On August 7, 2025, SoftBank Group released its Q1 FY2025 performance report. This document is not just a routine financial data disclosure but resembles a strategic declaration, clearly revealing that the group is at a critical transformation point. After experiencing the glory of the mobile internet era, SoftBank is resolutely betting its vast capital and future vision on the emerging golden track of artificial intelligence.

This profound strategic shift is manifested through a series of key financial indicators. On one hand, thanks to the soaring stock price of its core holding company Arm, the group’s net asset value (NAV) has reached a historical high; on the other hand, the large-scale investments made to seize the initiative in the AI field have significantly altered its debt and cash situation.

The financial report presents a SoftBank that is actively expanding its balance sheet to drive future growth. It is no longer content to be merely a diversified technology investor but is attempting to become a core builder and enabler in the AI era. From substantial follow-on investments in OpenAI to acquisition plans for chip design company Ampere, every move SoftBank makes revolves around the core elements of the AI industry chain. This strategy is undoubtedly aggressive, tying the group’s fate closely to the highly volatile AI market.

Investing $10 billion in OpenAI, Arm Supports Half of the Empire

SoftBank Group is undergoing a profound transformation from the ground up, shifting its focus from a diversified technology investment platform to an investment holding company with artificial intelligence as its absolute core. This transition is not merely a verbal strategic declaration but is reflected in every corner of its balance sheet through a series of decisive capital operations and asset swaps. Currently, SoftBank’s investment portfolio, financial health, and market posture are clearly being reshaped around the axis of “AI”.

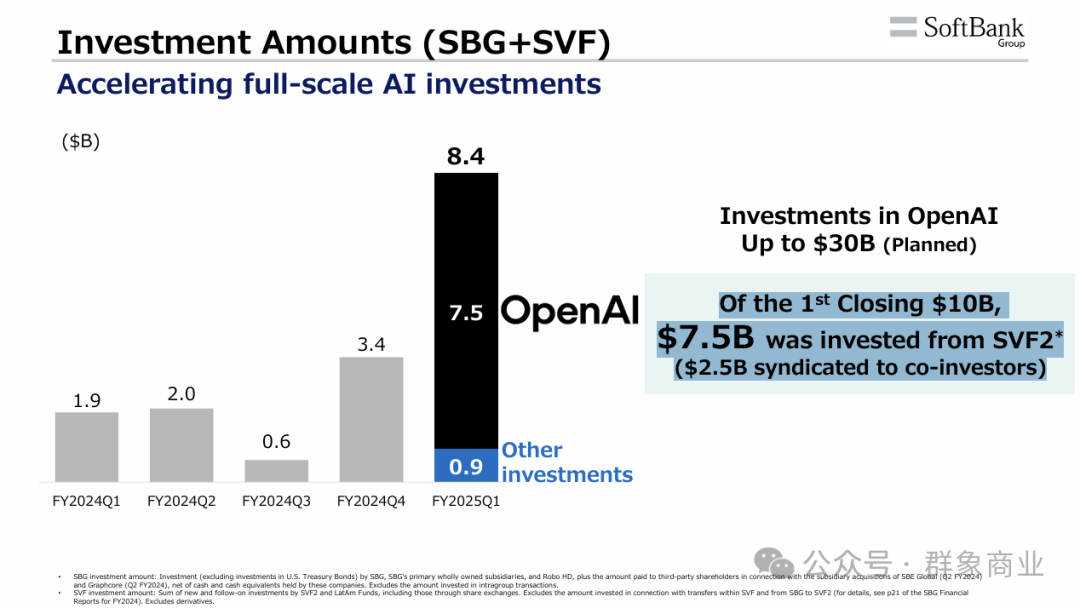

First, the most evident manifestation of its strategic determination is the aggressive investment push in the AI field. Among these, the investment in OpenAI is undoubtedly the core of this offensive. According to the financial report, SoftBank plans to invest a total of $30 billion in OpenAI, with the first phase of $10 billion, of which $7.5 billion is through the SoftBank Vision Fund 2 (SVF2), and the remaining $2.5 billion provided by a consortium of co-investors. The second phase of investment, amounting to $22.5 billion, is also on the agenda, scheduled for December 2025. The scale of this investment makes it the absolute focus of SoftBank’s recent capital expenditures.

