Welcome to cite:

Wang Kunlun. Current Status, Competitiveness and Future Development Strategies of China’s Industrial Robot Industry[J]. Robot Technology and Application, 2024, No.219(03):8-13

Abstract

To clarify the development direction of China’s industrial robot industry and find the key to industrial leapfrogging, it is necessary to identify the shortcomings and unresolved issues from the current state of industrial development, explore the potential advantages of the industry, and promote their maximization. This article comprehensively analyzes the industrial robot industry from three aspects: the current development status of China’s industrial robot industry, international competitiveness, and future development strategies. Firstly, it discusses the current development status of China’s industrial robot industry from aspects such as market scale, industrial chain structure, application scale, and fields/scenarios; next, it analyzes the international competitiveness of China’s industrial robots from the perspectives of technical bottlenecks and breakthroughs, brand influence, etc.; finally, it proposes future development strategies for China’s industrial robot industry. On one hand, China’s vast application scenarios play a role in supporting the industrial robot industry; on the other hand, from the perspective of the long-term development of China’s industrial robots, key technology research and development must remain a top priority for the future, while also integrating and strengthening the upstream and downstream industrial chains, enhancing synergy with new technologies such as 5G, artificial intelligence, and virtual reality, ultimately achieving industrial leapfrogging and transformation.

Keywords: industrial robots, key components, industrial chain, application scenarios, market share, brand influence

0 Introduction

The development of the global robot industry can be traced back to the late 1940s, when the Oak Ridge National Laboratory and the Argonne National Laboratory in the United States began developing remote-controlled mechanical hands for the handling of radioactive materials, marking over seventy years of evolution. Currently, robots are widely used in various fields of production and life, and with the continuous iteration of technological innovation, the development of the robot industry shows a vibrant trend.

In 2021, the Ministry of Industry and Information Technology and others issued the “14th Five-Year Plan for Robot Industry Development”, which accelerated the development of China’s robot industry. In terms of application classification, the fields of industrial robots and service robots are particularly prosperous.

As the largest market for industrial robots in the world, the development of China’s industrial robot industry is worth exploring in depth.

1 Current Status of China’s Industrial Robot Industry

1.1 Development Background

The term “robot” was first coined in 1921 by Karel Čapek. The development of industrial robots can be divided into three stages: from 1950 to 1960, the global industrial robot industry was in its infancy; from 1960 to 2000, it was defined as the stage of industrial rise, during which industrial robots began to industrialize and globalize; from 2000 to the present, the industrial robot industry is in the stage of industrial upgrading and intelligence. During this period, the vigorous development of technologies such as 5G, big data, and artificial intelligence has greatly promoted the process of industrial intelligence.

Lagging behind abroad, the development of China’s industrial robot industry began in the 1970s, roughly going through three development stages: the first stage was the technology exploration period (1970-1990); the second stage was the industry incubation period (1990-2009); the third stage is the industry development period (2009-present). After about 30 years of technological incubation, China’s industrial robot field has extended from technology exploration to industrial landing, ushering in a market explosion period.

1.2 Market Scale

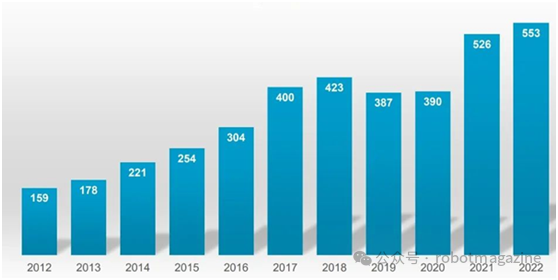

In October 2023, the International Federation of Robotics (IFR) released the “2023 World Robotics Report”. The report disclosed that in 2022, the number of newly installed industrial robots in global factories reached 553,052 units, a year-on-year increase of 5% (Figure 1). Among them, Asia accounted for 73%, Europe for 15%, and the Americas for 10%.

