Will robots also have to “pay taxes”?

At the 2025 World Robot Conference, Wang Xingxing, founder of Yushu Technology, stated in a media interview, “In the future, when robots can perform a large number of tasks like humans, the government can definitely tell companies that they will collect taxes for each robot that leaves the factory.”

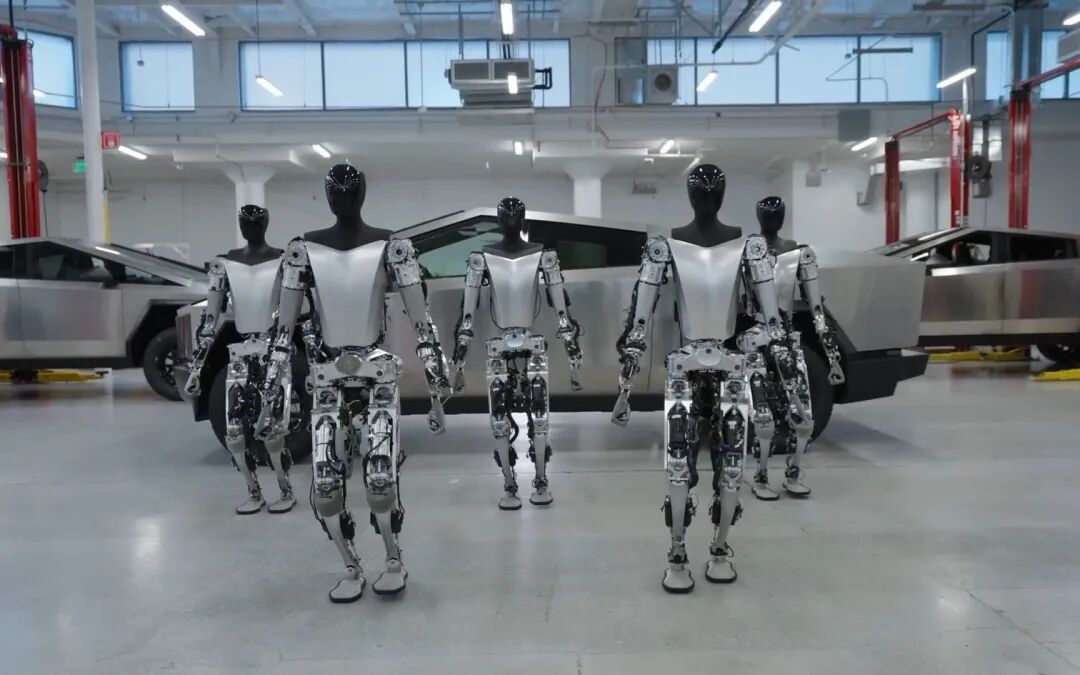

This is not a far-fetched sci-fi idea. Less than two years ago, humanoid robots were still seen as dancing stars on the Spring Festival Gala stage, with the Unitree H1 priced at 650,000 yuan, symbolizing a technological breakthrough rather than being workers on the production line.

Now, the price of the Yushu R1 has dropped to 39,900 yuan, almost equivalent to that of an economy electric vehicle.

“Automation replacing human labor” is transitioning from concept to reality.

At the same time, expectations in the international market are being continuously refreshed. Morgan Stanley’s latest report predicts that by 2050, the global market for humanoid robots will exceed $5 trillion, with nearly 1 billion units. This means that in the coming decades, we will witness a technological replacement wave comparable to the Industrial Revolution and the popularization of the Internet.

In this technological context, if robots can work like humans, the collection of a “robot tax” is not far off. What does this mean for China’s manufacturing industry?

01

Price Decline, Technological Dividends Begin to Unfold

In the past five years, the main players in China’s manufacturing automation were still “robotic arms” and “production line transformations.” However, starting in 2024, the popularity of humanoid robots has rapidly increased, not just due to media attention, but because hardware prices have seen a dramatic drop.

