Skip to content

I have been tutoring high school mathematics in Sichuan lately. Although I haven’t done math problems in twenty years, I can still manage the exercises in the workbook. If there are problems I can’t solve, I can understand the thought process after looking at the answers.

However, my student has stopped coming to class for several days. I’m not sure why; perhaps I was talking too much and too fast. The knowledge points are few, taking less than two minutes to explain. When it comes to functions, I can summarize the domain, range, monotonicity, and parity in four sentences. Then we can jump straight into practice problems.

Maybe it really was too brief. I haven’t touched math in twenty years, and I can solve problems with just four sentences, so she should be able to as well…

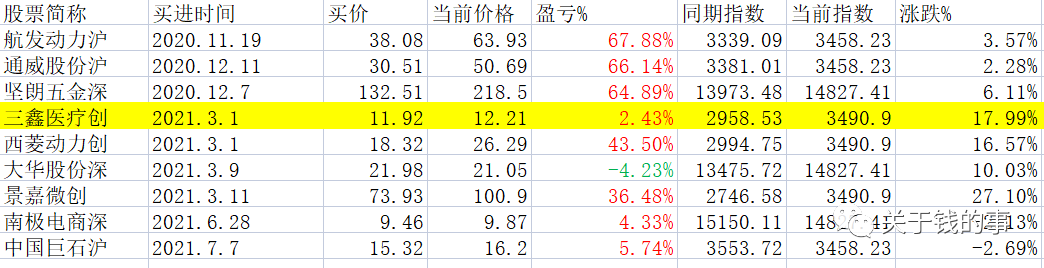

The reform of the three mountains is about to finish, and Sanxin Medical should sell quickly before incurring losses.

If it weren’t for value investing, one really has to consider stock characteristics. It’s about looking at its historical trend characteristics. If the historical trend shows three steps forward and two steps back, and you are someone who can’t stand such fluctuations, it’s best not to touch it; it can be very frustrating.

For example, an acquaintance asked me about Lianchuang on July 8. If you look at the K-line from that date, it has already increased more than double from that position, which is relatively high. Can we still enter?

1: There has been a volume increase here, indicating that action is about to happen. Also, the position on July 8 broke through the head and shoulders bottom.

2: Its historical trend is characterized by rapid and vertical movements.

So let’s be cautious; if we are afraid of missing out, we can enter with a smaller amount.

Take a look at carbon neutrality – carbon trading – forest carbon sinks; these are some fragmented pieces of information I wrote on July 12.

Under the 3060 dual carbon target, on July 7, 2021, the State Council clarified that based on pilot projects, the national carbon emissions trading market for the power generation industry will be launched this year in July. Carbon emission quotas will be allocated to enterprises based on certain rules, and enterprises that exceed their quotas will need to purchase the shortfall from the carbon exchange; otherwise, they will face hefty fines.

Some industries emit carbon during production, while others not only do not emit carbon but also can absorb it. Carbon absorption can be divided into two types: active carbon recovery and passive carbon recovery. Active carbon recovery is similar to carbon capture, where carbon dioxide is collected and reprocessed. Passive carbon recovery is interesting; planting a tree can absorb carbon dioxide.

Thus, major carbon-emitting enterprises often find that the quotas allocated by the state each year are insufficient and need to purchase additional emissions. It’s like a very overweight person who doesn’t get enough food rations and has to buy extra to fill their stomach, while other enterprises are like a thin person who can’t finish their own rations and even grows crops to sell.

The enterprises that do not consume their rations but grow crops to sell are what we are discussing today: forest carbon sink enterprises.

The carbon emitted is equal to the carbon absorbed, which is termed “carbon neutrality.” There are two paths to achieve carbon neutrality: increasing sources and reducing emissions. Reducing emissions means emitting less or not at all, while increasing sources means planting more trees to offset excess emissions with the absorption capacity of forests.

According to the methods and mechanisms of carbon offsetting, they can be roughly categorized into three types: international carbon offset mechanisms, independent carbon offset mechanisms, and regional, national, and local carbon offset mechanisms.

International Carbon Offset Mechanisms

In international carbon offset mechanisms (CDM), China has registered a total of 5 forestry carbon sink CDM projects successfully, located in Guangxi, Sichuan, and Inner Mongolia.

