01

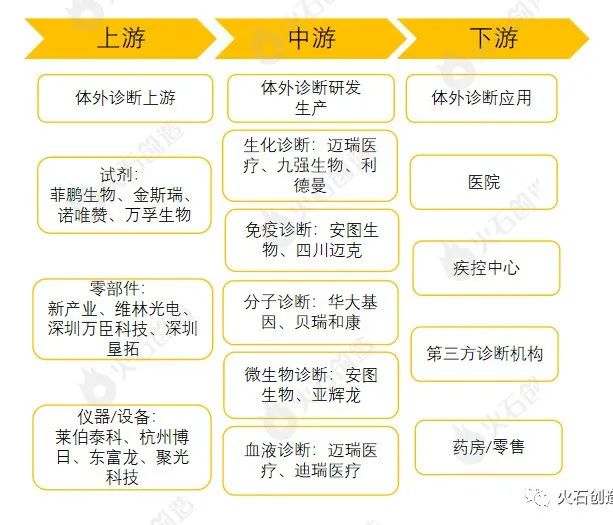

In Vitro Diagnostic Industry Chain Overview

The upstream of in vitro diagnostics mainly includes R&D and production of raw materials, reagents, and core components required for in vitro diagnostics., reagents include antigens, antibodies, biological enzymes, and magnetic microspheres, while core components include single-photon counting modules, lasers, sensors, plunger pumps, and sheath flow cells. The instruments for testing and producing in vitro diagnostics include PCR machines, biochemical analyzers, and POCT testing devices.The midstream of in vitro diagnostics generally refers to companies that develop and produce in vitro diagnostic reagents and instruments, which are divided into biochemical diagnostics, immunodiagnostics, molecular diagnostics, microbiological diagnostics, and blood diagnostics. Currently, the domestic focus is primarily on the first three types of diagnostics.The downstream of the in vitro diagnostic industry chain is applied in medical institutions, third-party medical laboratories, and pharmacies/retail.

Figure 1: In Vitro Diagnostic Industry Chain MapSource: Huoshi Chuangzao Industry Research InstituteUpstream field imports are heavily monopolized, domestic companies such as Feipeng Bio, Wanfu Bio, Hanhai New Enzyme, and Nuovizhan can provide essential raw materials and reagents for in vitro diagnostic R&D and production. Domestic companies are also continuously developing and advancing in the core components field, with certain market shares already established in the mid-to-low-end products. New Industry, Weilin Optoelectronics, Wancheng Technology, and Shenzhen Kentuo are representatives in this category, while companies producing instruments required for in vitro diagnostics include Borui, New Industry, and BGI Manufacturing. The midstream in vitro diagnostic companies have formed leading enterprises represented by Mindray Medical, Jiukang Bio, Lide Man, Antu Bio, and Yanhuilong.02

Regional Distribution of In Vitro Diagnostic Industry Chain

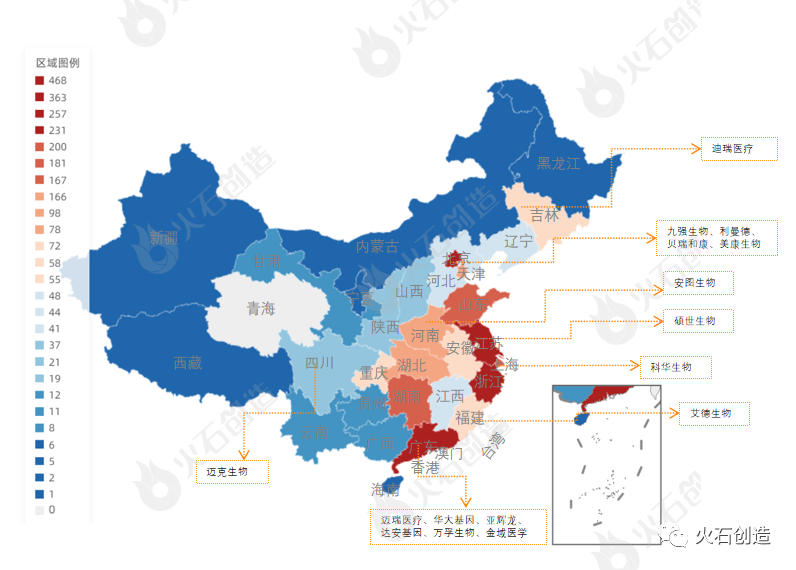

The following chart selects midstream R&D and production companies in the in vitro diagnostic field for statistics. The results show that there are a total of 2726 in vitro diagnostic R&D and production companies, exhibiting regional clustering characteristics, mainly distributed in Beijing and the Yangtze River Delta, Pearl River Delta regions, where the upstream in vitro diagnostic industry is dense, and funds and talents are concentrated, leading to the clustering of in vitro diagnostic R&D and production companies. The distribution of representative enterprises in in vitro diagnostics also conforms to the above characteristics.

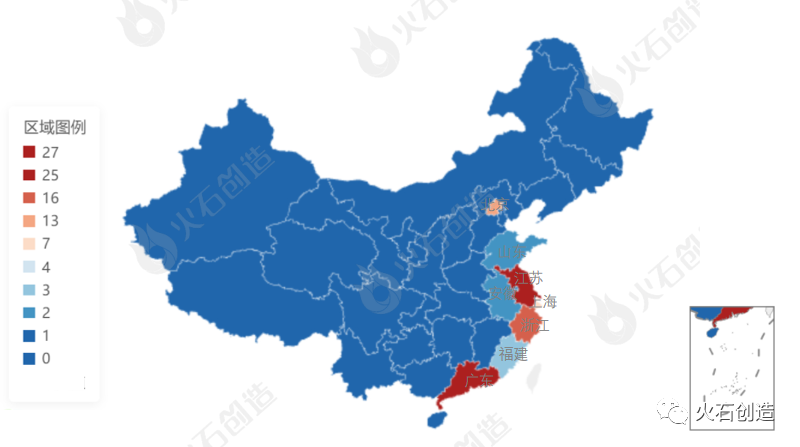

Figure 2: Distribution of In Vitro Diagnostic R&D and Production EnterprisesSource: Huoshi Chuangzao DatabaseIn vitro diagnostic R&D and production enterprises have experienced 102 financing events, From the financing distribution map, it can be seen that the financing event occurrence rate is highest to lowest in Jiangsu Province, Guangdong Province, Zhejiang Province, and Beijing, also showing regional dense distribution characteristics. Jiangsu Province, due to its advantages in capital, technology, enterprises, and talent concentration, maintains rapid development in the field of in vitro diagnostic R&D.

