Chip Industry Research Analysis Report (2025 Update)

1 Industry Overview

Chips (integrated circuits) are the cornerstone of modern information society. Through semiconductor manufacturing processes, components such as transistors, resistors, and capacitors are integrated on tiny silicon wafers to achieve functions such as information processing, storage, and transmission. In 2025, the global chip industry is undergoing profound changes driven by multiple forces such as the artificial intelligence (AI) revolution, geopolitical restructuring, and technological paradigm shifts. The industry is characterized by accelerated technological iteration (such as HBM3E, 3nm/2nm processes), significant regionalization of the supply chain (countries are increasing local supply chain construction), and diversification of application scenarios (deep penetration from consumer electronics to AI, automotive, and industrial IoT).

2 Market Analysis

2.1 Global Market Size and Growth Trends

After experiencing a cyclical adjustment in 2023, the global chip market is set to recover strongly starting in 2024 and continue into 2025. According to data from the World Semiconductor Trade Statistics (WSTS) and SEMI:

2024: The global semiconductor market size will reach $626 billion, a year-on-year increase of 18.1%, mainly due to the explosive demand for AI chips and the recovery of the storage market.

2025 (Forecast): Global semiconductor sales are expected to reach $700.9 billion, a year-on-year increase of 11.2%. Sales of semiconductor manufacturing equipment will also set a new record, expected to reach $125.5 billion, a year-on-year increase of 7.4%.

Long-term Outlook: The industry is moving towards the goal of $1 trillion in annual chip sales by 2030.

*Table: Global Semiconductor Market Size and Growth Rate (2023-2026) Comprehensive Forecast*

2.2 Current Status and Growth Drivers of the Chinese Market

As the largest chip consumption market in the world, China’s dynamics are crucial.

Market Size: In 2024, China’s semiconductor sales will exceed $150 billion, accounting for approximately 29.48% of the global market share. In 2025, the integrated circuit market size in mainland China is expected to further grow, with the global share likely to exceed 30%.

Growth Drivers:

1. Strong Policy Support: The establishment of the third phase of the National Integrated Circuit Industry Investment Fund (registered capital of 344 billion yuan) focuses on investment in equipment, materials, and other fields.

2. Acceleration of Domestic Substitution: Under external environmental pressure, domestic enterprises and research institutions are increasing R&D investment, achieving significant progress in packaging testing, mature processes, and some design areas.

3. Strong Demand from Emerging Markets: Rapid development in areas such as new energy vehicles, artificial intelligence, 5G communication, and industrial automation provides a broad market space and application scenarios for domestic chips.

2.3 In-depth Analysis of Sub-markets

2.3.1 DRAM Memory Market

In the second quarter of 2025, the global DRAM market is showing a simultaneous increase in volume and price, with the market size growing by 20% quarter-on-quarter, reaching $32.101 billion, a year-on-year increase of 37%, setting a historical quarterly high.

① Driving Forces: The demand for high-bandwidth memory (HBM3E) and high-end DDR5 from AI servers continues to rise, while traditional DDR4 is experiencing tight supply and rapid price increases due to capacity reductions.

② Competitive Landscape: The market is highly concentrated, with SK Hynix (38.2%), Samsung (33.5%), and Micron (22%) collectively holding about 94% of the market share. Nanya Technology (1.1%) and Winbond Electronics (0.6%) have benefited from the shift in demand for DDR4, showing significant growth.

③ Chinese Strength: ChangXin Storage, although not detailed in public rankings, is expected to hold the fourth position globally (approximately 10% market share), with rapidly improving technology and capacity, aiming to catch up with Micron in the future.

2.3.2 Wafer Foundry Market

In the first quarter of 2025, global wafer foundry revenue reached $72 billion, a year-on-year increase of 13%.

Technology Drivers: The demand for AI and HPC chips is driving the application and capacity expansion of advanced processes (3nm/4nm) and advanced packaging (such as CoWoS). TSMC’s CoWoS monthly capacity continues to increase.

