Warren Buffett: Investment requires only two things, how to value a company and leverage market sentiment.

The global semiconductor industry is entering a new cycle characterized by the end of inventory destocking and the resonance of AI computing power demand. GigaDevice maintains its leading position in NOR Flash and niche DRAM in China, while accelerating the introduction of automotive and industrial control MCUs, forming a “storage + control” dual-drive model. The NOR Flash and MCU sectors where GigaDevice operates have also become the core focus for capital betting on “domestic substitution + edge AI” dual beta.

1. GigaDevice’s Business and Comparable Companies

丨Core Business Description

• Industry Sector: Semiconductor – Storage Chip Design (Fabless)

• Products/Services: SPI NOR Flash, SLC NAND Flash, niche DRAM, 32-bit general-purpose MCU, automotive/industrial MCUs, and sensors

• Customers and End Markets: Consumer electronics, automotive electronics, industrial control, IoT, AI edge devices

• Sales Channels: Direct sales + distribution, global Fabless model

• Key Regions: Mainland China (Revenue ≈ 23%), Overseas (Revenue ≈ 77%)

丨Target Business Revenue Characteristics

In 2024, storage revenue is expected to reach 5.194 billion yuan, accounting for 70.6% of main business; MCU and analog product revenue is expected to be 1.706 billion yuan, accounting for 23%; sensor revenue is expected to be 448 million yuan, accounting for 6.1%.

Choosing comparable companies generally requires meeting at least two dimensions: one is a similar business structure, and it is their main strategic business; the other is that revenue has a certain scale.

Key Comparable Companies

Highly comparable companies’ business and revenue share

Data Source

• Market Share: GigaDevice, Winbond, and Macronix together occupy 90.7% of the global NOR Flash market, with a stable competitive landscape.

• Technical Benchmarking: Winbond’s 45nm NOR Flash has been mass-produced, and Macronix is advancing to 28nm process, in line with GigaDevice’s technology roadmap.• Downstream Applications: All three companies are accelerating their layout in automotive electronics, with GigaDevice’s automotive product revenue share increasing to 15%, forming direct competition with Winbond and Macronix.• Excluded Companies: Overseas Samsung/Hynix/Micron, domestic Beijing Junzheng, and Biwei Storage – Samsung/Hynix/Micron: Primarily standardized DRAM/NAND, significantly different from GigaDevice’s “niche” positioning, with low business overlap. – Beijing Junzheng, Biwei Storage: Storage or MCU accounts for <20%, with a diversified and scattered business structure, not meeting the business structure requirements.

Current Comparable Companies’ Major Valuation Multiples Comparison

Data Source:

If we observe the most comparable companies globally, several overseas companies are in unprofitable states, such as SanDisk losing 1.6 billion USD. In the A-share digital chip design industry, the current median PE valuation of comparable companies is 87.68 times, and GigaDevice’s current valuation is 88.48 times, which is at the market’s average valuation pricing. Leading companies typically can obtain a premium of over 20% above the market, combined with the tight supply of the company’s main products, the price increase continues, and the company’s performance is sustainable, with new products ramping up, the future revenue and profit space is expected to open up, and the premium level is expected to be maintained for a period of time.

Data Source

All calculations are based on current public information

Data Source

The above DCF (Discounted Cash Flow) valuation is based on the company’s ability to achieve a revenue compound growth rate of 30% over the next five years, with revenue growing from 7.4 billion in 2024 to 27.3 billion, and EBIT gross margin improving to 15-30%, while maintaining capital expenditures without waste to generate returns; operating capital is also effective, without significant increases in capital lock-up, the enterprise value obtained from this discounting is for reference only. In other words, the current market’s expected level is already based on significant growth assumptions, but a major reason for this is due to the industry’s performance volatility, stock price volatility is also large, thus its beta and required return WACC are also relatively high. If the company’s core products can remain stable in the future, including a decline in risk-free interest rates, a decrease in discount rates can also support its valuation.