Figure 3: Distribution of In Vitro Diagnostic Enterprises’ FinancingSource: Huoshi Chuangzao Database03

Trends

Overall, the scale of in vitro diagnostic companies in China is small and distribution is relatively scattered. With economic development and the increasing importance of health among the public, the industry has developed rapidly in recent years, and the outbreak of the pandemic has further increased the market scale of the in vitro diagnostic industry. The upstream core components and raw materials have long relied on imports. Currently, although domestic products have formed a pattern of domestic substitution in the low-end reagent field, the high-end market is still mainly controlled by foreign enterprises. A number of domestic companies represented by Mindray Medical, BGI Genomics, and Wanfu Bio are gradually encroaching on the market of overseas giants through continuous technological improvements and expanding competitive fields, with the hope of achieving more domestic substitutions in various subfields of in vitro diagnostics in the future.

Mass Spectrometry Development Expected to Open

A New Chapter for the IVD Industry

In recent years, the strong demand for testing in hospitals contrasts sharply with the slowing growth of IVD (in vitro diagnostic products) companies, with severe homogenization of mid-to-low-end products and increasingly fierce competition. We believe that two types of companies can emerge victorious in the fierce competition: one type is quality channel holders, and the other is high-tech pioneers. Mass spectrometry, as a gradually emerging high-end field in clinical testing, represents the latter voice and is expected to inject new vitality into the Chinese IVD market in the future.

Reasons

① High-end quantitative methods, domestic breakthroughs expected to lead the service end

Mass spectrometry analysis, as a high-end quantitative detection method, has strong advantages in sensitivity, specificity, analysis speed, and simultaneous detection of multiple indicators, which can technically replace some traditional detection methods in clinical practice. Due to reasons such as core patents and manufacturing processes, the production side still mainly relies on imported brands in the short term, with the domestic rate below 2%. Similar to high-end detection equipment such as “gene sequencing”, domestic breakthroughs are expected to occur first at the service end.

② Clinical testing, a new blue ocean market of 12.5 billion

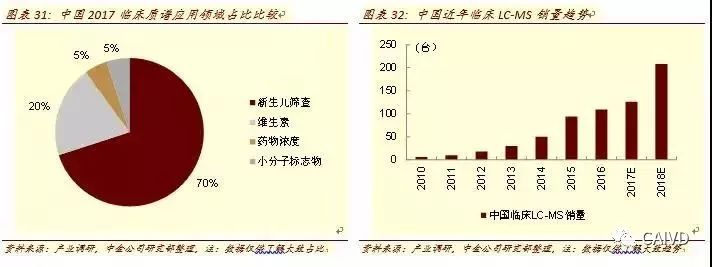

Domestic clinical testing using mass spectrometry is mainly applied in areas such as newborn genetic screening, vitamin D detection, microbiological diagnostics, and drug testing, with corresponding market spaces of 2.2 billion, 7.6 billion, 2.1 billion, and 600 million respectively. We initially estimate that clinical testing using mass spectrometry will be a blue ocean market exceeding 10 billion. Current mainstream service providers include KingMed Diagnostics, Dian Diagnostics, and other leading traditional medical diagnostic laboratories. Due to the high acquisition costs of 2-3 million RMB and the high requirements for data accumulation, it is expected that the domestic market will ultimately form an oligopoly market structure.

③ Clinical self-built projects (LDT) expected to open a broader market

Referring to the U.S. experience, the development of clinical testing using mass spectrometry is inseparable from the rise of independent clinical laboratories (ICL) and the improvement of clinical self-built projects (LDT). After the ICL has scaled up, it has the capacity to purchase expensive equipment and can achieve sample scaling through chain laboratories; LDT makes clinical testing using mass spectrometry more diversified, enriching the testing projects. After nearly 10 years of development, domestic ICLs have taken shape, and the gradual relaxation of LDT will open up broader space for the application market of clinical mass spectrometry.

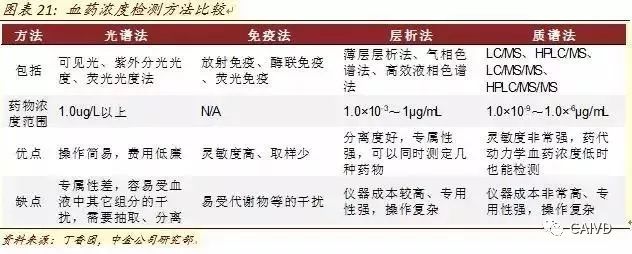

Mass spectrometry analysis——an excellent high-end quantitative detection method

Mass spectrometry analysis refers to a high-end quantitative detection method that weighs the mass of ions.

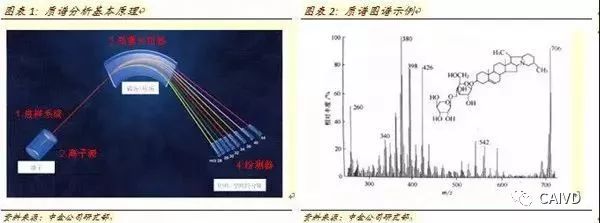

Mass spectrometry analysis method refers to the ionization of sample molecules, using the different forces acting on ions with different mass-to-charge ratios (m/z) in an electric or magnetic field to change their direction of motion, thus separating them spatially, and finally collecting and detecting these ions to obtain mass spectrometry graphs, achieving the purpose of analysis.

Mass spectrometry graphs have the horizontal axis representing the mass-to-charge ratio (m/z); the vertical axis represents the ion flow intensity, usually expressed in relative intensity (relative abundance). The relative abundance is defined as 100% for the strongest ion flow intensity, and other ion flows are displayed as a percentage. The analysis of mass spectrometry graphs requires strong professional reading ability, and major mass spectrometry manufacturers also provide corresponding mass spectrometry databases and analysis services.

High technical barriers, production side still mainly relies on imported brands

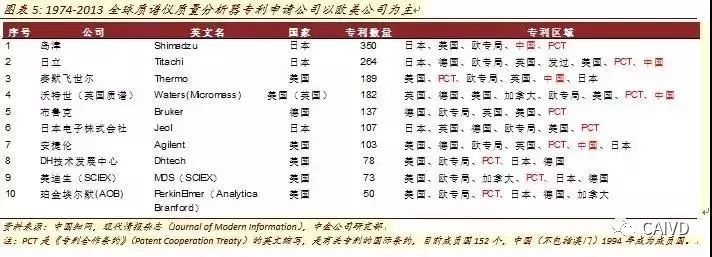

The patent applications for core technologies abroad experienced a significant explosion in the 1980s. In 1912, J.J. Thomson developed the first mass spectrometer to identify the neon element and its isotopes. Over the past 100 years, the technology and application areas of mass spectrometry have been continuously improved. Early mass spectrometers were mainly used for isotope determination and inorganic analysis, and from the 1940s began to be used for organic analysis; in the 1960s, the first combination of gas chromatography and mass spectrometry (GC-MS) emerged, and mass spectrometry became an important method for organic analysis. In the 1980s, with the addition of computers and various technological upgrades, mass spectrometry developed rapidly worldwide and was applied in a wider range of fields.