However, there are very few forestry carbon sink projects under the CDM, with only 66 registered globally, accounting for less than 1% of the total 8415 projects. The trading price is extremely low, at only 1.04 USD per ton. The trading volume is minimal, with a total trading volume of only 111.16 million tons in 2020, generating a total transaction value of merely 1.1506 million USD.

Independent Carbon Offset Mechanisms

For independent carbon offset mechanisms – Gold Standard (GS), China has registered 3 forestry carbon sink projects, located in Guangdong, Yunnan, and Liaoning. As of June 30, 2021, the Gold Standard has issued a total of 178 million tons of emission reductions, with 8.8 million tons of reductions expired or canceled. Cumulative transactions reached 101,000 tons, with an average transaction price of 14.1 USD per ton. The volume is small, but the price is high.

For independent carbon offset mechanisms – Verified Carbon Standard (VCS), currently 80 countries participate in VCS projects, with 29 forestry carbon sink projects registered in China. Globally, there have been 1711 registered VCS projects, issuing 694 million tCO2e. China ranks first in the number of registered projects.

Regional, National, and Local Carbon Offset Mechanisms (CCER)

The first two offset mechanisms are of global nature; what is most important for us is the third type: regional, national, and local carbon offset mechanisms (CCER).

As early as 2011, the National Development and Reform Commission issued a notice on conducting pilot carbon emissions trading. In 2012, it issued the “Interim Measures for the Management of Voluntary Greenhouse Gas Emission Reduction Trading,” clarifying that CCER projects can participate in carbon trading after being filed and verified.

In December 2020, the “Interim Measures for the Management of Carbon Emission Trading (Trial)” were introduced, stipulating that key emitting units can use the national certified emission reductions to offset their carbon emission quotas, with a maximum offset ratio of 5% of the carbon emission quota that needs to be cleared, and CCER is clearly included in the national carbon trading market.

In March 2021, the draft revised “Interim Regulations on Carbon Emission Trading” was issued, stating that implementation units of renewable energy, forestry carbon sinks, methane utilization, and other projects can apply to the competent ecological environment department of the State Council for verification of the greenhouse gas emission reductions produced by their projects. It was further clarified that CCER is included in forestry carbon sinks.

This means that in the carbon trading starting in July, forestry enterprises can sell their carbon emission quotas, and the carbon emission credits sold are essentially generated out of thin air. They do not require any cost, thus increasing revenue with a gross profit margin of nearly 100%. As long as carbon trading begins, profits are generated, and as long as forest resources exist, profits can be continuously created.

The province with the highest forest coverage in China is Fujian. In 2017, the “Fujian Forestry Carbon Sink Trading Pilot Plan” selected 20 counties and cities such as Shunchang, Yong’an, Changting, Dehua, Hu’an, Xiapu, Yangkou State-owned Forest Farm, and Wuyi State-owned Forest Farm to conduct forestry carbon sink trading pilot projects. The projects include carbon sink afforestation, forest management carbon sinks, bamboo forest management carbon sinks, etc. As of now, Fujian has approved a total of 20 projects with a total registered emission reduction of 2.9069 million tons. The cumulative transaction amount is 41 million yuan, with an average of 14.73 yuan per ton.

Similarly, cities like Guangzhou, Dongguan, Zhongshan, Huizhou, Shaoguan, and Heyuan in Guangdong province have been included in the pilot. Forestry carbon sinks account for 92% of the total projects, with a cumulative transaction amount of 49.52 million yuan, and an average price of 23.61 yuan per ton. Beijing’s forestry carbon sink transaction amount is 5.27 million yuan, with an average price of 37.7 yuan per ton.

Although the current trading volume of carbon emission credits is low, this is just the beginning of the pilot. Once it is on the right track, the approved forestry carbon sinks and trading volume across the country will increase by one or several orders of magnitude.

According to data from the National Bureau of Statistics, as of 2019, China’s forest stock volume reached 17.56 billion cubic meters, and the forest coverage rate reached 23.04%. The 14th Five-Year Plan indicates that during the 14th Five-Year Plan period, China’s forest coverage rate will increase to 24.1%. By 2035, the forest coverage rate will reach 26%, and the forest stock volume will reach 21 billion cubic meters.