3. 2025 Annual Report Analysis

丨Growth: Increased Year-on-Year and Quarter-on-Quarter

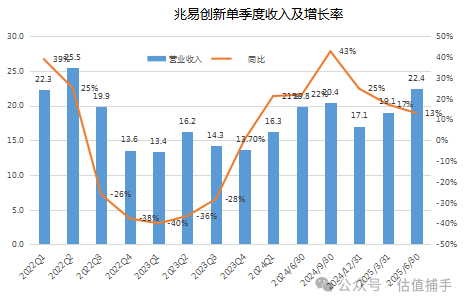

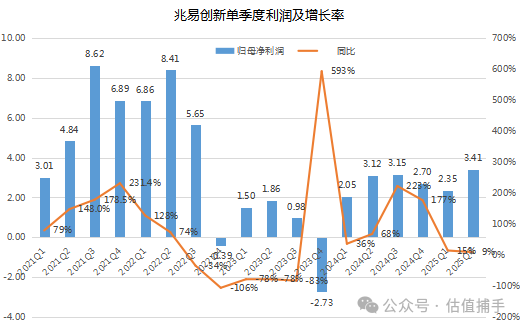

In the first half of 2025, revenue reached 4.15 billion yuan (YoY + 15.00%), net profit attributable to the parent company was 575 million yuan (YoY + 11.31%), and net profit excluding non-recurring items was 544 million yuan (YoY + 14.99%). Quarter by quarter, Q2 revenue was 2.241 billion yuan (QoQ + 17.40%), net profit was 341 million yuan (QoQ + 45.27%), showing significant seasonal effects.As of the end of June 2025, contract liabilities increased by 43.05% compared to the end of the previous year, reflecting an increase in customer prepayments, indicating support for revenue recognition in the second half of the year.

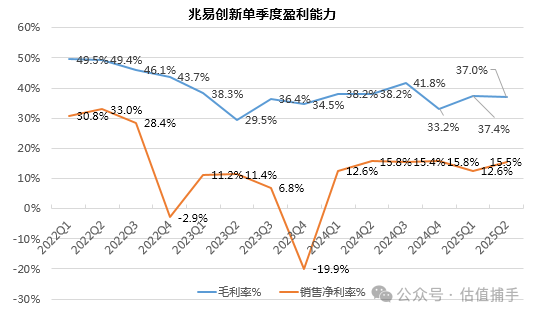

丨Revenue Growth DriversNOR FlashNOR Flash benefits from the increase in the number of AI edge devices per unit to 20-30, with the global market size expected to reach 3.111 billion USD in 2025 (YoY + 25.3%), while the onboard Flash capacity is gradually upgrading from 256Mb to 512Mb, driving revenue growth in the high single digits year-on-year.Niche DRAMNiche DRAM has seen a supply shortage due to major overseas manufacturers shifting capacity to mainstream products including DDR5, achieving both volume and price increases, driving revenue growth and gross margin improvement. The company’s new DDR4 8Gb products are rapidly ramping up in the TV and industrial sectors, with revenue doubling year-on-year. This has become a new engine for revenue growth. The company expects a growth rate of over 50% for DRAM revenue in 2025, with DDR4 accounting for over 60%.MCUAutomotive-grade products have passed ASIL D certification, with year-on-year revenue growth of nearly 20%, and the automotive electronics share increasing to 15%.l Profitability: Remains StableIn the first half of the year, the company’s gross and net profit margins remained generally stable, with niche DRAM benefiting from the supply shortage caused by foreign manufacturers exiting the market, leading to price increases starting in the second quarter. The gross margin of DRAM has seen a noticeable increase, while MCU has seen a slight decline. As the revenue share of DRAM gradually increases, the overall gross margin level remains stable.

丨Revenue Growth DriversNOR FlashNOR Flash benefits from the increase in the number of AI edge devices per unit to 20-30, with the global market size expected to reach 3.111 billion USD in 2025 (YoY + 25.3%), while the onboard Flash capacity is gradually upgrading from 256Mb to 512Mb, driving revenue growth in the high single digits year-on-year.Niche DRAMNiche DRAM has seen a supply shortage due to major overseas manufacturers shifting capacity to mainstream products including DDR5, achieving both volume and price increases, driving revenue growth and gross margin improvement. The company’s new DDR4 8Gb products are rapidly ramping up in the TV and industrial sectors, with revenue doubling year-on-year. This has become a new engine for revenue growth. The company expects a growth rate of over 50% for DRAM revenue in 2025, with DDR4 accounting for over 60%.MCUAutomotive-grade products have passed ASIL D certification, with year-on-year revenue growth of nearly 20%, and the automotive electronics share increasing to 15%.l Profitability: Remains StableIn the first half of the year, the company’s gross and net profit margins remained generally stable, with niche DRAM benefiting from the supply shortage caused by foreign manufacturers exiting the market, leading to price increases starting in the second quarter. The gross margin of DRAM has seen a noticeable increase, while MCU has seen a slight decline. As the revenue share of DRAM gradually increases, the overall gross margin level remains stable.