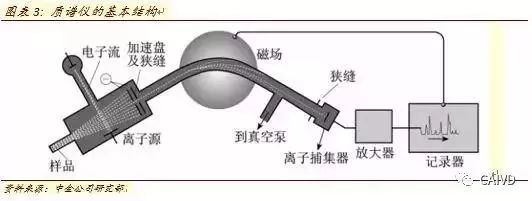

Mass spectrometers (Mass Spectrometry) generally consist of four parts: Inlet System, Ion Source, Mass Analyzer, and Ion Detector. Among them, the ion source and mass analyzer are the technical cores of the mass spectrometer. A detailed comparison of different ion sources and mass analyzers is provided in the appendix.

Currently, there is still a significant gap between domestic mass spectrometers and imported brands, especially regarding the core patents of ion sources and mass analyzers from international mainstream mass spectrometry manufacturers, which remains a key factor restricting the development of domestic mass spectrometry equipment in the short term. From the perspective of global mainstream mass spectrometry manufacturers, Waters, Agilent, Thermo Fisher Scientific, Bruker, etc., all have patent protection in the Chinese market.

The level of domestic production is relatively low, and the production side still mainly relies on imported brands. Compared to the more than 100 years of development history abroad, the development of mass spectrometry technology in China started relatively late, and the talent reserve is relatively insufficient. It was not until after 2000 that mass spectrometry technology began to accumulate. In 2006, Beijing Dongxi Analytical Instrument Co., Ltd. launched the GCMS-3100, the first commercial mass spectrometry product in China.

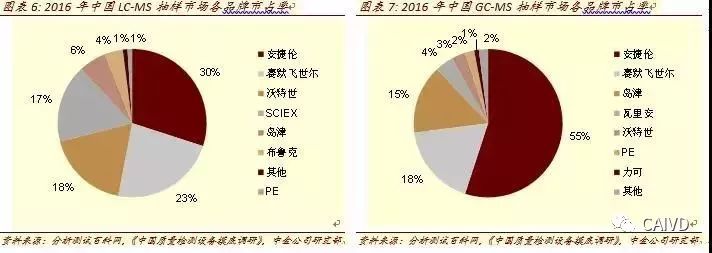

Currently, the market share of domestic mass spectrometers is relatively low. In a 2016 sampling survey, the domestic rate of LC-MS and GC-MS was less than 2%. We expect that before the expiration of core patents or significant technological breakthroughs in domestic devices, the domestic mass spectrometry market will still be dominated by imported brands. In the short term, for the medical clinical testing market, the MALDI-TOF MS used for microbial detection has seen relatively rapid development in recent years.

In recent years, the production of MALDI-TOF mass spectrometry in China has made certain breakthroughs, including the first market-listed clinTOF I from Yixin Bochuang, as well as products from Rongzhi Bio, Antu Bio, Hexin Instruments, and Dongxi Analytical, all of which have successively submitted product registrations or launched products. We believe that similar to the import substitution in the field of chemiluminescence, the success of domestic mass spectrometry import substitution still needs to be tested by the market.

Clinical Testing

The 12.5 billion blue ocean market of mass spectrometry service end

Mass spectrometry clinical testing, a new emerging field in the 10 billion IVD market.

The global market for mass spectrometers is relatively stable. In 2016, the equipment market was estimated to be 5.3 billion USD, and it is expected to reach a market size of 7.7 billion USD by 2021, with a compound annual growth rate of approximately 7.9%. The domestic mass spectrometer market is still in the early stages of development, with approximately 98% of mass spectrometers still being imported brands. Based on customs data, it is estimated that the mass spectrometer market in China was around 450 million USD in 2016.

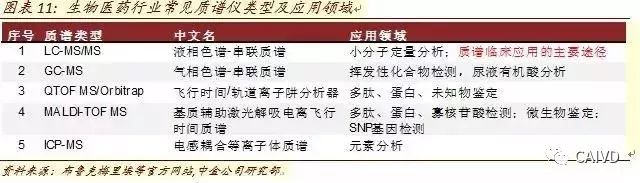

Biomedical is the third largest application field for mass spectrometry, accounting for about 6%, while others are mainly used for detection in traditional fields such as environment and semiconductors. In biomedicine, especially in clinical testing, the application is still in the early stages of development. The types of mass spectrometers commonly used in biomedicine mainly include LC-MS/MS, GC-MS, QTOF-MS/Orbitrap, and MALDI-TOF, among which LC-MS/MS is the main application model for clinical testing.

In 2008, Waters launched the tandem mass spectrometry newborn screening system in China, which was the first mass spectrometer approved for clinical application by the CFDA. In the following years, companies such as Bruker, Merieux, and AB SCIEX began to layout in the field of clinical mass spectrometry in China. Domestic companies such as Yixin Bochuang, Sairdi, and Yicheng Mudi have also made certain breakthroughs in registration, but as of now, domestic clinical mass spectrometry is still mainly dominated by imported brands.

Compared to traditional immunoassays, mass spectrometry testing has strong advantages in sensitivity, specificity, analysis speed, and simultaneous detection of multiple indicators. There is significant development potential in areas such as newborn genetic metabolic disease screening, vitamin and hormone testing, therapeutic drug monitoring, and microbial identification. We expect the initial mass spectrometry testing market to be a new market exceeding 10 billion, and the further opening of market space will require support similar to the LDT system in the U.S.

Main application area one:

Newborn Genetic Metabolic Disease Screening——2.2 billion market space

Genetic metabolic diseases are caused by genetic defects in the synthesis of certain enzymes, receptors, carriers, and membrane pumps composed of peptides and/or proteins that are necessary for maintaining normal metabolism. The purpose of newborn genetic metabolic disease screening is early diagnosis and treatment to avoid unfortunate occurrences such as dementia and defects.

The American College of Medical Genetics (ACMG) includes 54 genetic diseases in the newborn screening program, with 29 primary diseases and 25 secondary diseases, widely using LC-MS/MS for screening.

