Keywords: Display Chip, LCD Driver, TDDI, LED Display Driver, Large Size Display Driver, OLED Display Driver, Display Power Management

After decades of hard work, China’s display industry has rapidly developed under the support of national policies, funding, and technology, becoming the world’s largest panel manufacturing hub. According to data from Qunzhi Consulting, in 2020, China’s panel manufacturers shipped 54.7% of the global share. This figure is expected to continue to grow, with hopes of setting new records.

The production capacity of panel manufacturers presents a massive demand for chip supply, especially for display driver chips. According to Omdia data, the total demand for display driver chips in 2020 saw a double-digit year-on-year growth, reaching 8.07 billion units, expected to increase to 8.4 billion units in 2021. However, facing such enormous demand for display driver chips, chip manufacturers in mainland China hold a very low global market share, with a self-sufficiency rate of only about 5%.

The domestic panel and display chip industries, which should be on par with each other, are currently facing an awkward situation of “limping along”. In the past year, as the global chip capacity shortage has become increasingly severe, the shortage of display chips has begun to restrict the development of the entire downstream panel industry.

To completely resolve the “limping” situation and ensure the coordinated development of the panel and chip industries with proper capacity matching, panel manufacturers have begun to deeply bind with chip design companies for collaborative innovation. For example, BOE has invested in Yiswei, founded by its former chairman Wang Dongsheng; Huaxing Optoelectronics and BOE have both invested in Chipone; various signs indicate that panel manufacturers’ willingness to support local display driver chip companies is becoming stronger, and the panel industry’s role in promoting the development of the chip industry is beginning to show. The growth of the chip industry will also feed back into the panel industry, forming a virtuous cycle. Domestic display-related chip manufacturers are expected to seize historic opportunities for domestic substitution with the support of the upstream and downstream industrial chains and national policies.

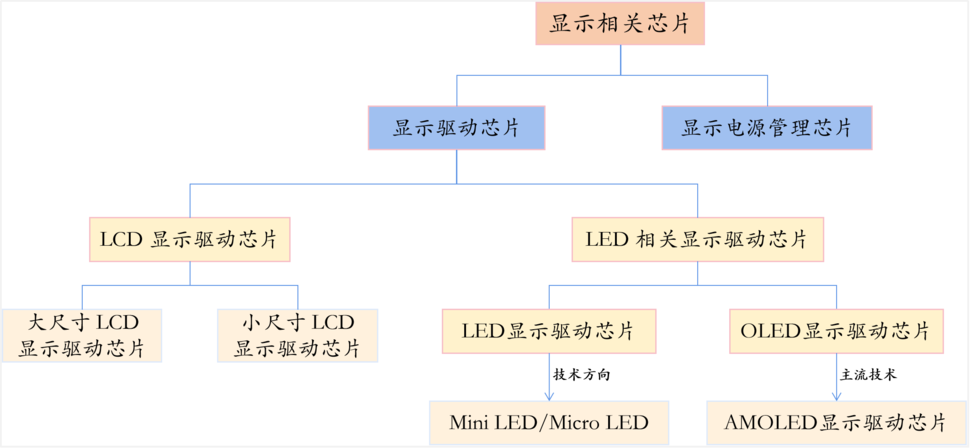

Display Driver Chips

Display chips mainly consist of two categories: display driver chips and display power management chips. Display driver chips are further subdivided into the markets for LCD and LED screens, including large size LCD and the latest technology paths in recent years, such as OLED and Mini LED.

Domestic Substitution of LCD Display Driver Chips is on the Rise

LCD display driver chips are further divided based on the size of the terminal screen into large size LCD display driver chips and small size LCD display driver chips.

