Author Introduction:

Li Jinhua, male, from Hanchuan, Hubei, is a researcher at the Institute of Quantitative Economics and Technical Economics of the Chinese Academy of Social Sciences, a distinguished professor at the Business School of the Chinese Academy of Social Sciences, and a doctoral supervisor. His research focuses on statistics and quantitative economics.

Source of the Article:

Journal of Beijing Technology and Business University (Social Science Edition), Issue 6, 2022. This WeChat version of the article omits annotations; please refer to the original text for citations.

The Development Reality and Policy Considerations of China’s Information Industry and Informatization in the Context of the Digital Economy

Abstract: Against the backdrop of the rapid development of the digital economy, China has always placed great importance on the development of the information industry and the improvement of the country’s informatization level. In terms of the information industry, over the past decade, China’s software product revenue and information technology service revenue have shown an upward trend; telecommunications business revenue has grown rapidly, network supply capacity has continuously strengthened, and fixed asset investment growth has significantly accelerated; the telecommunications industry in the eastern region has a higher level of development, while the level in the central and western regions is lower. The development of the digital economy has brought opportunities and challenges to China’s information industry, while also exposing shortcomings in meeting the requirements of digital economic development. In terms of informatization, industrial software and the industrial internet are converging, leading to the emergence of new business models in the industrial internet field; artificial intelligence is widely applied across various fields, profoundly impacting the digital transformation of traditional industries; the scale of industrial internet platforms is expanding, and a public service platform system has been established; however, in the context of big data, there are still shortcomings and deep-seated issues that need to be addressed in China’s informatization development. In the future, China needs to accelerate the construction of information industry and informatization infrastructure, enhance the energy efficiency of information industry products and equipment; break through technological bottlenecks in the industrial software sector, and accelerate software iteration, algorithm improvement, and technological upgrades; optimize the layout of the information industry, speed up the construction of information industry clusters to serve the development of the digital economy; strengthen international cooperation in information industry technology and capacity, and build a security guarantee system for information infrastructure.

Keywords: digital economy; information industry; informatization; industrial internet; artificial intelligence industry; information infrastructure

1. Research Background

In October 2021, Chinese President Xi Jinping announced at the 16th G20 Leaders’ Summit that China decided to apply to join the Digital Economy Partnership Agreement (DEPA). DEPA includes 16 sectors, covering hot topics such as e-commerce, data transfer, personal information security, artificial intelligence, and financial technology. Its main content includes paperless trade, electronic invoices, electronic payments, personal information protection, cross-border data flow, computer facilities, financial technology cooperation, artificial intelligence, government procurement, and competition policy. DEPA was initially signed by Singapore, New Zealand, and Chile in June 2020 and has since attracted the attention of many countries worldwide. In January 2021, DEPA took effect in New Zealand and Singapore, and in November in Chile. In August of the same year, South Korea completed its domestic procedures for joining DEPA and officially notified DEPA member countries of its intention to join in September. After proposing to join DEPA, China held more than ten special talks at the ministerial level, chief negotiator meetings, and informal consultations at the technical level with its member countries. China explained its legal regulations, policy practices, and regulatory measures in the digital field. Member countries expressed a welcoming attitude towards China’s accession to DEPA and decided to establish a working group for China’s accession to DEPA. Subsequently, the Chinese government conducted negotiations under the framework of the “China DEPA Working Group” to advance the accession process. It is foreseeable that China will contribute to international cooperation in the digital economy, innovation in the digital economy, and sustainable development in the digital economy.

The digital economy is a broad economic concept that represents a new economic form in the information age. It achieves rapid allocation and combination of production resources through the identification, storage, and utilization of data, realizing high-quality economic development. The digital economy requires the direct or indirect use of data to scientifically guide resource utilization, employing emerging technologies such as artificial intelligence, 5G communication, cloud computing, the Internet of Things, and blockchain. In this form, data is the core element, and information technology and networks are the main carriers. This form relies on the integrated application of data and information communication technology to change or transform production methods and lifestyles, reshape the national economic structure, and alter the global economic competition landscape.

The digital economy is highly related to a country’s information industry and informatization. Informatization is a historical process aimed at fully utilizing modern computing and information technology, developing information resources, promoting information exchange and knowledge sharing, enhancing the quality of life for the public, and achieving economic and social progress. Building a strong manufacturing country, enhancing China’s industrial competitiveness, and promoting the upgrading of China’s industrial and supply chains are key. The Chinese government has always placed great importance on the information industry and informatization construction. In August and September 2013, the Ministry of Industry and Information Technology (MIIT) issued the “Special Action Plan for Deep Integration of Informatization and Industrialization (2013-2018)” and the “Informatization Development Plan,” with the core idea of building a national information infrastructure, promoting e-government, building a service-oriented government, enhancing the informatization level of the national economy and social undertakings, and strengthening national information security capabilities. In July 2016, China released the “National Informatization Development Strategy Outline,” proposing three strategic tasks for national informatization development: enhancing development capabilities, improving application levels, and optimizing the development environment. The basic principles for designing informatization development are: adhering to overall promotion, innovation-driven, development-driven, benefiting people’s livelihoods, win-win cooperation, and ensuring security, aiming to achieve the strategic goal of advanced national information technology, developed industries, leading applications, and unassailable network security by 2025. In November of the same year, MIIT issued the “Informatization and Industrialization Integration Development Plan (2016-2020),” emphasizing the need to seize opportunities, respond to challenges, promote the deep integration of industrialization and informatization, build a strong manufacturing country, and promote economic and social transformation.

