According to the latest analysis from Omdia’s Automotive Display Intelligence Service, the global automotive display market is expected to experience strong growth, with display panel sales projected to reach $13.6 billion (approximately 97.648 billion yuan) by 2025, representing an 8% year-on-year increase. Omdia further predicts that by 2030, the market size will grow to $18.3 billion (approximately 131.394 billion yuan).

Omdia emphasizes that this revenue growth is not driven by unit sales but rather by the widespread adoption of advanced and high-value display panel technologies, particularly OLED (Organic Light Emitting Diode) and LTPS (Low-Temperature Polycrystalline Silicon) TFT LCD panels.

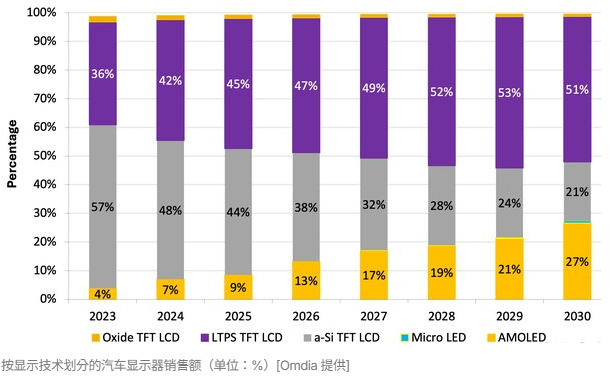

The report states that in terms of panel shipment revenue, LTPS TFT LCD is expected to account for 45% of the total automotive display market revenue of $13.6 billion by 2025, while OLED will account for 9%.

On the other hand, the revenue share of amorphous silicon (a-Si) TFT LCD panels is expected to decline from 48% to 44%.

Omdia states, “2025 will be the first year that the combined sales of LTPS TFT LCD and OLED exceed 50% of total sales,” adding that, “this marks a transition in the automotive display market towards high-value display technologies.”

Compared to traditional a-Si TFT LCD automotive display panels, LTPS TFT LCD offers numerous advantages, including higher resolution, greater brightness, lower power consumption, and better touchscreen integration. These advantages are particularly important for the rapidly growing electric vehicle industry, where performance and efficiency are critical.

LTPS TFT LCD is increasingly used in applications such as center console displays and instrument panels, and it dominates the heads-up display (HUD) field due to its brightness advantages.

Meanwhile, OLED is gradually replacing LCD due to its slim profile, high contrast, efficient power consumption, and support for free-form designs. The application of OLED in areas such as center consoles, instrument panels, and passenger displays is continuously expanding.

The average selling price (ASP) of both LTPS TFT LCD and OLED is higher than that of traditional a-Si TFT LCD, reinforcing the market’s shift towards higher value technologies.

Omdia predicts that “LTPS TFT LCD will become the mainstream display technology in the automotive display market,” and that “by 2028, its shipment revenue share will exceed 50%.”

At the same time, OLED is expected to dominate the luxury automotive cockpit sector, with a shipment revenue share exceeding 20% by 2028. Additionally, by 2030, the market share of a-Si TFT LCD is expected to decline significantly to 21% of total shipment revenue.

Omdia also emphasizes that deformable micro-LED displays will enter the automotive display market after 2028, forming the next wave of advanced display technologies.

David Hsieh, Senior Director of Displays at Omdia, stated: “While LTPS TFT LCD is exiting the smartphone display market, panel manufacturers such as AUO, BOE, TCL China Star, Japan Display, Innolux, Sharp, Tianma, and LG Display are actively entering the automotive sector in pursuit of higher value and profitability.”

He continued, “In contrast, as OLED continues to dominate the smartphone market, major OLED manufacturers such as Samsung Display, LG Display, and BOE are developing new tandem RGB OLED designs to accelerate their layout in the automotive field. The innovation of display manufacturers and intense OEM competition will be key driving forces for LTPS and OLED to dominate the future automotive display market.”

[Business Cooperation]Ms. Kang: 19168597393Email: [email protected]Mr. Chen: 13826958679Email: [email protected]

[Conference Consultation]

Ms. Zhang: 15112366757

Email: [email protected]

Long press the QR code to add Xiao Wei,reply with the keyword “Display” to enter the industry exchange group

Long press the QR code to add Xiao Wei,reply with the keyword “Display” to enter the industry exchange group