According to the report by Dongzhu Ecology in 2020, for every 1 cubic meter of forest growth, an average of 1.83 tons of carbon dioxide is absorbed, and 1.62 tons of oxygen is released.

With the increase in forest stock volume and forest coverage rate in China, the amount of carbon dioxide absorbed by forests will gradually increase, and the forestry carbon sink effect will become apparent.

Yueyang Forest Paper (600963) owns nearly 2 million acres of forestry resources. In 2017, it partnered with Shell Energy to become the first central enterprise in Hunan to enter the carbon sink trading market. In 2020, its subsidiary Maoyuan Forestry became the only national reserve forest project in Hunan that cooperated with the National Development Bank.

In 2021, in March, it signed a long-term carbon sink trading option contract with Shell, and in June signed a cooperation agreement with Baogang for a total of no less than 50 million tons of CCER over 25 years.

Yueyang Forest Paper is an integrated enterprise that simultaneously owns upstream forestry resources and downstream paper-making operations. Its main business includes the production and sale of mechanical paper, commodity pulp, and forestry management.

After 2017, it began to generate profits. Due to the hot carbon trading and paper products this year, four institutions expect its annual performance to grow by over 50%. In Q1 2021, its non-recurring net profit grew by 108.7%.

The proportion of non-recurring net profit to net profit has been stable. The average free cash flow over the past 5 years is 650 million, accounting for 221% of the average net profit over the past 5 years. The average cash surplus coverage ratio is 8.64 times.

The valuation of shareholder surplus discount method estimates the market value at approximately 20.55 billion, while the current market value is 19.31 billion, indicating undervaluation, but with small safety margins.

PEG = 0.95, indicating undervaluation, but with small safety margins.

From a technical perspective, it has increased in volume but is significantly deviated from the moving average, waiting for a pullback. (July 12)

Looking at it now, if it can reach MA60, I would like to wait a bit longer; if it can reach MA120, I would buy.

Fujian Jinsen (002679) has a forest area of over 800,000 acres, with a stock of 6.5023 million cubic meters, expected to reduce emissions by 32,200 tons annually. In 2017, the forestry management carbon sink project was approved in Fujian. In 2020, the first batch of national forestry carbon tickets was issued in Sanming, totaling 18,300 tons.

Fujian Jinsen is a key leading enterprise in agricultural industrialization and one of the most important production areas for commercial fir wood in the country. Its main business includes forest cultivation and management, and timber production and sales.

Since 2019, its revenue has declined, but costs have not decreased year-on-year, and financial expenses have surged. Its performance has been unstable. In 2019, its non-recurring net profit declined by 128.74%, and in 2020, it showed no improvement, remaining roughly the same as in 2019, with a year-on-year increase in non-recurring net profit of 6.21%.

In Q1 2021, its non-recurring net profit was a loss of 16 million, a year-on-year increase of 9.81%, showing no improvement.

The average free cash flow over the past 5 years is 30 million, accounting for 20.68% of the average net profit. The average cash surplus coverage ratio over the past 5 years is 0.32. There are serious issues with operating cash flow.

From a technical perspective: it has increased in volume, and the stock price is approaching MA60. The MA60, 120, and 250 are in a bullish arrangement. Waiting for a pullback to confirm the support level. (July 12)

Looking at it now, if it can reach MA250, I would like to give it a try.

Pingtan Development (000592) has nearly 900,000 acres of forest area.

Pingtan Development’s main business includes afforestation, forestry products, and tobacco fertilizers. Its performance has always been around the break-even point, with a huge loss of 226 million in 2020, equivalent to the total profit of the previous decade. The loss in 2019 was due to impairment losses on assets, including inventory depreciation.

In 2021, Pingtan Development had a net asset of 3.304 billion and total assets of 4.787 billion, with inventory of 2.398 billion. Inventory accounts for 72.58% of net assets and 50.09% of total assets.

In 2020, the largest loss in inventory provision was due to development costs. Development costs usually refer to all inputs that constitute the sale conditions of real estate products, including shared facility costs, environmental greening costs, and all external pipeline costs. We can also see that Pingtan Development still holds investment properties.