From 2017 to 2021, relevant national departments successively issued documents such as the “Information Industry Development Guidelines” (MIIT, National Development and Reform Commission), “Guiding Opinions on Further Promoting Informatization of Small and Medium-sized Enterprises” (MIIT), and the “14th Five-Year Plan for Deep Integration of Informatization and Industrialization” and the “14th Five-Year National Informatization Plan” (Central Cybersecurity and Informatization Commission). These documents (plans) outline the key points, major projects, and major tasks for the development of informatization in China, focusing on basic electronics, integrated circuits, basic software and industrial software, cloud computing, big data, and computer and communication equipment; major projects include basic electronics enhancement projects, intelligent products + service value enhancement projects, national information infrastructure construction projects, security capability enhancement projects, integrated circuit industry leapfrog construction projects, software industry enhancement development projects, and industrial internet industry pilot demonstration projects; major tasks include the innovative development of digital productivity, construction of digital infrastructure, utilization of data elements, security of digital industrial systems, and co-governance and sharing of digital social governance systems. These documents are an important part of the national “14th Five-Year” planning system and serve as action guidelines for the development of China’s information industry and informatization construction. In February 2022, the Ministry of Agriculture and Rural Affairs issued the “14th Five-Year National Agricultural and Rural Informatization Development Plan,” deploying plans for smart agriculture, digitalization of agricultural industrial chains, agricultural production efficiency, agricultural big data, and digital rural construction, outlining a blueprint for narrowing the digital gap between urban and rural areas and strengthening the informatization support capacity of agriculture and rural areas.

In academia, some scholars are also paying close attention to the development of China’s information industry and informatization. Huang Yongming and Chen Xiaofei studied the growth and industrial integration of China’s information industry using input-output coefficients and econometric models, finding significant differences in the demand for information technology across different industries. The integration of China’s information industry with non-information industries is further tightening, and China needs to increase investment in information industry infrastructure, fully leverage the technological diffusion effect of information industry agglomeration, and accelerate the integration of lagging traditional industries with the information industry. Vanke and Liu Yaobin studied the comparative advantages of China’s information industry domestic value chain at the provincial level, finding that the eastern coastal regions have obvious comparative advantages; in terms of industry, the manufacturing sector has a relatively obvious comparative advantage, while the service sectors represented by “scientific research and technical services,” “metal products, machinery and equipment repair services,” “rental and business services,” and “information transmission, software and information technology services” have relatively insufficient comparative advantages. China should avoid the phenomenon of excessive concentration of comparative advantages in a certain link of the domestic value chain of the electronic information industry in a single province, maintaining controllable differences in resource allocation policies that support provincial comparative advantages. Yu Meng and Guo Shiming studied the many problems and challenges faced by the upgrading of China’s information industry in the context of the third industrial wave, proposing to strengthen the ontological development of the information industry, enhance the proactivity of information industry development, and improve institutional guarantees. Zhou Jiali and Xiao Yan calculated trade location entropy, studied the evolution pattern of the global electronic information industry trade network, and analyzed the location entropy differences and trade pattern evolution of major information industry products, suggesting that China needs to strengthen key technology breakthroughs in the information industry to form monopolistic technological advantages; accelerate innovation in key links of the information industry business, strengthen fiscal and financial support for information industry agglomeration areas, promote the development of information technology to ensure industrial information security, and popularize and accelerate the application of practical technologies in the information industry under the digital economy. Gong Jing and others studied the transformation and development issues faced by China’s electronic information industry clusters, finding that the differentiated development of information industry clusters is not obvious, the public service system within the clusters is not well developed, and the independent innovation capability of the clusters is still weak. Therefore, China needs to adhere to the dual drive of institutional innovation and technological innovation, accelerate the climb to the high end of the global industrial chain, and implement strategies for large companies and brand strategies to drive the overall upgrade of the industrial chain. Zhang Yao and Cao Junjie studied the informatization issues in different regions of agriculture, finding that informatization increasingly promotes agricultural economic growth, and the disparity in informatization development levels has widened the gap in regional agricultural economic development, with significant differences in agricultural and rural informatization across different regions. Therefore, it is necessary to leverage the leading role of governments at all levels, strengthen the construction and application of agricultural and rural informatization, develop rural e-commerce, and promote the digital transformation and upgrading of agriculture to support agricultural and rural economic growth. Yan Chaodong and Ma Jing empirically studied the spatial spillover effects and characteristics of informatization on China’s industrial transformation and upgrading, finding that informatization can significantly promote the industrial transformation and upgrading of the local area, thus emphasizing the importance of the spatial effects of industrial transformation and upgrading, further strengthening the construction of the industrial internet, deepening the integration of informatization with industrial enterprises, and preventing the negative impacts of informatization spillover. Oliveira-Dias et al. studied the new opportunities and challenges brought by the use of information and digital technologies (IDT) in the context of Industry 4.0, discussing the impact of information and digital technologies on industrial development based on the life cycle of technology. Yu et al. believe that information and communication technology (ICT) has broader application prospects in the future, and modern industrial society must vigorously develop information technology and the information industry to achieve informatization. Dissanayake et al. discuss the important role of information technology (IT) in corporate governance, which is crucial for the success of IT organizations. Malik et al. discuss strategic business partnerships in the global information context, emphasizing the relevance of multiple integrations in global IT sector strategic business partnerships.

The aforementioned domestic and international literature has studied the issues of China’s information industry and informatization from different angles, but it is not difficult to find that there are few results studying the development of China’s information industry and informatization level from a macro perspective. This article explores the current issues of China’s information industry and informatization from a macro perspective and reflects on the future development paths of the information industry and informatization.

2. The Development of China’s Information Industry in the Context of the Digital Economy

(1) The Current Situation of China’s Information Industry Development

Human society has experienced three industrial revolutions, marked by the emergence of the steam engine, the use of electricity, and the development of atomic energy and information technology. This highlights the important position and role of information technology in human history. Information technology mainly refers to the acquisition, display, processing, storage, transmission, and conversion of text, numbers, images, and sounds supported by computer and communication technology. On one hand, it manifests as providing equipment, and on the other hand, it manifests as providing information services. The main characteristics of modern information technology are computer technology, microelectronics technology, and communication technology, hence it is often referred to as information and communication technology. The information technology industry is an emerging industry and a strategically significant industry that China is vigorously developing, playing an important supporting role in building a strong manufacturing country. The information industry is also an advanced service industry, a foundational industry, and a pillar industry. It develops based on modern scientific and technological theories, relying on advanced science and technology, and possesses high-tech, innovation, driving, and penetration characteristics, which are crucial for optimizing China’s industrial structure, transforming economic growth methods, social employment, and national security stability. Currently, countries around the world are leveraging the information industry to collect, store, and transmit socio-economic information, improving total factor productivity, shortening the time and space distance from scientific and technological inventions to practical production activities, promoting the development of technology-intensive industries, enhancing the level of industrial structure, and adjusting and optimizing the national economic structure.