Competitive Landscape: TSMC, with its technological leadership, has further increased its market share to 35%, continuing to lead the market. Samsung and Intel are striving to catch up. SMIC, as the leading foundry in mainland China, supports domestic demand in mature processes and some advanced technologies.

2.3.3 AI Chip Market

Demand for AI training and inference is currently the strongest growth engine in the chip industry.

Training Chips: Mainly dominated by NVIDIA‘s GPUs, but domestic chips such as Huawei Ascend and Cambricon are also actively catching up.

Inference and Edge AI: Driven by applications on mobile phones, cars, and IoT devices, the demand for more energy-efficient AI inference chips is surging, which also drives innovation in related storage and interface chips.

2.4 Growth Drivers and Challenges

2.4.1 Core Growth Drivers:

① Generative AI and Data Centers: These are the main catalysts for chip sales growth in 2025, with AI-related chips (GPU, CPU, HBM, DRAM, advanced packaging) expected to generate $150 billion in sales.

② Penetration of AI End Devices: AI PCs are expected to account for 50% of PC shipments in 2025, while AI smartphones will account for about 30%, potentially shortening upgrade cycles.

③ Automotive Electrification: The explosive growth of new energy vehicles has led to strong demand for automotive-grade IGBT modules.

④ Other Emerging Fields: Emerging scenarios such as industrial automation, smart grids, and humanoid robots are driving high-end chip demand with a compound annual growth rate of 25%.

2.4.2 Major Challenges:

Geopolitical Risks: Export controls and technology blockades continue to affect the stability of the global supply chain.

Industry Cyclical Fluctuations: The inherent boom-and-bust cycle of the industry requires vigilance against demand fluctuations.

Talent Shortages: The industry is expected to need more than 100,000 skilled workers annually by 2030 to maintain growth.

Cost and Complexity of Technological Iteration: The R&D investment in advanced processes is enormous and faces challenges from physical limits.

3 Technological Development

3.1 Process Technology Evolution

International Leading Level: Mass production of 3nm has been achieved, and progress is being made towards 2nm and more advanced Gate-All-Around (GAA) transistor structures. It is expected that wafer fab equipment investment will grow to $138.1 billion in 2026 to support 2nm production and AI capacity expansion.

Chinese Mainland Level: SMIC has achieved mass production of 14nm processes, and its N+1/N+2 processes (equivalent to 7nm) have been used to support Huawei’s Kirin 9000S chip. However, it is still limited in more advanced processes due to the acquisition of key equipment such as EUV lithography machines.

3.2 Advanced Packaging Technology

As Moore’s Law approaches physical limits, advanced packaging has become a key way to enhance chip performance, integration, and yield.

3D Packaging and Chiplet: Technologies such as TSMC’s CoWoS, SoIC, Intel’s Foveros, and JCET’s exclusive 3D packaging and Chiplet technology enable high-density packaging solutions that make AI chip performance comparable to 5nm monolithic chips.

HBM (High Bandwidth Memory): HBM3E has become standard for AI servers, with its stacking and interface technology being a frontier focus. Montage Technology holds over 70% of the global DDR5 second-generation MRCD/MDB chip market share and leads the formulation of HBM3E interface standards.

3.3 Storage Technology Innovations

DRAM: Evolving towards HBM3E and DDR5. Micron expects the HBM market size to exceed $15 billion in 2025, accounting for over 20% of the total DRAM market. The process is developing towards 1β (approximately 10nm level).

NAND Flash: The number of stacking layers in 3D NAND continues to increase, achieving mass production of 232 layers and moving towards higher layers.

3.4 Third Generation Semiconductor Applications

Third-generation semiconductors represented by silicon carbide (SiC) and gallium nitride (GaN) have significantly increased their penetration in fields such as new energy vehicles, photovoltaics, 5G communication, and fast charging.

-

SiC: Increases the charging efficiency of electric vehicles by 30%.

