⏱️ Reading time: Approximately 10 minutes

✨ Follow us for more quantitative knowledge insights

Project Introduction

Rust Trade is a comprehensive cryptocurrency trading system that combines high-performance market data processing capabilities with sophisticated backtesting tools, providing a one-stop solution for cryptocurrency quantitative trading. The system has the following core features:

- Real-time data collection: Obtains real-time market data from exchanges

- Advanced backtesting engine: Supports backtesting analysis for various trading strategies

- Professional desktop interface: Intuitive and user-friendly graphical interface

- Cross-platform support: Can run on Windows, macOS, and Linux

Project Structure

Rust Trade adopts a clear modular architecture design, dividing the entire project into the following core modules:

Core Module Introduction

1. trading-core (Core Trading System)

This is the core of the entire system, written in Rust, responsible for data processing, strategy execution, and trade management.

trading-core/

├── src/

│ ├── backtest/ # Backtesting engine and strategies

│ │ ├── engine.rs # Core backtesting logic

│ │ ├── metrics.rs # Performance metrics calculation

│ │ ├── portfolio.rs # Portfolio management

│ │ └── strategy/ # Trading strategy implementation

│ │ ├── sma.rs # Simple Moving Average strategy

│ │ └── rsi.rs # Relative Strength Index strategy

│ ├── data/ # Data access layer

│ │ ├── cache.rs # Multi-level cache implementation

│ │ ├── repository.rs # Database operations

│ │ └── types.rs # Core data structures

│ ├── exchange/ # Exchange integration

│ │ └── binance.rs # Binance exchange interface

│ ├── live_trading/ # Real-time trading system

│ │ └── paper_trading.rs # Paper trading implementation

│ ├── service/ # Business logic services

│ │ └── market_data.rs # Market data processing service

│ ├── config.rs # Configuration management

│ ├── lib.rs # Library entry

│ └── main.rs # CLI application entry

├── Cargo.toml # Rust dependency configuration

└── README.md # Module documentation

2. src-tauri (Desktop Application Backend)

Backend of the desktop application built on the Tauri framework, responsible for handling communication between the frontend interface and the trading core.

src-tauri/

├── src/

│ ├── commands.rs # Tauri command implementation

│ ├── main.rs # Application entry point

│ ├── state.rs # Application state management

│ └── types.rs # Frontend interface types

├── Cargo.toml # Tauri dependency configuration

└── tauri.conf.json # Tauri configuration file

3. frontend (Frontend Interface)

Modern frontend interface built with Next.js, providing an intuitive user experience.

frontend/

├── src/

│ ├── app/ # Application routing pages

│ │ ├── backtest/ # Backtesting interface

│ │ ├── trading/ # Real-time trading interface

│ │ ├── settings/ # Settings interface

│ │ └── page.tsx # Home page

│ ├── components/ # UI components

│ │ ├── layout/ # Layout components

│ │ └── ui/ # Basic UI components

│ ├── lib/ # Utility functions

│ └── types/ # TypeScript type definitions

├── package.json # Frontend dependency configuration

└── next.config.ts # Next.js configuration

Configuration and Documentation

.

├── config/ # Global configuration files

│ ├── development.toml # Development environment configuration

│ ├── schema.sql # Database table structure

│ └── live_strategy_log.sql # Strategy log table structure

├── README.md # Project main documentation

└── Cargo.toml # Workspace configuration

Source Code Architecture

Core Source Code Analysis

1. Data Model Design

In the types.rs file, the core data structure TickData is defined, which corresponds exactly to the tick_data table structure in the database. This design ensures data consistency and integrity.

/// Standard trading data structure - corresponds to tick_data table fields

#[derive(Debug, Clone, Serialize, Deserialize, PartialEq)]

pub struct TickData {

/// UTC timestamp, supports millisecond precision

pub timestamp: DateTime,

/// Trading pair, e.g., "BTCUSDT"

pub symbol: String,

/// Trading price

pub price: Decimal,

/// Trading quantity

pub quantity: Decimal,

/// Trading direction

pub side: TradeSide,

/// Original trade ID

pub trade_id: String,

/// Whether the buyer is the maker

pub is_buyer_maker: bool,

}

2. Exchange Interface Implementation

In the binance.rs file, the WebSocket connection and REST API calls for the Binance exchange are implemented. Through an asynchronous programming model, the system can efficiently handle real-time data streams.

/// Binance exchange implementation

pub struct BinanceExchange {

ws_url: String,

api_url: String,

client: reqwest::Client,

}

This implementation supports an automatic reconnection mechanism, ensuring continuous data retrieval even in unstable network conditions.

3. Data Storage and Caching

In repository.rs, persistent data storage and multi-level caching mechanisms are implemented. The system uses PostgreSQL as the primary storage and Redis as the secondary cache, with memory as the primary cache, forming an efficient three-tier caching architecture.

