Click the blue text to follow us

This report consists of 47 pages and has been uploaded to the 【Semiconductor Industry Research】 knowledge platform. If you need to obtain the high-definition complete PDF version, please check the download method at the end of the article. Below are some key content highlights.

Table of Contents

1. From ECU to SoC Chips: The Evolution of Automotive Computing Chips

1.1 Development of Automotive Intelligence and Evolution of Computing Chips

1.2 The Rise of SoC Chips: Opening a New Era of Intelligent System Integration

1.3 Increasing Importance: OEMs Accelerate Upstream Integration

2. Intelligent Cockpits, Intelligent Driving, and Autonomous Driving Lead Automotive Evolution, SoC Chip Demand Explodes

2.1 Competitive User-Perceived Areas in Automobiles: Increasing Requirements for Intelligent Cockpit SoC Chips

2.2 End-to-End + Equal Rights in Intelligent Driving: Full Force of Intelligent Driving SoCs

2.3 High-Level Autonomous Driving Gains Momentum: Expansion of the SoC Chip Market

3. Market Concentration: Domestic Substitution Gains Traction, Favoring Leading Domestic Enterprises to Continue Breaking Through with Industry Trends

3.1 Integration and Large Model Overlap: Accelerating Domestic Production of Cockpit SoCs

3.2 End-to-End and Equal Rights in Intelligent Driving: Improving Quality and Expanding Quantity of Intelligent Driving SoC Chips

3.3 Introduction of Major Domestic Brand Automotive SoC Chip Companies

From ECU to SoC Chips: The Evolution of Automotive Computing Chips

With the entry of new energy vehicles into the competitive second half, the empowerment of intelligence and the development towards the era of autonomous driving have become the main direction for the development of electric intelligent vehicles.

Driven by the deepening of intelligence, a large number of components have become electronic, with intelligent cockpits and intelligent driving being widely applied. “Software-defined vehicles” have become a trend. Since the 1980s, the gradually installed distributed electronic control units (ECUs) have increasingly failed to meet the development needs of intelligent vehicles, prompting an urgent upgrade of the automotive electronic and electrical (EE) architecture.

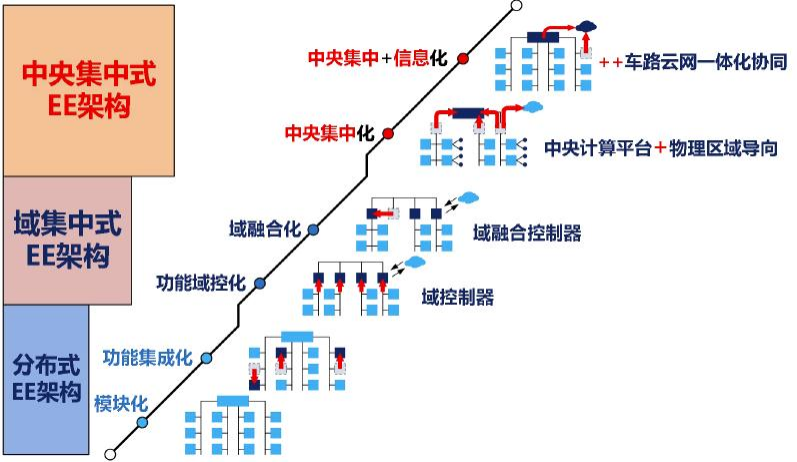

The evolution of automotive electronic and electrical architecture shows that while major manufacturers have detailed differences in planning, the overall trend is evolving from distributed to domain control, then to domain integration and central control, ultimately leading to a development trend combining cloud control.

Figure: Development Route of Automotive EEA from Distributed to Centralized + Informational

From the evolution route of the EEA architecture, the current automotive electronic and electrical architecture is evolving from domain control to domain integration, gradually exploring the development stage of central control.

Major domestic and foreign automotive companies are all moving towards domain control architecture. From the perspective of intelligent driving and controllers, the penetration rate reached 24% by April 2025, indicating that the industry is entering a growth phase.

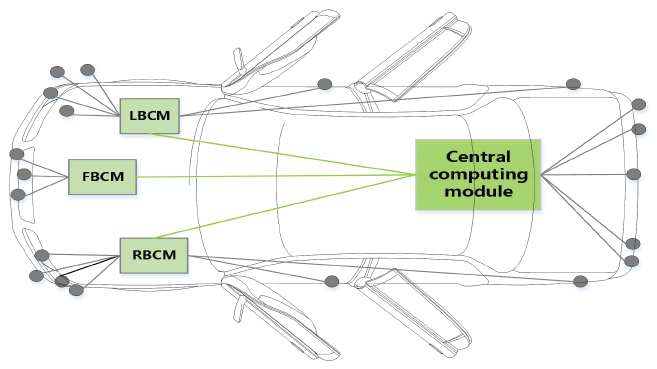

From the technical situations of different companies, Tesla’s MODEL 3 uses a combination of central computers and regional controllers (left L, right R, front F), while other major domestic and foreign automotive companies continue to develop based on functional domains and promote cross-domain integration.

Whether central control, regional control, or domain control, the integration and complexity of controllers have significantly increased. Traditional ECUs (Electronic Control Units) can no longer meet the demands of in-vehicle applications, making SoC chips a crucial foundation for the development of intelligent vehicles.