-

GaN: Penetration in 5G base station RF devices exceeds 60%.

3.5 Other Cutting-edge Technologies

-

Storage-Compute Integration Architecture: Cambricon’s first storage-compute integrated chip improves energy efficiency by 10 times.

-

New Chip Architectures: FPGAs play a key role in 5G and industrial control, with Unisoc’s 28nm FPGA chips matching Xilinx and passing automotive certification.

-

Silicon Photonics Technology: Technologies such as CPO (Co-Packaged Optics) are expected to solve the power consumption and bandwidth bottlenecks of high-speed data transmission.

Table: 2025 Comparison of China’s Chip Technology Development Level with International Standards

4 Policy Environment

4.1 Global Industry Policy Trends

In 2025, major global economies continue to increase policy support and strategic layout for the chip industry, which has become a strategic focus of national technological competition.

-

United States: The “CHIPS and Science Act” provides approximately $52.7 billion in funding support for semiconductor research and production, offering companies $24 billion in investment tax credits, and authorizing approximately $200 billion in grants for scientific innovation over the next decade. This act aims to revitalize the U.S. semiconductor industry, but it includes clauses that restrict U.S. companies from supporting semiconductor R&D and production in countries like China, distorting the global semiconductor supply chain.

-

European Union: A plan of $46.3 billion has been formulated to expand the capacity of the European semiconductor manufacturing industry, with total public and private sector investments expected to exceed $108 billion, mainly for the construction of new large manufacturing bases, aiming to increase the EU’s global chip manufacturing market share from the current 10% to 20% by 2030.

-

Japan: Approved subsidies of up to $3.9 billion for Japanese semiconductor company Rapidus Corp. to achieve mass production of 2nm chips by 2027, and plans to invest 10 trillion yen from 2022 to 2032 to enhance domestic chip manufacturing capabilities and diversify chip supply.

-

South Korea: Plans to strengthen the country’s semiconductor industry competitiveness by promoting investments from Samsung Electronics and SK Hynix to build large semiconductor clusters and advance a support plan exceeding 10 trillion won.

4.2 China’s Industry Policy Support

The Chinese government continues to strengthen its support policies for the chip industry.

-

Big Fund Phase III: Established the National Integrated Circuit Industry Investment Fund Phase III with a registered capital of 344 billion yuan, enhancing support for semiconductor manufacturers and equipment, materials suppliers, etc.

-

Tax Incentives: Corporate income tax incentives, tax incentives for the transformation of scientific and technological achievements, and additional deductions for R&D expenses have increased the enthusiasm of enterprises for independent innovation.

-

R&D Support and Key Technology Breakthroughs: The government promotes breakthroughs in key core technologies, emphasizing cutting-edge and disruptive technology breakthroughs, such as advanced processes, quantum computing, and new semiconductor materials R&D.

-

Subsidy Strength: In 2023, 25 top semiconductor companies in China received a total of government subsidies amounting to 20.53 billion yuan, a 35% increase from 2022.

4.3 Impact of Trade Environment and Responses

-

Impact: Export controls and trade friction measures from countries like the U.S. restrict the export of key semiconductor equipment, technologies, and related products to China. Companies listed on the “Entity List” face supply chain restrictions, affecting normal production and operations, and delaying the R&D and production processes of high-end chips in Chinese enterprises.

-

Responses: Chinese companies are adopting strategies such as strengthening technological R&D and innovation, expanding diversified markets, and strengthening supply chain management to cope with these challenges. This has also accelerated the process of domestic substitution, with domestic semiconductor equipment orders expected to increase by 120% year-on-year between 2024 and 2025.

5 Key Enterprise Analysis

This section will provide an in-depth analysis of key enterprises in the global and Chinese chip industry chain.

5.1 International Leading Enterprises

-

TSMC: The absolute leader in global wafer foundry, with its market share further increasing to 35% in Q1 2025. Its advanced processes (3nm/2nm) and advanced packaging (SoIC, CoWoS) technologies are leading, making it a core beneficiary of the AI chip wave. The planned global capacity layout aims to enhance supply chain resilience.