Figure 1 Global Installation of Industrial Robots

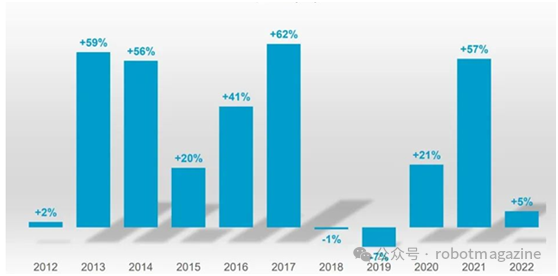

The report shows that in 2022, the number of industrial robots installed in China reached 290,258 units, a year-on-year increase of 5% (Figure 2), breaking the record set in 2021, once again claiming the title of the largest market for industrial robots in the world. Since 2017, the annual average growth rate of industrial robot installations in China has been 13%.

Figure 2 Year-on-Year Growth Rate of Industrial Robot Installations in China

According to the report, in 2022, Japan ranked second in terms of industrial robot installations, but the gap between its installations and China’s remains significant. In 2022, the number of industrial robots installed in Japan increased by 9% to 50,413 units. Since 2017, its average annual growth rate of robot installations has been 2%. It is evident that under the enormous demand of China’s industrial robot market, the development prospects are extremely broad.

1.3 Industrial Chain Structure

The industrial robot industry chain is divided into upstream, midstream, and downstream. The upstream consists of key components of robots, including controllers, servo drives, reducers, sensors, and end effectors; the midstream consists of the robot body; the downstream consists of robot integration development and applications.

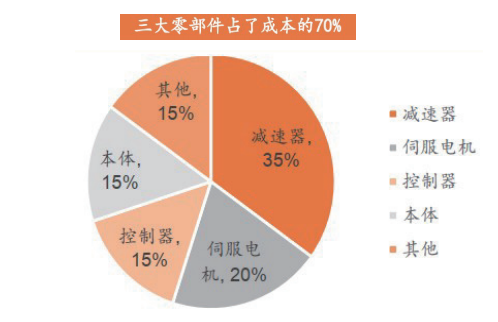

According to the “2023-2028 China Industrial Robot Industry Deep Investigation and Investment Strategy Research Report” by the China Business Industry Research Institute, the five key components of robots account for the vast majority of industrial robot costs, among which the reducer, servo drive, and controller account for approximately 35%, 20%, and 15%, respectively (Figure 3), with the reducer having the highest cost share, followed by the servo drive, and the controller in third place.

Figure 3 Cost Proportion of Key Components of Industrial Robots

In the early stages of development, China’s industrial robot industry was mostly concentrated in the mid and downstream of the industrial chain, namely body manufacturing, system integration, and secondary development, with upstream key components primarily relying on imports. Today, with strong national support and industrial promotion, some relevant enterprises in the upstream component industry of China have begun to emerge.

However, there is still considerable room for improvement in market share. In 2022, in China’s industrial robot market, ABB, Fanuc, KUKA, and Yaskawa (the four major families of global industrial robots) accounted for about 40% of the market share. In the same year, the domestic production rate of industrial robots was about 40%.

1.4 Application Scale and Scenarios

1.4.1 Application Scale

From the perspective of application classification, robots are generally divided into industrial robots and service robots internationally. In China, robots are classified into industrial robots, service robots, and special robots.

According to the “China Robot Industry Development Report (2022)” released by the China Electronics Society, in 2021, the global industrial robot market size was $17.5 billion, accounting for 41% of the global robot industry; it is expected that from 2022 to 2024, the compound annual growth rate (CAGR) of the global industrial robot market size will be 9%. In 2021, China’s industrial robot market size was $7.5 billion, accounting for 53% of China’s robot industry; it is expected that from 2022 to 2024, the CAGR of China’s industrial robot market size will be 15%. Thus, it can be seen that the market size of China’s industrial robots CAGR is far higher than the global average. Statistics from the Ministry of Industry and Information Technology show that currently, the application of industrial robots covers 60 major categories of the national economy and 168 subcategories, making China the world’s largest industrial robot application country for ten consecutive years.

In the future, the development of China’s industrial robots will continue to improve. The China Business Industry Research Institute predicts in the “2023-2028 China Industrial Robot Industry Deep Investigation and Investment Strategy Research Report” that by 2024, the market size of China’s industrial robot industry will exceed 70 billion yuan.