Figure: Schematic Diagram of Tesla Model 3’s Electronic and Electrical Architecture

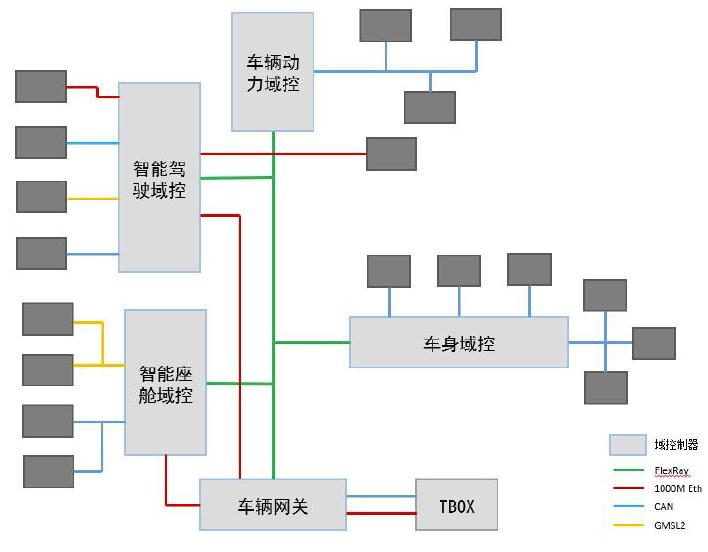

Figure: Schematic Diagram of Zeekr Automotive’s Electronic and Electrical Architecture

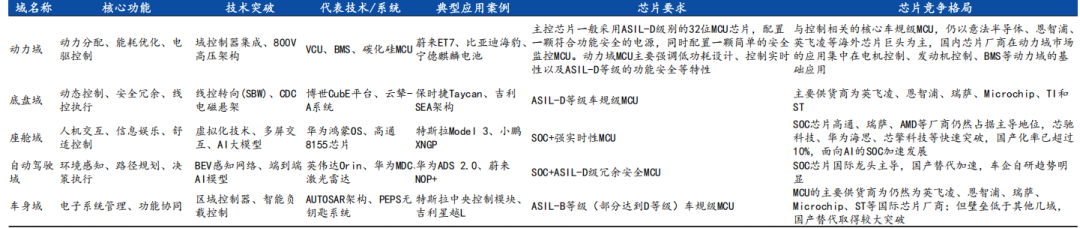

In terms of the commonly used functional domain distribution, after module centralization, intelligent connected vehicles are mainly divided into five domains: power domain, chassis domain, cockpit domain, autonomous driving domain, and body domain. The power domain is mainly responsible for managing the powertrain, including the engine management system (EMS) and transmission control module (TCM) for traditional vehicles, as well as the vehicle controller (VCU), motor controller (MCU), and battery management system (BMS) for new energy vehicles. Due to low computing power requirements but high safety requirements, the main control chip is generally an ASIL-D level 32-bit MCU (Microcontroller Unit) chip.

The chassis domain is the core of vehicle dynamic control, covering four subsystems: steering, suspension, braking, and transmission, and accelerating the transformation towards deep collaboration in line control, steering, and active suspension. Due to the same high safety scenario, the main control chip is still primarily ASIL-D level MCUs.

The body domain is mainly responsible for integrating and managing the vehicle’s electronic systems. Its core modules include lighting systems (high/low beam, turn signals, ambient lights, etc.), door and window control systems (windows, sunroofs, electric tailgates), wiper and washing systems, heating and ventilation modules (seat/steering wheel heating), and body safety and anti-theft systems (PEPS, collision signal triggers). Due to the rich scenarios, the basic requirement is ASIL-B level, with some reaching ASIL-D (when integrated with VCU) level, with the main control chip being MCU-based.

The cockpit domain and the newly added autonomous driving domain are the core battlegrounds for SoC chips. The cockpit domain focuses on centralized control of the in-cabin environment, including human-machine interaction, infotainment, and comfort, with high information processing density and some high safety requirements. The main control chip consists of SoC + MCU; the autonomous driving domain covers the integration and control of vehicle perception, decision-making, and execution systems, requiring both high computing power and high safety. The domain controller computing platform uses SoC chips + redundant safety MCUs. In the current environment, cockpit and driving integration and central control are accelerating, and SoC chips are evolving in that direction.

Table: Technical Analysis of the Five Domains under Domain Architecture

SoC chips (System on Chip) are system-level chips, which are highly integrated semiconductor products that integrate all components required for a complete electronic system onto a single chip. Typically, they include processor cores, memory, digital signal processors, communication modules, and power management units. This integrated design breaks through the limitations of traditional multi-chip discrete architectures, forming a complete system on a chip that can independently run operating systems and perform complex tasks.

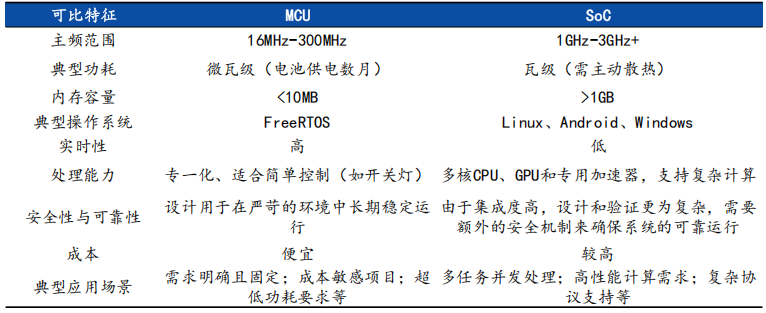

Traditional MCUs are known as “microcontrollers,” which are integrated circuits that include a processor core (usually a microprocessor), memory (such as flash and RAM), and input/output (I/O) interfaces. Compared to MCUs, SoC chips integrate more heterogeneous processing units internally, have a more complex structural design, and possess stronger processing and computing capabilities. Their high performance, low power consumption, small size, and high reliability make them suitable for multitasking and more complex computational tasks, such as advanced driver assistance systems, autonomous driving, and in-vehicle infotainment systems.