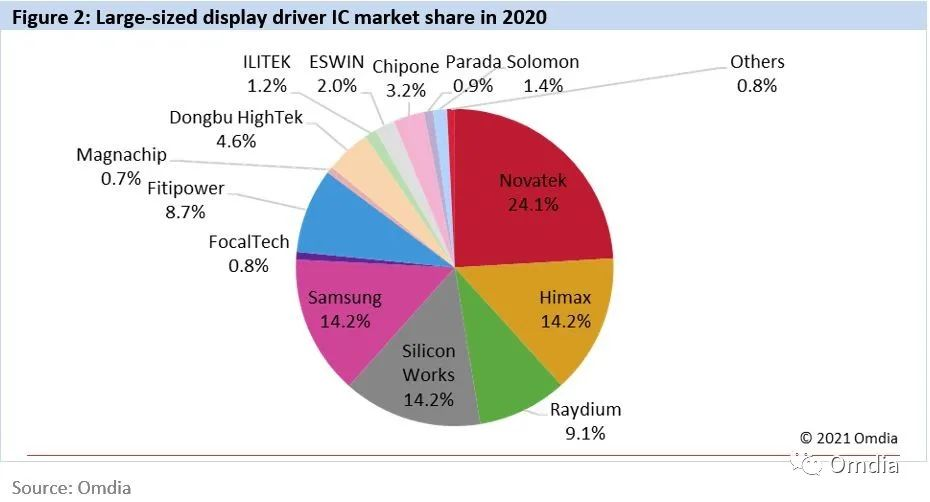

Large Size LCD Display Driver Chips are mainly used for the display driving of televisions, laptops, and some monitoring screens and automotive electronic displays. Suppliers are primarily foreign companies, with the top seven manufacturers being Taiwanese or Korean enterprises, holding a CR7 (concentration of the top seven) of about 90%, indicating high market concentration. Novatek holds the largest market share at about 24%, followed by Himax and Korea’s Samsung LSI and Silicon Works.

Among the top ten companies in the global large size display driver chip market, only two are mainland companies, with a combined market share of 5.2%. Chipone holds a market share of 3.2%, while Yiswei holds 2%. As Chipone’s large size LCD display driver chip products gradually cover almost all downstream leading panel manufacturers, the market share of domestic manufacturers is expected to continue to grow, accelerating the domestic substitution process for large size LCD display driver chips.

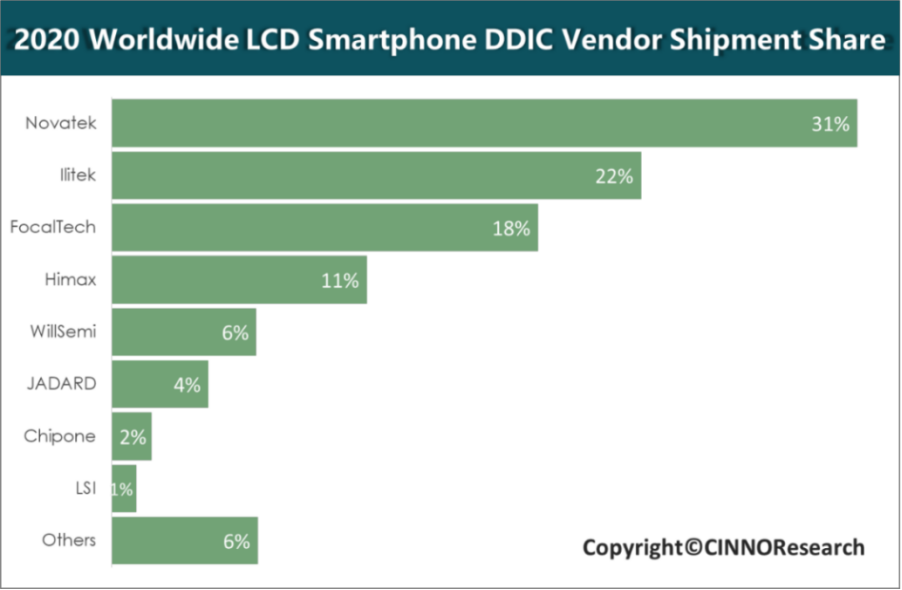

Small Size LCD Display Driver Chips are primarily used in smartphones. In 2020, Novatek ranked first in global smartphone LCD driver chip shipments with a market share of 31%, followed by Ilitek, FocalTech, Himax, WillSemi, JADARD, Chipone, and Samsung System LSI. Mainland Chinese companies hold over 12% of the global smartphone LCD display driver chip market share.