Short-term issues cannot be resolved.

Dongzhu Ecology (603359) signed a cooperation agreement with Shanghai Environment and Energy Exchange and Green Technology in June of this year.

Dongzhu Ecology is the most qualified and strongest comprehensive landscape company in China. Its main business includes seedling planting, ecological landscape design, ecological restoration and landscape engineering construction, and landscape maintenance.

Dongzhu Ecology’s performance has shown steady and rapid growth, with a compound annual growth rate of 46.98% from 2008 to 2020. In 2020, its non-recurring net profit increased by 7.73% year-on-year, and in Q1 2021, its non-recurring net profit increased by 28.6% year-on-year.

Since its listing, it has had an average free cash flow of -40 million, with an average cash surplus coverage ratio being negative.

For such a high growth rate of performance, the cash situation is very poor, which makes me a bit uneasy. Accounts receivable and other receivables are particularly high. Especially, other receivables have increased significantly over the past three years.

In Q1 2021, the total of accounts receivable and other receivables reached 1.018 billion, accounting for 30.21% of net assets of 3.37 billion and 13.68% of total assets of 7.444 billion. The proportion is too high.

Such an unsafe financial situation makes it meaningless to use absolute valuation methods.

With a nearly 47% compound growth rate over the past 10 years, the market only gives a 12.25 times price-to-earnings ratio, indicating that there must be some problems.

From a technical perspective, it has increased in volume. However, the moving average system has not performed well yet.

The financial safety of Yueyang Forest Paper is high, but the risk-reward ratio at the current price is not attractive; I still need to wait for a pullback.

Fujian Jinsen’s finances are very poor, but they are very real. If it can be elevated, it will ride the wave of the dual carbon target – carbon trading – forestry carbon sinks. Thus, this stock has a high speculative proportion.

The other two are not considered for now.

Now looking at smart controllers, these are some fragmented pieces of information I wrote on July 14.

What is a smart controller?

Smart controllers are the central nervous system and brain of various terminal products. For example, a smart device has upstream components such as IC chips, PCB boards, MOSFETs, diodes, resistors, capacitors, and other components for computation. The downstream includes application devices like automotive electronics, household appliances, power tools, industrial equipment, smart homes, lithium batteries, medical devices, and consumer electronics.

Thus, the device that connects upstream computation and downstream operation is the smart controller. It generally includes MCU chips, digital displays, micro switches, and other control components, as well as PCB capacitors and resistors.

Before smart controllers, we used traditional mechanical controllers. However, mechanical controllers have many drawbacks, the most obvious being that mechanical controllers can only achieve linear control and cannot meet intelligent level requirements. For example, when heating a rice cooker, mechanical control can only linearly increase the temperature, while a smart controller can maintain a constant temperature at each set time.

Demand Side of Smart Controllers

With the development of intelligence and networking, the diversity of terminal products is increasing, and in the context of the Internet of Things, every device requires one or more smart controllers.

A smart fridge, for instance, requires at least three smart controllers: a touch display controller, a compressor frequency conversion controller, and a power controller. A cordless power tool requires at least three smart controllers: various functional smart controllers in the work area, a battery pack protection board controller, and a lithium charging controller.

Especially in the case of smart home products, many are small and precise products. The more products there are, the more smart controllers are used. Intelligent products are increasingly favored by the market. A consumer trend report released by Suning in 2019 showed that smart fridge sales accounted for over 35%, and the smart rate of appliances like water dispensers exceeded 30%, while the smart rate of electric steamers and water purifiers reached as high as 80%.

The demand side for smart controllers can be divided into four major categories: automotive electronics account for 25%, household appliances account for 20%, power tools account for 16%, and smart buildings and homes account for 9%. The industry information network predicts that the global market size will reach 1.5 trillion USD by 2020.

The cost proportion of smart controllers varies greatly among different smart products. For example, in the case of Joyoung induction cookers, the cost proportion of the smart controller is about 17.5%. For Joyous pressure cookers, the cost proportion of the smart controller is about 3%. The average cost proportion is about 10%.