1.4.2 Application Scenarios

Currently, under the dual influence of market demand and policy guidance, the application of industrial robots has shown a blooming phenomenon. The manufacturing industry is the most concentrated application scenario, with industrial robots being ubiquitous in fields such as automotive, electronics, food processing, photovoltaics, metal processing, chemical products, mining, and textiles. Industrial robots have become indispensable highly automated equipment in modern production.

In January 2023, the Ministry of Industry and Information Technology and seventeen other departments issued the “Implementation Plan for the Application of ‘Robot +'” (hereinafter referred to as the “Plan”). Among the main goals proposed in the Plan, the development goal for industrial robots is to double the density of manufacturing robots by 2025 compared to 2020, significantly enhancing the ability of robots to promote high-quality economic and social development.

The Plan emphasizes focusing on ten major application areas, including manufacturing, agriculture, construction, energy, commercial logistics, as well as medical health, elderly care services, education, commercial community services, safety emergencies, and extreme environment applications. Among these fields, industrial robots are the most widely used and largest type of robots.

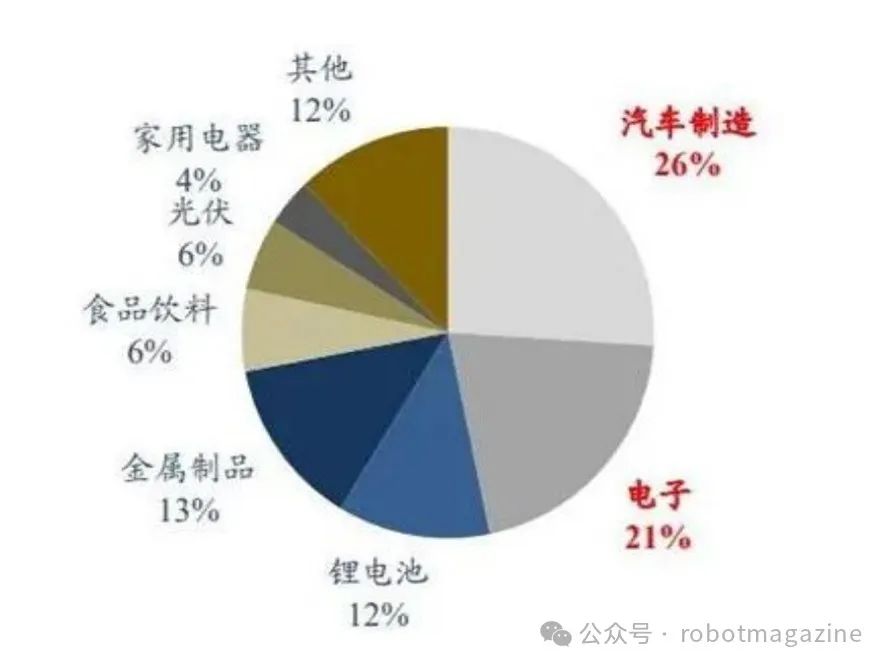

According to a deep report on the automation equipment industry released by Dongwu Securities, in 2022, the sales of industrial robots in the automotive and electronics industries accounted for 47% (Figure 4), making them the largest downstream sector for industrial robots.

Figure 4 Proportion of Automotive and Electronics Manufacturing in China’s Industrial Robot Sales in 2022

In the automotive manufacturing sector, industrial robots are mainly used in processes such as welding, stamping, painting, and assembly. Due to their high efficiency, precision, flexibility, and safety, they greatly enhance the production efficiency and product quality of the automotive industry. In addition to the production of high-quality automotive components, the role of industrial robots in intelligent manufacturing in the automotive industry is becoming increasingly significant, promoting the transformation and upgrading of the entire automotive industry.

In the electronics production sector, industrial robots are mainly applied in sorting boxes, film tearing systems, laser plastic welding, and high-speed palletizing. In the electronics sub-market, applications such as electronic ICs and surface mount components are quite widespread. They not only improve the speed and precision of electronic assembly but also significantly reduce production and labor costs.