China has always placed great importance on the development of information technology and the information industry, continuously developing emerging business formats such as the Internet of Things, mobile internet, and cloud computing, innovating information application technologies and business models, accelerating the replacement of traditional products with new electronic products, promoting the widespread application of industrial software, communication information technology, and electronic technology in various fields, especially in the industrial sector, and facilitating the integration of informatization and industrialization. The trend of service-oriented information industry in China is becoming more evident. Key indicators show that the development level of China’s information industry is steadily improving.

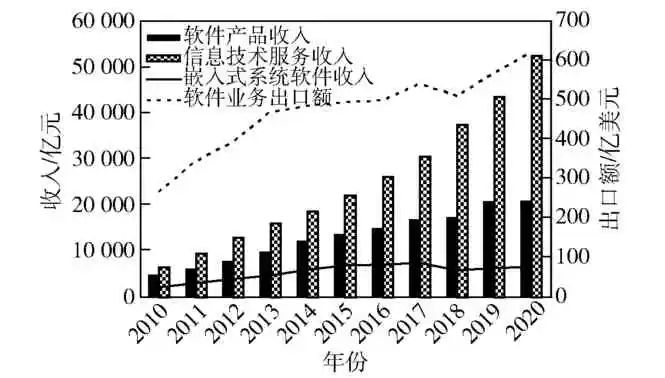

From Figure 1, Table 1, and the “2021 China Software and Information Service Industry Development Report” published by the China Software Industry Association, the following characteristics of China’s information industry development can be observed.

Figure 1 Trends in Major Indicators of China’s Information Industry Development

Data Source: “China Statistical Yearbook 2021”.

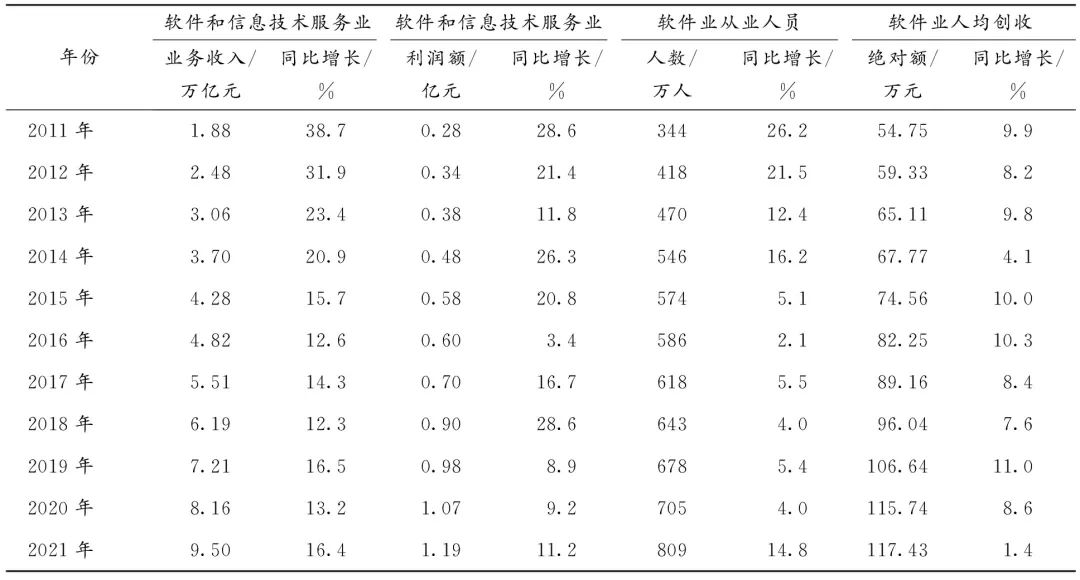

Table 1 Major Indicators of China’s Information Industry Development

Data Source: MIIT Official Website (https://www.miit.gov.cn/gxsj/index.html).

First, China’s software product revenue and information technology service revenue are on the rise. Between 2010 and 2020, important indicators reflecting the development of China’s information industry, such as software product revenue and information technology service revenue, have shown an upward trend, while revenue from embedded system software and software business exports has remained stable, not reflecting a growth trend. In 2020, the total number of software and information technology service enterprises above designated size in China was 40,300, with total business revenue of 8.16 trillion yuan, a year-on-year increase of 13.2%. The business revenue and profit of China’s software and information technology service industry continue to grow, but the year-on-year growth rate is declining, especially in 2019 and 2020, when profits saw a significant decline. Over the past decade, the absolute number of employees in China’s software industry has been increasing, but the year-on-year growth rate is declining; the absolute amount and growth rate of per capita revenue in the software industry are both on the rise. Overall, the operational status of China’s software and information technology service industry is good, with an expanded growth rate of embedded system software revenue, continued growth in software industry export business and profitability, and a continuous increase in the number of employees, with the scale constantly expanding.

Second, China’s telecommunications business revenue has grown rapidly, network supply capacity has continuously strengthened, and fixed asset investment growth has significantly accelerated. Over the past decade, China’s telecommunications business has developed rapidly, especially in fixed data, mobile data, and internet services, with good development conditions. Emerging digital services aimed at enterprises, such as cloud computing, big data, and data center services, have developed rapidly, and their contribution to the growth of telecommunications business revenue is continuously increasing. At the same time, the added value and profit of the electronic information manufacturing industry have grown rapidly. Against the backdrop of sustained global tightness in integrated circuit manufacturing capacity, China has made good investments in related fields, achieving significant growth in investments in semiconductor device equipment, electronic components, and electronic special materials manufacturing. In recent years, Chinese basic telecommunications enterprises have focused on building ubiquitous, integrated, cloud-edge collaborative networks to enhance cloud-network integration service capabilities. Data provided by MIIT shows that by the end of 2021, China had built and put into operation 1.425 million 5G base stations, establishing the world’s largest 5G network; 7.86 million 10G PON ports have been built, capable of covering 300 million households.

