Driven by the explosive growth of AI computing power and domestic substitution, the semiconductor equipment industry is facing unprecedented investment opportunities. As the technological competition between China and the U.S. intensifies, the proportion of domestic chip procurement continues to rise. Semiconductor equipment, as a “bottleneck” in the upstream of the industrial chain, has become a core national strategy. According to SEMI’s forecast, the global semiconductor equipment market will exceed $127 billion by 2025, with mainland China leading the world in growth as the largest market. The National Big Fund’s third phase, with a focus on the equipment sector, combined with the expansion wave of downstream wafer fabs, has ushered in a golden development period for domestic equipment manufacturers. This article will deeply analyze the core equipment track of semiconductors, revealing the investment lines that investors should not miss.

Semiconductor Equipment: The Cornerstone of the Industrial Chain and the Breakthrough Point for Domestic Substitution

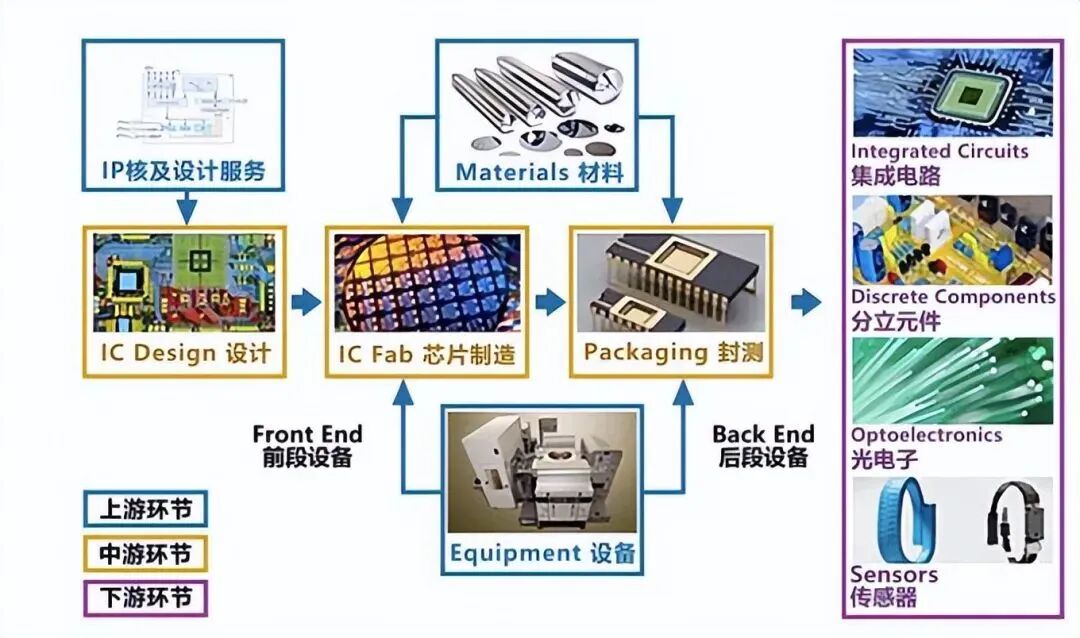

Semiconductor equipment is the “mother machine” of chip manufacturing, directly determining the process level and yield. Currently, driven by the emerging demand for AI computing power, the industry’s prosperity is accelerating. Semiconductor equipment encompasses two major processes: front-end manufacturing (accounting for 90% of the market) and back-end packaging and testing, involving 11 categories and over 50 types of specialized equipment.

Data sources indicate that the equipment market is highly concentrated, but domestic manufacturers are breaking through in key areas such as etching and lithography. As major domestic manufacturers expand advanced processes, equipment demand will continue to explode, providing investors with ample layout space.

Core Equipment Analysis: Breakthrough Points for Domestic Substitution and Investment Opportunities