Domestic genetic metabolic diseases that enjoy subsidies include phenylketonuria (PKU), congenital hypothyroidism (CH), and in some southern regions, congenital adrenal hyperplasia (CAH) and glucose-6-phosphate dehydrogenase deficiency (G-6-PD). More than 40 other tests are self-funded and can be selected based on family history of genetic diseases.

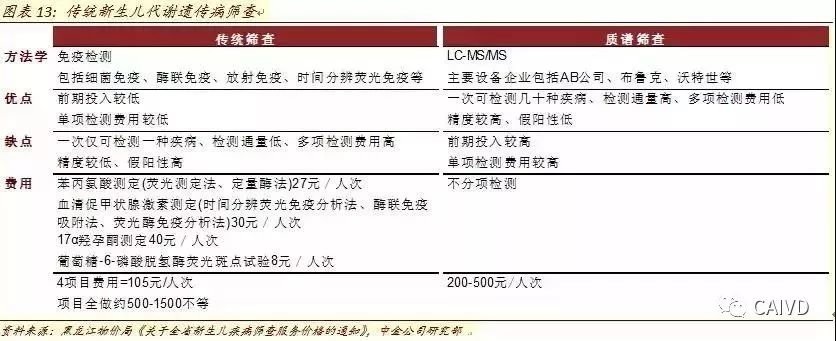

The advantage of mass spectrometry is its ability to test multiple diseases with one blood sample. Traditional newborn genetic metabolic disease screening often uses immunoassay methods to test one disease at a time. Currently, the common model in various regions is to add tests based on government-subsidized projects according to family history of genetic diseases. Currently, domestic genetic disease screening involves more than 40 items, and considering that decision-making parents may not be very familiar with family disease history, if 40 tests need to be done, the comprehensive cost can be as high as 500-1500 RMB per person.

Mass spectrometry testing does not require testing for each disease individually; it can complete multiple test items with just one sample. The market is still in the early stages of development, with differences in testing items and costs ranging from 200-500 RMB per person. In the short term, compared to the simple traditional screening of 3-4 diseases, the cost is still relatively high. However, in the future, as the number of newborn screening test items increases, the operational and cost advantages will become increasingly apparent.

Newborn metabolic genetic disease mass spectrometry testing, 2.2 billion market space. Between 2003 and 2013, the number of newborns in China fluctuated around 16 million annually. In 2016, the number of newborns in China reached 18.46 million. Considering the ongoing impact of the two-child policy, we expect the number of newborns in the future to exceed 18 million annually. In 2007, the national average screening rate for newborns was 39%, exceeding 50% in 2010, and we expect the screening rate to reach nearly 70% in 2016. With a 40% penetration rate for mass spectrometry testing and an average cost of 300 RMB per person, the market space is approximately 2.2 billion RMB. We expect that as the penetration rate of mass spectrometry testing increases, the potential space will be vast.

Main application area two:

Vitamin D Testing——Market space exceeding 7.6 billion

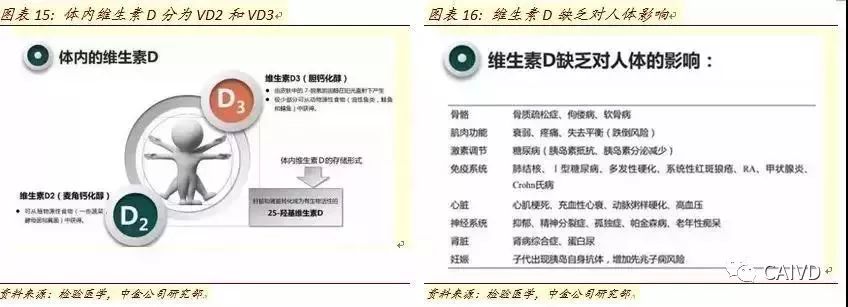

Vitamin D is an important health indicator, and testing is not yet widespread in China. Vitamin D is a steroid derivative, which can be subdivided into vitamin D2 and vitamin D3. In the human body, it promotes the absorption of calcium and phosphorus in the intestines, increases blood calcium levels by enhancing renal tubular absorption of calcium and phosphorus, and, when blood calcium is too low, works with parathyroid hormone (PTH) to promote the release of calcium and phosphorus from bones.

Long-term vitamin D deficiency can lead to rickets, osteoporosis, osteomalacia, and other diseases. Recent studies have also shown that vitamin D deficiency is linked to tumors, hypertension, diabetes, and other complications. Regularly testing vitamin D levels is significant for disease prevention, and some European and American countries have included vitamin D in routine examinations.

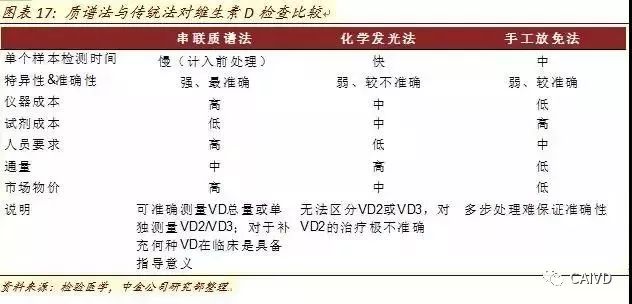

The mass spectrometry method is the gold standard for vitamin D testing. In the body, vitamin D2 and vitamin D3 are transported to the liver through the bloodstream, where they are converted into 25-hydroxyvitamin D (25(OH)D) by liver enzymes, and then transported to the kidneys for a second hydroxylation into 1,25(OH)2D. The content of vitamin D2 in the human body is relatively low. Traditional methods such as radioimmunoassay, competitive protein binding method, and chemiluminescence method test the total amount of 25(OH)D in the blood, with poor specificity and resistance to matrix interference, and cannot simultaneously detect 25(OH)D2 and 25(OH)D3, thus failing to accurately reflect the vitamin D situation. This is one of the main reasons why vitamin D testing has not been widely developed in China. Tandem mass spectrometry is currently recognized globally as the gold standard for vitamin D testing.

Vitamin D testing is widely applicable, with a market exceeding 7.6 billion for mass spectrometry testing.

The applicable conditions are broad. In theory, any diseases or potential diseases associated with vitamin D require vitamin D testing, mainly including: 1) patients at high risk of bone loss, including osteoporosis, osteomalacia, rickets, fractures, and elderly people who have fallen recently; 2) patients with insufficient endogenous vitamin D production, including those who are bedridden for long periods, have reduced sun exposure, or belong to darker-skinned populations; 3) patients with abnormal vitamin metabolism, including obese patients, pregnant and breastfeeding women, hormone therapy, malabsorption syndrome, liver failure, granulomatous diseases, chronic kidney disease patients, and kidney transplant patients.