The “China Robot Technology and Industry Development Report (2023)” released at the 2023 World Robot Conference shows that China has a vast robot application market. With the steady implementation of the “Robot +” initiative, the fields of robot applications are accelerating to expand, with continuous deepening applications in sectors such as new energy vehicles, medical surgery, power inspections, and photovoltaics, strongly supporting the digital transformation and intelligent upgrading of the industry.

2 International Competitiveness of China’s Industrial Robots

2.1 Technical Bottlenecks and Breakthroughs

Due to the development of China’s industrial robot industry extending from the mid and downstream, the accumulation of technology in the upstream of the industrial chain is insufficient. After years of catching up, there has been certain progress in market share and technological level, but there is still considerable room for improvement.

The “Blue Book of Industries: Report on China’s Industrial Competitiveness (2022-2023)” released by the Center for Industry and Enterprise Competitiveness of the Chinese Academy of Social Sciences indicates that as China’s robot (mainly industrial robots) industry grows stronger, the resilience of the robot industry chain and supply chain gradually increases, but overall it is still inadequate, characterized by low technical levels and numerous risk points.

Currently, the countries with high levels of research and development in industrial robots are the United States, Japan, and Germany. These countries have conducted long-term exploration and accumulation in the research, development, and manufacturing of industrial robots. The United States leads in AI technology for industrial robots and humanoid robots, while Japan excels in the upstream key components of industrial robots such as reducers, having established a strong technological moat; Germany has strong capabilities in raw materials and body components.

Compared to these countries, China’s shortcomings mainly lie in the upstream key components of the industrial robot industry chain. This segment is the most technically demanding part of the entire industrial robot industry and represents the largest gap between China and the world’s leading levels. Taking reducers as an example, industrial robot reducers mainly include RV reducers and harmonic reducers (Figure 5). Currently, the domestically produced harmonic reducers have made considerable progress, while RV reducers have also made significant advancements in large load capacity and wide-range transmission, with some products reaching internationally advanced levels.

Figure 5 RV Reducers (Top) and Harmonic Reducers (Bottom)

The blue book points out that the performance of domestic key components has a significant gap compared to international first-class levels, with high-end key components relying on imports, posing a “bottleneck” risk.

However, in recent years, with strong national policy support, active enterprise investment in research and development, and downstream demand driving the industry forward, the development of China’s industrial robot industry has been rapid, with the process of autonomy accelerating, and the pace of domestic substitution steadily advancing, thus rapidly reducing the “bottleneck” risk.

According to Dongwu Securities’ “Deep Report on the Automation Equipment Industry – Deep Report on the Robot Industry”, from 2015 to 2022, the domestic production rate of robots increased from 17.5% to 35.7%, and in 2022, the domestic production rate of industrial robots increased by 4 percentage points year-on-year, reaching 41% in the first quarter of 2023, a year-on-year increase of 9 percentage points.

2.2 Brand Influence

In recent years, China’s industrial robot industry has been catching up and has produced some well-known enterprises in the industry. For example, in the reducer field, leading component companies such as Huandong Technology, Zhizhong Precision, and Green Harmonic have emerged, and in the category of large six-axis robots, leading companies such as Estun, Asteon, Aeffort, and New Times have also come to the forefront.

From the perspective of different body forms, industrial robots are mainly divided into six-axis robots, Selective Compliance Assembly Robot Arms (SCARA), Delta robots, collaborative robots, and several other types. Among them, six-axis robots have the highest technical barriers and the largest shipment volume, further divided into large six-axis robots and small six-axis robots based on load capacity.

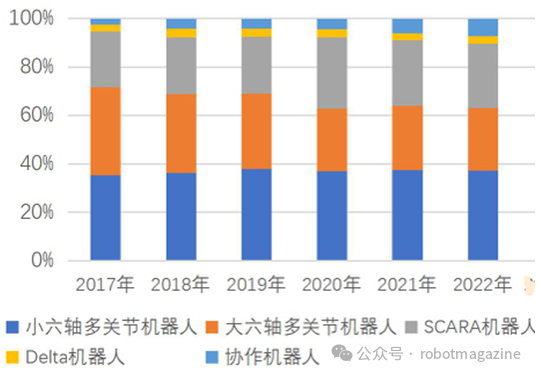

From 2017 to 2022, the sales volume of six-axis multi-joint robots and SCARA robots accounted for over 90% of the total sales volume of China’s industrial robot market, with around 90% in 2022, where small six-axis, large six-axis, and SCARA robots accounted for 37%, 26%, and 27%, respectively.