Third, the level of telecommunications industry development in China’s eastern region is high, while the level in the central and western regions is low. Statistics provided by MIIT indicate that in recent years, the software business revenue in the eastern region has accounted for 80.2% of the national total revenue, with some provinces and central cities with developed software industries further enhancing their strength, and the proportion of their information industry business revenue has further increased, with total profits also continuing to grow. In 2021, the top five provinces in software business revenue were Beijing, Guangdong, Jiangsu, Zhejiang, and Shandong, with these five provinces completing business revenue of 626.92 billion yuan, accounting for 66.0% of the national software industry revenue. At the same time, China’s internet business revenue has also shown a rapid growth trend in recent years, with operating profit growth maintaining double digits, although operating costs have risen significantly. China’s information services, audio and video services, and internet platform services have performed well in terms of total revenue and structure, with online sales and online services being very active. In addition, the level of internet access services and internet data services has continuously improved, with several provinces maintaining a rapid growth trend in internet business. The top five provinces with good development conditions for internet business in China are Beijing, Guangdong, Shanghai, Zhejiang, and Jiangsu, with internet business revenue growth rates of 29.6%, 9.3%, 31.1%, 13.0%, and 5.1%, respectively. Moreover, the comprehensive price of China’s telecommunications industry has been on a downward trend, playing a positive role in reducing the production and living costs of residents and promoting the development of the digital economy.

(2) Analysis of the Impact of the Digital Economy on China’s Information Industry

Data from the Ministry of Commerce shows that currently, the digital economies of the United States, Germany, and China are leading globally. In terms of development ideas, the United States emphasizes the free flow of data and opposes data localization; Germany focuses on data privacy protection and intellectual property protection; while China places more emphasis on governance of digital sovereignty. However, regardless of the focus, vigorously developing the digital economy has become a consensus among both developed and developing countries. It is certain that the digital economy will become a major trend in global industrial development in the future.

The development of the digital economy has brought opportunities and challenges to China’s information industry, while also exposing problems in meeting the requirements of digital economic development. To support the development of the digital economy, both the central and local governments have introduced policies to vigorously develop information infrastructure, blockchain, 5G technology, cloud computing, artificial intelligence, big data, and integrate them on a large scale into manufacturing, education, health, entertainment, logistics, and other industries, promoting various enterprises to move to the cloud. At the same time, various regions are also accelerating the construction or upgrading of digital infrastructure and information infrastructure, with broad prospects for the development of the information industry. However, China’s information industry faces urgent problems that need to be solved in the short term, manifested as: the underlying basic software and industrial software functions are not strong, lacking advancement and innovation, with a high degree of external dependence, especially in comparison to international advanced levels, there is still a significant gap in China’s industrial software, a weak foundation for technological innovation, a lack of high-end domestic products, a lack of independently developed products, weak driving force in software and industrial internet application scenarios, and an unclear role in promoting; the social atmosphere for software intellectual property protection has not yet fully formed, and in some areas, there are still “bottleneck” issues; there is still significant room for improvement in the construction of industrial internet, Internet of Things, and big data centers, as well as their applications in energy, steel, petrochemical, chemical, building materials, non-ferrous metals, and pharmaceuticals; new business formats and models such as intelligent manufacturing, network collaboration, personalized customization, digital manufacturing, and digital management have not been popularized, and their maturity needs to be improved; China’s new generation of information technologies, such as 5G, have not yet fully achieved cross-border integration, with high industry barriers between enterprises, and the application of “5G + industrial internet” faces technical challenges; some emerging technologies have inherent security issues, such as vulnerabilities and backdoors in cloud services and data centers, and the intensification of information services has exacerbated unknown security risks; compared to countries (regions) such as the United States, the European Union, and Japan, China’s electronic information technology, mid-to-high-end products, and brands are clearly at a disadvantage. While China’s information industry is large and has a complete range of products, the industry structure is imbalanced, with important industries not accounting for a high proportion, and some key information industries lacking core technologies, with abundant low-end industry products, while high-end products rely on imports; there is insufficient independent innovation capability, a lack of a batch of internationally competitive large enterprises, and a lack of core technology intellectual property, making it difficult to create brands with significant international influence in the face of technological barriers. These issues directly or indirectly affect the development of the digital economy.