In the small size panel fields such as smartphones and tablets, the trend towards integration of display driver chips with touch control chips (TDDI) is irreversible, with penetration rates exceeding 50% in the smartphone sector and over 40% in the tablet sector. Since TDDI requires mastery of both display and touch chip technologies, the technical barriers are high. Currently, only two domestic companies have entered the top ten.

In 2020, the mainland company WillSemi acquired Synaptics’ TDDI business in Asia for $120 million, officially entering the display driver chip market. In 2020, it held a 6% market share in the smartphone LCD driver chip market, ranking fifth.

Chipone is the leading domestic display chip enterprise, being the only company in China to independently develop and mass-produce TDDI chips. In 2020, Chipone held nearly a 2% market share in the smartphone LCD driver chip market, ranking seventh. Since November 2020, Chipone has begun mass production of TDDI for Xiaomi, and this product has reportedly entered the HMOV (Huawei, Xiaomi, OPPO, VIVO) supply chain, with expectations of rapid market share growth in the future.

LED Display Driver Chip Landscape is Stable, Stronger Players Prevail

Traditional LED display driver chips are already very mature products, with the industry mainly relying on the gradual implementation of emerging applications such as small-pitch LED, Mini LED, and Micro LED to drive rapid market growth.

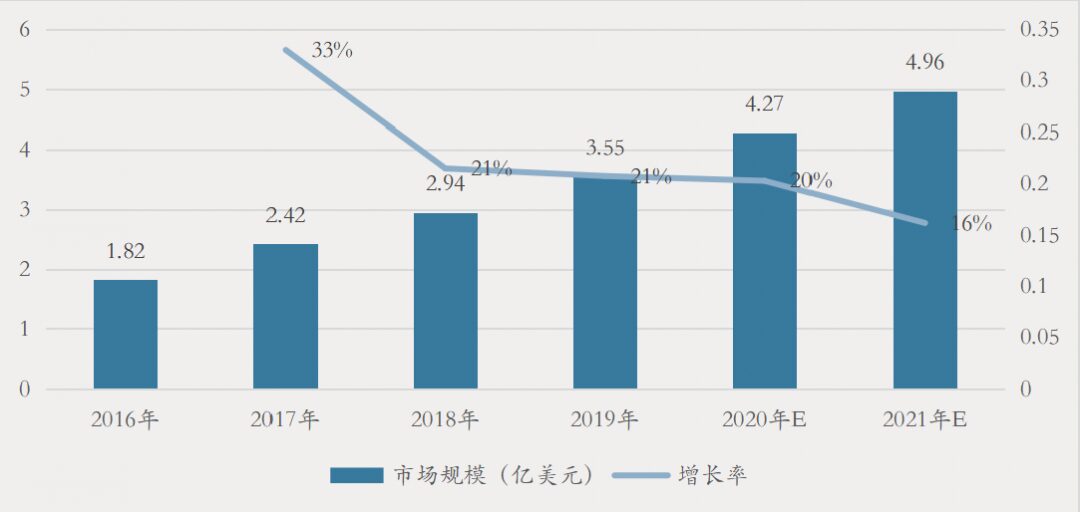

According to statistics from LED inside, the global LED display driver chip market size was $427 million in 2020, and is expected to reach $496 million in 2021, representing a 16% year-on-year growth.

Chart: Global LED Display Driver Chip Market Size

Data Source: LED inside “2019 Global LED Display Market Outlook”

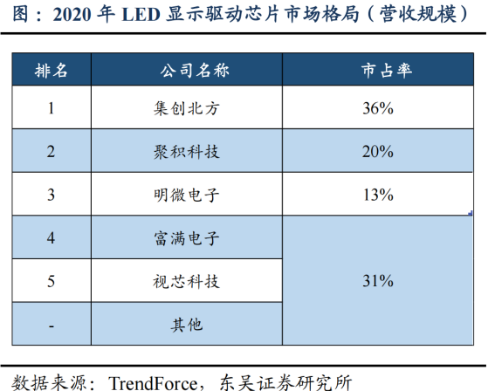

The global LED display driver chip market is highly concentrated, with the top five manufacturers accounting for over 75%. Currently, Chipone has replaced Novatek as the largest LED display driver chip supplier globally, holding a 36% market share.