From a layman’s perspective, the design philosophy of SoC is “All in one,” which is a super platform for system integration, characterized by multi-core heterogeneous computing, large-capacity storage support, and complex functional modules; while the design philosophy of MCU is “Simplicity First,” which is an expert in executing single tasks, characterized by a single-core CPU, only basic storage units, and necessary peripheral interfaces. Typically, MCUs are used for real-time tasks and directly control hardware; while SoCs run complete operating systems and handle complex algorithms such as image recognition, voice interaction, and autonomous driving.

Therefore, in intelligent cockpits and intelligent driving, SoCs and MCUs often coexist in a collaborative manner. For example, in autonomous driving, MCUs are responsible for executing real-time control and high-reliability tasks such as engine control, steering control, and braking control, while managing in-vehicle communication; SoCs are used to support parallel computing and complex algorithms, processing multi-sensor perception data, and performing motion control. Due to the high complexity, additional mechanisms are often required to ensure safety. Therefore, intelligent driving domain controllers often have MCUs responsible for safety redundancy.

Table: Comparison of Main Features between MCU and SoC

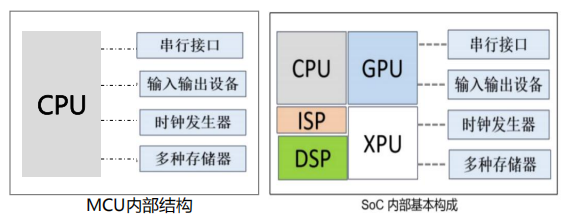

From the internal structure perspective, MCUs integrate processors, memory, input/output interfaces, and other peripherals; SoC chips are system-level chips that, compared to MCUs, integrate more heterogeneous processing units, have a more complex structural design, and possess stronger processing and computing capabilities. From a hardware structure perspective, automotive SoC chips typically also consist of processors, memory, and peripheral I/O, but are more complex than MCUs.

From a practical application perspective, the performance evaluation of SoC chips mainly includes: PU computing power, manufacturing cost, energy efficiency, thermal management capability, interface support, and safety.

Figure: Comparison of Internal Structures of MCU and SoC

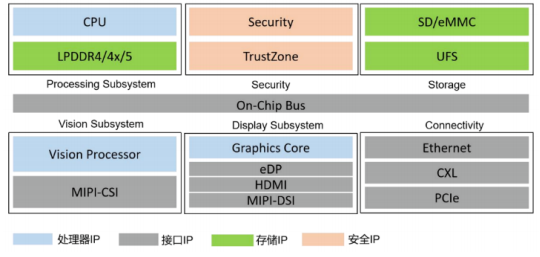

Figure: SoC Chip Architecture

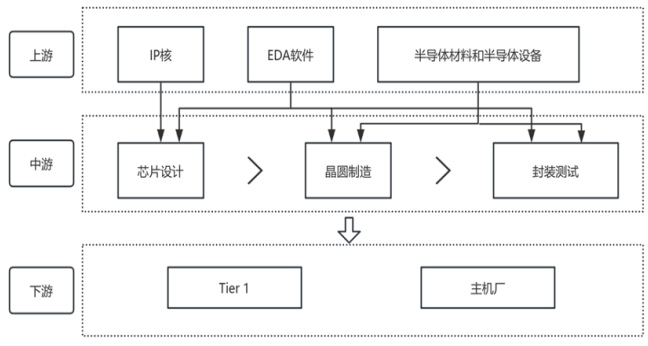

The upstream of the SoC chip industry chain mainly includes IP core licensing, EDA (Electronic Design Automation) software, and other design tool manufacturers, as well as semiconductor materials and equipment. Among them, IP core licensing and EDA software and other design tool manufacturers empower chip design companies, helping them accelerate the chip development cycle and time to market. Semiconductor materials and equipment manufacturers provide the basic materials and advanced equipment for chip manufacturing, ensuring high efficiency and quality in chip production.The midstream of the SoC chip industry includes three main links: chip design, chip manufacturing, and packaging testing. Some companies have vertically integrated, covering all links, while others only participate in one link. Depending on the included links, these semiconductor companies’ business models are generally divided into vertical integration models (IDM model), wafer foundry models (Foundry model), and fabless models (Fabless model).Tier 1 and automotive companies belong to the downstream of chip design companies. In the past industrial chain model, the entire supply chain was linear, with chip design companies as Tier 2, having close contact and cooperation with Tier 1, and little interaction with automotive companies. However, many automotive companies now actively seek communication and cooperation with leading chip companies to jointly research user needs and customize chips suitable for their own needs. This cooperation model not only helps enhance the competitiveness of automotive companies’ products but also ensures the stability of chip supply.