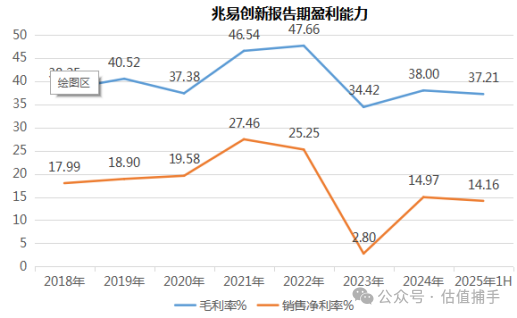

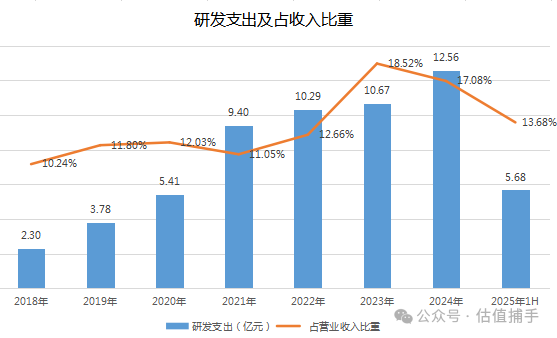

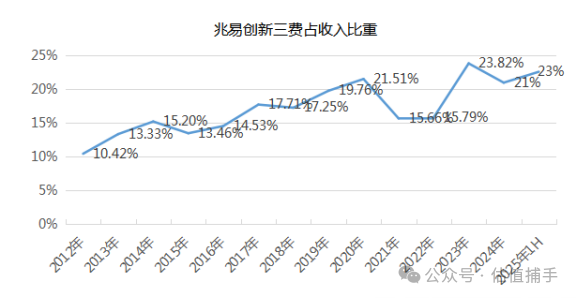

The company’s half-year report shows a net profit margin of 14.16%, which has seen a slight decline. This is mainly due to continued high R&D investment, while the proportion of three expenses has increased due to reduced interest income.The company continues to maintain a high R&D investment model, with R&D expenses of 568 million yuan in the first half, accounting for 14% of operating income, focusing on 28nm NOR Flash, automotive-grade MCU, and AI sensors, continuously solidifying technical barriers.

The company’s half-year report shows a net profit margin of 14.16%, which has seen a slight decline. This is mainly due to continued high R&D investment, while the proportion of three expenses has increased due to reduced interest income.The company continues to maintain a high R&D investment model, with R&D expenses of 568 million yuan in the first half, accounting for 14% of operating income, focusing on 28nm NOR Flash, automotive-grade MCU, and AI sensors, continuously solidifying technical barriers.

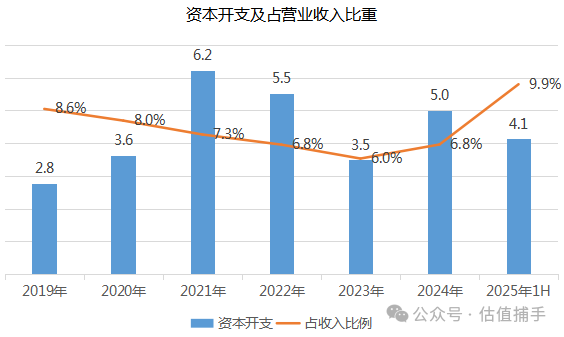

丨Capital Expenditures Continue to IncreaseGigaDevice adopts a Fabless model (no wafer fab), outsourcing heavy asset links such as wafer manufacturing, packaging, and testing, focusing solely on chip design. Therefore, the company’s capital expenditures are mainly used for R&D investment, equity investment, and a small amount of equipment upgrades.Based on technological investments, the company’s capital expenditures continue to increase, with capital expenditures reaching 410 million yuan in the first half, accounting for 10% of revenue.Ongoing capital expenditures have put pressure on profits.

丨Capital Expenditures Continue to IncreaseGigaDevice adopts a Fabless model (no wafer fab), outsourcing heavy asset links such as wafer manufacturing, packaging, and testing, focusing solely on chip design. Therefore, the company’s capital expenditures are mainly used for R&D investment, equity investment, and a small amount of equipment upgrades.Based on technological investments, the company’s capital expenditures continue to increase, with capital expenditures reaching 410 million yuan in the first half, accounting for 10% of revenue.Ongoing capital expenditures have put pressure on profits.

丨Accelerated Mergers and Acquisitions

In 2024, increase capital in Changxin Technology and acquire Suzhou Saixin, strengthening the synergy between storage and automotive electronics;

In 2025, plans to continue using raised funds for the construction of the 28nm NOR Flash production line.