Figure 6 Sales Proportion of Small Six-Axis, Large Six-Axis, and SCARA Robots from 2017 to 2022

Therefore, the domestic production rate of six-axis robots is a direct reflection of China’s industrial robot technology and brand strength. Data shows that in 2022, the domestic production rate of large six-axis robots was 17%, with Estun, as the leading enterprise in this field, accounting for 8% of the market share.

Currently, China has a number of high-quality reducer companies, but it should be noted that in the reducer market, Japan’s Nabtesco and Harmonic still occupy a large portion of the market share. Additionally, the “four major families” of industrial robots have basically integrated the industrial chain, controlling about 40% of the Chinese industrial robot market, indicating that the development of China’s industrial robot enterprises still has a long way to go.

3 Future Development Strategies of China’s Industrial Robot Industry

3.1 Strengthening and Supplementing the Chain to Improve the Technical Level of Key Components

Currently, foreign giants are shifting their focus towards software, and Chinese industrial robot companies need to seize this window of opportunity to further strengthen autonomous control technology, enhance brand influence and added value, and continue to expand into the midstream and upstream of the industrial chain.

The goals mentioned in the “14th Five-Year Plan for Robot Industry Development” also emphasize the development ideas of industrial robots. The plan states that by 2025, China will become a global source of innovation for robot technology, a high-end manufacturing hub, and a new highland for integrated applications, with annual revenue growth of the robot industry exceeding 20%, and the density of manufacturing robots doubling. By 2035, China’s robot industry will reach an internationally leading level, and robots will become an important component of economic development, people’s lives, and social governance. These goals mainly rely on industrial robots and other carriers to achieve.

Specifically, based on independent research and development, enterprises should also consider capital acquisitions to accelerate mastering key technologies of industrial robot key components and bodies.

The key components of industrial robots are the parts with the highest technical barriers in the industry. Enterprises need to focus on breaking through corresponding key technical difficulties, enhancing investment in the research and development of reducers, controllers, servo motors, etc., and improving technological reserves.

At the same time, it is essential to strengthen the innovation collaboration between the industrial robot industry chain and new technologies, such as 5G communication technology, big data, cloud computing, and AI technology, to empower with intelligence, digitalization, and integration, thereby improving the technical level and service experience of industrial robots, increasing the domestic production rate of key components of industrial robots, and gradually achieving autonomy and controllability across the entire industrial chain ecosystem.

3.2 Exploring Demand Potential and Expanding Market Share

China’s industrial robot industry’s advantages are mainly concentrated in the mid and downstream of the industrial chain, while the mid and upstream segments, which have high demand and considerable profits, are currently in a catch-up position, indicating significant potential for exploration.

In 2023, from the perspective of market share, the proportion of Chinese industrial robot enterprises has been steadily rising, mainly due to the explosive demand in domestic sectors such as photovoltaics, new energy vehicles, and energy storage, with photovoltaic demand being the most robust.

This presents a window of opportunity for the development of China’s industrial robots. For instance, Japan’s industrial robot industry entered a period of significant development after World War II, amid the recovery of the manufacturing industry, where the rapid growth of automotive and electronic machinery manufacturing provided fertile ground for the development of industrial robots.

Japan’s industrial robot development path is also worth researching and learning from. Unlike the United States and European developed countries, Japan adopts a “targeted approach” + “cooperative collaboration” model for the upstream, midstream, and downstream of the robot industry chain, which deeply reflects the essence of “specialization in one’s own field”.

Japanese component manufacturers specialize in the research and production of key components such as reducers and controllers, while body manufacturers focus on the research and manufacturing of the body. System integration emphasizes user needs and experiences, improving the circulation system. The three parties are independent yet collaborate with each other, essentially achieving integration across the upstream, midstream, and downstream of the industrial chain, establishing a solid industrial structure, and maintaining a competitive advantage in international competition.