Figure: Structure of the SoC Chip Industry Chain

Figure: Major Enterprises in the Upstream of the SoC Chip Industry Chain

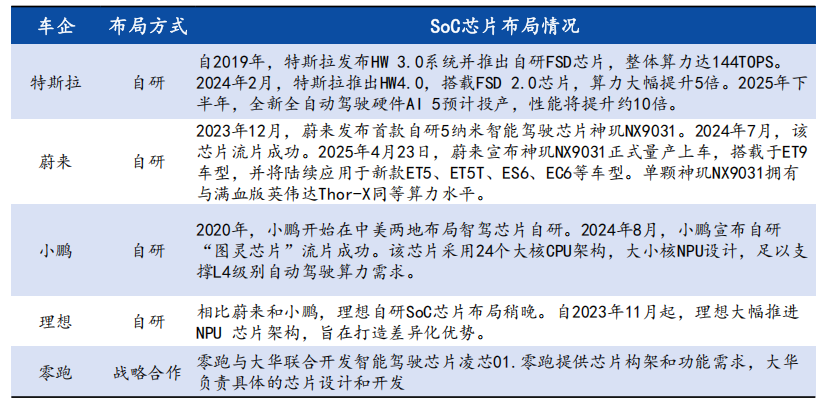

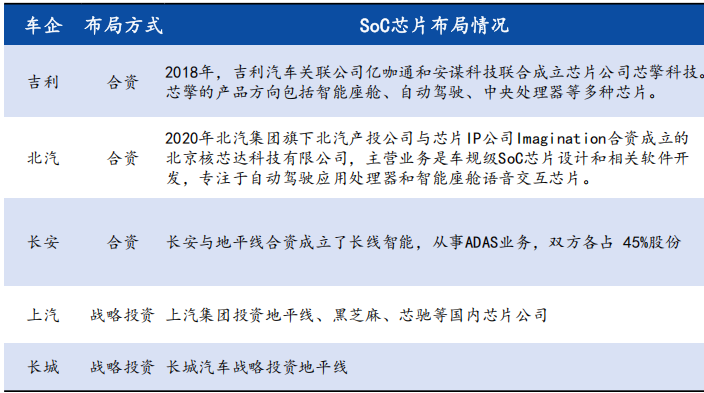

Currently, mainstream automotive companies are actively laying out the automotive SoC chip track. The layout methods of various automotive companies are not entirely the same, and some companies may even use multiple models simultaneously. The layout methods can be roughly divided into the following four types: self-research, joint ventures, strategic investments, and strategic cooperation.√ Self-Research Model: Currently, new force automotive companies represented by Tesla, NIO, Xiaopeng, and Li Auto mainly focus on self-research of SoC chips in the intelligent driving field, forming teams for chip design and development. Few automotive companies are self-developing intelligent cockpit SoC chips.√ Joint Venture Model: Automotive companies establish joint ventures with chip companies to integrate resources from both sides, accelerating the chip development process and enhancing product competitiveness.√ Strategic Cooperation: Automotive companies engage in deep strategic cooperation with chip manufacturers, where automotive companies provide requirements and architecture, and chip manufacturers complete design and development. This model allows automotive companies to customize chips that meet their own needs, enhancing product competitiveness while reducing R&D costs and risks.√ Strategic Investment: Automotive companies take stakes in chip companies to achieve strategic cooperation, forming a closer collaboration model.

Table: Layout of SoC Chips by New Force Automotive Companies

Table: Layout of SoC Chips by Traditional Automotive Companies

Intelligent Cockpits, Intelligent Driving, and Autonomous Driving Lead Automotive Evolution, SoC Chip Demand Explodes

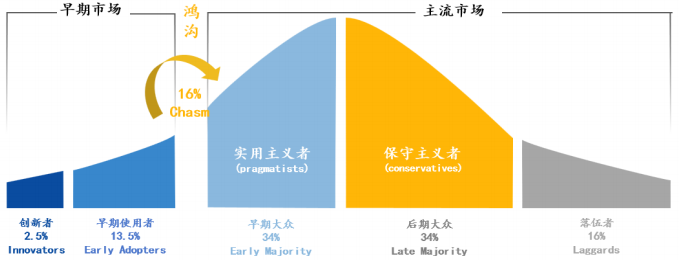

New energy vehicles have surpassed a 50% penetration rate, entering the “late mass market” stage. Consumers care about the fulfillment of overall needs in a “one-stop” manner. This enhancement of overall demand includes both the endorsement achieved through branding and the continuous provision of “optimal solutions for minimal units” that exceed user expectations.

Whether in brand building or promoting “optimal solutions for minimal units,” the focus on user-perceived areas such as appearance, interior, and cockpit is a key direction for automotive companies’ competition.

Figure: Technology Adoption Curve of Electric Intelligent Vehicles

Figure: Factors Considered by Xiaomi YU7 Major Customers When Buying Cars

Due to the large contact area with users and frequent interactions, the intelligent cockpit is an important area perceived by users of electric intelligent vehicles.

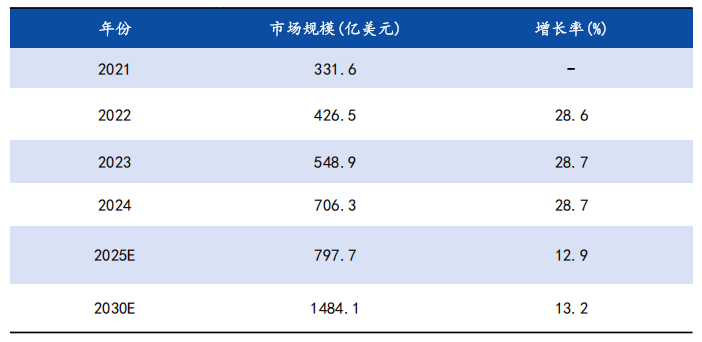

The intelligent cockpit market has shown rapid development in recent years, with both its scale and growth rate being quite impressive. From 2021 to 2024, the global intelligent cockpit market size is expected to grow from $33.16 billion to $70.63 billion, with a compound annual growth rate of 28.66%. It is projected that by 2025, the global market size will reach $79.77 billion, and by 2030, it will reach $148.41 billion.