丨Capital Return Gradually Recovers

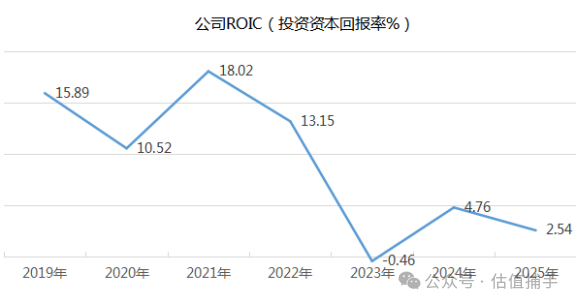

GigaDevice’s ROIC (Return on Invested Capital) has entered a recovery channel after experiencing a cyclical low, a trend mainly benefiting from industry recovery, product structure optimization, and strategic adjustments. Brokers predict a net profit attributable to the parent company of 1.46 to 1.55 billion yuan in 2025 (YoY +32.5%), and if the gross margin returns to over 40%, ROIC is expected to recover to over 10%. The current WACC is about 10%, and if ROIC continues to rise to over 15% (close to the historical median of 19.17%), it will enter the value creation range. 丨Company Strategic Layout and Growth Points• Product Matrix:NOR Flash: Accelerate the R&D of 28nm process, aiming for mass production in 2026, to seize the high-end market (such as AI servers).• DRAM:Low Power DDR4 small capacity products to increase to double digits, with a target revenue of over 1 billion yuan in 2025.• MCU:Automotive-grade products have passed ASIL D certification, with a target revenue share of automotive electronics increasing to 20% in 2025.• Analog Chips:After acquiring Saixin, the analog business has become a new growth point, with a target revenue share of 15% in 2025. • Capacity Assurance:Changxin’s 12-inch wafer fab has a capacity utilization rate of over 85%, prioritizing GigaDevice’s DRAM foundry needs.

GigaDevice’s ROIC (Return on Invested Capital) has entered a recovery channel after experiencing a cyclical low, a trend mainly benefiting from industry recovery, product structure optimization, and strategic adjustments. Brokers predict a net profit attributable to the parent company of 1.46 to 1.55 billion yuan in 2025 (YoY +32.5%), and if the gross margin returns to over 40%, ROIC is expected to recover to over 10%. The current WACC is about 10%, and if ROIC continues to rise to over 15% (close to the historical median of 19.17%), it will enter the value creation range. 丨Company Strategic Layout and Growth Points• Product Matrix:NOR Flash: Accelerate the R&D of 28nm process, aiming for mass production in 2026, to seize the high-end market (such as AI servers).• DRAM:Low Power DDR4 small capacity products to increase to double digits, with a target revenue of over 1 billion yuan in 2025.• MCU:Automotive-grade products have passed ASIL D certification, with a target revenue share of automotive electronics increasing to 20% in 2025.• Analog Chips:After acquiring Saixin, the analog business has become a new growth point, with a target revenue share of 15% in 2025. • Capacity Assurance:Changxin’s 12-inch wafer fab has a capacity utilization rate of over 85%, prioritizing GigaDevice’s DRAM foundry needs.

4.

Core Views of Brokerage Research Reports

• Positive Factors:AI terminal demand explosion (such as robots,AR/VR) drives NOR Flash usage growth, niche DRAM industry supply gap continues until 2026 year.

GigaDevice’s Core Competitiveness:

• Industry Leader: global market share isaround 20%, ranking second for two consecutive years.DRAM business is rapidly ramping up,backed by Changxin, with priority capacity assurance.

• Product Diversification: Storage + MCU + Sensors have significant synergy effects, with stronger resistance to cyclical fluctuations than pure storage manufacturers.

• Domestic Substitution Dividend: Automotive-grade MCU has entered the supply chain of BYD and NIO, with vast replacement space for STMicroelectronics.

• Leading Technology Iteration:45nm NOR Flash mass production cost is 15% lower than 55nm ,28nm R&D progress is the first in the country.

5. Conclusion

Under the explosion of AI terminal demand and the wave of domestic substitution, GigaDevice’s storage and MCU businesses form a performancedriving force,the 2025 mid-year report verifies its growthpotential.In the upward industry cycle, with a slight technological lead and cost advantage, it is expected to achieve a gross margin recovery to over 40% by 2026. It is recommended to pay attention to the progress of 28nm NOR Flash mass production and the customer expansion of automotive-grade MCU, with long-term potential to grow into a global semiconductor design leader.

This article is complete~~~

Special Note: The above analysis is only a personal compilation of data, representing personal views, and does not constitute any investment advice, for reference only.

#Semiconductor #Packaging #Storage Chips #GigaDevice #AI #Domestic Substitution