/// TickData data repository, responsible for database operations

pub struct TickDataRepository {

pool: PgPool,

cache: TieredCache,

}

4. Backtesting Engine Core

In engine.rs, a complete backtesting engine is implemented. This engine supports various trading strategies and provides detailed performance metrics calculations.

pub struct BacktestEngine {

portfolio: Portfolio,

strategy: Box,

config: BacktestConfig,

}

5. Portfolio Management

In portfolio.rs, portfolio management functions are implemented, including position management and profit-loss calculations.

pub struct Portfolio {

pub initial_capital: Decimal,

pub cash: Decimal,

pub positions: HashMap,

pub trades: Vec,

// ...

}

6. Strategy Interface and Implementation

The strategy module adopts an object-oriented design philosophy, defining a unified strategy interface to facilitate the extension of new trading strategies.

pub trait Strategy {

fn name(&self) -> &str

fn initialize(&mut self, params: HashMap) -> Result<(), String>;

fn reset(&mut self);

fn on_tick(&mut self, tick: &TickData) -> Signal;

}

7. Performance Metrics Calculation

In metrics.rs, rich performance metrics calculation functions are implemented, including Sharpe ratio, maximum drawdown, win rate, etc.

pub struct BacktestMetrics;

impl BacktestMetrics {

/// Calculate Sharpe ratio

pub fn calculate_sharpe_ratio(returns: &[Decimal], risk_free_rate: Decimal) -> Decimal {

// ...

}

/// Calculate maximum drawdown

pub fn calculate_max_drawdown(equity_curve: &[Decimal]) -> Decimal {

// ...

}

}

Strategy Engine

Rust Trade comes with two classic trading strategies built-in, providing users with an out-of-the-box quantitative trading experience.

Simple Moving Average Strategy (SMA)

This strategy is based on the dual moving average crossover principle, generating a buy signal when the short-term moving average crosses above the long-term moving average, and a sell signal when the short-term moving average crosses below the long-term moving average. The strategy parameters are configurable, allowing users to adjust the lengths of the short and long periods to adapt to different market conditions.

The strategy implementation in sma.rs is as follows:

fn on_tick(&mut self, tick: &TickData) -> Signal {

self.prices.push_back(tick.price);

// Maintain reasonable data length

if self.prices.len() > self.long_period * 2 {

self.prices.pop_front();

}

if let (Some(short_sma), Some(long_sma)) =

(self.calculate_sma(self.short_period), self.calculate_sma(self.long_period)) {

// Golden cross: short-term SMA crosses above long-term SMA

if short_sma > long_sma &&

!matches!(self.last_signal, Some(Signal::Buy { .. })) {

let signal = Signal::Buy {

symbol: tick.symbol.clone(),

quantity: Decimal::from(100),

};

self.last_signal = Some(signal.clone());

return signal;

}

// Death cross: short-term SMA crosses below long-term SMA

else if short_sma < long_sma &&

matches!(self.last_signal, Some(Signal::Buy { .. })) {

let signal = Signal::Sell {

symbol: tick.symbol.clone(),

quantity: Decimal::from(100),

};

self.last_signal = Some(signal.clone());

return signal;

}

}

Signal::Hold

}

Relative Strength Index Strategy (RSI)

The RSI strategy is based on the Relative Strength Index indicator, generating a buy signal when the RSI indicator is below the oversold level, and a sell signal when the RSI indicator is above the overbought level. This strategy captures reversal opportunities by identifying the market’s overbought and oversold states.

The strategy implementation in rsi.rs is as follows:

fn on_tick(&mut self, tick: &TickData) -> Signal {

// Calculate price changes

if let Some(last_price) = self.prices.back() {

let change = tick.price - last_price;

if change > Decimal::ZERO {

self.gains.push_back(change);

self.losses.push_back(Decimal::ZERO);

} else {

self.gains.push_back(Decimal::ZERO);

self.losses.push_back(-change);

}

// Maintain fixed length

if self.gains.len() > self.period {

self.gains.pop_front();

self.losses.pop_front();

}

}

self.prices.push_back(tick.price);

if self.prices.len() > self.period + 1 {

self.prices.pop_front();

}

if let Some(rsi) = self.calculate_rsi() {

// Buy signal when oversold

if rsi < self.oversold &&

!matches!(self.last_signal, Some(Signal::Buy { .. })) {

let signal = Signal::Buy {

symbol: tick.symbol.clone(),

quantity: Decimal::from(100),

};

self.last_signal = Some(signal.clone());

return signal;