-

Samsung Electronics: A powerful IDM (Integrated Device Manufacturer), fiercely competing with SK Hynix in the storage chip (DRAM, NAND) sector, ranking second in the DRAM market with a share of 33.5% in Q2 2025, while closely following TSMC in the wafer foundry sector.

-

SK Hynix: Holds a leading advantage in the HBM sector, ranking first in the DRAM market with a share of 38.2% in Q2 2025. Its HBM3E products are key components for training AI servers.

-

NVIDIA: The dominant player in AI computing chips, with its GPUs and accelerated computing platforms serving as the infrastructure for current AI training. Continuously launching more powerful chip architectures and system solutions to solidify its market position.

-

Micron: A major U.S. storage chip giant, ranking third in the DRAM market with a share of 22% in Q2 2025. The HBM market size is expected to exceed $15 billion in 2025, actively expanding the production capacity of high-value-added products such as HBM3E and 128GB DDR5.

5.2 Analysis of Core Chinese Enterprises

-

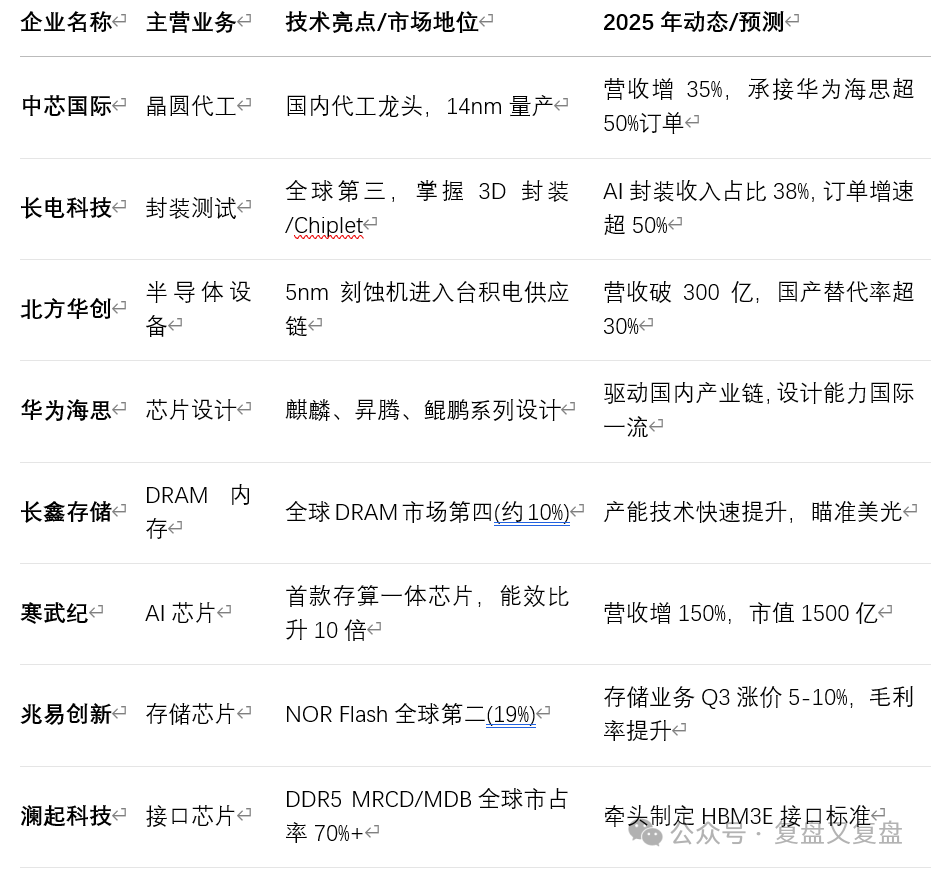

SMIC: The leading wafer foundry in China, serving as the cornerstone of 14nm domestic manufacturing. Its 14nm yield has reached international leading levels, and its N+1/N+2 processes support the return of Huawei’s Kirin 9000S chip. In the first half of 2025, revenue grew by 35%, taking on over 50% of Huawei HiSilicon’s 14nm and below process orders.