1. Etching Equipment: Domestic Leaders Leading Technological Breakthroughs

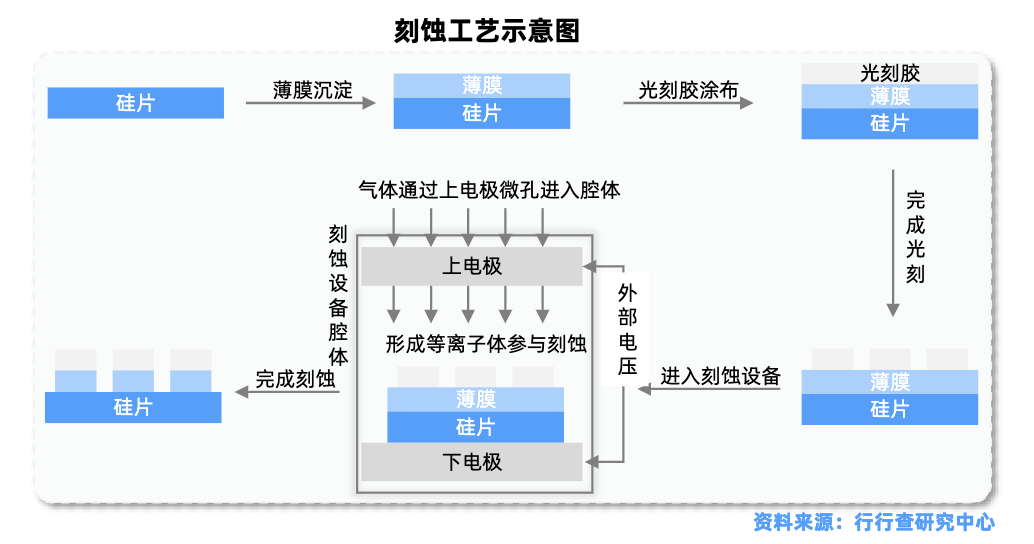

Etching equipment is one of the three core devices in chip manufacturing, responsible for transferring patterns to functional layers, forming the microscopic structure of integrated circuits. Dry etching is the mainstream technology, with global market share dominated by overseas giants such as Lam Research and Tokyo Electron, holding 90% of the market. However, domestic manufacturers have achieved significant breakthroughs:

- •

SMIC: CCP and ICP etching equipment cover 90% of application scenarios, with technology reaching international advanced levels.

- •

North Huachuang: Self-developed ICP equipment achieves full process coverage, accelerating integration into domestic production lines.

Etching process diagram below shows its precision processing capabilities:

The market share of domestic etching equipment continues to rise, benefiting from the expansion of logic chips, with a compound annual growth rate expected to exceed 30% in the next three years, making it a high-growth track for investors.

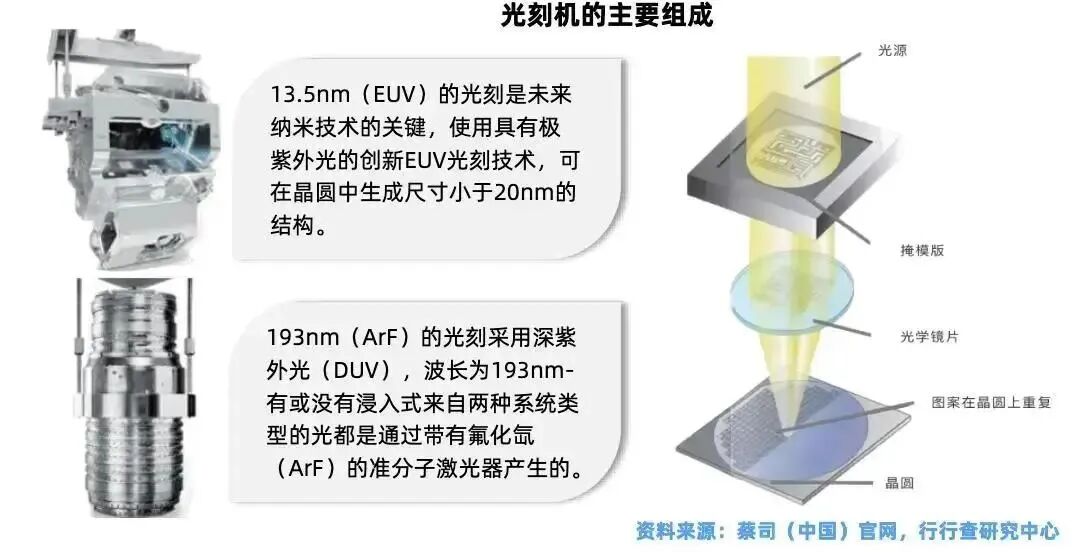

2. Lithography Equipment: The Highest Technological Barriers, Domestic Chain Accelerating Breakthroughs

Lithography processes account for one-third of chip production costs, and lithography machines (photo lithography machines) are the devices with the highest technological barriers, with over 80,000 parts in EUV models. The global market is dominated by ASML, but a complete domestic industrial chain has been established:

- •

Complete Machine Integration: Shanghai Micro Electronics leads the design, with HW, Yuliangsheng, and others participating in R&D.