The mass spectrometry testing market exceeds 7.6 billion. In actual operation, vitamin D testing mainly targets perinatal women, newborns, and the elderly over 60. Traditional vitamin D testing costs vary between 100-200 RMB depending on the level of hospitals and methodologies. Assuming a cost of 150 RMB per person for vitamin D testing, with penetration rates of 40% for perinatal women, 40% for newborns, and 5% for elderly people over 60, the market for vitamin D mass spectrometry testing is estimated to be at least 7.6 billion RMB.

Main application area three:

Microbial Diagnostics——Market space of 2.1 billion

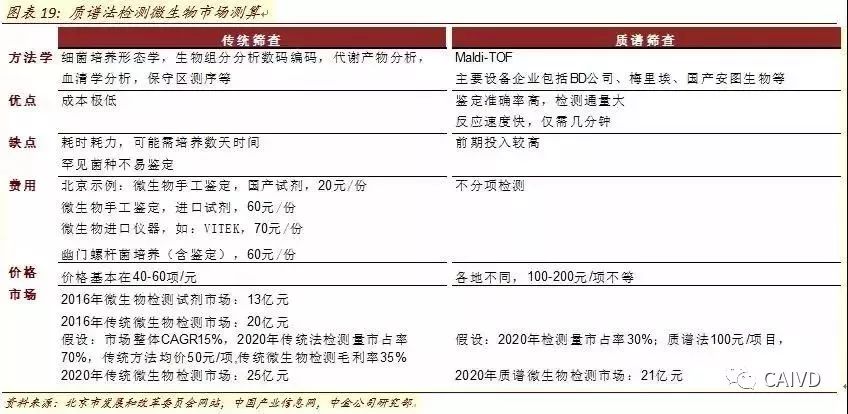

Microbial diagnostics refers to providing evidence for the prevention, diagnosis, treatment, and efficacy observation of clinical infectious diseases through pathogen and drug sensitivity analysis. Traditional rapid microbial diagnostics include three methods:

1) Direct detection of samples, such as PCR testing;

2) Detection after enriching bacterial bodies;

3) Detection after isolation and culture.

Results can be obtained in minutes, showing significant time advantages. Traditional detection methods require the screening and culture of strains, which can take several days, consuming time and effort, and the experimental procedures are relatively cumbersome. Mass spectrometry microbial testing has a significant advantage in waiting time, and one experiment can test multiple samples simultaneously, greatly improving accuracy and detection throughput, with broad replacement space in the future.

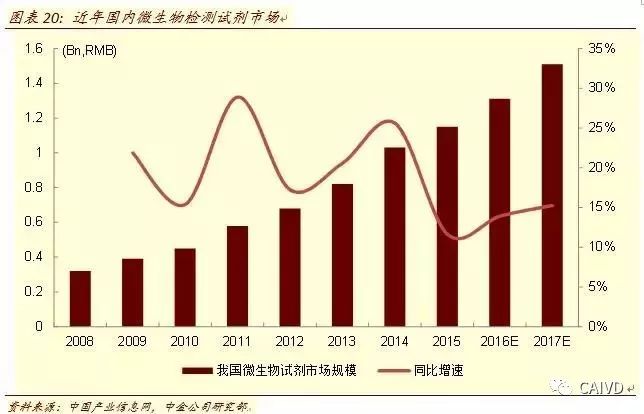

2.1 billion technology upgrade replacement space. In 2016, the domestic microbial testing reagent market was approximately 1.3 billion. Referring to the gross profit margin disclosed by KingMed Diagnostics, we estimate that the industry’s microbial testing gross profit margin is around 35%, so the microbial testing market in 2016 was about 2 billion. Considering the future increase in penetration of mass spectrometry testing (30%) and approximately double the price factor, we estimate that the microbial testing market for mass spectrometry will be around 2.1 billion by 2020.

Main application area four:

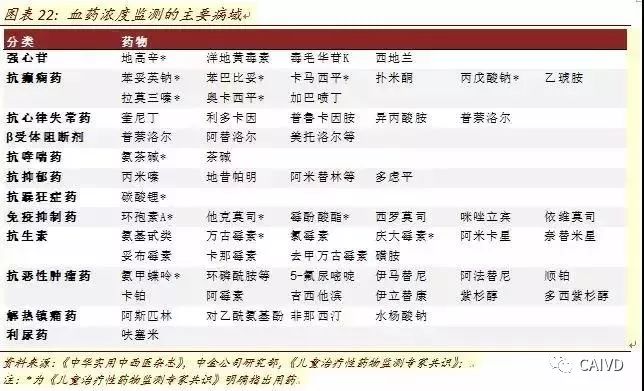

Drug Testing——Market space of 600 million

Drug testing (therapeutic drug monitoring, abbreviated as TDM) refers to monitoring drug efficacy during clinical drug treatment while collecting blood drug concentrations (or urine, saliva, etc.) to optimize the dosing scheme, achieving satisfactory efficacy and avoiding toxic side effects.

The mass spectrometry method is the most precise method for blood drug concentration testing. Blood drug concentration is the main reference index for TDM. Currently, the main methods for blood drug concentration testing include spectroscopy, immunoassay, chromatography, and mass spectrometry, among which mass spectrometry can be understood as an upgrade of chromatography, with mass spectrometry serving as the analyzer for samples post-chromatography. Compared to traditional methods, mass spectrometry is a more sensitive and accurate detection method, although the initial investment in equipment and operational requirements for personnel are relatively high. Cost factors are the main reason for its widespread promotion.

Theoretically, drugs that need TDM include 1) drugs with a low therapeutic index and narrow safety range, with strong toxic reactions; 2) drugs with significant individual differences in pharmacokinetics; 3) drugs with nonlinear pharmacokinetic characteristics; 4) long-term use drugs where efficacy is not easily judged quickly.

Domestic TDM development is still in its early stages. Existing clinical guidelines include the 2011 “AGNP Consensus Guidelines for Monitoring Psychiatric Drugs: 2011” which clearly lists 128 psychiatric drugs; the 2015 Chinese Medical Association Clinical Pharmacology Group’s “Expert Consensus on Therapeutic Drug Monitoring in Children” which identifies 15 drugs, etc.

600 million market space. We estimate that the domestic psychiatric mass spectrometry testing market is about 540 million, and the mass spectrometry testing market for immunosuppressive drugs in organ transplantation is about 3 million, totaling around 600 million when combined with other small drug markets.

Pushing the ICL platform

Waiting for the LDT system to open up greater space

The rise of clinical laboratory self-built projects (LDT) has brought prosperity to clinical mass spectrometry in the U.S.