3. The Current Situation of China’s Informatization Development in the Context of the Digital Economy

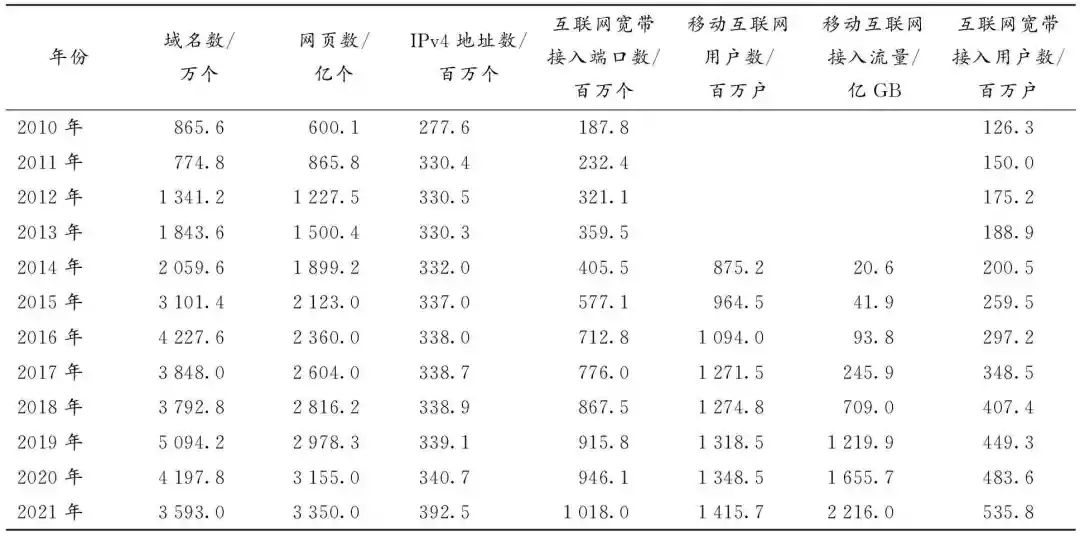

Informatization is a social historical process and an advanced productive force that cultivates and develops intelligent tools centered on computers and widely applies them in various fields of social economy, benefiting human society. National informatization refers to the overall planning and organization of informatization activities at the national level, continuously developing and deeply utilizing information resources, applying modern information technology in agriculture, industry, national defense, and various aspects of social life, promoting industrial upgrading, enhancing national competitiveness, and achieving national modernization. The important characteristics of informatization are an advanced and solid information industry foundation, full application of information technology, highly shared information resources, and a well-developed information network system, with various information resources, information systems, and public communication network platforms. Informatization construction includes the research and development of information technology, information equipment manufacturing, information consulting services, as well as enterprises’ investments and outputs in telephone communication, websites, e-commerce, customer information management, and product quality management systems. The main indicators reflecting a country’s informatization level include the number of domain names, the number of web pages, the number of internet broadband access ports, the number of mobile internet users, mobile internet access traffic, and the number of internet broadband access users. Table 2 lists the main indicators reflecting China’s informatization level.

Table 2 shows that in the past decade, the number of web pages, IPv4 addresses, internet broadband access ports, mobile internet users, mobile internet access traffic, and internet broadband access users have all shown an upward trend, reflecting the continuous improvement of China’s informatization development level from a macro perspective. The informatization development situation of important industries in China is as follows (see Figure 2).

Table 2 Major Indicators of China’s Informatization Development

Data Source: “China Statistical Yearbook 2021”.

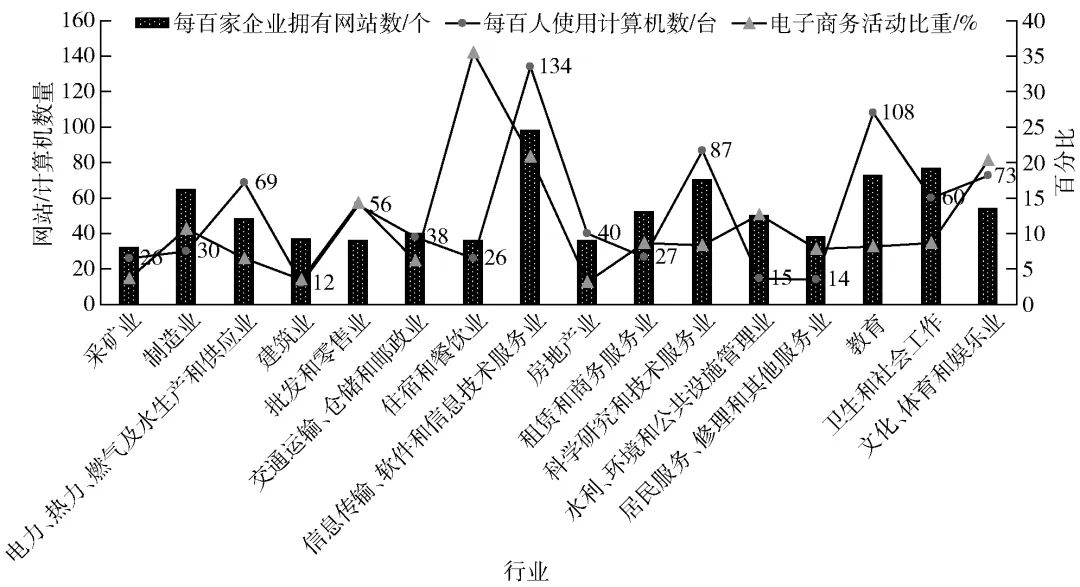

Figure 2 Informatization Development Situation of Important Industries in 2020

Note: Data source is “China Statistical Yearbook 2021”. The number of enterprises by industry is based on the survey results of “Informatization and E-commerce Application” for the year 2020. The proportion of e-commerce activities refers to the share of enterprises conducting e-commerce sales or e-commerce procurement through the internet among all enterprises.

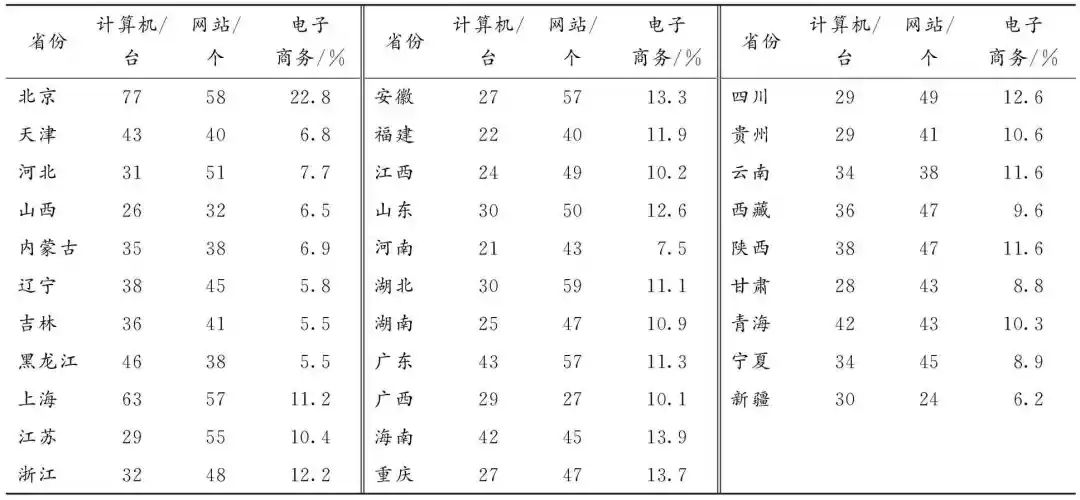

Figure 2 shows that the “information transmission, software and information technology service industry,” “mining industry,” and “manufacturing industry” are among the 16 industries with a high level of informatization in China. Among them, the industries with a higher number of websites per hundred enterprises are “accommodation and catering industry,” “information transmission, software and information technology service industry,” “scientific research and technical service industry,” “manufacturing industry,” “health and social work,” and “electricity, heat, gas, and water production and supply industry”; the industries with a higher proportion of e-commerce activities are “information transmission, software and information technology service industry,” “culture, sports and entertainment industry,” and “manufacturing industry”; the industries with a higher number of computer users per hundred people are “information transmission, software and information technology service industry,” “education,” “scientific research and technical service industry,” “electricity, heat, gas, and water production and supply industry,” “culture, sports and entertainment industry,” and “wholesale and retail industry.” Overall, the informatization level of the service industry is higher than that of the secondary industry. Furthermore, Table 3 lists the main analysis indicators reflecting the informatization development level of various provinces in China in 2020.