- •

Core Components: Key technologies have been broken through by Keyi Hongyuan (light source), Guowang Optical (objective lens), and Huazhuo Jingke (dual-workpiece stage).

- •

Supporting Materials: Nanda Optoelectronics (photoresist), Qingyi Optoelectronics (mask) have achieved domestic substitution.

The system diagram of the lithography machine shows its complexity:

Domestic 28nm lithography machines have been mass-produced, with plans to advance to 14nm, and related companies such as Shanghai Micro Electronics have significant valuation upside potential.

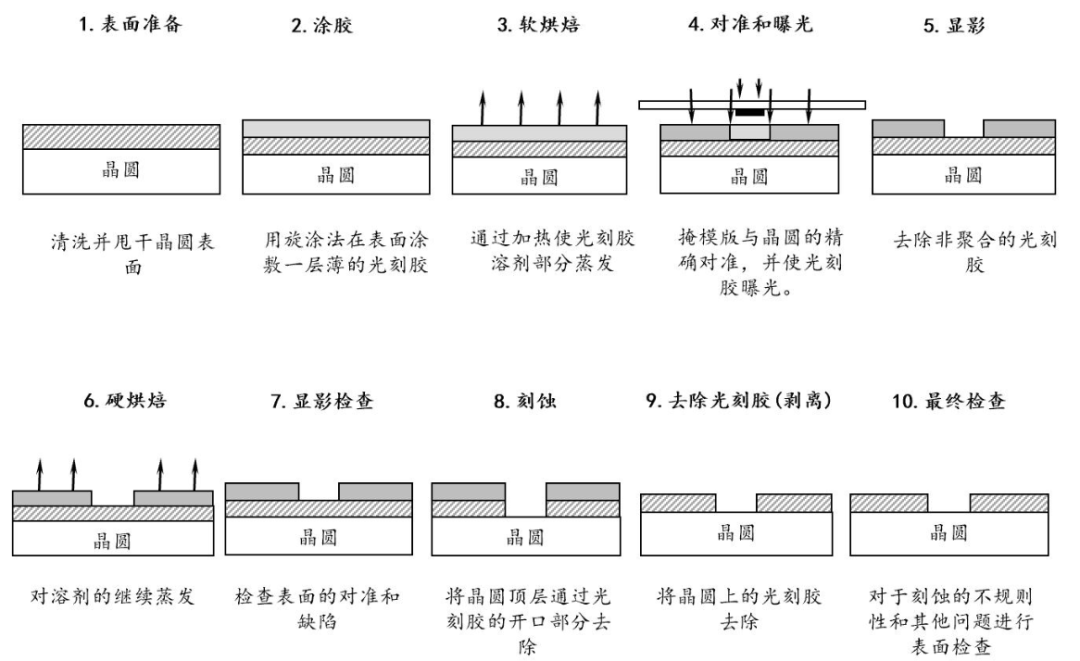

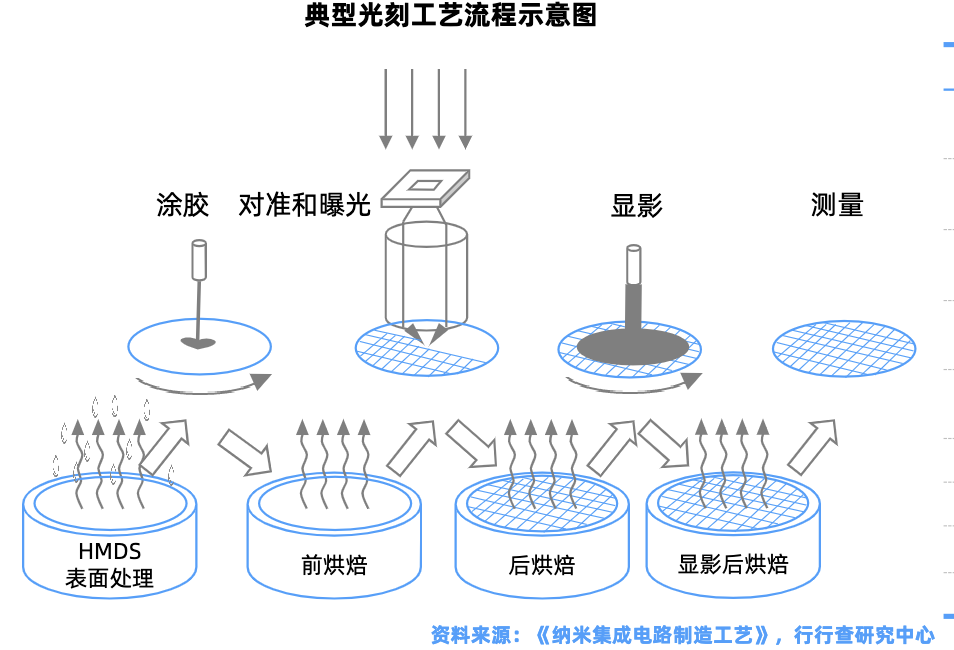

3. Coating and Developing Equipment: The “Golden Partner” of Lithography, Chip Source Micro Takes the Lead

Coating and developing equipment is the only core device that operates in conjunction with lithography machines, completing the entire process of photoresist coating, baking, and developing. The global market is dominated by Tokyo Electron, holding 90% market share, but domestic Chip Source Micro has achieved mass production of front-end equipment, receiving orders from major manufacturers for 28nm processes.