-

JCET: The global leader in packaging and testing, a revolutionary player in AI chip packaging. As the third-largest packaging and testing company globally, it uniquely masters 3D packaging and Chiplet technology, providing high-density packaging solutions for Huawei’s Ascend 910C AI chip, with performance comparable to 5nm monolithic chips. In 2025, AI-related packaging revenue is expected to account for 38%, with order growth driven by Huawei’s AI chip mass production exceeding 50%.

-

NAURA: A domestic equipment disruptor. Its 5nm etching machines have entered TSMC’s supply chain, with a domestic replacement rate of over 30% for PVD equipment. Revenue is expected to exceed 30 billion yuan in 2025, with Huawei’s equipment procurement accounting for 20%.

-

Hisilicon: A domestic chip design giant, although limited in advanced process production, its chip design capabilities are world-class. Relying on Huawei’s strong ecosystem, it continues to launch products in mobile SoCs (Kirin series), AI acceleration chips (Ascend series), and server CPUs (Kunpeng series), driving the development of the domestic chip industry chain.

-

YMTC & CXMT: The hope for China’s storage chips.

-

YMTC: Leading in the 3D NAND Flash field, successfully developing 232-layer 3D NAND flash memory chips.

-

CXMT: Focused on DRAM memory, launching LPDDR5 series DRAM products. The industry expects its actual DRAM market share to rank fourth globally (approximately 10%).

Cambricon: A pioneer in domestic AI chips. Released the first storage-compute integrated chip, improving energy efficiency by 10 times, applied in Huawei Cloud AI inference scenarios. Revenue is expected to grow by 150% in 2025, with a market value exceeding 150 billion yuan.

Will Semiconductor: Strong in semiconductor discrete devices and integrated circuits, especially with a high market share in image sensor chips. Expanding its business through mergers and acquisitions, its products feature high pixel counts and low power consumption, widely used in image acquisition and processing in consumer electronics.

GigaDevice: A leader in the storage field. Its global NOR Flash market share is second (19%), with automotive-grade products certified; niche DRAM capacity reaches 800 million units/month, with a yield of 98%. Storage business prices are expected to rise by 5%-10% in Q3, with gross margins improving by 3-5 percentage points.

Montage Technology: A leader in HBM interface chips. The only company globally to mass-produce DDR5 second-generation MRCD/MDB chips, with a market share exceeding 70%, with a single chip price of $20; CXL memory controllers have entered the AWS and Microsoft supply chains.

Table: Key Indicators and Positioning of Major Chinese Chip Enterprises in 2025

6 Investment Opportunities and Risk Analysis

6.1 Focus on Current Market Investment Opportunities

In the second half of 2025, investment opportunities in the chip industry are closely related to stock market performance, mainly revolving around AI computing demand, deepening domestic substitution, and technological breakthroughs.

-

AI Computing Chips and HBM Industry Chain: The demand for AI servers continues to explode, driving the demand for related chips and high-bandwidth memory (HBM). In Q2 2025, the global DRAM market grew by 20% quarter-on-quarter, with HBM3E becoming mainstream. The HBM market size is expected to exceed $15 billion in 2025, accounting for over 20% of the DRAM market. SK Hynix (market share 38.2%), Samsung (33.5%), and Micron (22%) dominate the market, but there is significant potential for domestic substitution.

-

A-share Related Targets:

-

Cambricon (688256.SH): As a leading domestic AI chip company, its stock price surged to 1243 yuan/share on August 22, 2025, with a total market value exceeding 500 billion yuan. Deeply adapted to domestic large models (such as DeepSeek-V3.11), benefiting from the explosive demand for AI inference chips.

