In the context of the booming digital economy, embedded software serves as a key force driving industrial upgrades, and its importance is self-evident. To encourage enterprises to innovate and develop, the government has introduced the immediate tax refund policy for embedded software value-added tax (VAT), helping companies reduce their tax burden and unleash more development vitality. However, despite the favorable policy, enterprises need to accurately grasp the key points of the policy and operate in compliance to fully enjoy its benefits.

1. Scope of Policy Application

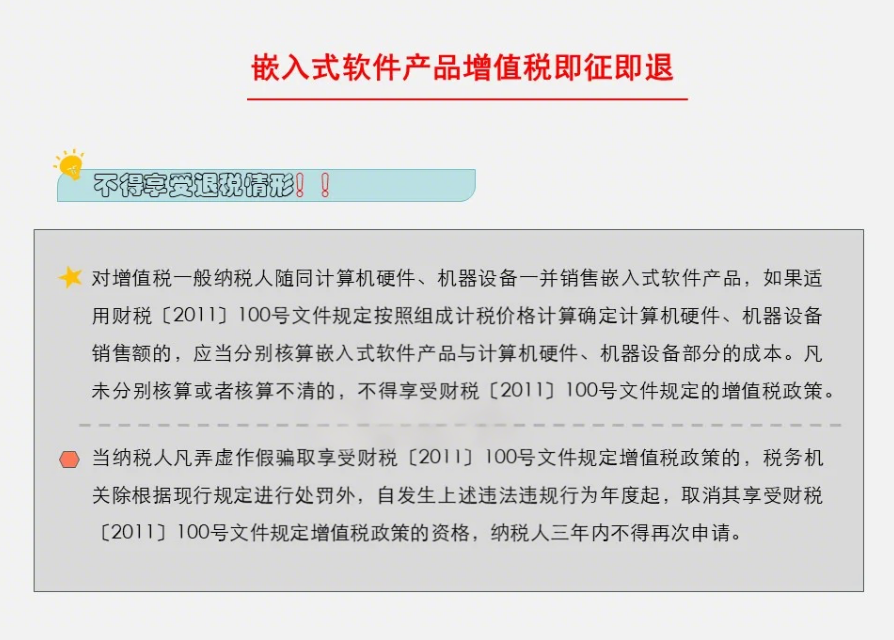

According to the “Notice on VAT Policy for Software Products” (Cai Shui [2011] No. 100) issued by the Ministry of Finance and the State Administration of Taxation, general VAT taxpayers selling self-developed embedded software products are subject to a VAT rate of 13%. They can apply for an immediate tax refund for the portion of the actual tax burden that exceeds 3%. Here, embedded software products refer to software products embedded in computer hardware and machinery that are sold together with them, constituting a part of the computer hardware or machinery. It is important to note that imported software that has undergone localization modifications (requiring redesign and improvement, excluding mere Chinese character localization) is also eligible for this policy. However, software developed under commission, if the copyright belongs to the commissioning party or is jointly owned, will not be subject to VAT (but the transfer of copyright will be taxed as a taxable service and will not enjoy a tax refund).

2. Conditions for Enjoying the Policy

1.Qualification Proof: Enterprises must obtain testing certification from a software testing institution recognized by the provincial software industry authority to prove compliance with software quality and standards. They must also possess a “Software Product Registration Certificate” issued by the software industry authority or a “Computer Software Copyright Registration Certificate” issued by the copyright administrative department.

2.Independent Accounting: Enterprises must separately account for the costs of embedded software products and the computer hardware and machinery components. If they do not account separately or if the accounting is unclear, they will not be able to enjoy this policy. Additionally, the accounting of sales revenue and input tax for software products must also be accurate.

3. Calculation of Immediate Tax Refund Amount

The formula for calculating the immediate tax refund amount is: Immediate Tax Refund Amount = Current Period VAT Payable for Embedded Software Products – Current Period Sales Revenue of Embedded Software Products × 3%. Where the current period VAT payable for embedded software products = Current Period Output Tax for Embedded Software Products – Current Period Deductible Input Tax for Embedded Software Products, and the current period output tax for embedded software products = Current Period Sales Revenue of Embedded Software Products × 13%. The current period sales revenue of embedded software products = Total Sales Revenue of Embedded Software Products and Computer Hardware and Machinery – Current Period Sales Revenue of Computer Hardware and Machinery. The sales revenue of computer hardware and machinery is calculated based on the average selling price of similar goods sold by the taxpayer in the most recent period; if there is no similar price, it is calculated based on the average selling price of similar goods sold by other taxpayers in the most recent period; if it is still indeterminate, it is calculated based on the cost of computer hardware and machinery × (1 + 10%).

4. Declaration Process and Precautions

1.Preparation of Materials: Enterprises need to prepare software product testing reports, software product registration certificates or computer software copyright registration certificates, sales contracts, invoices, and other relevant materials to ensure that the materials are complete and authentic, as this is an important basis for tax authorities’ review.

2.Tax Declaration: When declaring VAT, enterprises must accurately fill out the declaration form, truthfully enter information such as the sales revenue of embedded software products, and submit the immediate tax refund application as required.

3.Tax Authority Review and Tax Refund: The tax authority will review the materials and declaration content submitted by the enterprise, checking aspects such as the nature of the software products and the calculation of sales revenue. After passing the review, the tax refund will be issued according to regulations. Enterprises should note that the invoicing name must match the copyright certificate, retain pricing basis for hardware, submit complete materials for the first tax refund, and proactively report to the tax authority if there are changes in conditions such as software upgrades.

The immediate tax refund policy for embedded software brings tangible opportunities for burden reduction to enterprises. Companies should thoroughly study the policy, accurately calculate, and standardize declarations to fully enjoy the policy benefits, injecting strong momentum into their development.