In the context of industrial upgrading and high demand for labor replacement, Chinese industrial robot enterprises have engaged in deep cooperation with downstream customers, drawing on development models from Japan and others, which will undoubtedly lead to further industrialization and scaling.

In addition to competing for market share with foreign companies in sectors like photovoltaics and new energy vehicles, there is also room for Chinese robot enterprises to explore demand potential in high technical barrier fields such as large six-axis robots and welding robots.

After domestic manufacturers overcome key technical challenges in these fields, they can optimize their product structures and functions while ensuring quality and performance, minimizing customer costs, and deeply expanding in the aforementioned fields, gradually increasing the domestic production rate and expanding market share, thus forming a positive cycle of market supply and demand.

Promoting the forward development of the industry and establishing a healthy “competitive collaboration” relationship among enterprises is crucial. Under the pressure of industrial demand, enterprises should develop rationally and orderly rather than rushing in all at once, which could lead to significant resource consumption and vicious competition.

Enterprises should focus on their strengths in technology research and development. They should target key components such as controllers, servo drives, reducers, sensors, end effectors, robot bodies, and system integration design and manufacturing technologies, and delve into them to break through difficulties.

At the same time, upstream and downstream enterprises should cooperate and complement each other, establishing a long-term and deep cooperative relationship in supply and demand to form a “win-win” model.

The government should also play a guiding role in this process. Firstly, it should construct a roadmap for industrial development through top-level design, providing a basis for all parties in the industry; secondly, it should create a favorable industrial environment, coordinating the relationship between the supply and demand sides of robots, promoting innovation capability, reducing robot usage costs, and enhancing the level of robot applications; finally, it should guide the emergence of a batch of autonomous brand robot enterprises, seizing a number of technology-driven, impactful typical models, thereby promoting the healthy and orderly development of the entire industry.

3.3 Expanding Innovative Application Scenarios

At the end of 2022, ChatGPT emerged, directly igniting a comprehensive explosion of artificial intelligence technology in 2023. Accompanying this is the expectation for a new wave of rapid development for the robot industry chain.

Currently, technologies such as 5G, big data, cloud computing, and AI are experiencing concentrated breakthroughs, with humanoid robots emerging as a core carrier that integrates these technologies.

On October 20, 2023, the Ministry of Industry and Information Technology issued the “Guiding Opinions on the Innovative Development of Humanoid Robots”, proposing that by 2025, an innovative system for humanoid robots will be initially established, with breakthroughs in key technologies such as “brain, small brain, and limbs”, ensuring the safe and effective supply of core components.

AI large models are positioned as the “brain” of humanoid robots. With cognitive enhancement, in the future, as humanoid robots iterate and their applications land, they will integrate the functions of industrial robots, service robots, and special robots. The application scenarios for humanoid robots will be extremely broad, ranging from factories to homes, from shopping malls to farms, making their presence ubiquitous.

3.4 Strengthening Brand Building and Enhancing Brand Influence

3.4.1 Strengthening Brand Building

Robots are known as the “jewel on the crown of manufacturing”, and thus various countries around the world have joined the competition in this field. China has also issued numerous supporting policies, and local governments have launched corresponding subsidies or financial incentives to promote the development of the robot industry.

On this basis, in order to quickly “catch up” and lead the industry trend, Chinese industrial robot enterprises should focus on building their own brand strength.

Currently, the brand strength of Chinese industrial robot enterprises has significantly improved. According to data from the market research agency MIR, in the first quarter of 2023, three domestic manufacturers, Estun, Inovance Technology, and Aeffort, entered the global TOP 10.

Enhancing brand influence and competitiveness still needs to be based on mastering the core technologies of industrial robots. Due to the early focus of China’s industrial robots on the mid and downstream of the industrial chain, there remains a considerable gap in key components compared to foreign countries, which inevitably affects the brand influence of related enterprises on the global stage. Matching brand positioning with technical levels is common marketing wisdom; thus, possessing core capabilities in key areas is a prerequisite for brand reconstruction.