-

Montage Technology (688008.SH): A global leader in storage interface chips, with significant advantages in the DDR5 field, expected to enter the HBM interface chip sector.

-

Liangrui New Materials (688300.SH): A key supplier of packaging materials (fillers) for HBM, benefiting from HBM capacity expansion.

-

Domestic Substitution of Semiconductor Equipment and Materials: With the expansion of domestic wafer fabs and the increase in domestic replacement rates, equipment and materials companies are experiencing full orders. The Big Fund Phase III (registered capital of 344 billion yuan) focuses on this field.

-

A-share Related Targets:

-

NAURA (002371.SZ): A leading domestic semiconductor equipment platform, with revenue of 29.838 billion yuan in 2024, net profit increasing by 44.17% year-on-year. Its 14nm process equipment is becoming competitive.

-

SMIC (688012.SH): A leading etching equipment company, benefiting from the expansion of domestic logic and storage chip production lines.

-

Special Integrated Circuits and High-end Logic Chips: The industry inflection point has emerged, with strong demand for domestic FPGA, CPU/GPU, and high gross margins (e.g., Unisoc’s integrated circuit products have gross margins exceeding 70%).

-

Unisoc (002049.SZ): A leader in special integrated circuits, with revenue growth of 6.07% year-on-year in H1 2025, and a net profit growth of 4.39% year-on-year. Its FPGA and system-level chips are successfully promoted in aerospace and other fields.

Haiguang Information (688041.SH): A core supplier of domestic CPU/GPU, with a 20% limit on the stock price on August 22, 2025, benefiting deeply from domestic AI computing demand.

High Elasticity Opportunities in the Sci-Tech Innovation Board Semiconductors: Funds prefer semiconductor companies on the Sci-Tech Innovation Board. The Sci-Tech Chip 50 ETF (588750) rose over 10% on August 22, 2025, with significant trading volume, and net inflows exceeding 3 billion yuan in the past month.

Sector Logic: The Sci-Tech Innovation Board gathers many core enterprises in the domestic semiconductor industry chain, such as Chipone (AI ASIC leader), Huahong (power semiconductor IDM leader), etc., combining high growth potential and policy support.

6.2 Risk Analysis: Focus on Market Fluctuations and Policy Changes

Investing in the chip industry requires vigilance against the following risks, which may directly impact the stock performance of related companies:

-

Technological Iteration and R&D Risks: Semiconductor technology updates rapidly. If a company’s R&D progress lags (e.g., the evolution of HBM technology to HBM4), or products do not meet expectations, it may lead to loss of market share and pressure on stock prices.Probability: Medium-High; Impact: High

-

Geopolitical and Supply Chain Risks: Export controls and technology blockades from countries like the U.S. continue to pose risks. This may disrupt the supply chains of some companies, delay production plans, and subsequently affect performance and valuation.Probability: Medium-High; Impact: High

-

Industry Cyclical and Demand Fluctuation Risks: The semiconductor industry is cyclical. If the global macroeconomic downturn or AI application deployment does not meet expectations (e.g., slowing growth in AI server shipments), it may lead to demand shrinkage and product price declines (despite current DRAM/NAND prices rising), affecting corporate profitability.Probability: Medium; Impact: High

-

Valuation and Market Sentiment Risks: Some semiconductor stocks, especially those on the Sci-Tech Innovation Board, have seen significant short-term gains, and valuations may have already discounted future performance. When market sentiment shifts, they may face substantial stock price volatility and correction pressure.Probability: Medium; Impact: Medium-High

Table: Chip Industry Investment Risk Ratings and Response Strategies

6.3 Investment Strategy Recommendations: Follow Trends and Select Stocks

Based on the current market, the following strategies are recommended:

-

Seize Core Main Lines, Focus on Performance Realization: Prioritize selecting companies in high-prosperity tracks such as AI computing (HBM, GPU/ASIC), domestic substitution (equipment, materials, special chips), with strong technological capabilities, full orders, and the ability to continuously realize performance, such as SMIC, NAURA.

