, requiring continuous accumulation and sustained investment in innovation.

—Editor | Luo Yingfan

Images are sourced from the internet

This article does not constitute any investment advice; the stock market carries risks, and investments should be made cautiously.

■ Disclaimer

This article involves content related to listed companies, based on the author’s personal analysis and judgment of information disclosed by listed companies in accordance with their legal obligations (including but not limited to temporary announcements, periodic reports, and official interactive platforms); the information or opinions in this article do not constitute any investment or other business advice, and Market Value Observation does not bear any responsibility for any actions taken as a result of adopting this article.