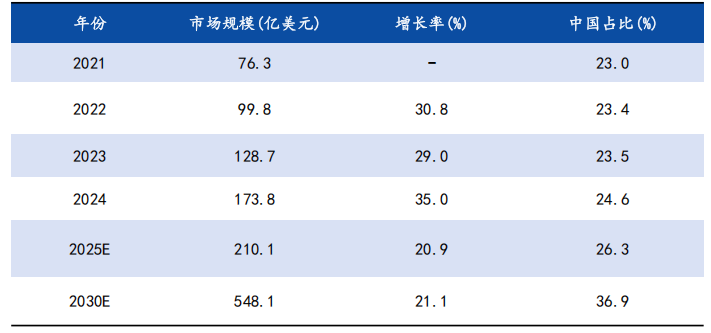

Among them, the development of the intelligent cockpit market in China is particularly prominent, with the market size expected to grow from $7.63 billion in 2021 to $17.38 billion in 2024, achieving a compound annual growth rate of 31.58%, higher than the global market’s 28.66%. It is expected that by 2030, the market size in China will further grow to $54.81 billion, maintaining a high compound annual growth rate of 21.14% during this period.

Table: Global Intelligent Cockpit Market Size and Forecast

Table: China Intelligent Cockpit Market Size and Forecast

With the gradual development of intelligent driving, the focus of competition in the automotive industry has gradually shifted to user-perceived intelligent functions. The configuration level of intelligent cockpits has become one of the important reference indicators for consumers when purchasing cars, and it is also a key area for OEMs to create differentiation and brand influence. As the integration of cockpit functions increases, the required hardware resources and computing power demands are also continuously rising, leading to an increasing demand for intelligent cockpit SoC chips. High computing power and high-performance SoC chips will become essential for intelligent cockpits.

In traditional cockpit solutions, systems such as central navigation, instrument panels, and HUD are independent, each controlled by separate ECUs. However, this distributed architecture has many limitations. With the development of automotive intelligence, the degree of cockpit integration is increasing, and the originally dispersed ECUs are gradually integrated into a cockpit domain controller. The most intuitive manifestation of this integrated transformation is the “one chip, multiple screens,” where a single high-performance SoC chip in the cockpit domain controller drives multiple screens within the cockpit. The implementation of the “one chip, multiple screens” solution places higher demands on SoC chips:

(1) Multi-interface support, increasing more DP or DSI interfaces to enable the SoC chip to drive several different display devices simultaneously, supporting high resolution and high refresh rate display requirements.

(2) High-performance CPU and GPU, where a high-performance CPU ensures smooth operation of multiple apps on different devices simultaneously; a higher-performance GPU provides better graphics processing and video encoding/decoding capabilities, resulting in clearer displays and smoother animations.

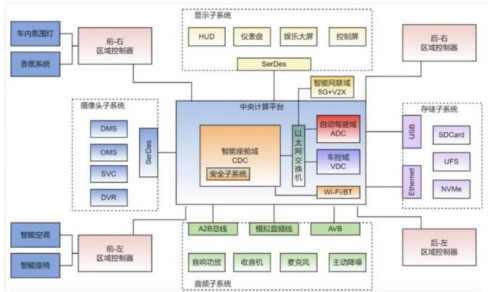

Figure: Intelligent Cockpit SoC Chip Architecture

Market Concentration: Domestic Substitution Gains Traction, Favoring Leading Domestic Enterprises to Continue Breaking Through with Industry Trends

Driven by the upgrade of the EE architecture, the overall control of the cockpit has developed from mechanical and distributed to electronic and integrated, gradually extending from the cockpit concept to the entire vehicle’s cabin space, while increasing safety requirements. The complexity of cockpit integration continues to rise, and the amount and complexity of data to be processed are also increasing, leading to a soaring demand for computing power. The current main trends for cockpit SoCs include:

(1) One chip, multiple screens: A single high-performance SoC chip in the cockpit domain controller drives multiple screens such as the central navigation screen, LCD instrument panel, HUD, air conditioning display panel, passenger entertainment screen, and rear entertainment screen. This requires the processor to have enough DP or DSI interfaces to drive multiple screens; the CPU capability must be strong enough to maintain application smoothness; the GPU’s graphics capability must be high to ensure screen clarity and smoothness, while also needing good support for hypervisors or hardware isolation to enable multi-system operation.

(2) Integration of in-cabin perception technologies: Moving from purely physical buttons to tactile interaction, voice interaction, gesture control, and visual interaction (DMS/OMS) in a multimodal perception direction. This places demands on the rich heterogeneous resources of CPUs, GPUs, DSPs, and NPUs in SoC chips.

(3) Cockpit and driving integration: From cost reduction, better human-machine interaction, and maximizing the use of SoC computing power, the integration of cockpit and driving is gradually becoming a development trend. The industry generally follows the development direction from One Box to One Board, and finally to One Chip. One Chip means achieving all functions with a single chip.

(4) Local deployment of large AI models: With the development of artificial intelligence, major automotive companies have accelerated the integration of AI into vehicles this year, creating high-level AI intelligent cockpit systems with proactive cognition and emotional interaction. The current trend for AI large models in vehicles is shifting from cloud-based large models to edge-based “small models” (under 1 billion parameters) with limited functionality, towards edge-based large models (50 billion-300 billion+ parameters), achieving deep functional developments such as multimodal integrated interaction, full-scene proactive cognition, real-time data processing, and immersive experiences. This requires SoC chips to be updated to provide more robust CPU, NPU performance, and ultra-high bandwidth capabilities.