}

// Sell signal when overbought

else if rsi > self.overbought &&

matches!(self.last_signal, Some(Signal::Buy { .. })) {

let signal = Signal::Sell {

symbol: tick.symbol.clone(),

quantity: Decimal::from(100),

};

self.last_signal = Some(signal.clone());

return signal;

}

}

Signal::Hold

}

Quick Start

Environment Preparation and Installation

1. Install Necessary Tools

# Install Rust (ensure version >= 1.70)

curl --proto '=https' --tlsv1.2 -sSf https://sh.rustup.rs | sh

source $HOME/.cargo/env

# Verify installation

rustc --version

cargo --version

# Install Node.js (version >= 18)

# Windows users can download the installer from https://nodejs.org/

# macOS users can use brew install node

# Linux users can install via package manager

# Install PostgreSQL (version >= 12)

# Windows: Download from https://www.postgresql.org/download/windows/

# macOS: brew install postgresql

# Ubuntu: sudo apt install postgresql postgresql-contrib

# Install Redis (optional, version >= 6)

# Windows: https://github.com/microsoftarchive/redis/releases

# macOS: brew install redis

# Ubuntu: sudo apt install redis-server

2. Clone the Project and Configure the Database

# Clone the project code

git clone

cd rust-trade-master

# Create the database

# Windows users execute in PowerShell:

# psql -U postgres -c "CREATE DATABASE trading_core;"

# macOS/Linux users execute:

createdb trading_core

# Import the database table structure

# Windows users:

# psql -U postgres -d trading_core -f config/schema.sql

# macOS/Linux users:

psql -d trading_core -f config/schema.sql

3. Configure Environment Variables

Create a <span>.env</span> file in the project root directory:

# .env file content

DATABASE_URL=postgresql://localhost/trading_core

REDIS_URL=redis://127.0.0.1:6379

RUN_MODE=development

RUST_LOG=info

Compile and Run the Project

1. Compile the Core Module

# Enter the core module directory

cd trading-core

# Compile the project

cargo build

# For production environment, use optimized compilation

cargo build --release

2. Install Frontend Dependencies

# Return to the project root directory

cd ..

# Enter the frontend directory

cd frontend

# Install frontend dependencies

npm install

3. Run in Different Modes

Run in CLI Mode

# Return to the trading-core directory

cd ../trading-core

# View help information

cargo run -- --help

# Start real-time data collection

cargo run live

# Start real-time data collection with paper trading enabled

cargo run live --paper-trading

# Start backtesting mode

cargo run backtest

# Sync historical data (example)

cargo run sync --symbol BTCUSDT --days 30

Desktop Application Mode

# Enter the frontend directory

cd ../frontend

# Run in development mode (with hot reload)

npm run tauri dev

# Build production version

npm run tauri build

Pure Web Interface Mode

# In the frontend directory

# Start the development server

npm run dev

# Build production version

npm run build

# Start the production server

npm start

Configure Trading Pairs and Parameters

Configure trading pairs in the <span>config/development.toml</span> file:

# Trading pairs to monitor

symbols = ["BTCUSDT", "ETHUSDT", "ADAUSDT"]

[server]

host = "0.0.0.0"

port = 8080

[database]

max_connections = 5

min_connections = 1

max_lifetime = 1800

[cache]

[cache.memory]

max_ticks_per_symbol = 1000

ttl_seconds = 300

[cache.redis]

pool_size = 10

ttl_seconds = 3600

max_ticks_per_symbol = 10000

Backtesting Execution Example

Command Line Backtesting

# Enter the trading-core directory

cd trading-core

# Start the backtesting interactive interface

cargo run backtest

# Backtesting interface operation example:

# 1. Select strategy (SMA or RSI)

# 2. Select trading pair (e.g., BTCUSDT)

# 3. Set initial capital (e.g., 50000)

# 4. Set commission rate (e.g., 0.1%)

# 5. Start backtesting

Programmatic Backtesting Execution

// Execute backtesting in Rust code

use trading_core::backtest::{BacktestEngine, BacktestConfig};

use trading_core::backtest::strategy::{SmaStrategy};

// Create strategy instance

let strategy = Box::new(SmaStrategy::new());

// Configure backtesting parameters

let config = BacktestConfig::new(Decimal::from(10000)) // Initial capital 10000

.with_commission_rate(Decimal::from_str("0.001").unwrap()); // 0.1% commission

// Create backtesting engine

let mut engine = BacktestEngine::new(strategy, config)?;

// Load historical data (from database or other sources)

let historical_data = load_historical_data("BTCUSDT")?;

// Execute backtesting

let result = engine.run(historical_data);

// Output results

result.print_summary();

Real-time Trading Execution Example

Start Real-time Data Collection

# In the trading-core directory

cargo run live

Start Real-time Mode with Paper Trading

# In the trading-core directory

cargo run live --paper-trading

Programmatically Start Real-time Trading

// Start real-time trading in Rust code

use trading_core::service::MarketDataService;

use trading_core::exchange::BinanceExchange;