The investment amount chart in the financial report shows that the total investment in Q1 FY2025 soared to $8.4 billion, far exceeding the total investment level for FY2024, with OpenAI alone accounting for $7.5 billion, underscoring its strategic importance.

In addition to OpenAI, SoftBank also plans to acquire server chip design company Ampere for $6.5 billion, further enhancing its landscape in AI infrastructure and application layers.

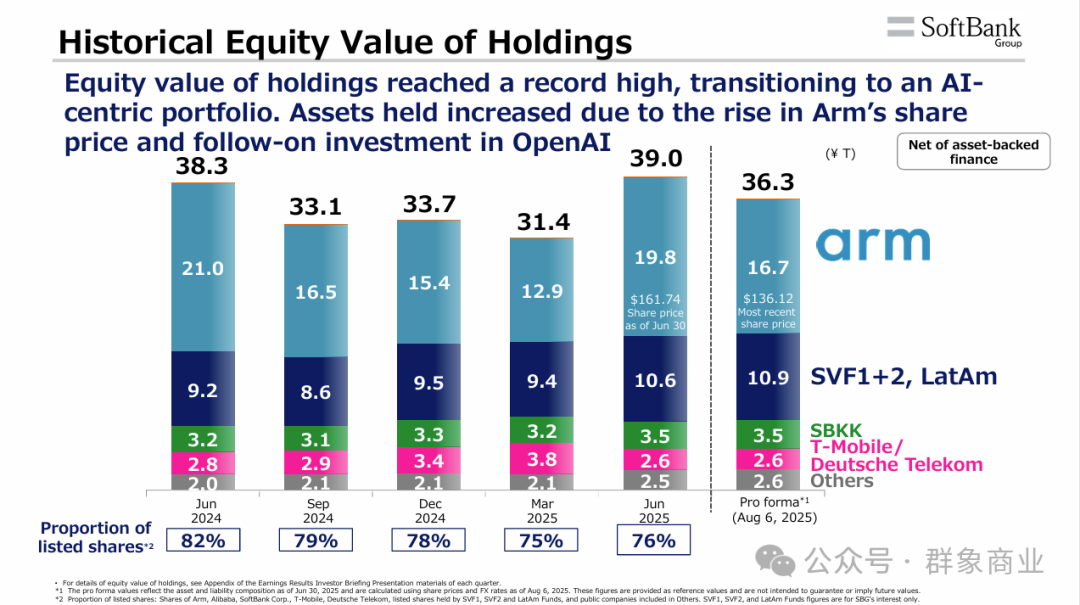

Secondly, this aggressive investment strategy has directly triggered a dramatic adjustment in the structure of its investment portfolio. According to its historical holding value chart, the total value of SoftBank’s holdings has reached a historical high of 39 trillion yen when accounting for the latest market prices. Within this vast asset portfolio, Arm’s position has rapidly risen, becoming the absolute ballast.

As of June 30, 2025, the value of Arm’s holdings has reached 19.8 trillion yen, accounting for over 50% of the adjusted total holding value, making it the most important asset on SoftBank’s balance sheet to date. In stark contrast, Alibaba, which once brought mythical returns to SoftBank, has gradually faded in its role, with the financial report indicating that all options related to Alibaba have been fully settled in physical terms.

This shift clearly outlines SoftBank’s strategic path of reallocating capital from mature mobile internet assets to high-growth AI core assets. To provide “ammunition” for new AI investments, SoftBank is also actively monetizing some existing assets, such as selling $4.8 billion worth of T-Mobile stock this quarter. This “exchange of old for new” capital reallocation operation is a key execution method for reshaping its investment portfolio.