(5) Further enhancement of integration: Integrating 5G modems, Wi-Fi 7, BT, V2X, and other modules into intelligent cockpit SoCs, achieving a fusion of high-speed connectivity and intelligent computing capabilities through a single chip, enhancing the real-time performance, multitasking capabilities, and user experience of in-vehicle systems, while also helping OEMs reduce costs by eliminating the need for external T-Boxes.

(6) Rapid penetration of system-level packaging (SIP): Facing the increasing power demands and the growing complexity of device types, traditional COB designs face challenges in PCB reliability, thickness, and warpage control. SIP packaging, through BGA ball planting technology, back-end capacitor design, and rich underfill process experience, can effectively solve the challenges customers face in hardware design, process, and reliability, ensuring stable operation of products in harsh environments.

(7) Process technology advancing from 7nm to 4nm and below: According to statistics from Zosi Automotive Research, mainstream chip processes are advancing from 7nm to 4nm and below, with the proportion of chips at 7nm and below expected to reach 36% by 2024 and exceed 65% by 2030. The next generation will progress to 4nm and 3nm, with significant improvements in transistor density, performance, and power control compared to the currently widely used 7nm and 5nm process chips, better supporting the high throughput and continuous operation of AI computing tasks in various application scenarios.

(8) With the rapid entry of cockpit domain control into the sinking market: By 2024, the delivery volume of passenger cars equipped with cockpit domain controllers (based on automotive company parts naming) in the Chinese market (excluding imports and exports) is expected to reach 6.7319 million units, with the installation rate rising from 17.56% in 2023 to 29.37%; models in the 250,000-300,000 yuan price range and 500,000 yuan price range remain the mainstay of cockpit domain control, with installation rates reaching 70%. However, the installation rate of cockpit domain control in the 100,000-250,000 yuan price range has shown rapid growth, increasing from 9.01% in 2022 to 28.42%, a year-on-year increase of 2.58 times; new car deliveries in the 100,000-250,000 yuan price range account for about 58% of the overall market, while the penetration rate of cockpit domain controllers is only 28.42%. With AI empowerment, the penetration of intelligent cockpits will further expand, leading to an expansion of cockpit SoC chips.

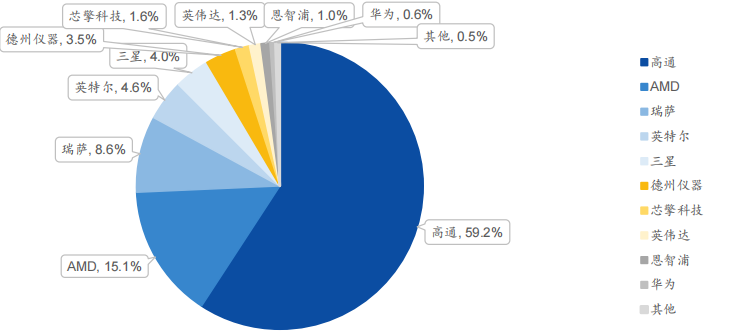

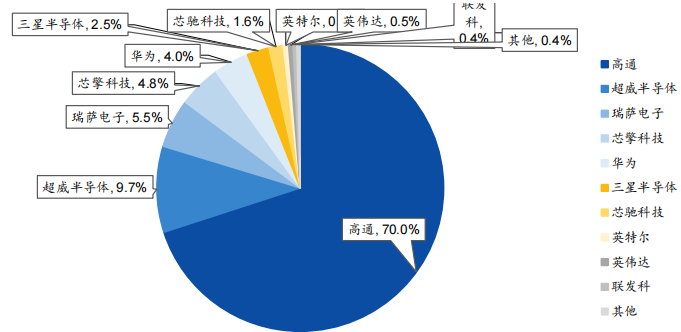

From the market structure perspective, the current market concentration in the intelligent cockpit field is relatively high, with foreign giants occupying a dominant position due to their deep technical accumulation and first-mover advantages. By 2024, Qualcomm, AMD, and Renesas are expected to account for 85% of the market share, with Qualcomm dominating the market with a 70% share.

Driven by the technological transformation and updates of cockpit SoC chips, coupled with the penetration of intelligent cockpit terminals into the sinking market, domestic chip suppliers have rapidly risen in recent years. From less than 3% in 2023 to over 10% in 2024, the significant increase in the market share of domestic chips is evident. Among them, Chipone Technology has successfully surpassed Intel, Samsung, and Texas Instruments, ranking fourth in 2024, rising three places compared to 2023. Its market share has grown from 1.6% in 2023 to 4.8%, demonstrating a 300% increase and further proving the competitiveness of domestic chips in the market.

To better support the deployment of larger parameter AI models on the edge, local manufacturers are also seizing new technological opportunities. For example, Chipone Technology’s new generation AI cockpit SoC-X10 adopts a 4nm process technology, with NPU computing power reaching 40 TOPS, while also matching a 128-bit LPDDR5X memory interface with a bandwidth of up to 154 GB/s, more than twice the bandwidth of the current mass-produced flagship cockpit chips, capable of outputting 20 tokens per second for a 7B (7 billion parameters) model, with a response time controlled within one second.