Table 3 Main Indicators of Informatization Development in Various Provinces in 2020

Note: Data source is “China Statistical Yearbook 2021”. The full name of “computer” in the table header is “number of computer users per hundred people”; the full name of “website” is “number of websites per hundred enterprises”; the full name of “e-commerce” is “proportion of e-commerce activities”.

It is not difficult to find that the provinces with a higher level of computer usage are Beijing, Shanghai, Heilongjiang, Tianjin, and Guangdong, while the provinces with a lower level of computer usage are Henan, Fujian, Jiangxi, Hunan, Shanxi, and Chongqing. Notably, Hainan, Qinghai, and Shaanxi also show good performance in terms of computer usage. The provinces with a higher level of website development are Hubei, Beijing, Shanghai, Anhui, Guangdong, Jiangsu, Hebei, and Shandong, while the provinces with a lower level of website development are Xinjiang, Guangxi, Shanxi, Yunnan, Heilongjiang, and Inner Mongolia. The provinces with outstanding performance in e-commerce trading activities are Beijing, Hainan, Chongqing, Anhui, Shandong, Sichuan, Zhejiang, and Fujian, while the provinces with weaker performance are Heilongjiang, Jilin, Liaoning, Xinjiang, Shanxi, Tianjin, and Inner Mongolia. Generally speaking, economically developed provinces also have higher informatization levels.

In addition to the aforementioned figures and tables, MIIT has provided digital data and related research reports that also reflect the performance of China’s informatization development in other aspects.

First, industrial software and the industrial internet are converging, and the big data industry is developing rapidly, creating new business models in the industrial internet field. Currently, industrial software and the industrial internet are merging, creating new business models in the industrial internet field, including digital management models, intelligent production models, networked collaboration models, personalized customization models, and service extension models. At present, China’s industrial software products are basically complete, with certain R&D capabilities and service support capabilities, effectively solving technical and management issues in the industry, and providing industry solutions to support the autonomous and controllable development of the industrial field. Meanwhile, China’s big data industry is developing rapidly, with widespread applications of big data. According to the “2021 China Big Data Industry Development White Paper” released by CCID in August 2021, as of August 31, 2021, China had completed the registration of 16,565 big data enterprises, with the three provinces with the most big data enterprises being Beijing, Guangdong, and Shanghai, with 3,531, 2,745, and 1,651 enterprises respectively, accounting for 47.9% of the national total. Big data enterprises are highly concentrated in three industries: information transmission, software, and information technology services. According to the classification of development maturity, 12,432 registered enterprises are in the high-quality development stage, and 4,133 enterprises are in the healthy development stage, with the number of enterprises in the high-quality development stage accounting for over 20%. In the development process of the big data industry, artificial intelligence (AI) technology has been integrated and applied, breaking through data governance bottlenecks, forming a data trading market, and achieving new practices in data pricing and data rights confirmation; projects such as “East Data West Computing,” “Industrial Big Data + Industrial Internet,” intelligent health management, cloud-based diagnosis and treatment, and data security governance have improved data service efficiency, playing a significant role in building a new industrial system that is green and low-carbon, enhancing work efficiency, and innovating work methods.

Second, the artificial intelligence industry is advancing overall, impacting all aspects of the economy and society. In April 2022, the China Academy of Information and Communications Technology released the “Artificial Intelligence White Paper (2022).” Data shows that in 2020, the market size of China’s core artificial intelligence industry exceeded 150 billion yuan, with its rapid growth mainly coming from the application of artificial intelligence technologies such as computer vision and natural language understanding, as well as the upgrading and popularization of artificial intelligence products such as smart speakers, intelligent customer service, and intelligent vehicle systems (smart connected vehicles). Over the past decade, algorithms, computing power, and data have all shown remarkable performance, with artificial intelligence technology transitioning from laboratory experiments to industrial applications on a large scale, and generative artificial intelligence technology becoming increasingly mature, deeply integrating with scientific research and continuously innovating traditional research paradigms. Currently, the field of artificial intelligence has given birth to ultra-large-scale training models, with a vast data scale continuously constructing integrated knowledge hotspots in the field. Artificial intelligence has been widely applied across various fields, affecting people’s daily production and life, with the focus of industrial development shifting from “artificial intelligence +” to “+ artificial intelligence,” with the processing and application scenarios of massive data becoming very common, and artificial intelligence profoundly impacting the digital transformation of traditional industries.

Third, the scale of industrial internet platform industries is expanding, and a public service platform system is taking shape. Currently, China is undergoing digital transformation in manufacturing and implementing intelligent manufacturing projects, with the vast majority of provinces, cities, and districts nationwide prioritizing the development of the industrial internet in their strategies. Data from the Ministry of Industry and Information Technology shows that by the end of 2021, there were over 2,400 projects under construction for “5G + industrial internet,” with the industrial internet industry scale exceeding one trillion yuan; nearly a thousand industrial internet platforms have been built, with 105 playing significant roles in industries and regions; a batch of specialized and characteristic platforms continue to emerge, and a multi-level systematic platform system has initially taken shape. Currently, China has basically established a national industrial internet big data center “1+N” system, with the industrial internet systems in important economic regions such as Beijing-Tianjin-Hebei, the Yangtze River Delta, and the Guangdong-Hong Kong-Macao Greater Bay Area having been laid out; an internet security system has initially taken shape, with monitoring covering 14 industrial sectors, 140 key platforms, and over 110,000 connected enterprises, and the functions of the security system are gradually improving. At the same time, China has over 1,800 projects under construction for “5G + industrial internet” in advanced manufacturing and traditional manufacturing fields such as equipment manufacturing, electronic device manufacturing, steel, and mining, creating thousands of innovative application cases for 5G. In the same year, China’s industrial software achieved revenue of 241.4 billion yuan, a year-on-year increase of 24.8%. The market scale of sensors is about 300 billion yuan, achieving an annual growth rate of nearly 18%, higher than the global average of 9.2%. The industrialization process of basic components is accelerating, with the industrialization of industrial 5G chips, modules, and terminal products continuously speeding up, and traditional modules and terminals evolving towards intelligence, supporting more advanced and complex applications. Currently, a relatively mature and well-established infrastructure for the industrial internet platform IaaS layer has been built nationwide, and the industrial internet data system has been completed; communication enterprises, industrial control enterprises, and large industrial manufacturing enterprises have widely applied public service platforms and achieved significant results; a number of demonstration bases for the information industry have been established nationwide, and a number of benchmark projects have been completed. Notably, the application of “5G + industrial internet” is strong and deep in key industries such as steel, chemicals, and building materials; specific fields such as “industrial internet + safety production” and “industrial internet + green low-carbon” have shown significant effects in integrated innovative applications.