• In 2023, the price of the Yushu H1 was 650,000 yuan;

• In 2024, the G1 dropped to 99,000 yuan;

• By early 2025, the starting price of the R1 is 39,900 yuan.

This level of price reduction is rare even in the consumer electronics industry, let alone in the nascent humanoid robot market.

According to the latest data from Tianyancha, the number of registered companies engaged in humanoid robots and related component manufacturing has increased by 45% year-on-year, reaching nearly 1,200. Guangdong, Jiangsu, and Shanghai have significant agglomeration effects, accounting for over 40% of the overall market share. This not only reflects the rapid expansion of the industry chain but also indicates that mass production is taking shape.

The decline in humanoid robot prices is driven by three overlapping effects:

1. Mass production: As more manufacturers enter the market, the components, assembly, and testing of humanoid robots are moving towards large-scale production.

2. Localization of components: High-precision servo motors, sensors, and reducers that were previously reliant on imports are gradually being replaced by local supply chains, significantly reducing costs.

3. Adaptation of local AI models: In core areas such as motion control, speech understanding, and visual recognition, domestic large models combined with local computing power allow robots to complete more tasks without expensive cloud-based inference.

If we refer to the historical penetration curve of industrial robots, once prices enter the “psychological comfort zone,” the industry penetration rate often increases exponentially. The penetration rate of industrial robots in China was only 36 units per 10,000 workers in 2015, but by 2023, it has reached 392 units, completing in 8 years what took Japan and South Korea 20 years.

Compared to industrial robots, humanoid robots have inherent advantages in mobility and task flexibility. Once they break through key application scenarios such as logistics handling, maintenance, and assembly, their growth curve may be steeper than that of industrial robots. The price drop not only means that more companies can afford them but also allows R&D companies to collect data faster through iterations, forming a technological closed loop that further promotes positive cycles of performance and cost.

This combination of technological and cost dividends is rapidly bringing the industry from the “concept phase” closer to the “application explosion phase.” At this point,the market’s focus is no longer on “can it be done,” but rather on “how much can be done and how quickly.” After the price dividend is released, when will humanoid robots truly enter factories to replace high-risk and high-intensity human jobs?

02

The Critical Point for Application Implementation is Approaching

Humanoid robots have been very popular in the past two years, but they have not yet truly “worked” on a large scale. Currently, what we see in videos and exhibitions are mostly performances and demonstrations, which is due to audience preferences and because in actual production environments,humanoid robots still face three major obstacles to replacing human labor: task complexity, operational stability, and return on investment cycle.

In the past two years, the industry’s judgment on the pace of implementation has clearly accelerated. On one hand, technological breakthroughs are shortening debugging cycles. For example, in logistics handling, traditional industrial robots need to preset trajectories for each workstation, while humanoid robots can adjust their actions in real-time based on visual and tactile feedback. This means they can integrate into existing work environments without large-scale production line modifications.

On the other hand, companies’ attitudes towards pilot projects are also changing. Products like Yushu Technology’s R1, Tesla’s Optimus, and Toyota’s T-HR3 are beginning to enter the “real scene” testing phase in manufacturing, warehousing, and healthcare industries. Yushu revealed in a media interview that a domestic auto parts factory has deployed the R1 for material handling and simple assembly, replacing two night shift workers, with the payback period for one machine compressed to less than 18 months.

This change in ROI is crucial for corporate decision-making. In the past, investments in industrial robots often required a payback period of 3 to 5 years, but once humanoid robots bring the payback period down to less than 2 years, demand will no longer depend on “whether it is worth trying,” but will shift to “how to quickly deploy more.”

From a competitive landscape perspective, domestic humanoid robot manufacturers are forming two routes:

• There are full-stack players like Yushu Technology and UBTECH, integrating research and development from hardware to AI models, attempting to form end-to-end product barriers.

• There are also modular suppliers like Yunsen Technology and Hesai Technology, focusing on single-point components such as sensors and actuators, entering the supply chains of multiple complete machine manufacturers at lower costs.

