International investment bank research report updated on August 28, featuring 39 reports (Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, UBS, Barclays, JPMorgan, Nomura).“Original research report” can be accessed via the link at the top of the article.1. Key Highlights of the Report

-

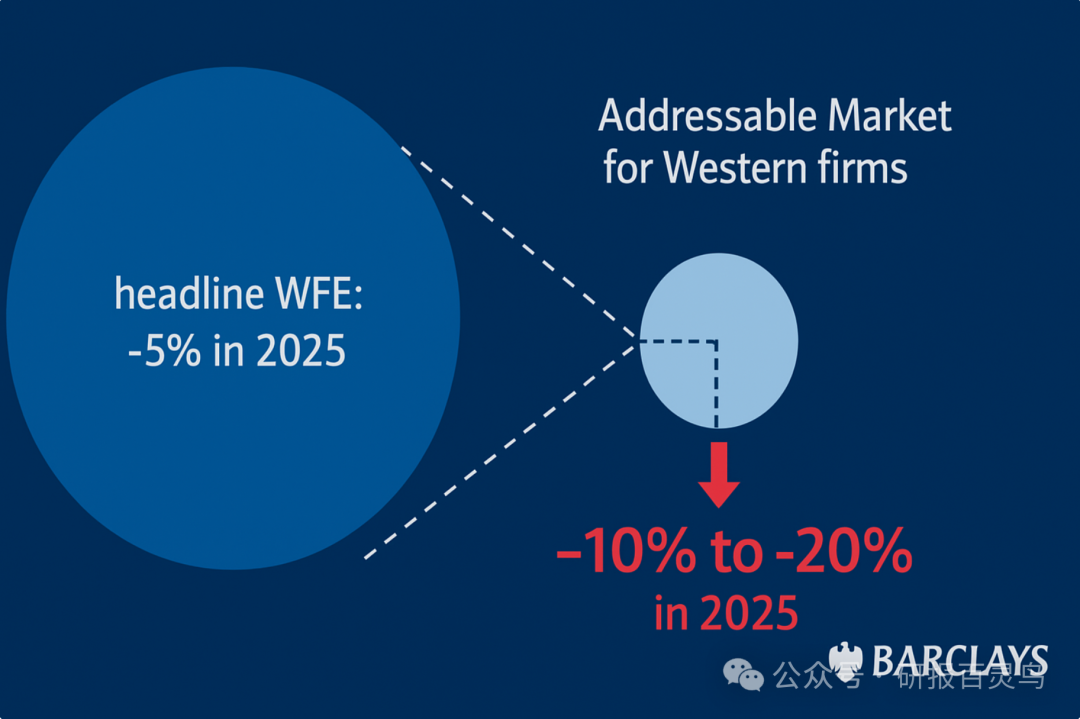

Revised expectations, but don’t celebrate too early: Barclays has raised its overall expectations for the China Wafer Fab Equipment (WFE) market. It is expected to decline slightly by 5% in 2025 (better than previously expected), with a potential recovery of 5% growth in 2026.

-

Overseas manufacturers’ “addressable market” is shrinking: The biggest warning in the report is that for overseas (especially American) equipment manufacturers, the actual “addressable market” they can compete in China is rapidly shrinking due to the dual pressures of local substitution and export controls.

Note:[Overseas manufacturers’ “addressable market”] = [Total China WFE market] – [Market share taken by local manufacturers] – [Market share lost due to export controls]

-

Data is alarming, real sentiment is colder: Barclays predicts that this “addressable market” may decline by 10-20% in 2025 and will continue to shrink in 2026. If export controls are tightened, the decline in 2026 could exceed 15%.