With the implementation of small-pitch LED and Mini LED applications, it is evident that this year not only have upstream display driver chip manufacturers like Chipone and Mingwei Electronics experienced significant performance growth, but downstream companies like Jufei Optoelectronics in the mini LED backlight module sector have also seen considerable growth. It is expected that Chipone will further increase its market share in global LED display driver chips to 40%, with industry concentration continuing to rise.

OLED/AMOLED Display Driver Chips Have Broad Prospects

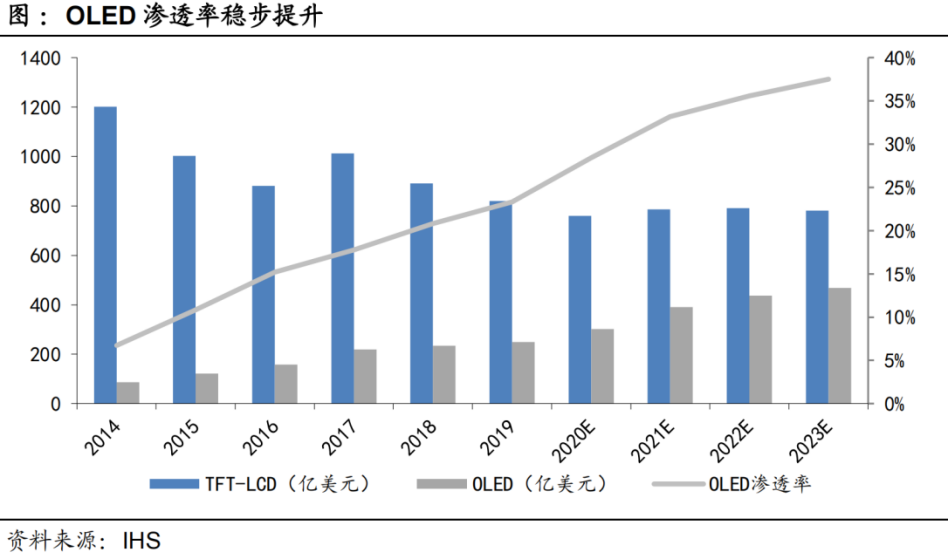

As the penetration rate of OLED panels in smartphones gradually increases, it is expected that the global OLED display driver chip market will grow from $1.764 billion in 2019 to $2.107 billion in 2021.

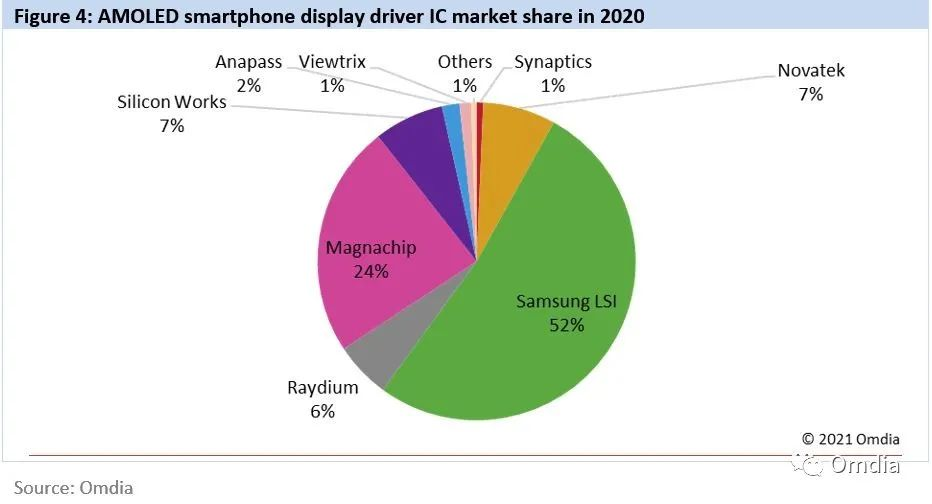

Currently, 80% of the global OLED display driver chip market is occupied by Korean companies, with the remaining significant shares held mainly by Taiwanese manufacturers.