Finally, the aforementioned strategic adjustments are fully reflected in its core financial health indicators. Despite large-scale investments, SoftBank’s overall financial condition showed some resilience this quarter. The net asset value (NAV) increased significantly from 25.7 trillion yen at the end of the previous fiscal year to 32.4 trillion yen, driven mainly by a 7.6 trillion yen contribution from Arm’s stock price increase.

More critically, the loan-to-value (LTV) ratio improved slightly from 18.0% to 17.0%. The financial report provides a detailed breakdown, indicating that Arm’s strong stock performance positively impacted the LTV by 3.9 percentage points, while the sale of T-Mobile stock contributed 1.7 percentage points of improvement, successfully offsetting a 2.8 percentage point negative impact from the investment in OpenAI.

However, the flip side is that the group’s net debt has also increased by 0.9 trillion yen, reaching 6.6 trillion yen, with the investment in OpenAI being one of the main reasons for the increase in debt. Fortunately, the group still maintains a substantial cash position of 3.7 trillion yen (approximately $25 billion), providing a buffer for subsequent investments and debt management.

Overall, SoftBank’s current situation is driven by its AI strategy, with an increasingly concentrated asset portfolio, a record high NAV, but also a simultaneous increase in debt, indicating that its overall financial structure is evolving towards a high-leverage, high-potential return direction.

“Exchange of Old for New” and “Capital Alchemy”

SoftBank Group’s strategic tilt towards the AI field is both a keen capture of market trends and relies on its years of carefully constructed, diversified, and resilient financing system. It can be said that SoftBank’s confidence in making such a heavy bet in the AI field comes from its judgment of external opportunities and its confidence in internal financial capabilities.

From the external environment, SoftBank’s decision aligns with the clear trends in the capital market. The financial report clearly states that the recent market rebound has been primarily led by “AI-related stocks.” Specific data also supports this, as from March 31, 2025, to June 30, 2025, the Philadelphia Semiconductor Index (SOX) surged by 30%, significantly outperforming the 11% increase in the S&P 500 and the 14% increase in the Nikkei Index during the same period. This market sentiment provides a favorable macro backdrop for SoftBank’s AI strategy.

More importantly, SoftBank’s core investment portfolio, particularly Arm, is one of the biggest beneficiaries of this AI wave, with its stock price performing robustly. The rise in Arm’s stock price not only serves as a direct engine for SoftBank’s NAV growth but also greatly enhances its capital strength for reinvestment, creating a positive cycle.

From an internal mechanism perspective, SoftBank’s ability to support such large-scale investments is attributed to its mature “trinity” financing strategy.

The first pillar is “leveraging held assets.” This is the core means by which SoftBank acquires investment capital. With a massive holding value of 39 trillion yen, SoftBank has ample liquidity sources. Its specific operational methods are diverse, including direct sales of holdings to achieve monetization, such as the recent sale of T-Mobile stock; and utilizing non-recourse financing, such as margin loans secured by its holdings in Arm and SoftBank stock, or using options trading on Deutsche Telekom shares to lock in funds in advance.

The financial report mentions that whether in monetizing equity in listed or unlisted companies, SoftBank has a rich operational record, enabling it to flexibly convert existing assets into incremental investment capital.

The second pillar is “leveraging cash positions.” SoftBank always maintains a substantial cash position, with 3.7 trillion yen in cash at the end of the quarter. This fund not only provides direct firepower for its investment activities but also builds a solid financial safety net. According to its financial policy, this cash is sufficient to cover bond redemptions due within the next two years, which is one of its core risk management principles.

Additionally, SoftBank has an unused $5 billion margin loan facility from Arm, further enhancing its liquidity reserves to ensure it can respond calmly to market fluctuations.