The ten-step lithography process demonstrates its critical role:

With the upgrade of AI chip processes, the demand for coating and developing equipment has surged. As the only mass producer in China, Chip Source Micro’s market share has increased from 4% to 10%, making it a rare target in this niche field.

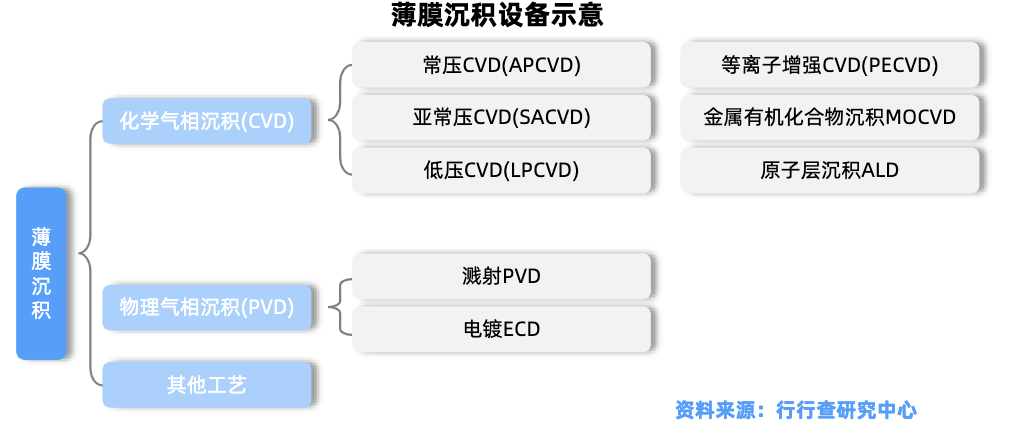

4. Thin Film Deposition Equipment: TuoJing Technology Leads the CVD Track

Thin film deposition equipment is used to build the basic structure of chips, with PECVD and sputtering PVD technologies dominating the market. Applied Materials and Tokyo Electron hold 80% market share, but domestic manufacturers are rapidly rising:

- •

TuoJing Technology: The leading domestic CVD equipment manufacturer, with a leading market share in PECVD.

- •

North Huachuang: PVD equipment breaks the overseas monopoly.

The classification diagram of thin film deposition technology is as follows:

Downstream 3D NAND and DRAM expansions drive equipment demand, with TuoJing Technology’s orders being robust and significant performance elasticity.

