It is internationally recognized that 2025 will be the year when AI agents will generate revenue rather than just tell stories. Many companies in the United States have already created revenue using AI agents, creating a vibrant and competitive atmosphere across the Pacific. So, which listed company here primarily generates revenue from AI software? Previously, I wrote about Tonghuashun, and today a company has come into my view — Huasheng Tiancheng.

As usual, let’s start with the company’s evolution.

I. Founding and Technological Foundation Period (1998–2003 years)

1. 1998 year: Company Established

• Founded by technical backbones from the Sixth Research Institute of the Ministry of Electronics Industry in Beijing, initially focused on system integration and hardware agency business (such as IBM, Sun Microsystems, and other international brands), laying the foundation for subsequent technical service capabilities.

2. 2001 year: Strategic Transformation

• Reorganized into a joint-stock company, positioning professional services as a new growth point, transitioning from hardware agency to IT solution provision, serving finance, telecommunications, and other fields.

II. Listing and Business Expansion Period (2004–2011 years)

1. 2004 year: Entering the Capital Market

• Listed on the Shanghai Stock Exchange (stock code: 600410), financing accelerated technology research and market expansion.

2. 2009 year: A Key Step Towards Internationalization

• Acquired the Hong Kong-listed company ASL (stock code: 00771) for HKD 262 million, integrating its Southeast Asian customer resources and technical capabilities, becoming one of the first IT service providers covering the Asia-Pacific region, with technical service revenue accounting for 40%.

3. 2011 year: Cloud Computing Layout

• Approved by the CSRC to become one of the first domestic cloud computing financing enterprises, launched the “Tiancheng Cloud” brand in 2012, establishing a cloud computing industry alliance and providing hybrid cloud solutions.

III. Strategic Transformation and Ecological Layout Period (2017–2023 years)

1. 2017 year: “Connection + Platform + Intelligence” Strategy

• Invested in IoT chip manufacturer Tailin Microelectronics (listed on the Sci-Tech Innovation Board in 2023, 688591), entering the core segment of smart hardware.

2. 2018 year: Deepening Cloud Ecology

• Launched the “One Core and Four Clouds” strategy, focusing on cloud solutions for industries such as manufacturing and logistics, promoting the implementation of domestic cloud architecture.

3. 2020 year: Diversification and Capital Breakthrough

• Proposed the “Cloud Achieves Cloud Victory” architecture, with cloud business fully maturing;

• Invested in Grid Dynamics, which went public on NASDAQ (GDYN), expanding global layout.

IV. New Positioning in the AI Era (2024 to Present)

1. Strategic Focus on AI Applications • Positioned as an “Enterprise-level AI Service Provider”, reshaping enterprise scenarios with generative AI, launching products such as intelligent customer service and Bid King (AI bid document generation), and intelligent contact centers.

2. Intelligent Computing Center Construction

• The Tianjin Intelligent Computing Center (300P computing power) and the Suzhou Guochuang Intelligent Computing Center (500P phase one) have been established, serving government and new energy vehicle sectors.

3. Deepening Ecological Cooperation

• Collaborated with Huawei (smart parks, customer service systems), Baidu (large model applications), Intel, etc., to launch the “Intelligent Machine Integration” solution, aiming for AI computing business revenue to account for 28% by 2025.

Current Status and Global Layout

• Business Scale: Covers 15 countries and 40 cities, with over 7000 employees, holding stakes in 4 listed companies (ASL, Grid Dynamics, and Tailin Microelectronics, etc.).

• Technical Accumulation: Holds 22 core patents, serving over 16,000 enterprise clients (such as the National Development Bank and China Mobile).

• Financial Performance: Turned profitable in 2024 (net profit of 24.12 million), with a forecasted increase of 148%–173% in the 2025 mid-year report (driven by AI business).

Summary: Huasheng Tiancheng’s journey has undergone a four-stage transformation from hardware agency → system integration → cloud services → AI ecology, with core driving forces being technological foresight (such as cloud computing, AI) and capital mergers (ASL, Tailin Micro). The current strategic focus is on the commercialization of AI applications and intelligent computing infrastructure, with challenges in sustainable profitability under high R&D investment and competition from international giants.

What is the relationship between the company and Huawei in the intelligent computing infrastructure business? As we all know, Huawei’s Ascend series is China’s sharpest weapon against Nvidia.