Domestic manufacturers have achieved breakthroughs in technology in the smartphone OLED display driver chip market, with Yunyinggu Technology achieving a 1% market share in 2020. Chipone‘s affiliate Oled has recently received investments from Huawei Hubble and several state-owned funds. Its AMOLED products have entered mass production. Zhongying Electronics has also achieved mass production of AMOLED driver ICs. The above three companies have become some of the few domestic enterprises to achieve technological breakthroughs in this field.

There is Huge Potential for Domestic Substitution in Panel Power Management Chips

Power management chips are the most widely used category in semiconductors, extensively applied in home appliances, smartphones and tablets, chargers and adapters, smart meters, lighting, communication devices, industrial control equipment, and more. Power management chips are essential in power supply systems, as they convert, distribute, detect, and manage electrical energy in electronic systems. If they fail, it can cause the electronic devices to stop working, hence they are referred to as the “heart” of electronic devices. Without power management chips, almost all electronic products in daily life cannot function properly.

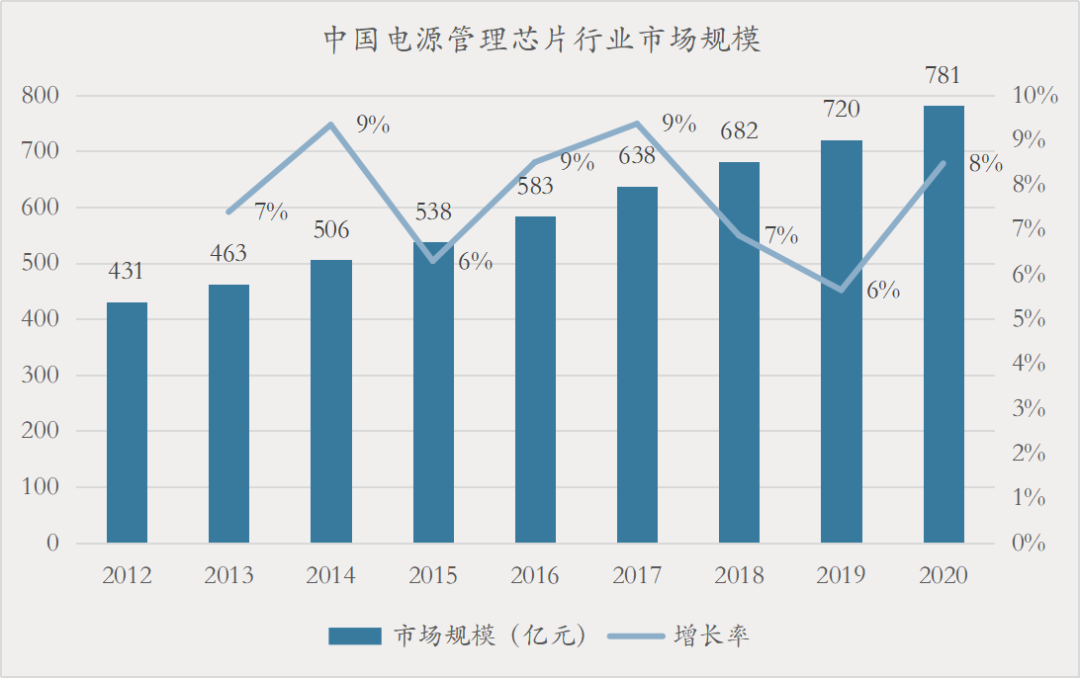

In 2020, the global power management chip industry market size was approximately $30 billion, with the domestic market size around 78.1 billion yuan, accounting for about 40% of global market demand, making it the largest single market globally.