Figure: Ranking of Intelligent Cockpit Domain Control Chip Installation Volume in 2023

Figure: Ranking of Intelligent Cockpit Domain Control Chip Installation Volume in 2024

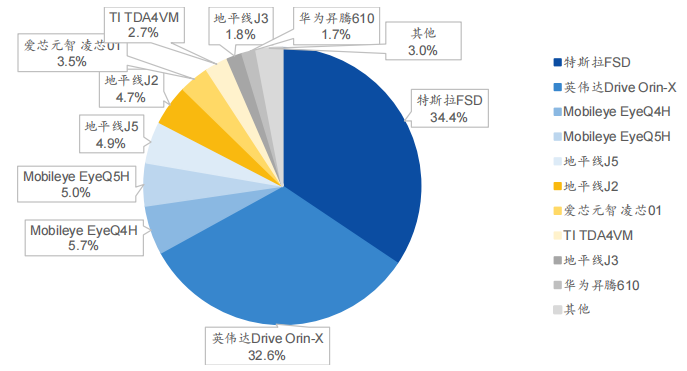

In the autonomous driving SoC chip industry, the barriers to entry are high, requiring companies to invest heavily in R&D, with market R&D cycles typically lasting several years. Leading companies occupy the main market share due to their technological and product accumulation. Foreign companies such as NVIDIA, Tesla, and Mobileye entered the industry earlier and have product advantages, occupying a significant market share.

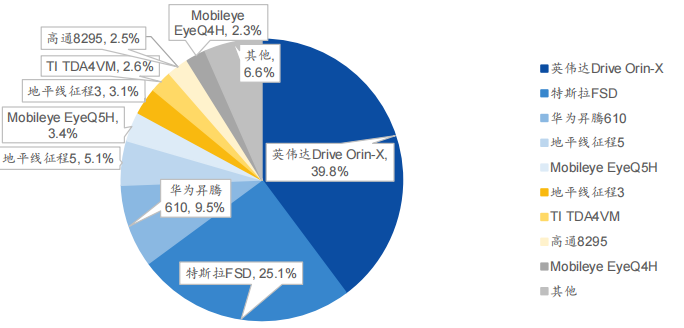

According to the ranking of intelligent driving SoC chip installation volume for the entire year of 2023, NVIDIA, Tesla, and Mobileye accounted for 34.4%, 32.6%, and 5.7% of the market share in China’s autonomous driving SoC chip market, respectively. Starting in 2024, the chip market will present a diversified competitive landscape. The installation volume of NVIDIA chips will increase to 39.8%, while Tesla’s will decrease to 25.1%, and domestic chips such as Huawei Ascend 610 and Horizon J5 will see significant increases in installation volume, reaching 9.5% and 5.1%, respectively.

From the chip landscape perspective, the chip configuration demands of different price segment vehicles vary, breaking away from the situation where NVIDIA dominated the market. The rise of domestic chips is particularly notable, with products from companies like Horizon and Black Sesame Intelligence accelerating domestic substitution, creating a competitive landscape with diverse offerings across all price segments.

Figure: Ranking of Intelligent Driving SoC Chip Installation Volume in 2023

Figure: Ranking of Intelligent Driving SoC Chip Installation Volume in 2024

In terms of domestic substitution of intelligent driving SoC chips, different computing power level chips each have their characteristics:

√ Low computing power chip field, benefiting from chip product strength, a relatively complete toolchain, and strong localization service capabilities, domestic low computing power chips have rapidly gained favor among many domestic automotive companies with intelligent driving R&D needs under the backdrop of supply chain security and controllability. For example, Horizon’s J2/J3 chips have computing power of 4/5 TOPS, targeting the ADAS market where Mobileye operates, and they offer higher computing power and openness compared to Mobileye’s EyeQ4, while being priced at only half of Mobileye’s EyeQ4, receiving positive market feedback. In terms of front-view integrated machine solutions, by 2024, domestic manufacturers Aisin Yuan Zhi and Horizon have already surpassed 50% market share in the standard configuration of front-view integrated machine models for new force passenger vehicles. The total installation volume of domestic front-view integrated machines is expected to reach 10.8068 million sets in 2024, with a penetration rate of 47.15%. The industry is expected to continue growing with the trends of intelligent driving equality and going global.

√ Medium computing power chip field, driven by “intelligent driving equality,” the market below 200,000 yuan is increasing the deployment of high-level intelligent driving features such as high-speed NOA, while avoiding computing power redundancy as much as possible to enhance cost performance, leading to rapid development of medium computing power chips, providing domestic manufacturers with favorable development opportunities. From the perspective of industry development in 2025, based on considerations of algorithm capability matching, ecosystem, and services, several models from Geely, Changan, BYD, and Chery have chosen domestic manufacturers’ Horizon J6E/M solutions, with related companies experiencing rapid growth.

√ High computing power chip field, due to the limitations of small models in terms of computing power and data transmission at the algorithm level, end-to-end large models have become the computational solution for high-level intelligent driving such as urban NOA. The requirements for chips’ computing power continue to rise for high-level solutions approaching L3, and corresponding technological changes also create space for domestic substitution. Although current models supporting urban NOA generally choose NVIDIA’s Orin-X as the main control chip, companies like Huawei, Horizon, Chipone Technology, and Black Sesame are also attempting or have already integrated their chips. For example, Horizon’s J6P, with AI computing power of 560 TOPS, has reached strategic cooperation with Chery and is expected to launch mass production models in September 2025. Chipone Technology, incubated by Geely, has launched the 512 TOPS Star One chip, which competes with dual Orin-X chips, participating in the competition for universal intelligent driving. This chip can achieve a maximum computing power of 2048 TOPS through multi-chip cascading, fully supporting L2-L4 level computing needs, and is expected to be mass-produced in 2025 and delivered in 2026.