-

Use ETFs for Layout, Diversify Stock Risks: For investors looking to reduce individual stock volatility risks, attention can be paid to Sci-Tech Chip 50 ETF (588750) and other industry ETFs, providing a one-click layout of the semiconductor industry chain and sharing the overall growth dividends of the industry.

-

Dynamic Risk Assessment, Maintain Investment Flexibility: Closely monitor international trade policy trends, industry inventory cycle changes, and important companies’ financial reports and performance guidance, adjusting investment portfolios in a timely manner. Be cautious with overvalued targets.

-

Long-term Perspective, Focus on “Invisible Champions”: In semiconductor materials, equipment components, IP, and other sub-sectors, there are some “invisible champion” companies with core technologies and significant domestic substitution potential, worthy of long-term tracking and layout.

7 Conclusion and Recommendations

7.1 Industry Outlook Summary

In 2025, the global chip industry will continue to maintain a growth trend, with the market size expected to reach $700.9 billion (year-on-year growth of 11.2%), driven mainly by AI computing demand, storage technology upgrades, and automotive electrification. In terms of technological innovation, process technology is advancing towards smaller nanometer levels, with advanced packaging and storage technology innovations becoming key ways to enhance chip performance. The Chinese market will continue to grow faster than the global average, but still faces “bottleneck” issues in areas such as advanced processes, EDA tools, and core equipment. Geopolitics will continue to shape the global supply chain landscape, with trends towards regionalization and localization strengthening.

7.2 Development Recommendations

Based on an in-depth analysis of the chip industry, the following recommendations are proposed:

-

For Enterprises:

Increase R&D Investment, Break Through Key Core Technologies: Especially in advanced processes, EDA tools, semiconductor equipment, and high-performance materials.

Build a Collaborative Industrial Ecosystem: Strengthen the collaborative development of various links in the chip design, manufacturing, packaging testing, equipment materials, etc., to enhance the overall competitiveness of the industry chain.

Actively Explore Emerging Application Markets: Accelerate the application of chip technology in emerging fields such as artificial intelligence, smart connected vehicles, IoT, and industrial automation, cultivating new market growth points.

Optimize Supply Chain Management, Enhance Risk Resistance: Reduce geopolitical and supply disruption risks through supply chain diversification and strategic reserves.

-

For Investors:

Focus on High-Growth Sub-sectors: Such as AI chips, HBM, semiconductor equipment, component materials, and third-generation semiconductors.

Concentrate on Enterprises with Core Technologies and Domestic Substitution Capabilities: Especially leading enterprises and “invisible champions” with competitive advantages in sub-sectors.

Beware of Industry Cyclicality and Geopolitical Risks: Adopt a diversified investment strategy, focusing on companies’ technological barriers and long-term competitiveness rather than short-term fluctuations.

-

Combine Long-term Holding with Flexible Allocation: Consider long-term holding of core assets in hard technology, while flexibly allocating in high-growth sub-sectors.

-

For Policymakers:

Continue to Provide Stable Policy Support and Funding Investment: Especially in basic research, talent cultivation, and breakthroughs in key core technologies.

Create a Good Innovation Environment and Intellectual Property Protection System: Encourage enterprises to make long-term R&D investments and innovations.

Deepen International Cooperation: Strengthen technological cooperation and market development with international chip companies while ensuring supply chain security, integrating into the global innovation network.

Enhance Talent Cultivation and Introduction: Improve the construction of integrated circuit disciplines, increase investment in talent cultivation, and attract global top talents.

In summary, the chip industry is a foundational and leading industry in the digital economy era, related to national economic security and technological competitiveness. 2025 will be a key year for the restructuring of the global chip industry landscape, and Chinese enterprises need to seize the opportunities brought by the AI wave, break through the dilemmas caused by technological blockades, and achieve high-quality development of the chip industry.

This response was generated by AI and is for reference only; please verify carefully.

The article was largely generated by AI and is for reference only, not constituting investment advice!