The Internet Weekly of the Chinese Academy of Sciences rated Huasheng Tiancheng as the “2024 Leading Enterprise in the Field of Artificial Intelligence” due to its National Innovation Center’s intelligent computing project being selected as an “Excellent Case for National Digital China Construction.” Additionally, Huasheng Tiancheng clearly disclosed in its 2024 semi-annual report that the company is the core integrator for Huawei’s Ascend Intelligent Computing Centers, undertaking planning and construction tasks for multiple intelligent computing centers nationwide. It specifically mentioned that among the 21 intelligent computing centers planned by Huawei, Huasheng Tiancheng has won bids for 15 projects. For example, the Tianjin Hebei District project has a total computing power of phase one reaching 300P with a total investment of 2.4 billion yuan. The company’s announcement shows that in the first quarter of 2025, the newly added intelligent computing business contract amount was 1.87 billion yuan (a year-on-year increase of 320%), with the intelligent computing business accounting for 32% of revenue, directly validating its core integrator business scale.

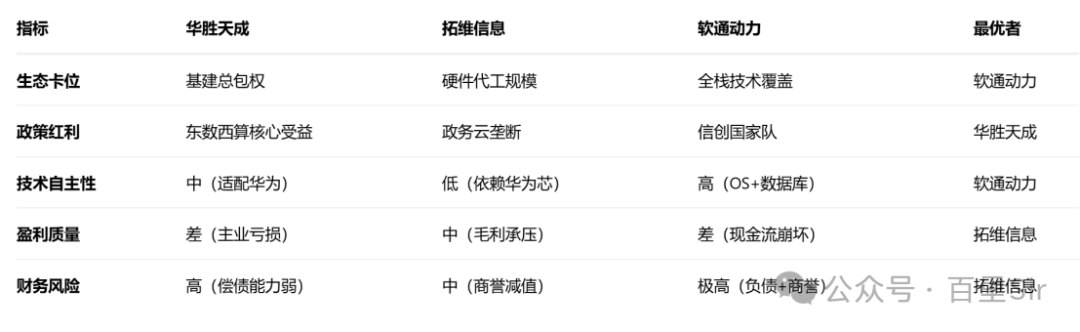

Since the company is tied to Huawei, how does it compare to other star companies in the Huawei ecosystem? Tuwei Information and Softcom Power are also well-known companies within the Huawei ecosystem.

I have listed the comparison of the three companies in the table below.

From several dimensions such as ecological positioning, I have also scored them accordingly.

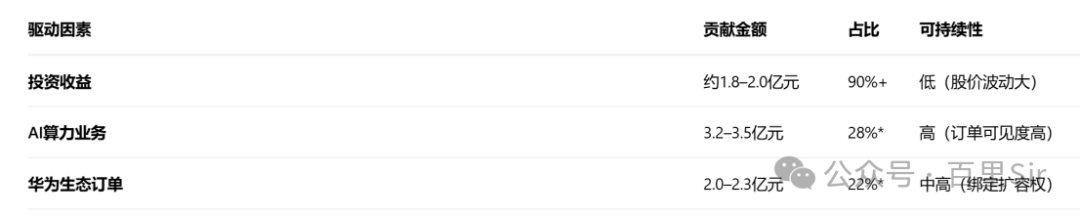

2025 Company Mid-Year Performance Forecast (Net Profit 180 million–200 million yuan, a year-on-year surge of 148.59%–172.88%) I have analyzed that the core reasons for the explosive growth in performance can be summarized in three points.

Investment income refers to the stake in the company Tailin Microelectronics (688591.SH) which is expected to see its stock price rise over 120% in 2025, with Huasheng Tiancheng confirming fair value change income of approximately 180 million yuan, accounting for 90% of the mid-year net profit.

Having discussed the present, let’s talk about the future. Where will the company’s growth points be? I believe there are three areas.

The first area is Data Annotation and AI Quality Inspection:

Data annotation bases are being established in Shenyang, Guiyang, and Hefei, with 3000 annotators, and in 2024, AI data business revenue is expected to reach 420 million yuan (year-on-year growth of +112%), with a gross margin of 45%, making it the highest profit margin segment.

Providing annotation platforms for medical and financial sectors (for example, the model training cycle for a certain top-tier hospital has been reduced from 18 months to 6 months), with costs reduced by 30%.