-

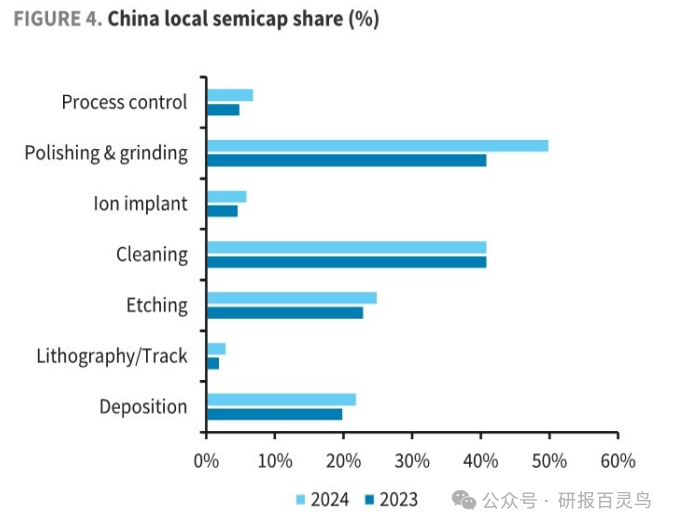

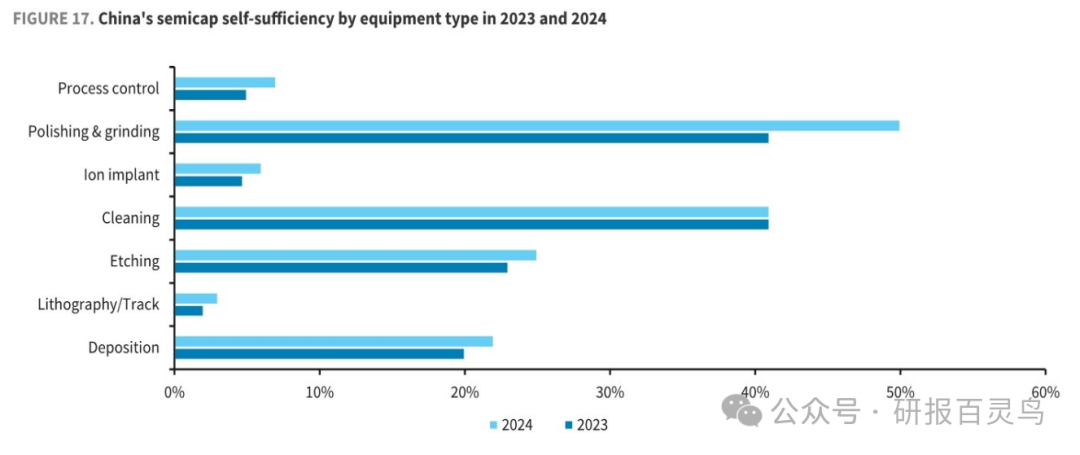

Rise of local forces: Local equipment manufacturers in China are making rapid progress, especially in polishing, grinding, etching, and cleaning, where they have captured a significant market share (some exceeding 20%), with localization rates increasing by more than 5 percentage points annually.

2. Interpretation of the Main Text

Barclays’ core argument is that investors can no longer use the macro indicator of “overall size of the Chinese semiconductor equipment market” to judge the prospects of overseas equipment companies. This is because the internal structure of the market is undergoing drastic changes. For overseas suppliers, the total size of the cake seems to remain largely unchanged, but their share is being rapidly taken away. This is a structural change, not a cyclical one.

Analysis: The report describes the historic opportunity window we are currently in. The market that overseas manufacturers are “losing” is precisely the battlefield that local equipment manufacturers “must win.” The external restrictions brought about by geopolitical factors have objectively broken the long-standing path dependence of customers on overseas equipment, giving domestic manufacturers an unprecedented opportunity to validate (Verification) and iterate in core production lines.

Logic 1: The huge gap between the overall market (Headline) and the addressable market

The report clearly provides two sets of distinctly different forecast data. The overall market is expected to decline by only 5% in 2025, while the addressable market for overseas manufacturers may decline by 10% to 20%. The report also specifically distinguishes suppliers from different regions: due to stricter export controls, the addressable market for American suppliers is expected to shrink by 20% in 2025, while European/Japanese suppliers are in a slightly better position, with an expected decline of 10%.

Analysis: The 20% share that American suppliers are expected to lose is the core target that domestic manufacturers need to quantify and compete for. This means that it becomes clear which customers have the most urgent supply chain security needs and which production lines have opened up equipment replacement windows. The stricter the external restrictions, the longer the potential customer list for domestic manufacturers becomes. The task for domestic manufacturers is to proactively strike, using reliable product performance, rapid response services, and localized supply chain advantages to fill the market vacuum that has been “squeezed” out.

Logic 2: The ongoing process of localization substitution

The report points out that the localization rate of Chinese equipment has reached about 15% in 2023, and is expected to exceed 20% in 2024. In terms of sub-sectors, polishing & grinding is progressing the fastest, with local share approaching or even exceeding 50% by 2024; cleaning and etching have also made significant progress. However, in high-end fields such as lithography, atomic layer deposition (ALD), and process control, the local share remains below 10%, which is a clear shortcoming.

Analysis: The report validates that the “single-point breakthrough, systematic advancement” strategy for localization is entirely correct. Breakthroughs in polishing, etching, and other fields have accumulated data from large-scale stable operations on production lines and customer trust. The shortcomings pointed out in the report are clear directions for national R&D investment and resource concentration. Domestic manufacturers are closely collaborating with leading domestic wafer fabs as “R&D partners” to tackle challenges together, aiming to break through in these most difficult areas and build a complete local equipment ecosystem.

Logic 3: Shift in investment focus

The report dissects the composition of China’s WFE in 2025, where logic chips account for 70% and memory chips account for 30%. In terms of technology nodes, mature processes (Lagging edge) account for as much as 59%, making it the absolute investment mainstay.

Analysis: The mature process market is vast, with relatively short technology validation cycles, making it the core battleground for domestic manufacturers to achieve scaled revenue, dilute R&D costs, and cultivate engineering teams. This creates a powerful “growth flywheel” for domestic manufacturers: Winning orders in mature processes -> Generating stable revenue and massive application data -> Supporting R&D for more advanced technologies -> Entering advanced process production line validation with established customer trust -> Ultimately achieving breakthroughs across the entire product line. The mature process market is the “strategic depth” on which domestic manufacturers rely for survival and development, providing a solid foundation for climbing to more advanced nodes.

📈 Investment Advice: Focus on “Low Substitution Risk + High Growth Tracks”, Beware of Regulatory Upgrades Impact

The report suggests a more cautious attitude towards overseas semiconductor equipment companies that are highly dependent on the Chinese market, especially those whose products overlap significantly with local manufacturers. The report specifically points out that “LRCX and KLAC have more widespread business in China, while AMAT is expected to see a decline sooner.”

ASML, with its monopoly position in lithography, has extremely low substitution risk in the short term. However, companies like ASMI, while having advantages in the ALD field, should also be wary of potential breakthroughs by Chinese manufacturers in the coming years.

3. My Brief Commentary

The “resilience” of the Chinese semiconductor WFE market has been validated. Understanding the Chinese semiconductor market can no longer rely solely on growth rates and total volume; it is essential to consider structure and flow. For global semiconductor equipment manufacturers, the Chinese market is rapidly transforming from an open “blue ocean” into a complex, competitive “ecological tank”. Whether they can survive and thrive in this new ecosystem will greatly test each manufacturer’s technological moat and strategic adaptability.