For many companies developing embedded software products, the immediate VAT refund is an important tax benefit. However, a common question arises: if a company met the criteria in the past two years but did not apply for a refund, can they still recover this portion of “real money” now?

The answer is: Yes! But the time window is crucial.

1. Core Policy Points for Embedded Software VAT Refunds

According to the “Notice on VAT Policies for Software Products” (Cai Shui [2011] No. 100) issued by the Ministry of Finance and the State Administration of Taxation, the following core conditions must be met to enjoy VAT refunds for embedded software:

1.“Separation of Software and Hardware” is Key: Companies must account for embedded software products separately, clearly distinguishing the sales revenue and costs of software and hardware. This is the fundamental prerequisite for applying for a refund.

2.Clear Ownership: Companies must own the copyright or ownership of the embedded software being sold.

3.Core Indicators Must Be Met: The software component must meet the definition of “computer software products,” which must simultaneously satisfy:

Functional Indicator: Carrying specific functions and application tasks.

Carrier Indicator: Stored on tangible media such as disks or CDs.

Operational Indicator: Capable of running on computers or other devices.

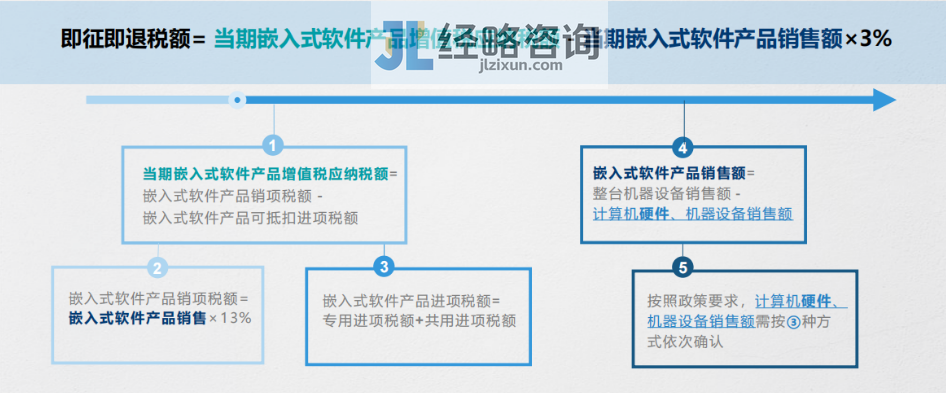

Refund Calculation Method (Simplified): The VAT amount to be refunded for embedded software products = Sales revenue of embedded software products × 13% – Deductible hardware costs for embedded software products × 13%

2. Retrospective Application: Policy Allows, but Time is Tight

The State Administration of Taxation’s “Announcement on Issues Related to VAT Policies for Software Products” (Announcement No. 19, 2012) clearly states in Article 3:

“If a taxpayer sells embedded software products that meet the refund conditions specified in this notice, and has not timely declared to enjoy the immediate refund policy, they may apply for retrospective refunds. The deadline for retrospective refunds is within two years from the date of sale.”

Key Interpretations and Practical Points:

1.“Two Years” is a Hard Deadline: This is the core constraint for retrospective refunds. For example, today is July 16, 2025:

Companies can apply for retrospective refunds for sales of qualifying embedded software products made after July 17, 2023.

For products sold on or before July 16, 2023, the right to a refund has expired, and applications can no longer be made.

2.“Not Timely Declared” is a Prerequisite: This clause applies to situations where the sales at the time met the refund conditions, but for various reasons (such as lack of understanding of the policy, unclear accounting, process delays, etc.), the application was not made on time. If the sales did not meet the conditions at the time, retrospective claims cannot be made.

3.Higher Requirements for Application Materials: The materials required for retrospective applications are usually more complex and stringent than those for current applications. Companies need to provide sufficient original documents (such as contracts, invoices, clear accounting records, software copyright certificates, product testing reports, etc.) to prove that they met all refund conditions at the time of sale.

3. Action Recommendations: Conduct Immediate Self-Inspection and Seize the Last Opportunity

1.Urgent Self-Inspection (From July 2023 to Present):

Product Review: List all embedded software products sold in the past two years.

Check Conditions: Verify whether each product met the core refund requirements of “separation of software and hardware accounting,” “clear ownership,” and “meeting the three indicators” at the time of sale.

Accounting Data: Accurately separate and calculate the software sales revenue and corresponding deductible hardware costs for each qualifying product.

2.Prioritize “Critical Point” Business: Focus on sales activities between July and August 2023, as this revenue is at the final stage of the two-year retrospective period and should be prioritized to avoid missing out.

3.Systematic Financial and Tax Management: Establish a dedicated system to ensure compliance management throughout the entire process of embedded software products from contract signing, financial accounting, invoicing to refund applications, to avoid missing opportunities again.

4.Seek Professional Support: The details of the refund policy are complex, and retrospective applications are even more challenging. It is recommended that companies:

Internal Collaboration: Ensure close cooperation between finance, technology, and sales departments to ensure data accuracy and a complete evidence chain.

External Support: Collaborate with professional tax consultants or agencies familiar with software VAT refund policies (such as Jinglue Consulting) to efficiently complete compliance diagnostics, material preparation, and application work, maximizing the success rate.

Jinglue Consulting specializes in financial and tax planning for software companies and is well-versed in the details and practical points of embedded software VAT refund policies. If you have questions about retrospective applications or daily refund management, please feel free to contact us for personalized solutions to ensure that the tax benefits you deserve do not go to waste!

Policy benefits are fleeting, and compliance retrospection cannot be delayed. Let us, the professionals, help you secure every penny of your entitled VAT refunds.