The third pillar is “leveraging debt financing.” When necessary, SoftBank prudently utilizes the debt market guided by LTV levels. Its debt financing channels are also diversified. In terms of bonds, it issues bonds in different currencies to both domestic retail investors and international institutional investors, and with its solid investor base built over the years, each issuance receives enthusiastic subscriptions.

In terms of loans, in addition to having committed credit from a banking consortium with over 25 years of cooperation, SoftBank can quickly organize syndicate loans for large acquisition projects, such as the successful $15 billion bridge loan obtained from 21 major global banks to support investments in OpenAI and Ampere.

Moreover, hybrid financing is also considered an alternative in its toolbox to optimize capital structure under different market conditions.

What firmly binds these three pillars together is the “financial policy cornerstone” that SoftBank relies on for survival. The core of this policy has two iron rules: first, during normal periods, the LTV must be maintained below 25%, and even in emergencies, it should be controlled within a maximum of 35%; second, there must always be cash available to cover bond redemptions due within two years.

SoftBank emphasizes in its financial report that for an investment holding company like itself, LTV is a more appropriate credit assessment indicator than traditional profitability or operating cash flow, as it directly reflects the coverage capacity of the company’s marketable assets that can be quickly liquidated against its total liabilities.

SoftBank believes that an LTV below 25% is an “extremely safe” level, sufficient to withstand severe market shocks like “Black Monday” or the 2008 financial crisis. It is this strict financial management that gives SoftBank the confidence and ability to decisively and massively deploy capital when seizing historic opportunities.

End of the Alibaba Era, Can AI Save SoftBank?

SoftBank Group’s current expansion strategy centered on AI is essentially a continuation and amplification of its investment philosophy of “high conviction, high leverage, high return” embedded in its corporate DNA. Looking back at its development history, whether it was the early investment in Alibaba or the integration and acquisition of Sprint, it reflects its characteristic of daring to make heavy bets on the waves of technological change when identified. From this perspective, SoftBank’s current layout is supported by a solid historical success precedent. However, unlike before, the scale of capital involved in this transformation, the concentration of assets, and the complexity of the market environment have placed SoftBank in a situation of both opportunities and challenges.