Fourth, under the backdrop of the rapid development of big data and the digital economy, there are also shortcomings in China’s informatization development. Currently, the rapid development of the big data industry has raised higher requirements for China’s informatization. Overall, there are many problems in China’s informatization, manifested as: a lack of unified planning for informatization, with local governments, industries, and departments acting independently, and the construction system and operational mechanism being underdeveloped, with institutional and mechanism construction lagging behind, and significant disparities in informatization levels across different regions; there are vulnerabilities in informatization security, with some laws and regulations not adapting to the rapidly developing informatization reality, and the laws and regulations related to internet and information data security being incomplete and imperfect, with gray areas in information data and network security management, and regulatory measures needing to be improved in terms of standardization, institutionalization, and legalization; there are still technical challenges in information network security, information data security, and personal data protection, with the breadth and depth of advanced information technology applications needing to be improved; there is a digital divide in different regions, with a trend of widening; some regions emphasize the construction of information infrastructure while neglecting the popularization and application of information technology, especially the insufficient integration of information technology with digital technology and artificial intelligence technology, and the role of informatization in driving industrialization and promoting the development of artificial intelligence and the digital economy has not yet fully manifested, nor has informatization fully played its role in driving economic growth, transforming traditional industries, and promoting the development of advanced manufacturing and modern service industries, nor has its impact on energy conservation, resource protection, and achieving sustainable economic development been fully reflected.

4. Future Policy Considerations

The analysis of the current situation of China’s information industry and informatization provides a foundation for thinking about the development of informatization and the information industry. In the future, China needs to accelerate the construction of information industry and informatization infrastructure, enhance the energy efficiency of information industry products and equipment; break through technological bottlenecks in the industrial software sector, and accelerate software iteration, algorithm improvement, and technological upgrades; optimize the layout of the information industry, speed up the construction of information industry clusters to serve the development of the digital economy; strengthen international cooperation in information industry technology and capacity, and build a security guarantee system for information infrastructure.

(1) Accelerate the construction of information industry and informatization infrastructure, enhance the energy efficiency of information industry products and equipment

The research mentioned earlier shows that China’s information industry is developing rapidly, with a large product scale and fast business growth. However, there are shortcomings in the development of China’s information industry, such as the need to strengthen information industry infrastructure, and the efficiency of enterprise information products and equipment is not very high. Therefore, it is necessary to accelerate the construction of barrier-free information infrastructure, fully consider the layout of facilities such as optical cable lines and mobile base stations in urban roads, highways, and railways; accelerate the construction of high-speed optical fiber broadband networks, industrial internet, and industrial IoT, strengthen technological breakthroughs in basic hardware and software and key manufacturing processes, and build a 5G basic network with world-leading levels, covering the entire country, with excellent performance and efficient operation, forming a new type of infrastructure network that is fully digital and intelligent, corresponding to the functions of traditional infrastructure. It is necessary to appropriately build information infrastructure and major projects in advance, accelerate the upgrading and transformation of existing optical network access equipment, promote the upgrading of internal and external networks of enterprises, and expand the capacity of backbone networks to enhance the carrying capacity of backbone networks. It is necessary to strengthen the construction of data processing facilities, promote the diversification of data processing methods, strengthen the accounting management of data assets, establish data circulation and transmission planning and standards, and strive to eliminate the institutional barriers to data circulation. It is necessary to reduce the application costs and usage thresholds of information technology, lower the operating costs of information resources, leverage the advantages of information resources, achieve resource-intensive development, improve the efficiency of information resource utilization, and enhance the energy efficiency of information industry products and equipment.

In addition, the construction of informatization infrastructure should be planned in conjunction with the construction of artificial intelligence and digital technology infrastructure, reasonably layout new-generation supercomputing, cloud computing, and broadband infrastructure based on regional economic development needs and levels, and build an internationally leading infrastructure system driven by digital innovation, based on computing and information networks, and centered on computing power and algorithm facilities. It is necessary to increase efforts to digitally transform and empower backward traditional infrastructure, and proactively lay out key infrastructure such as 5G base stations, cloud computing centers, big data centers, and information technology centers to prepare for the deep application of advanced information technology and digital technology in the future.