If calculated with a 10% cost ratio, in 2019, China’s household appliance sales reached 1.6 trillion, thus the annual demand for smart controllers is around 160 billion yuan.

Looking at the power tool market, China is a major manufacturing and exporting country for power tools, accounting for over 80% of global exports. Even in 2020, it maintained a growth rate of 5.3%, reaching 490 million units. It is conservatively estimated that the demand scale for smart controllers in the power tool sector is about 14 billion yuan.

In the automotive electronics market, global car sales exceed 90 million vehicles. The number of controllers (ECUs) in cars varies from dozens to hundreds. Assuming an average of 70 ECUs per vehicle, with a unit price of 100 yuan, the total global market demand reaches 6 trillion yuan.

In 2020, the two leading smart controller companies in China, HeTai and Tuobang, had revenues of 4.666 billion and 5.56 billion yuan, respectively. Compared to the market demand scale, there is still a significant gap, indicating substantial room for growth.

Supply Side of Smart Controllers

China is the global electronic manufacturing center, and the overseas revenue scale in the smart controller sector has been continuously growing, with the compound growth rate of top enterprises’ overseas revenue reaching 26% over the past decade.

In 2020, Tuobang’s overseas revenue was 3.065 billion, accounting for 55.12% of total revenue; HeTai’s overseas revenue was 3.248 billion, accounting for 69.62% of total revenue.

Of course, China’s smart controllers have not yet become global leaders. The only two competitors are in Germany. The top one is Bosch, with an annual revenue of 550 billion. The second is Delta in Taiwan, with an annual revenue of 65.4 billion. The third is Tuobang, with an annual revenue of about 5.6 billion. The fourth is EGO in Germany, with an annual revenue of 5.1 billion. The fifth is HeTai, with an annual revenue of 4.7 billion. The sixth is Denso in Germany, with an annual revenue of 3.8 billion.

The combined revenue of the two leading smart controller companies in China is only about 10 billion, which is 55 times less than Bosch.

However, enterprises of Bosch and Delta’s scale do not only produce smart controllers; they are comprehensive giants. Tuobang and HeTai in China are specialized controller enterprises.

From the perspective of the 26% compound growth rate in overseas revenue of Chinese controllers, the speed of the two leading enterprises capturing the entire market is not slow. There are vast demand markets both domestically and internationally that can be improved.

Tuobang: The domestic leader in the smart controller industry, focusing on four application fields: home appliances, tools, lithium batteries, and industrial control.

Since 2013, its performance has steadily risen, with a compound annual growth rate of 41.62%. 2020 was the fastest growth year, with a year-on-year increase of 92.85% in non-recurring net profit. In Q1 2020, the year-on-year increase in non-recurring net profit was 527.31%.

Seventeen institutions estimate that Tuobang’s average compound growth rate over the next two years will be 31.33%, with PEG = 0.96, indicating undervaluation, but with low safety margins.

The average cash surplus coverage ratio over the past 5 years is 1.16.

From a technical perspective: it has increased in volume, and previously, it found support near the MA60 and MA120 lines multiple times. It is currently facing the MA60 line; I will wait for a pullback to MA60 before making a decision.

HeTai: One of the domestic leaders in the smart controller field, mainly engaged in smart hardware and smart controllers, with layouts in microwave millimeter-wave chips and automotive electronics. Its clients include Electrolux, Whirlpool, Siemens, TTI, Arcelik, BSH, BorgWarner, Hisense, Haier, and Supor.

Its subsidiary Chengjing Technology also has microwave millimeter-wave radio frequency chip technology, applied in satellite remote sensing, satellite navigation, and communication fields in China.

Since 2012, its performance has been steadily increasing, with a compound annual growth rate of 37.19%. In 2020, its non-recurring net profit increased by 26.34% year-on-year. In Q1 2021, its non-recurring net profit increased by 92.37% year-on-year.

Twenty-five institutions estimate that the average compound growth rate over the next two years will be 43.2%, with PEG = 1.43, slightly high.

From a technical perspective: it has increased in volume, but the pullbacks are MA120 and MA250; I will wait for a pullback before making a decision.

If Tuobang can reach MA120, I will consider trying it.