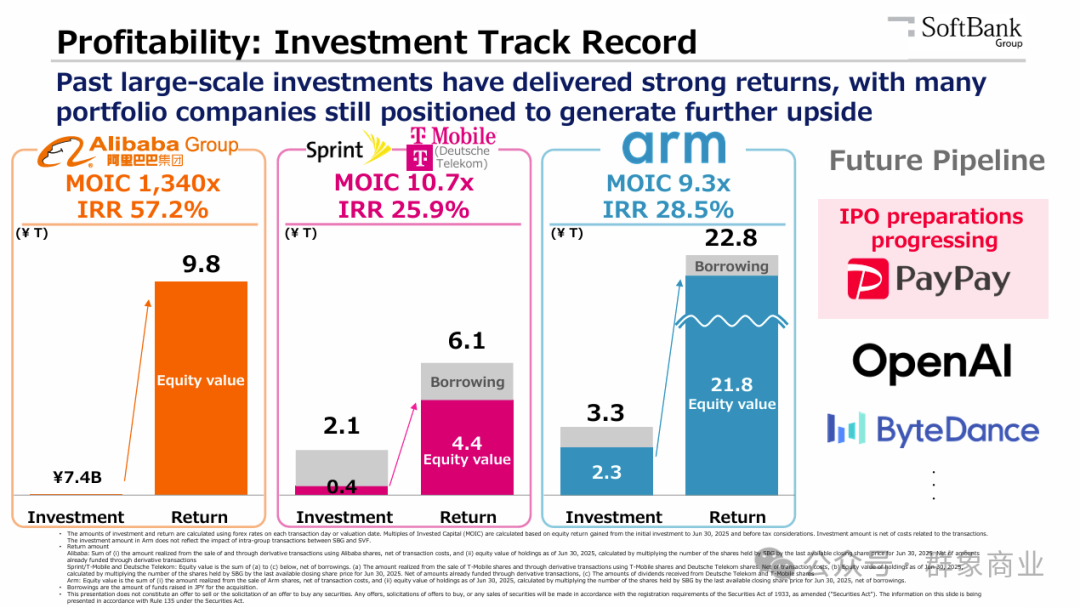

Historical success is an important source of SoftBank’s confidence. The financial report dedicates a page to showcase its past large investment successes. The initial investment of only 7.4 billion yen in Alibaba ultimately yielded an investment return multiple (MOIC) of 1,340 times and an annualized internal rate of return (IRR) of 57.2%. The acquisition of Sprint and the subsequent merger with T-Mobile also brought a MOIC of 10.7 times and an IRR of 25.9%. Even the acquisition of Arm for 3.3 trillion yen has achieved a MOIC of 9.3 times and an IRR of 28.5% to date.

These cases collectively demonstrate that SoftBank’s investment model has historically been effective. By accurately identifying and heavily investing in platform companies with disruptive potential, SoftBank can achieve excess returns far exceeding the market average. Therefore, it can be expected that the current investments in core AI companies like OpenAI are SoftBank’s attempt to replicate and surpass these historical successes.

However, the challenges are equally significant, first reflected in the increasingly acute asset concentration risk. SoftBank’s investment portfolio is becoming unprecedentedly reliant on a few companies, especially Arm. In this quarter, the stock price fluctuations of Arm alone contributed 7.6 trillion yen to SoftBank’s NAV growth.

This means that SoftBank’s net asset value is highly positively correlated with Arm’s stock performance, which is a double-edged sword. When market sentiment towards AI is high, this concentration can lead to significant amplification of returns, but once the market direction reverses, its NAV will also face the risk of severe retraction. SoftBank’s financial policy has also anticipated this possibility, admitting that LTV may face pressure due to “investment and market deterioration.” Therefore, the success or failure of the entire strategy largely depends on whether AI-related stocks can maintain high valuations in a “highly uncertain environment,” which carries considerable variability.

Secondly, there are enormous execution and financing risks. The scale of SoftBank’s announced follow-up investments is staggering, with a second phase investment in OpenAI amounting to $22.5 billion and a $6.5 billion acquisition of Ampere. This requires massive capital expenditures. Currently, the company has arranged bridge loans (including $14 billion for refinancing and the first phase of investment), but these short-term loans will ultimately need to be replaced with long-term financing tools.

SoftBank’s plan is to “orderly monetize assets” and utilize the debt market to meet these funding needs. Although SoftBank expresses full confidence in its financing capabilities, in the context of global macroeconomic and market liquidity uncertainties, whether it can smoothly and cost-effectively complete such large-scale asset sales and refinancing will be a significant test of its financial operation capabilities.

More importantly, the success or failure of these investments is not guaranteed. The financial report includes numerous disclaimers regarding forward-looking statements, warning investors of various known and unknown risks associated with investment activities.

In summary, SoftBank Group is undergoing a critical and profound strategic shift in its development history, and its Q1 FY2025 performance report is a concrete manifestation and detailed blueprint of this shift. It has resolutely bound the future of the enterprise to the wave of the AI era, marking a bold choice and an expedition full of unknowns.

SoftBank’s strategy is to maximize the use of its currently strongest weapon, a net asset portfolio led by Arm that has reached a historical high, along with an efficient and diversified financing machine, to provide funding support for winning a core position in next-generation platform companies like OpenAI.

This path not only aligns with SoftBank’s past successful investment paradigm in the high-tech field but also pushes its risk exposure to new heights. The future outcome will depend on the complex interactions of several core variables: whether the highly volatile global AI market can maintain prosperity; whether the highly concentrated investment portfolio can withstand potential market corrections; and whether the grand and complex financing and investment plans can be executed flawlessly.

SoftBank’s goal is no longer just to invest in AI but to reshape itself into an indispensable part of the AI value chain through a series of interconnected capital operations.