Smart Emergency Policy Dividend:

The national “14th Five-Year Plan” emergency planning requires a digital coverage rate of 80% by 2025, corresponding to a market of 200 billion yuan. The company’s “Holographic Emergency” system has been implemented in Zhejiang and Jiangsu, with revenue growth of 112% in 2024, achieving disaster reduction benefits of direct losses reaching 37 times.

By 2025, the revenue share of this business is expected to increase to 25%, becoming a core growth driver for the government sector.

The second area is AI Agent Business

The company’s Bid King 2.0: Achieves full-process automation of bidding, reducing bid document writing time from 1 week to 1 day, already applied in government and financial procurement scenarios, with efficiency improved by more than 10 times.

Intelligent Customer Service System: After being implemented in a certain policy bank, service costs decreased by 12%, training costs decreased by 15%, and expanded to the tobacco and automotive sectors, with model accuracy improved by 3–5 times.

Mocha Intelligent Operation and Maintenance Platform: Covers government, finance, and other industries, with fault prediction accuracy improved by 40%, and operation and maintenance manpower reduced by 50% (saving a certain bank 8 million yuan annually).

Additionally, as one of the first industry partners of Baidu Smart Cloud, the company has launched AI application products based on the Qianfan platform, becoming a supplier in Baidu’s ACG delivery framework. Collaborating with Volcano Engine and Intel, it released the “Intelligent Machine Integration”, integrating computing power engines (Intel GPU) + large model platform (HiAgent) + delivery services, lowering the threshold for enterprises to deploy AI.

Revenue Contribution Expectations: The equity incentive requires that in 2025, ICT business revenue reaches 1.5 billion yuan (year-on-year growth of +67%), with the proportion of AI applications increasing, and the target for 2027 is 3.85 billion yuan, accounting for over 70% of total ICT revenue.

The third area is the rapid development of deep binding with Huawei’s Ascend ecosystem.

Undertaking 71% of Huawei’s Ascend Intelligent Computing Centers nationwide (a total of 15 centers), including the Tianjin Hebei District project (long-term 1500P), Jinan Artificial Intelligence Computing Center, etc., with contracts clearly stating “priority renewal rights for expansion.”

In Q1 2025, won the bid for China Mobile’s AI server procurement worth 210 million yuan (Ascend 910B model), marking the first order after the transformation, validating delivery capabilities.

Jointly released the “Smart Park AI Integration Machine” with Huawei, integrating Ascend chips and DeepSeek large models, implemented in safety production, security, and other scenarios, with orders exceeding 500 million yuan.

Equity incentives bind the original core team of Huakun Zhenyu (the largest server partner of Huawei Ascend), bringing in talents like Guo Yuanxing, and accessing government/operator order resources.

Although relying on the Huawei ecosystem poses risks of chip sanctions (manufacturing limitations for Ascend 910B), the company has developed the HyperX architecture compatible with domestic chips (such as Haiguang), and is laying out edge-end Tailin Microelectronics chips (holding 7.44% stake), achieving a 30% reduction in costs through end-cloud collaboration.

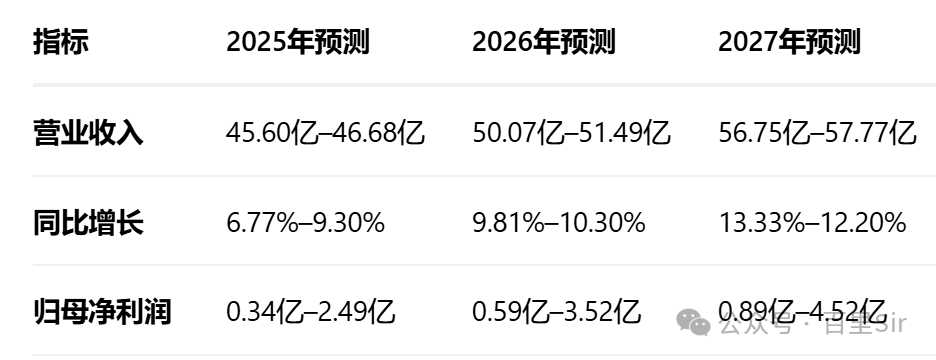

Finally, let’s look at the company’s financial forecast for the next three years.

The current market value of the company is 20.6 billion yuan, even if calculated based on a profit of 450 million yuan in 2027, it is a 45 times PE. It can be said that the recent excessive market hype has already overdrawn its growth for the next three years. (END)