In addition, ensuring steady improvement in product performance and quality, as well as keeping up with user experience and service levels, will foster customer trust. Coupled with strong operations of autonomous brand strength, over time, brand influence and competitiveness will gradually increase.

3.4.2 Expanding Brand Influence

ABB, Fanuc, KUKA, and Yaskawa are known as the “four major families” of global industrial robots, perceived as high-end brands with strong brand influence. Consequently, their products enjoy higher added value, higher profit margins, and higher brand premiums in the market.

How to position the brand is also a crucial aspect of strengthening brand influence. Currently, there is an urgent need to break the inherent impression that Chinese robot products are mainly concentrated in the mid-to-low-end market, and securing more orders from leading customers and accumulating reputation and trust from well-known customers will facilitate a smoother path for brand upgrading.

4 Conclusion

As of now, China’s industrial robot industry has developed for several decades, and it is currently in a period of concentrated breakthroughs in technologies such as 5G, big data, cloud computing, and AI, which signifies a window of opportunity for transformation for Chinese industrial robot enterprises. According to the industry development cycle of approximately 30 years, we are currently at a critical juncture for Chinese industrial robot enterprises to reshape their brand strength.

Chinese industrial robot enterprises need to grasp the trends of intelligence, high-end, integration, and ecology, as these trends will become the mainstream direction for the future development of the global robot industry.

Author: Wang Kunlun (China Electronics Society)

END

● The grand event is coming! The 2024 Embodied Intelligent Robot Development Conference ● Highlights of the 2023 Annual Report of 55 Listed Robot Companies: Mixed Blessings, Intensifying Restructuring ● Highlights of the Embodied Intelligent Robot Development Conference: Leading Themes, High Specifications, Excellent Roadshows

● The grand event is coming! The 2024 Embodied Intelligent Robot Development Conference ● Highlights of the 2023 Annual Report of 55 Listed Robot Companies: Mixed Blessings, Intensifying Restructuring ● Highlights of the Embodied Intelligent Robot Development Conference: Leading Themes, High Specifications, Excellent Roadshows

● The wave of embodied intelligent robots is coming, another industry grand event is about to set sail

● Dialogue with Tsinghua University’s Zhao Mingguo: Accelerating evolution to replicate Boston Dynamics’ movements, what we need is confidence and innovation!

● Preliminary results of the 2023 National Science and Technology Awards announced! Nine 985 universities! XJTU and Huazhong University of Science and Technology in the top three! (Full list attached)

● Unprecedented! American engineers collaborate with ChatGPT4 to design AI chips

● Russian President Putin approves a new version of the “2030 National Strategy for Artificial Intelligence Development”

● A small town in Denmark with a population of less than 20,000! How did Odense become a global robot center?

● The “Commercialization Year” has begun, and humanoid robots welcome new strong players

● Swiss researchers develop new artificial muscles, lighter, safer, and stronger!

● The EU halts Amazon’s acquisition of iRobot, what will become of the former cleaning robot giant?

● The top ten news in the robot industry in 2023

● Muscular tissue-driven bipedal robot emerges, a breakthrough in biological hybrid robots!

● Professionals discuss the robot-as-a-service model – the future of automation

● A comprehensive overview of China’s humanoid robot research teams

● Under the heat of humanoid robots, the struggle between advancement and resistance

● Who is the most outstanding? Highlights of 53 listed robot companies’ 2023 mid-year report

● Download the financial reports of 53 listed robot companies (PDF attached)

● Academician Report|Pan Yunhe: Behavioral intelligence and product intelligence of artificial intelligence

● Academician discusses new driving forces for promoting collaborative intelligent manufacturing of robots

● Academician discusses six key technologies for innovative design of robots

● Ximu Technology expands new angles in humanoid robot research

● Academician discusses the dual driving model for the future development of artificial intelligence

● Academician discusses how institutional intelligence brings “Transformers” from the screen to reality

Contact Us· WeChat: myrobot2001· Contact Number: 18100123515

Contact Us· WeChat: myrobot2001· Contact Number: 18100123515