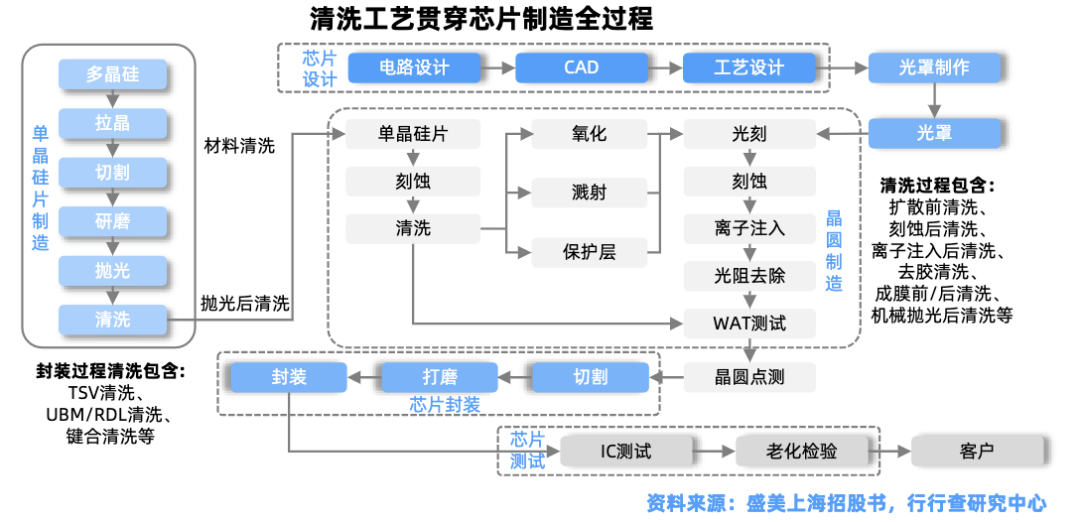

5. Cleaning Equipment: Shengmei Shanghai Leads in Technology

The cleaning step accounts for 30% of the chip manufacturing process, with wet cleaning being the mainstream method. Shengmei Shanghai has achieved a global market share of 6.6% with SAPS and TEBO ultrasonic technology, ranking fifth globally. The market structure of cleaning equipment:

As the yield requirements of wafer fabs increase, the domestic cleaning equipment penetration rate has jumped from 10% to 30%, benefiting Shengmei Shanghai and North Huachuang significantly.

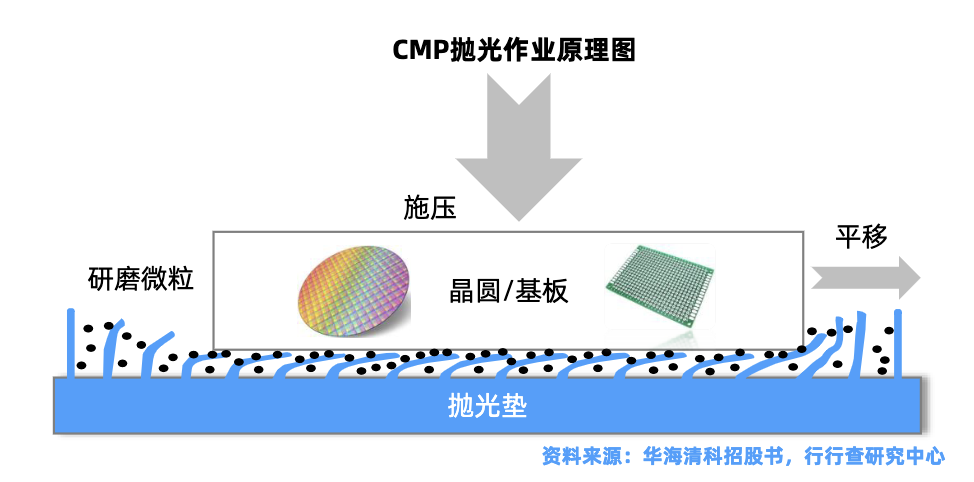

6. CMP Equipment: Huahai Qingke Breaks International Monopoly

Chemical Mechanical Polishing (CMP) is a key technology for nano-level flattening, and Huahai Qingke is the only 12-inch CMP equipment manufacturer in China, breaking the overseas monopoly as early as 2014. The equipment composition diagram is as follows:

Driven by the demand for advanced packaging, the CMP equipment market is growing at an annual rate of 15%, with Huahai Qingke as the leader, showing potential for upward valuation.