The development of clinical testing using mass spectrometry in the U.S. is inseparable from the rise of independent clinical laboratories (ICL) and the improvement of clinical self-built projects (LDT). On the one hand, under the gradually maturing regulations for clinical laboratory management, the chain of independent clinical laboratories has accelerated, and the scale effect not only enables the purchase of expensive high-end testing equipment but also brings a large number of chain testing samples; on the other hand, CLIA opens up clinical laboratory self-built projects (LDT), making it possible for mass spectrometry to conduct clinical testing in broader fields.

The rapid development of independent clinical laboratories in the U.S. enables high-end equipment testing.

In the U.S., there are mainly three types of laboratories responsible for medical testing: Physician Office Laboratories (POL), Independent Clinical Laboratories (ICL), and hospital internal laboratories. Among them, POL and small laboratories set up by physicians are relatively stable, while the latter two, independent clinical laboratories and hospital internal laboratories, are large laboratories capable of conducting clinical mass spectrometry LDT.

The number of POL laboratories is relatively stable. With the promulgation of the revised Clinical Laboratory Improvement Amendments (CLIA) in 1988, laboratory management has become increasingly standardized, and non-POL laboratories represented by independent clinical laboratories have developed rapidly. Quest and Labcorp, independent clinical laboratories in the U.S., have rapidly expanded through chain development, and by the end of 2017, they accounted for nearly 40% of the U.S. medical testing market.

Scaling up makes high-end equipment acquisition possible. Scaling not only alleviates procurement cost pressure but also makes large-scale sample collection possible. We conducted a return on investment scenario analysis for a mass spectrometer costing around 2 million, assuming a 5-year depreciation with a residual value of 0 after 5 years. The annual operational costs for personnel, consumables, and equipment maintenance are 50,000 RMB/year, and the single project fee is 100 RMB. Therefore, the sample volume required to recoup the investment within 5 years is at least 4,500 samples. Considering that the equipment development cycle is around 3 years, if the equipment is eliminated after 3 years, nearly 7,200 samples will be needed annually. For a single project, secondary hospitals generally face significant sample pressure. The development of independent clinical laboratories provides the possibility for the clinical application of mass spectrometry.

The development of LDT allows for wider application of clinical mass spectrometry testing.

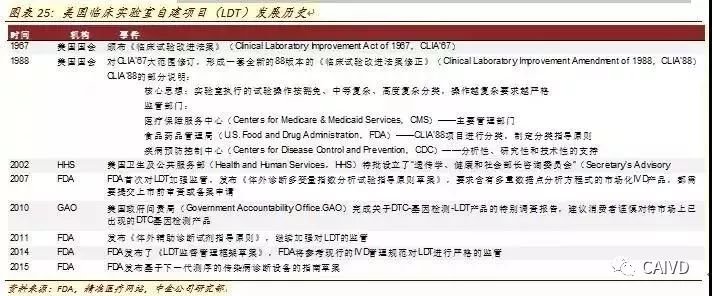

Definition of Clinical Laboratory Developed Tests (LDT). The American Society for Clinical Pathology (ASCP) defines it as: in vitro diagnostics developed, validated, and used internally in laboratories for diagnostic purposes. LDT can only be used within the laboratory that developed it and can use purchased or homemade reagents, but these reagents cannot be sold to other laboratories, hospitals, or physicians. The implementation of LDT does not require FDA approval. Commercially available kits or testing systems approved by the FDA, if modified in any way during clinical laboratory use, must also comply with all applicable management rules for LDT. Europe does not have a clear concept of LDT, and it is more reflected in the form of in-house reagents.

The rise of LDT to some extent adapts to the development of precision medical testing. The development of medicine has undergone two historical transformations: the establishment of evidence-based medicine, which systematically corrects traditional medicine; and the establishment of precision medicine, which provides individualized supplements to evidence-based medicine. Translational medicine and personalized medicine have gradually become the driving forces of modern precision medicine. Clinical laboratory developed projects (LDT) based on molecular, genetic, and proteomics technologies provide possibilities for some high-end technologies to move from the laboratory to clinical applications.

The development of LDT in the U.S. began with the first laboratory management act, the Clinical Laboratory Improvement Amendments (CLIA) enacted by Congress in 1967. Entities that meet CLIA qualifications (mainly laboratories) are the initial prototypes of LDT, which are IVD products designed, prepared, and used independently. In 1988, Congress revised the act to meet laboratory development requirements, which is the current 88 version of CLIA, with the Centers for Medicare & Medicaid Services (CMS) responsible for supervision, and the FDA and CDC assisting. Between 1990 and 2015, the FDA gradually strengthened its regulation of the CDT industry and improved corresponding management specifications.

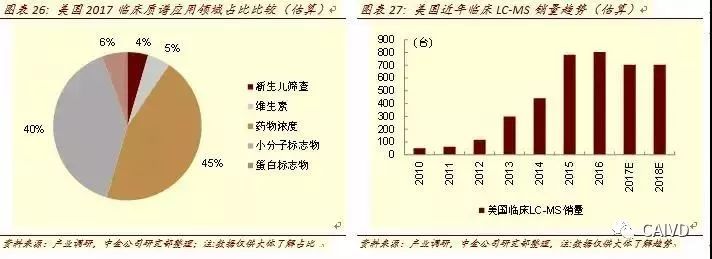

Under the LDT system, the rapid development of clinical mass spectrometry testing in the U.S. has occurred. By 2017, nearly 3,000 mass spectrometers were used for clinical testing in the U.S., with about 45% used for drug concentration testing and about 40% for small molecule biomarker detection. The LC-MS used for small molecule biomarker detection has shown a very strong growth trend in recent years, with around 50 units used for clinical testing in 2010, and by 2017, it is expected to exceed 700 units.

Domestic Independent Clinical Laboratories (ICL) Gradually Mature

Greater market for clinical mass spectrometry awaits the opening of LDT

Domestic independent clinical laboratories have gradually matured. Including Dean Diagnostics, KingMed Diagnostics, etc., domestic independent clinical laboratories have undergone rapid expansion. For example, Dean Diagnostics had only 8 laboratories in 2010, and is expected to increase to 33 by 2017; KingMed Diagnostics had only 14 in 2010, and is expected to increase to 35 by 2017. The gradual maturity of domestic independent clinical laboratories makes it possible to purchase high-end equipment and expand new projects within the coverage of hospitals.

Domestic ICLs have successively launched clinical mass spectrometry projects. Including KingMed Diagnostics, Dean Diagnostics, Da An Gene, Huayin Health, and Hehe Medicine, domestic third-party independent clinical laboratories have gradually launched clinical projects in mass spectrometry in recent years. For example, KingMed Diagnostics was one of the first to launch vitamin D testing products; Dean Diagnostics established a joint venture with AB Sciex and introduced talents from the U.S. to focus on clinical testing and metabolomics; Da An Gene’s invested Keli Meta focuses on the field of mass spectrometry testing.

