Global technology giant Samsung Electronics is facing severe challenges.

In the second quarter of 2025, Samsung Electronics delivered a concerning report card. The company’s sales increased slightly by 0.67% year-on-year, but operating profit plummeted by 55.23% year-on-year, to approximately 24.35 billion RMB (4.6761 trillion KRW), marking a six-quarter low. The operating profit from the semiconductor business, which once contributed over half of the profits, has dropped by 94%, leaving only about 2.08 billion RMB.

Semiconductor Business Under Pressure

The Device Solutions (DS) division responsible for chip business reported sales of approximately 145.08 billion RMB, an 11% increase quarter-on-quarter, but the operating profit was only about 2.08 billion RMB, a sharp decrease of approximately 4.16 billion RMB quarter-on-quarter.

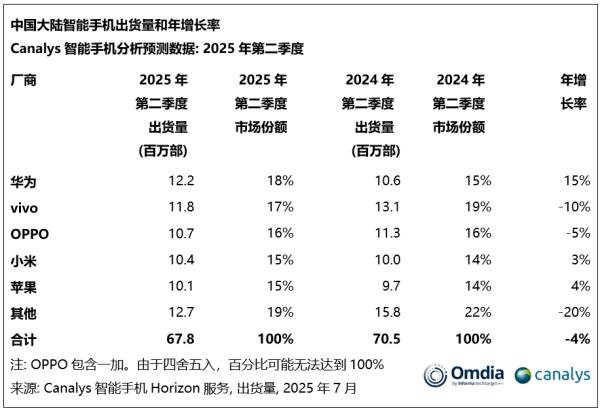

Regional market performance shows a polarization. Samsung’s smartphone market share in China has dropped to 0.77%, completely exiting mainstream competition.

However, its components business remains strong, especially in the memory chip sector, where its global market share remains around 40%, and the OLED panel business continues to dominate the high-end market.

Intertwined Internal and External Factors

The difficulties currently faced by Samsung are the result of multiple factors.

The global semiconductor industry is experiencing a cyclical downturn. As a “barometer” of the semiconductor industry, memory chip prices are the most volatile. As the world’s largest memory chip manufacturer, Samsung has endured significant pressure during this downturn. On one hand, weak demand has led customers to cut orders, resulting in a decrease in inventory value; on the other hand, intensified industry price wars have further compressed profit margins.

Additionally, the strong rise of competitors is a challenge. TSMC holds a 67.6% market share in the foundry sector, far exceeding Samsung’s 7.7%; in the HBM chip sector, SK Hynix has gained a leading advantage.

On the technical front, Samsung faces challenges in advanced process technology. The yield issues with the 3nm process have not been fully resolved, affecting its competitiveness against TSMC. At the same time, delays in HBM chip development have resulted in missed orders from key customers like NVIDIA.

U.S. restrictions on chip exports to China have impacted Samsung’s semiconductor business market expansion, while the rise of domestic Chinese companies is changing the competitive landscape. Companies like Yangtze Memory Technologies and ChangXin Memory Technologies are making breakthroughs in the memory chip sector, while smartphone brands like Huawei and Xiaomi dominate the end market.

Challenges and Opportunities Coexist

In the face of current challenges, Samsung is advancing a deep transformation strategy.

The company has identified artificial intelligence as a core growth area, announcing plans to achieve 90% AI integration in its devices by 2030, embedding AI features in 400 million Galaxy phones annually. In 2024, Samsung’s R&D investment growth rate ranks first among global semiconductor companies, demonstrating its determination to increase innovation.

In the short term, Samsung’s performance may rebound due to new product launches and improvements in HBM chip shipments. However, in the long term, Samsung needs to redefine its position in the global supply chain—whether to continue pursuing technological omnipotence or to focus on its strengths. The answers to these questions will determine whether Samsung can be reborn.

Samsung’s rise and fall serves as a mirror reflecting the brutal competition and unpredictable changes in the global technology industry.