// Create exchange instance

let exchange = Arc::new(BinanceExchange::new());

// Create data repository

let repository = Arc::new(TickDataRepository::new(pool, cache));

// Configure trading pairs to monitor

let symbols = vec!["BTCUSDT".to_string(), "ETHUSDT".to_string()];

// Create market data service

let service = MarketDataService::new(exchange, repository, symbols);

// Start service

service.start().await?;

Practical Case Study

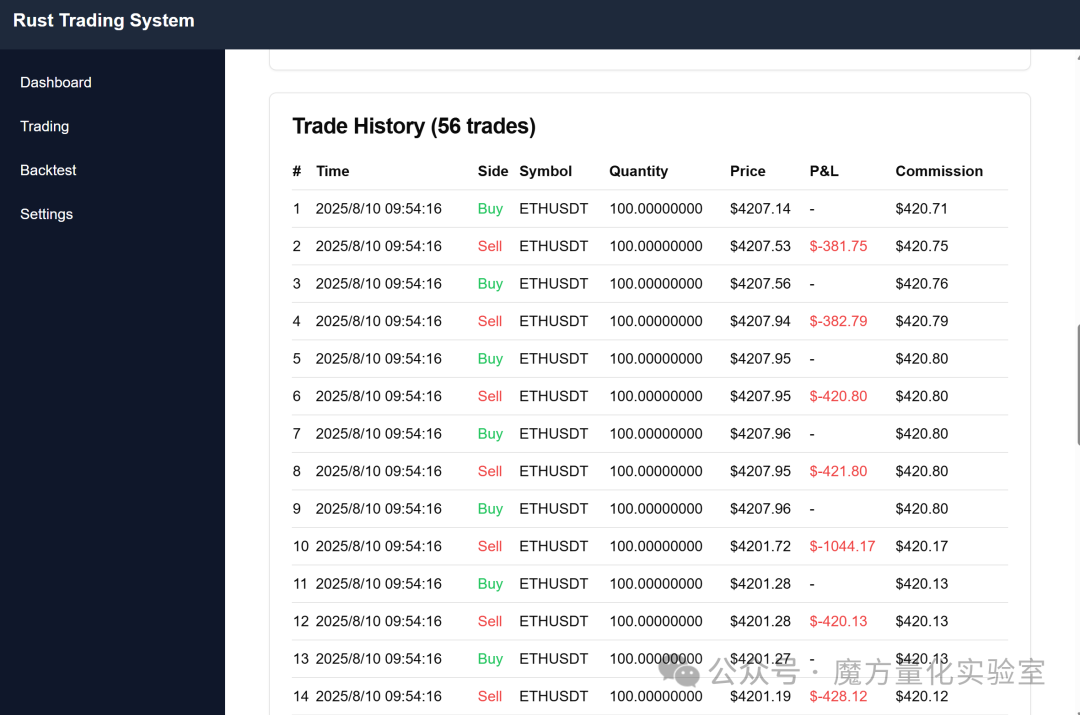

BTCUSDT Trading Backtest

Let us demonstrate the powerful features of Rust Trade through a practical backtesting case. We will use the Bitcoin to US Dollar (BTCUSDT) trading pair for backtesting analysis with the Simple Moving Average strategy.

During the backtesting process, the system will load historical data and execute trades according to the strategy rules. After the backtest is complete, the system will generate a detailed analysis report, including:

- Initial capital and final asset value

- Total profit and loss and return rate

- Trade count statistics

- Win rate and profit-loss ratio

- Maximum drawdown and Sharpe ratio and other risk indicators

Through these indicators, users can comprehensively evaluate the performance of the strategy and optimize parameters based on the results.

Performance Advantages

Rust Trade demonstrates excellent performance, thanks to the high-performance characteristics of the Rust language and the carefully designed architecture:

- Single data insertion takes about 390 microseconds

- Batch insertion of 100 data takes about 13 milliseconds

- Cache hit response time is about 10 microseconds

- Historical data query takes about 450 microseconds

This outstanding performance enables Rust Trade to meet the demands of high-frequency trading scenarios.

Configuration Flexibility

Rust Trade offers a rich set of configuration options, allowing users to customize according to their needs:

- Supports multiple trading pair configurations

- Configurable database connection parameters

- Flexible log level settings

- Multi-environment configuration support (development, production, testing)

Conclusion

As an open-source cryptocurrency trading system, Rust Trade provides powerful tools for quantitative trading enthusiasts, enabling them to enhance trading efficiency and optimize investment decisions through this system.

Project Address

https://github.com/Erio-Harrison/rust-trade

Follow 【Magic Cube Quant】 to master open-source quantitative trading!