Waiting for breakthroughs in the LDT system to open up greater clinical mass spectrometry space. Compared to the relatively mature market in the U.S., due to the lack of corresponding LDT mechanisms in China, clinical mass spectrometry is more focused on relatively mature markets. In 2017, we expect that the number of mass spectrometers used for clinical testing in China will not exceed 350, with about 70% used for newborn screening, 20% for vitamin testing, and vitamin D testing still in the early stages of promotion, requiring time for market cultivation. In 2017, it is estimated that there will be about 120 LC-MS used for clinical testing in China, although there is still a significant gap compared to the U.S. market, the market has already expanded significantly compared to fewer than 10 units used in 2010.

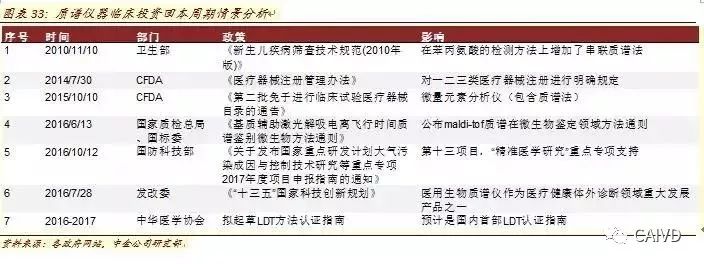

Policy is at a trial development stage, and the overall trend is positive. Currently, the policy level for the clinical application of mass spectrometry in China is still at a trial stage. Analogous to the application of traditional Car-T technology, gene sequencing, and other innovative technologies in the medical field, “one pipe dies and another goes wild” remains a dilemma faced by the government. We expect that clinical mass spectrometry testing will also undergo a gradual process of “management” and “release”.

In recent years, the CFDA has relaxed regulations on the clinical application of mass spectrometry; the Ministry of Health has promoted the application of MS-MS in newborn disease screening; and the National Quality Supervision Bureau and the National Standards Bureau have formulated general rules for MALDI-TOF MS, which has promoted its development in the field of microbial testing to a certain extent.

The further opening of the clinical application space for mass spectrometry still requires continuous attention to the opening of the LDT system and the attitude of the pricing department. For the future management of clinical applications of mass spectrometry, we expect that the CFDA will likely be responsible for the registration approval and management of equipment, with other ministries assisting in its development. The progress/breadth of the Chinese Medical Association’s LDT certification guidelines and the CFDA’s degree of openness will directly relate to the future imagination of the clinical application market for mass spectrometry; and the pricing bureau’s support for the promotion of new technologies based on medical insurance dilemmas will still be a factor that must be considered in its actual application fields. The overall trend is positive, but specific impacts need to be observed in the future.

New regulations: Starting from June 1, all Class III medical devices will begin to use unique identifiers.

Without using UDI, they will not be approved for market!

Recently, the National Medical Products Administration, the National Health Commission, and the National Medical Insurance Bureau jointly issued the “Notice on Doing a Good Job in the Second Batch of Implementation of Unique Device Identifier for Medical Devices” (hereinafter referred to as the “Notice”).

The notice clarifies that starting from June 1, on the basis of the first batch of 9 categories and 69 varieties of medical devices with unique identifiers, all remaining Class III medical devices(including in vitro diagnostic reagents)are included in the scope of the second batch of unique identifier implementation.

What is the unique device identifier for medical devices?

What is the unique device identifier for medical devices?

The Unique Device Identifier (UDI) for medical devices refers to a code composed of numbers, letters, or symbols that is attached to the product or packaging of medical devices using standards, used for the unique identification of medical devices, which can effectively improve the scientific management efficiency of medical devices.

The notice states that starting from June 1, 2022, medical devices produced must have a unique device identifier (UDI).Before going on the market, registrants must upload the product identifiers and related data to the unique device identifier database according to relevant standards or specifications, ensuring that the data is true, accurate, complete, and traceable.

For medical devices that have maintained information in the National Medical Insurance Bureau’s medical consumables classification and coding database, they must supplement the unique identifier information in the unique identifier database and ensure the consistency of data with the medical consumables classification and coding database.

In other words, starting today, all Class III medical devices will begin to implement “real-name registration”!

According to the requirements of the National Medical Products Administration, those who do not fill in the product identifiers (UDI) as required will have their registration application materials not accepted.

This means that Class III medical devices that do not use UDI will also be unable to register and go on the market.

Failure to comply will result in heavy penalties!

In addition, the newly implemented “Regulations on the Supervision and Administration of Medical Device Production” since May 1 of this year also clearly stipulates the work on unique identifiers for medical devices:

Medical device registrants, filers, and entrusted manufacturers should carry out coding, data uploading, and maintenance updates in accordance with the requirements of the state for implementing unique identifiers for medical devices.

Those who do not carry out coding, data uploading, and maintenance updates as required by the state for unique identifiers for medical devices will be ordered by the drug supervision and administration department to make corrections within a time limit;failure to correct will result in a fine of 10,000 to 50,000 RMB; serious cases will result in a fine of 50,000 to 100,000 RMB.

Medical device operating enterprises should implement the unique identifier system for medical devices in accordance with national regulations and establish and implement product traceability systems to ensure product traceability.

Previously, the phenomenon of no code or multiple codes for a single item in the circulation and use of medical devices was common, severely affecting the precise identification of medical devices in all links of production, circulation, and use, making effective supervision and management difficult.

However, after the full implementation of the medical device “real-name system”, it is expected to achieve “one device, one code, one identity”, connecting all links from production to circulation to clinical use with “one code”.

Once a product violation occurs, it can be automatically identified and accurately traced back to the responsible enterprise through UDI, forcing manufacturers to strictly control quality during production and sales.

After solving the traceability problem, manufacturers and distributors of medical devices will face stricter supervision! Ensuring quality control of products and being responsible for their products is particularly important.

Multiple provinces have issued documents

Clearly define the scope of unique identifier implementation

Currently, the progress of unique identifiers for medical devices has reached the final urgent implementation stage, and multiple provinces are actively issuing documents to accelerate the promotion of unique identifiers for medical devices.