(2) Break through technological bottlenecks in the industrial software sector, accelerate software iteration, algorithm improvement, and technological upgrades

China’s software industry has achieved significant achievements, but the industrial chain and supply chain of the software industry are fragile, with a weak industrial foundation and shortcomings in key core technologies, and the risk of breakage still exists, with software products positioned at the mid-to-low end of the value chain, and the international competitiveness of the software industry ecosystem is still weak. Therefore, it is necessary to strengthen original innovation and collaborative innovation in the software industry, and enhance the integration and application of software in various fields, especially in advanced manufacturing. From the perspective of national strategy, it is necessary to improve the industrial software industry and policy environment, increase investment in the software industry, lead industrial software innovation through industrial giants, promote the deep integration of software technology with the industrial field, and promote the research and development and promotion of new, high-end industrial software. It is necessary to strengthen the software capabilities of enterprises, fundamentally reverse the phenomenon of “heavy hardware and light software.” It is necessary to cultivate talents in software research and development and application, building a team of compound technical talents who are proficient in manufacturing design and software development. It is necessary to effectively protect software intellectual property, cultivate loyal enterprise users, and achieve important industrial software iteration, algorithm improvement, and continuous technological upgrades. It is necessary to strengthen the advantages of the national software industry chain, fill in the gaps, focus on improving service levels and quality, promote the continuous upgrading of the software industry chain, and enhance the international competitiveness of the software industry chain. It is necessary to strengthen the support level of the software industry, solidify the development foundation of common technologies and basic components in the software industry, build a good software industry database and resource library, and strengthen awareness of software quality and intellectual property. At the same time, it is necessary to organize technology alliances, strengthen collaborative technological breakthroughs in the industrial software industry, continuously enhance the technological research and development capabilities of industrial software, unleash the innovative vitality of “software-defined,” and form an autonomous and controllable software industry innovation system.

It is necessary to develop advanced software platforms and algorithms, eliminate unreasonable digital barriers, firmly grasp core technologies in big data, build a big data industry chain, promote the agglomeration development of the digital industry chain, support innovative demonstrations in the industry chain, and strengthen information enterprises and digital enterprises.

(3) Optimize the layout of the information industry, accelerate the construction of information industry clusters, and serve the development of the digital economy

At present, the distribution of information industry resources in China is uneven compared to other production resources, and there is significant heterogeneity in informatization levels across different regions, with information industry resources concentrated in developed eastern regions and lower informatization levels in western regions. Therefore, it is necessary to optimize the layout of the information industry and promote coordinated development of the information industry in the eastern, central, western, and northeastern regions. It is necessary to cultivate a batch of leading enterprises with strong innovation capabilities and brand influence, and rely on these leading enterprises to build a batch of information industry clusters with internationally leading standards. It is necessary to build and improve a series of industrial chains within the industry clusters, including industrial internet industry chains, information network industry chains, cloud computing industry chains, big data industry chains, and Internet of Things industry chains, promoting the transformation of information industry chains within clusters into industrial networks, enhancing the self-adaptive and self-repairing capabilities of the industrial chain, and improving the stability and competitiveness of the industrial chain. It is necessary to deeply promote the co-construction and sharing of 5G within information industry clusters, stimulate new demands for digital development, intensively utilize existing resources, guide the agglomeration of industrial resources, and promote different industrial clusters towards specialization and high-end development, pushing China’s information industry towards the mid-to-high end of the global value chain. It is necessary to promote demand-driven supply, strengthen the nature and status of information enterprises as market entities, establish and improve a shared ecosystem suitable for the healthy development of the information industry, and create an open and win-win environment for the development of the information industry that is synchronized with the international market.

Against the backdrop of global industrial division of labor and the development of the digital economy, it is necessary to accelerate the digital transformation of industrial parks, build centers to promote digital transformation; fully tap into international and domestic market resources, rapidly upgrade digital economy technologies through information industry clusters and information technology; leverage comparative advantages, promote the digital transformation of various enterprises supported by information technology, and effectively convert the opportunities brought by information technology and digital technology into tangible results and benefits; support small and medium-sized enterprises in information industry clusters to continuously explore and innovate, strengthen data security, avoid data monopolization by enterprises, achieve reasonable data sharing within information industry clusters, form a virtuous data sharing ecosystem, and promote the digital industrialization and industrial digitalization of information industry clusters.

(4) Strengthen international cooperation in information industry technology and capacity, and build a security guarantee system for information infrastructure

In the context of significant changes in global industrial layout, China’s information technology and industry development face increasingly fierce competition. Currently, the overall level of digitalization and informatization in China is not high, the overall process of digital transformation is slow, and certain important information technologies are still lagging behind, with a lack of high-level and high-quality information talents. Therefore, China needs to strengthen cooperation in technology, products, capacity, and talents in the information industry, and actively participate in the alignment of international rules for information technology. It is necessary to accelerate the construction of globally leading software technology parks, increase investment in national software parks, build a batch of national digital service export bases, and international information industry and digital trade ports, promoting international cooperation and innovation in information technology, information regulation, information standards, and rules, forming pathways for the orderly cross-border flow of data and digital security. It is necessary to promote the sharing of industrial big data among upstream and downstream enterprises in the information industry chain, build large-scale comprehensive platforms across industries and fields, characteristic platforms for key industries and regions, and cultivate specialized platforms for specific technology fields. In cities with developed information industries, it is necessary to promote the construction of international data centers, providing basic internet data center (IDC) services and cross-border data exchange services in a secure and orderly manner, and carry out cross-border data transactions, computing power leasing, and data processing services in regions where conditions permit. It is necessary to vigorously develop smart industries centered on the digital economy and develop high-end digital information industries. It is necessary to accelerate the layout of industrial internet platforms in information industry clusters, promote traditional enterprises to carry out digital and intelligent factory transformations, widely support enterprises to move to the cloud, continuously improve the total factor productivity of advanced manufacturing and strategic emerging industries, and enhance the informatization level of small and medium-sized enterprises.

At the same time, it is necessary to focus on the full life cycle management of big data, accelerate the construction of a big data security standardization system, and carry out international cooperation in the research and formulation of big data security standards, constructing a big data security standard system framework from multiple dimensions, including basic principles, information digital technology, platform data security, data service security, and information digital industry applications. It is necessary to focus on the collection, storage, transmission, use, opening, and privacy protection of big data, strengthen the basic construction and operational monitoring of communication networks within information industry clusters, forming a solid and reliable security guarantee system for information infrastructure, ensuring the secure storage and use of data, creating a data security ecosystem, and forming a data security community.

Journal submission website: http://btbuskxb.ijournals.cn

Consultation phone: 010-68984614, 010-68986079

Journal domain publication invitation code: tg3666

Journal WeChat account: btbuxb

This journal implements an anonymous peer review system, does not charge any fees such as publication fees or review fees, and pays authors corresponding remuneration according to regulations.

Image source: Author

Article content: Author

Editing and typesetting: Journal of Beijing Technology and Business University

Click the blue text to read the original text