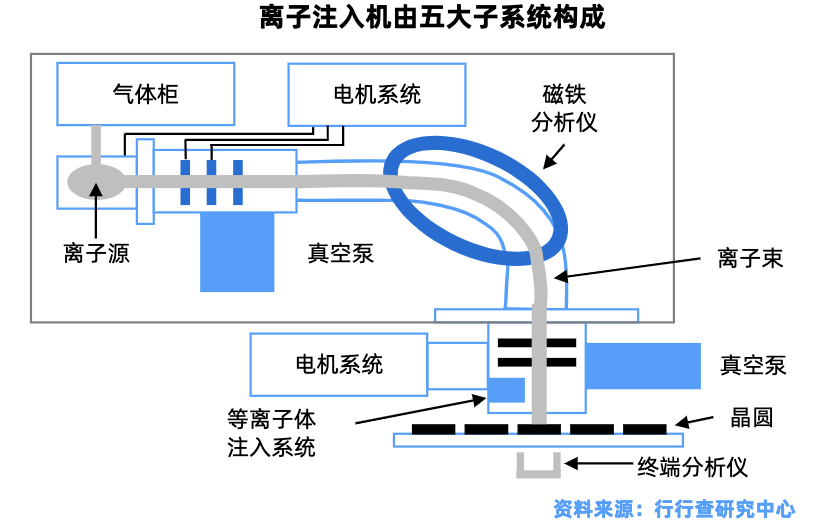

7. Ion Implantation Equipment: Kaishitong Leads the Low Energy High Current Market

Ion implantation is a core doping process, with Kaishitong leading the 12-inch low energy high current equipment market, and Zhongke Xinxin achieving full coverage of 28nm. The technology classification diagram is as follows:

Upgrades in logic chip processes drive equipment demand, with domestic manufacturers having a replacement space worth hundreds of billions.

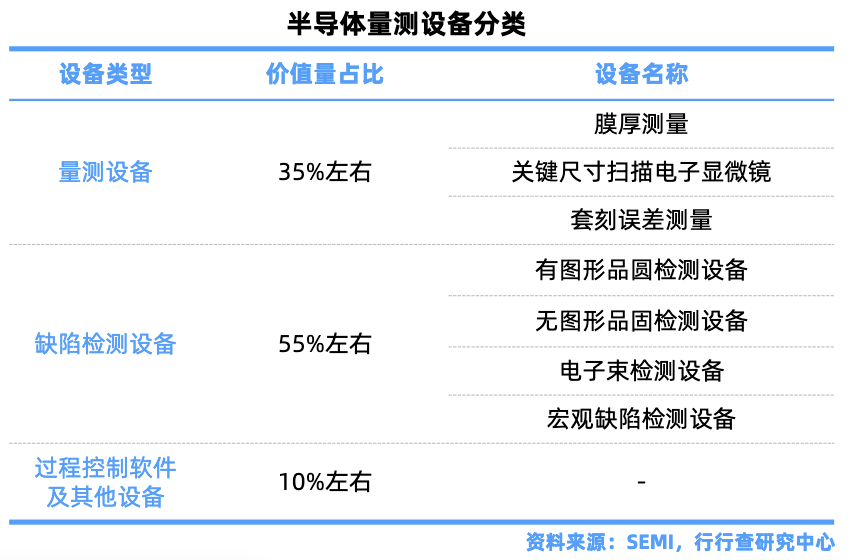

8. Measurement/Detection Equipment: Zhongke Feicai Breaks Yield Bottlenecks

Measurement and detection equipment are key to improving chip yield, with Zhongke Feicai breaking through in defect detection, breaking KLA’s monopoly. The application diagram of the equipment is as follows:

As processes below 3nm become mainstream, the measurement and detection equipment market is growing at over 20%, with domestic substitution accelerating.

9. Advanced Packaging Equipment: AI Chips Ignite Demand

AI chips and HBM memory are driving the explosion of advanced packaging equipment, with bonding equipment being the core technology. TuoJing Technology has launched the first domestically produced hybrid bonding equipment, while Qinghe Crystal has innovated dual-mode technology. The global market is dominated by ASMPT, but domestic manufacturers such as Huazhuo Jingke and Chip Source Micro are quickly following suit.

In 2024, the advanced packaging equipment market is expected to grow by 30%, with companies like TuoJing Technology benefiting from the AI computing wave.

Market Outlook: Accelerating Domestic Substitution, A Good Time for Investors to Position

SEMI data shows that global semiconductor equipment sales will reach $117.1 billion in 2024, exceeding $127 billion in 2025. The mainland China market is leading with a 20% growth rate, with domestic equipment penetration increasing from less than 10% to 30%. On the policy front, the Big Fund’s third phase focuses on supporting the equipment sector, with local government special funds increasing, forming a collaborative ecosystem of “equipment-materials-manufacturing”.

Investment Suggestions: Focus on three main lines —

- 1.

Technology Breakthrough Type: SMIC (etching), Shanghai Micro Electronics chain (lithography).

- 2.

Domestic Substitution Type: Shengmei Shanghai (cleaning), Huahai Qingke (CMP).

- 3.

Emerging Demand Type: TuoJing Technology (advanced packaging), Chip Source Micro (coating and developing).

Disclaimer: The content of this article is for industry analysis reference only and does not constitute any investment advice. The stock market has risks, and investors should proceed with caution.