DRAM

Some DDR4 chip prices have seen an expanded decline.

This week, the market atmosphere continues to cool, with buying momentum appearing quite insufficient. The price decline of DDR4 512×16/1Gx16 chips has significantly widened, as factory inventory levels are ample, and the order situation at the end-user level is poor, resulting in actual demand not being released, leading buyers to generally remain cautious. Reball chips have also seen significant price reductions due to weak demand, with actual transaction prices dropping to around USD1.3, and buying support remains limited.

After a period of strong demand that drove prices of DDR4 RDIMM sharply upwards, this week, as buying gradually weakened, prices have temporarily stabilized, halting the upward trend. Although there are inquiries from factories, the willingness to accept orders is no longer as proactive as before, and market transactions have turned dull.

For DDR4 1Gx8 3200/2666, the spot prices for SK Hynix DJR-XNC/CJR-XNC are around USD3.45/3.20, while Samsung WC-BCWE’s spot prices remain around USD8.00, with WG-BCWE still in short supply, and WC-BCTD prices are approximately USD8.20.

For DDR4 512×8 3200, the general price for Samsung WF-BCWE is around USD2.20.

For DDR4 512×16 3200/2666, the spot price for SK Hynix DJR-XNC has dropped to USD5.20, while Samsung WC-BCWE prices have significantly corrected to around USD6.70, and WC-BCTD prices have also been substantially corrected to around USD6.20.

For DDR4 256×16, Samsung WF-BCTD has dropped to around USD2.14.

Reference prices for modules:

KST DDR4 8G 3200 $28.75

KST DDR4 16G 3200 $54.75

KST DDR4 32G 3200 $107.00

KST DDR5 8G 5600 $20.50

KST DDR5 16G 5600 $36.50

KST DDR5 32G 5600 $68.50

NAND Flash

Wafer prices mostly remain stable.

This week, wafer prices have mostly remained stable, with no significant fluctuations observed. Due to limited spot supply, market quotes have received some support, and there are still some buyers in the low-price range, but due to a price gap between buyers and sellers, actual transaction progress has been limited, and the overall market atmosphere is relatively weak.

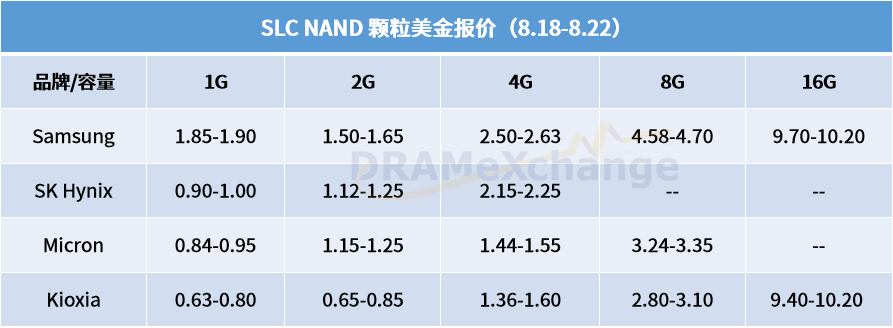

MLC/SLC chip inquiries have appeared intermittently, but factories generally maintain a wait-and-see attitude, with insufficient buying power for high-priced spot goods, leading to unclear trading performance.

This week, the overall demand in the eMMC market is weak, with buyers showing low enthusiasm for stocking up, resulting in poor market activity. Due to a lack of actual transaction support, quotes mostly maintain a fluctuating consolidation pattern.

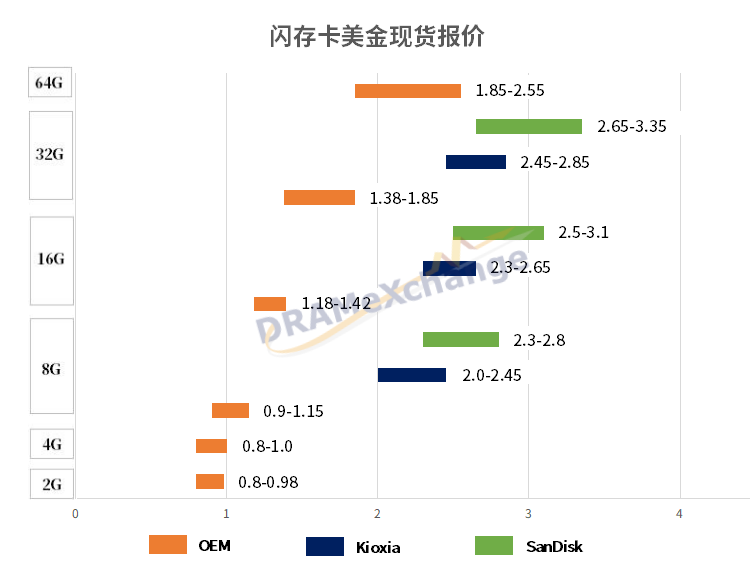

TF Cards

The overall transaction volume has not increased.

This week, the performance of TF cards has been relatively flat, with market demand still limited. Buyer inquiries have been sporadic, with demand concentrated on certain specified capacities, and the supply side’s price changes have been minimal. Buyers remain cautious, with target prices still not high, making it difficult for both parties to reach an agreement, resulting in no increase in overall transaction volume.

▶ About Us

TrendForce is a global high-tech industry research organization, with research areas covering memory, AI servers, integrated circuits and semiconductors, wafer foundry, display panels, LEDs, AR/VR, new energy (including solar photovoltaics, energy storage, and batteries), AI robotics, and automotive technology, among other cutting-edge technology fields. With years of in-depth research, TrendForce is committed to providing forward-looking industry research reports, industry analysis, project planning assessments, corporate strategic consulting, and brand integration marketing services to government and enterprise clients, making it a trusted decision-making partner in the high-tech field.

Scroll up and down to view

Have you discovered the “Share” and “Like” buttons? Click to see!