Chart: Market Size of China’s Power Management Chip Industry

Data Source: CCID Consulting, China Business Industry Research Institute

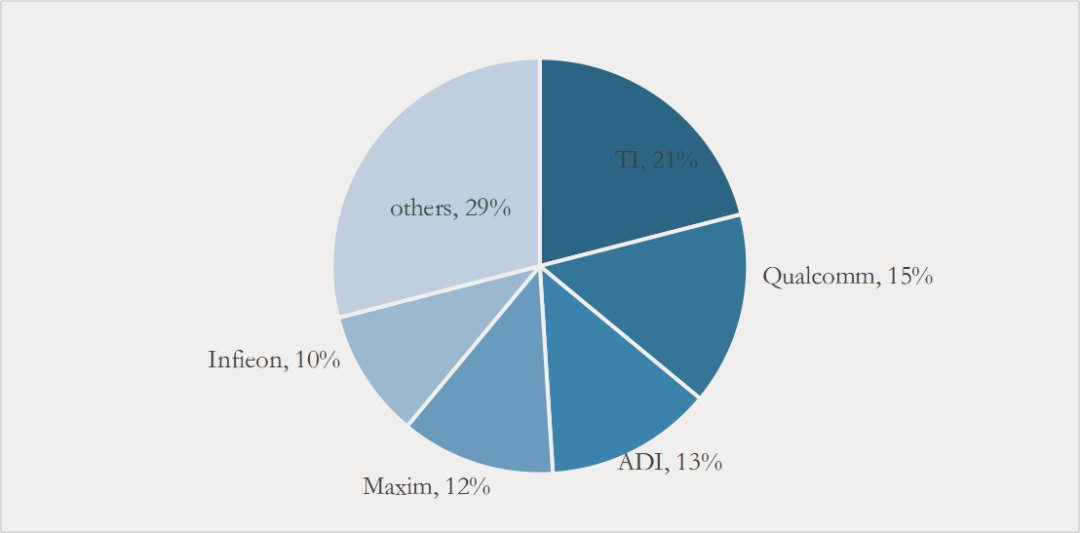

The power management chip industry market is highly concentrated, with the top five global manufacturers accounting for about 71% of the global market share, and these five manufacturers monopolize over 90% of the domestic market share, with a self-sufficiency rate of only about 5% in the domestic market.

Chart: Top Five Global Power Management Manufacturers

Data Source: Qianzhan Industry Research Institute

Domestic listed companies have a wide range of applications for power management chip products, but almost all are applied outside the panel sector, with only Shengbang Technology having some products related to AMOLED displays.

The leading domestic display chip company, Chipone, focuses its power management chips solely on panel applications, with clients including BOE, Huaxing Optoelectronics, and other leading panel manufacturers, which does not constitute direct competition with domestic listed companies, making it the top supplier of panel power management chips in the country. In the panel power sector, the market space exceeds $1 billion, which is almost entirely occupied by foreign manufacturers, offering significant potential for domestic substitution.

Chart: Major Domestic Power Management Manufacturers

Domestic Chip Enterprises

Domestic manufacturers have achieved technological breakthroughs and even surpassed in various fields of display chips, while domestic downstream panel companies have grown into global leaders in the panel sector, creating an urgent demand for supply chain security. Under the guidance of national policies, support from downstream panel manufacturers, and collaborative innovation across the industry chain, the trend of domestic substitution in the display chip sector is clear..

We believe that in the field of LED display chips, domestic companies will expand their competitive advantages and initiate internationalization steps, leading continuous technological innovations in Mini LED and Micro LED to capture overseas markets and further increase market concentration; in the LCD display chip and power management sectors, domestic leading companies have entered the supply chain of top-tier international panel manufacturers. With product performance and price advantages, rapid response to local LCD panel customer needs, and deep binding and collaborative innovation between the upstream and downstream of the industry chain, they will accelerate the domestic substitution process; in the OLED display chip sector, domestic manufacturers are in a stage of striving to catch up and gradually achieving technological breakthroughs, entering panel and smartphone manufacturers’ supply chains through wearable devices. In the short term, there will be a small-scale growth trend. In the future, it is expected that as domestic OLED panel manufacturers improve yield rates and dominate global production capacity in the next 2-3 years, the domestic substitution of OLED display driver chips will enter a period of explosive growth.