This division of labor accelerates product maturity in the industry while reducing the trial-and-error costs for individual companies. Just like the smartphone industry in 2010, once the costs and performance standards of components are standardized, product iterations will enter the fast lane, and application scenarios will expand explosively in a short time.

Therefore,the real critical point is not the technology itself, but when multiple companies achieve positive ROI in various industry pilot projects, and the supply chain can simultaneously meet the demands of large-scale production, the market will quickly transition from “concept” to “necessity.”

The first round of industry reshuffling may be completed in terms of production capacity and channel layout, rather than in laboratories. Companies like Yushu are seizing market share with pricing while diversifying risks through overseas expansion, which also means that the future leaders in China’s humanoid robot market may likely follow a path of first capturing the global market and then feeding back domestic demand.

03

Once the Critical Point is Surpassed, Growth Will Be Exponential

Morgan Stanley’s prediction is just the tip of the iceberg. By 2050, the $5 trillion global humanoid robot market means millions of new units will be produced and deployed each year. However, for manufacturers, the decisive factor is not “whether to do it,” but who can occupy the high ground of production capacity and supply chain before the explosion.

In the past, the penetration curve for industrial robots in Japan and South Korea showed a turning point when prices fell below 1.5 times the per capita GDP, completing the leap from “few trials” to “industry-wide adoption” within 3 to 5 years. In China, from 2016 to 2021, the price of industrial robots dropped by about 30%, while shipments increased nearly threefold; once prices continue to decline, the response from the incremental market will be faster than that of Japan and South Korea.

Therefore, referring to the development path of industrial robots, the conditions for accelerating the humanoid robot market are more sensitive. Humanoid robots have high cross-industry portability; the same robot can switch between different vertical fields with just a change of task algorithms and end tools, significantly reducing expansion costs. Additionally, the speed of AI iteration and embodied intelligent model upgrades is less constrained by hardware than mechanical modifications, relying more on computing power and algorithm optimization, which means performance improvements may approach the speed of consumer-grade electronic products.

Currently, the annual production capacity of leading domestic humanoid robot manufacturers is still in the tens of thousands, but driven by both the capital market and complete machine manufacturers, it is expected that by 2027, the total industry capacity will exceed 1 million units. At that time, even if calculated based on a low-end model priced at 30,000 yuan, the market scale will approach 30 billion yuan, and this is just the basic model for “physical labor,” excluding high-value-added fields such as healthcare, services, and military.

More importantly, industry differentiation will become apparent in the early stages of the explosion:

• Companies with full-stack R&D capabilities will lock in high-value and complex task scenarios, forming high-margin segments.

• Manufacturers focusing on low-cost, popular robots will compete for market share through scale and channels, adopting a low-margin, high-volume strategy.

• Component and AI model suppliers may become the most profitable segments, similar to players in the smartphone supply chain that produce screens, chips, and operating systems.

In this landscape, the “robot tax” will not just be a policy topic but will become part of the industry’s cost structure, forcing companies to make more aggressive choices in pricing, deployment pace, and global market layout. In other words, the real competition does not happen at the conference site, but in the supply chain lock-in battle on the eve of the explosion.

When the three curves of price, capacity, and ROI cross the threshold simultaneously, humanoid robots will penetrate various industries at a geometric speed, leaving less than two years for latecomers.

Today’s 39,900 yuan may be the moment of the future “10,000 yuan smart machine.” Once the threshold is crossed, the rest will be exponential replication, and the “robot tax” may become a part of daily life in the future.

Disclaimer: This article is based on the company’s statutory disclosure content and publicly available information, and comments are made, but the author does not guarantee the completeness and timeliness of this information.

Additionally: The stock market has risks, and investment should be approached with caution. This article does not constitute investment advice, and investment decisions should be made independently.

END

Original production by the financial self-media “Blueberry Finance,”

Unauthorized reproduction is prohibited.

For business cooperation, please add WeChat: 615872972