Figure: Market Share of Front-View Integrated Machine Computing Unit Suppliers for New Force Passenger Vehicles in 2024

Introduction of Major Domestic Brand Automotive SoC Chip Companies

Horizon: Leading Domestic Player in “Intelligent Driving Equality” with Continuous Progress in Robotics Business

(1) Company Development Overview: The Greatest Common Divisor of Domestic Substitution

Horizon was established in July 2015 and is a leading provider of intelligent driving computing solutions in China, focusing on providing advanced driver assistance (ADAS) and high-level autonomous driving (AD) solutions for passenger vehicles. The company adheres to the concept of combining software and hardware, providing comprehensive technical services including intelligent chips, dedicated software, algorithms, and open toolchains to empower automotive intelligence. Currently, Horizon has made significant progress in the field of autonomous driving SoC chips. As of April 2024, the shipment volume of the “Journey” series chips has exceeded 5 million units, providing core technologies and services for ADAS and AD, empowering over 110 mass-produced models. In addition, Horizon ranks second in the market share of both low-level and high-level intelligent driving chips in China, with market shares of 21.3% and 35.5%, respectively, covering well-known domestic automotive companies such as BYD, Li Auto, SAIC, Geely, and international brands like Volkswagen.

(2) Company SoC Chip Layout for Intelligent Driving: Breakthrough in Computing Power, Moving Towards Mid-High End

Horizon’s intelligent driving assistance solutions integrate various sensors, including LiDAR, front-view cameras, surround-view cameras, ultrasonic radars, long-range millimeter-wave radars, and medium/short-range millimeter-wave radars, to achieve high-precision positioning and comprehensive environmental perception. This multi-sensor fusion solution can provide more comprehensive environmental perception capabilities, thereby enhancing the safety and reliability of autonomous driving systems.

Black Sesame: Pioneer of Domestic Mid-High Computing Power SoCs Benefiting from “Intelligent Driving Equality” Opportunities

(1) Company Development OverviewBlack Sesame Intelligence was established in July 2016, providing automotive-grade computing chips and chip-based solutions for automotive companies. The company started with the Huashan series high-computing power chips used for assisted driving and launched the Wudang series cross-domain computing chips in 2023 to meet the more diverse and complex demands for advanced functions in intelligent vehicles. The company’s own automotive-grade products and technologies provide key task capabilities for intelligent vehicles, including assisted driving, intelligent cockpits, and advanced imaging.(2) Company SoC Chip Layout for Intelligent DrivingHuashan No. 1 A500: In 2019, Black Sesame released Huashan No. 1 A500, which can provide 5-10 TOPS of computing power with a single SoC chip.Huashan No. 2 Series: In June 2020, Black Sesame released the Huashan No. 2 series A1000 and A1000L. In April 2021, it launched A1000pro, which successfully completed tape-out in July of the same year. In 2022, Black Sesame reached cooperation with Jika Intelligent and Dongfeng Group to install A1000 chips in Geely and Dongfeng Group’s pure electric sedans and SUVs. In May 2023, Black Sesame announced cooperation with FAW Group to install Huashan A1000L chips in Hongqi models. In December 2024, the company will release the A2000 series chips, which are designed as high-computing power chip platforms for the next generation of AI models.

Wudang C1200 Series: In April 2023, Black Sesame released the Wudang series chips C1200, specifically designed for multi-domain integration and cockpit-driving integration scenarios. Its C1296 series is the industry’s first cross-domain integration chip platform, covering multiple cross-domain functions including in-cabin perception, infotainment, CMS, automatic parking, intelligent headlights, and safety information systems.

Aisin Yuan Zhi: From Security to Intelligent Driving, Leading Enterprise in Integrated Machines Accelerating Expansion into Mid-High Computing Power

(1) Company Development Overview: Aisin Yuan Zhi Semiconductor Co., Ltd. was established in May 2019, dedicated to creating world-leading artificial intelligence perception and edge computing chips, serving terminal computing, assisted driving, and edge computing markets. The core members come from the security chip team under Megvii Technology, and since its establishment in 2019, the company has focused on smart cities and smart transportation, officially announcing its entry into the intelligent driving field in 2023. Based on its development path, the company is deeply engaged in the AI vision chip track, with its self-developed Aisin Zhi Miao® AI-ISP (Image Signal Processing) and mixed-precision NPU technologies currently possessing core competitiveness.

(2) Major Intelligent Driving Products: The company’s intelligent driving products include the ultra-high cost-performance integrated machine solution M55H, the M57 used in ADAS front-view integrated machines and domain control systems, and the single SoC all-time parking integrated solution M76H, along with the engineering platform xADEP for assisting development. The overall computing platform is currently in the mid-low computing power field and continues to promote comprehensive layouts in high, medium, and low markets.

• M55H: Innovative Proton ISP technology, self-developed high-computing power Neutron NPU, and rich SoC resources, aimed at ADAS integrated machines, DMS/OMS, and CMS applications. AI computing power of 8 TOPS; under 125°C junction temperature and 80% load on CPU & NPU, power consumption is less than 3.2W.

• M76H: Single SoC all-time parking integrated solution, supporting BEV + TRANSFORMER, AI computing power of 60 TOPS; 8-core high-performance CPU, CPU computing power reaches 35K DMIPS, with thermal power (TDP) under 10W at 125°C junction temperature.

—— Excerpt from “In-Depth Report on Automotive SoC Chips: Intelligent Vehicles Lead Evolution, SoC Chips Accelerate Domestic Substitution“For the complete report, please log in to the knowledge platform to download

[Semiconductor Industry Research] Knowledge Platform: Providing high-quality report resources for those in need!

How to become a member of the platform?Long press to recognize the QR code to enter the platform