Listed Companies

Mingwei Electronics (688699)

Founded in 2003, with a market value of 21.5 billion yuan. Focused on the research and development of LED display/lighting drivers, LED smart landscape drivers, and power management chips. The company has achieved mass production of Mini LED driver chips, with approximately 70% of revenue in 2020 coming from LED display driver products.

Fuman Electronics (300671)

Founded in 2001, with a market value of 25.5 billion yuan. Main products include power management chips, LED control and driver chips, MOSFETs, RF front-end chips, etc. The company had approximately 836 million yuan in revenue in 2020, with 60% of revenue coming from LED control and driver chips.

Shengbang Technology (300661)

Founded in 2007, with a market value of 78.4 billion yuan. A leading company in the domestic power management chip field. The company’s products cover two major areas: signal chain and power management, with over 1,000 models across 16 series. The company had approximately 1.2 billion yuan in revenue in 2020, with over 70% of revenue coming from power management products, and some products related to AMOLED display power management chips.

Jingfeng Mingyuan (688368)

Founded in 2008, with a market value of 26.6 billion yuan. Products include motor control/driver chips, smart power modules, AC/DC and DC/DC power chips. The company is a leader in general LED lighting and smart lighting driver chips, with approximately 1.1 billion yuan in revenue in 2020, with over 90% of revenue coming from LED lighting driver products.

Xinpeng Microelectronics (688508)

Founded in 2005, with a market value of 16.7 billion yuan. A leading company in the domestic power management chip sector for small household appliances, highly recognized by domestic first-tier appliance manufacturers like Midea and Gree. The company had approximately 400 million yuan in revenue in 2020, with over 90% of revenue coming from power management chips, and over 40% from appliance-related chips.

Zhongying Electronics (300327)

Founded in 1994, with a market value of 20.1 billion yuan. Focused on MCU and lithium battery management chip design, began developing AMOLED driver chips in 2011, and has achieved mass production. The company had approximately 1 billion yuan in revenue in 2020, with AMOLED display driver chip revenue accounting for about 6%.

Weier Technology (603501)

Founded in 2007, with a market value of 241.1 billion yuan. A global leader in CIS chips, gradually expanding into discrete devices, RF chips, and analog chips. In 2020, the company officially entered the TDDI chip market through acquisition, with TDDI product revenue of about 700 million yuan, accounting for around 4% of total revenue.

Note: Market value data is as of August 11, 2021.

Unlisted Companies

Chipone

Founded in 2008, it is the leading display chip enterprise in mainland China, with products including display driver chips (LCD, LED/Mini LED, and OLED display driver chips), power management chips, fingerprint recognition chips, touch chips, etc. It has the most complete product line in the display field and has proactively laid out next-generation display technologies such as silicon-based OLED and Micro LED, covering almost all leading enterprises in downstream niche fields.

Yunyinggu Technology

Founded in 2012, focusing on display technology research and development, IP licensing, and display driver chips/circuit boards as core businesses. The company’s chips can improve the resolution and clarity of amorphous silicon liquid crystal panels based on existing production lines. This technology can be directly applied to various display carriers such as LCD, LED, OLED, and flexible display materials, widely used in products like smartphones, PDAs, and digital cameras, and can also be extended to projectors and televisions. The company has received investments from well-known industry institutions such as Xiaomi Technology, BOE, Aurora Venture Capital, CICC Capital, and Huawei Hubble.

Oled Microelectronics

Founded in 2019, focusing on the research and design of AMOLED display driver chips, currently achieving mass production. The company is under the same actual controller as Chipone, and has received investments from well-known institutions such as Beijing Yizhuang Guotou and Wuyuefeng Venture Capital, and in August of this year, it introduced Huawei Hubble as the second largest shareholder.

Qingfeng Capital is a private equity investment institution focusing on hard technology fields such as semiconductors and life sciences. With the mission of “industry accumulation, value excavation,” we are committed to discovering and cultivating quality enterprises!