In addition to Class III medical devices, provinces such as Hainan, Fujian, Sichuan, Beijing, and Tianjin have successively carried out unique identifier work for Class II medical devices;

Fujian and Gansu provinces have also launched the UDI coding maintenance function, requiring related enterprises to log in to the sunshine procurement platform to maintain medical consumables UDI coding;

Gansu has explicitly stipulated that Class III medical devices produced after June 1, 2022, must provide unique identifier information before they can be included in the provincial platform for bidding and procurement, and those without unique identifier information cannot be procured or used!

In addition to the provinces mentioned above, many provinces and cities have issued documents clearly defining the implementation time and scope of unique identifiers for medical devices. The working situation of various provinces and cities is summarized as follows:

Henan issued the “Implementation Plan for Promoting the Unique Identifier Work of Medical Devices” on April 28, requiring that all Class III medical devices produced in the province have a unique identifier starting from June 1, and encouraging and supporting registrants and filers of Class I and II medical devices in the jurisdiction to actively promote the implementation of unique identifiers.

In the medical insurance link, strengthen the connection between the coding of medical consumables and the unique identifiers of medical devices, and explore the application model of unique identifiers in the centralized procurement and medical insurance settlement of medical consumables.

Ningxia in the “Notice on the Implementation of Unique Identifier Work for Medical Devices” clearly requires that all Class III medical devices (including in vitro diagnostic reagents) must have unique identifiers before June 1, 2022. It encourages qualified manufacturers of Class I and II medical devices to apply unique identifiers and achieve coding.

Shandong in the “Implementation Plan for Promoting Unique Identifiers (UDI) for Medical Devices in Shandong Province” requires to ensure that all Class III medical devices produced from June 1 this year have UDI; encourages and supports registrants of Class II medical devices to actively implement UDI, striving for all Class II medical devices produced from January 1, 2024, to have UDI; encourages and supports registrants of Class I medical devices to promote the implementation of UDI according to their actual situation.

Chongqing in the “Notice on Matters Related to the Implementation of the Second Batch of Unique Identifiers for Medical Devices” requires that starting from June 1, 2022, all Class III medical devices must have unique identifiers. It encourages and supports other varieties of medical devices in the city to implement unique identifiers, and the bureau will gradually promote the pilot implementation of unique identifiers for Class II medical devices (including in vitro diagnostic reagents).

Gansu in the “Notice on the Centralized Maintenance of Unique Identifier Data for Medical Consumables” requires enterprises to complete the maintenance of UDI coding on the sunshine platform by May 20. Class III medical devices produced after June 1, 2022, must provide unique identifier information before they can be included in the provincial medical procurement platform for bidding. Those without unique identifier information cannot be procured or used.

Hainan in the “Notice on Joint Promotion of Unique Identifier Implementation for Medical Devices” clearly requires that all Class III and Class II medical devices (including in vitro diagnostic reagents) in Hainan Province be included in the implementation scope of unique identifiers. It supports and encourages Class I medical devices that meet the conditions to implement unique identifiers. The unique identifiers for Class III products began to be implemented on December 1, 2021, while Class II products began to be implemented on June 1, 2022.

Jilin in the “Notice on the Comprehensive Launch of Unique Identifier Pilot Work for Medical Devices” clearly requires that all Class III medical devices (including in vitro diagnostic reagents) in the province be included in the implementation scope and strengthen the connection between the classification and coding of medical consumables and unique identifiers for medical devices.

Jiangxi in the “Notice on Joint Promotion of Unique Identifier Implementation for Medical Devices” requires that starting from June 1, all Class III medical devices (including in vitro diagnostic reagents) in the province use UDI, and encourages and supports the use of UDI for Class II products.

Shanxi in the “Notice on the Comprehensive Promotion of Unique Identifier Implementation for Medical Devices in Production and Operation Links” requires that all Class III medical devices start using UDI from June 1.

Hunan in the “Implementation Plan for Promoting the Unique Identifier System for Medical Devices in Hunan Province” encourages the promotion of UDI for all Class III medical devices in the province, exploring the connection between unique identifiers and the coding of medical consumables in the medical insurance system.

Hebei in the “Notice on Matters Related to the Implementation of Unique Identifiers for Medical Devices” requires that starting from November 1, 2021, the first batch of Class III medical devices (including in vitro diagnostic reagents) produced in the province begin implementing UDI, and encourages other medical device products to begin implementing UDI.

Sichuan in the “Notice on Joint Promotion of Unique Identifier Implementation for Medical Devices” states that all Class III medical devices must use UDI by November 2021.

Jiangsu in the “Implementation Plan for Promoting Unique Identifier Work” states that starting from January 1, 2021, in addition to the first batch of medical device varieties required by the state to use UDI, it also encourages other varieties to begin implementing UDI.

In applying for the registration and production license of Class II medical devices and the production license of Class III medical devices, the Provincial Drug Supervision Administration will conduct separate sorting and prioritize processing; relevant varieties will be given priority review and processing when applying for provincial medical consumables sunshine listing.

Yunnan has currently completed the use of UDI for all Class III medical devices and some Class II medical devices.

Guangdong has completed the use of UDI for the first batch of medical device varieties required by the state by the end of December 2021 and encourages other medical device varieties to use UDI.Shenzhen completed the use of UDI for the first batch of medical device varieties required by the state before October last year.

Anhui in the “Implementation Plan for Promoting the Unique Identifier (UDI) Work” states that starting from June 1, 2022, all Class III medical devices (including in vitro diagnostic reagents) must use UDI and supports and encourages other products to use UDI.

Fujian has completed the UDI coding work for the first batch of varieties required by the state and Class III products in the province, and encourages other listed Class II products to complete coding.

Beijing and Xinjiang have completed the coding of the first batch of varieties required by the state and encourage other varieties to use UDI coding. The Xinjiang Autonomous Region’s medical insurance system will carry out research on the connection between the unique identifier code for medical devices and the “medical insurance code”, promoting the “three medical linkages”.

Shanghai has required that starting from January 1, 2021, the first batch of varieties required by the state and other varieties in the “first batch focus governance list” use UDI coding.

Shanxi requires that starting from June 1, 2022, the UDI coding work for the first batch of products required by the state be continued, and all other Class III medical devices must promote the implementation of UDI.

Tianjin has completed the use of UDI for all Class III and Class II medical devices produced in the city, as well as for first-level imported and domestically produced products not produced in the city.

Zhejiang in the “Implementation Plan for Promoting Unique Identifiers (UDI) for Medical Devices” requires that starting from June 1, all Class III medical devices (including in vitro diagnostic reagents) must use UDI coding and encourages and supports other medical device products to use UDI coding.

Information source: Qinghua Cambridge Business School Data collection: Weijian Jun Statement: The copyright of this article belongs to the original author and does not represent the position of this WeChat public account. If there are copyright issues, please contact for deletion.