This weekend has brought a flurry of positive news, and I believe everyone is looking forward to next week, not just for next week, but indeed for September as well. The positives come from several aspects: on one hand, there are favorable policies, such as the statement from the China Securities Regulatory Commission (CSRC) to continue maintaining a stable and positive development momentum, guiding long-term and patient capital into the market; secondly, there is positive economic data. Both the manufacturing and non-manufacturing PMIs have shown a month-on-month rebound, indicating signs of economic recovery, and the market is supported by fundamental factors; thirdly, and most importantly, there has been a cluster of favorable news related to chips and semiconductors, with SMIC suspending the acquisition of assets, and Alibaba’s chip breakthroughs, which clearly adds fuel to the recently cooling semiconductor sector. The market is anxious: will the semiconductor chip market see a second wave? Can the high-low switch be realized? How should we allocate in September? These are not easy questions to resolve, so we have done a lot of work this weekend. We have studied the rotation patterns since April, hoping to find guidance for September’s allocation. This is the main content of our work today. Before doing this work, we need to interpret some major driving events over the weekend, as these events are related to the direction of the market and the selection of main lines and hotspots.

1) Interpretation of Major Driving Events and Market Impact Analysis

1) Li Chenggang, the international trade representative and vice minister of the Ministry of Commerce, held talks with relevant officials from the US government and business representatives

The Chinese trade delegation held talks with US government officials, and clearly no positive results were achieved. China expressed its position, hoping that both sides adhere to the principles of mutual respect, peaceful coexistence, and win-win cooperation, and continue to make good use of the China-US economic and trade consultation mechanism to manage differences and expand cooperation, jointly promoting the healthy, stable, and sustainable development of China-US economic and trade relations.

This expression of hope is also a criticism of the US, and will not have any impact on the market.

1) CSRC Wu Qing: Continue to consolidate the positive momentum of the capital market

The CSRC held a symposium, stating that it will continue to consolidate the positive momentum of the capital market, emphasizing the need to enhance the market’s attractiveness and inclusiveness, and actively advocate for long-term investment, value investment, and rational investment.

It is particularly emphasized that, the continuous consolidation of the positive momentum of the capital market is crucial. Everyone must pay attention: the most important words here are “continuous consolidation,” which means that the support for capital and the market is ongoing. Secondly, the current nature of the market is only stabilizing and improving. Any major peaks in the Chinese securities market are related to policies, mostly aimed at curbing overheating, and the current statement indicates that the bull market will continue, and this is just the beginning. It also mentions inclusiveness, which is beneficial for activating the market. Finally, in terms of investment philosophy, it advocates for long-term investment, value investment, and rational investment. Implicitly, it supports a slow bull market.

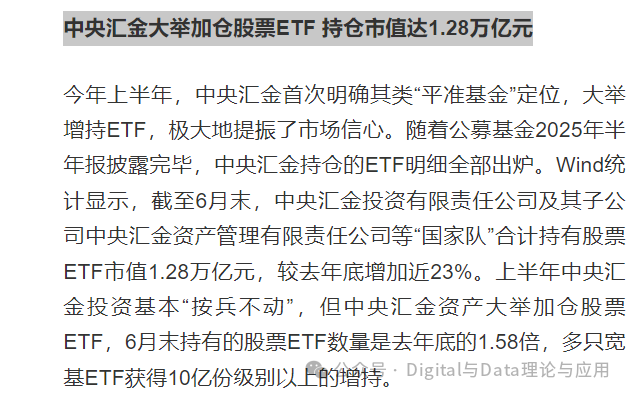

2) 3) Central Huijin significantly increased its holdings in stock ETFs, with a market value of 1.28 trillion yuan

Central Huijin has significantly increased its holdings in stock ETFs in the first half of the year.

This tells us two points: first, stock ETFs are a good investment method, which we need to strengthen our research on, therefore, in September’s allocation, we will select several important ETFs, or construct a dedicated ETF pool for everyone to choose from. Secondly, Central Huijin’s significant increase in holdings indicates an optimistic attitude towards the market.

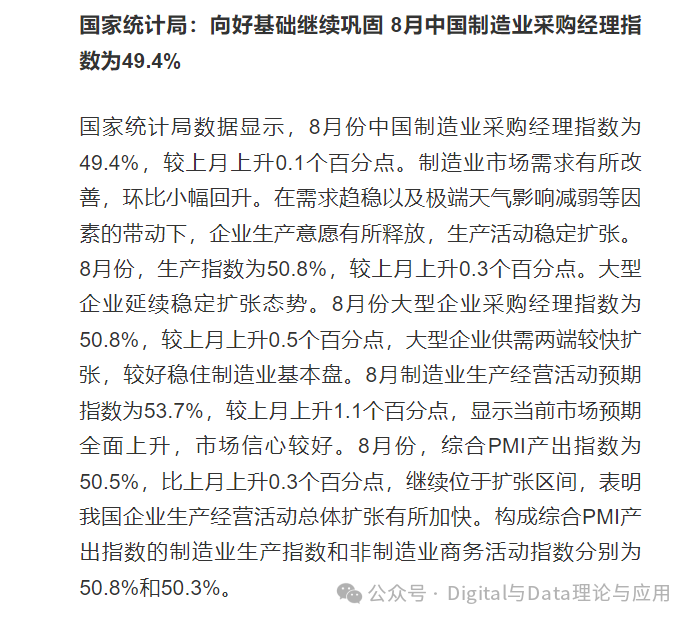

3) National Bureau of Statistics: The positive foundation continues to consolidate, with China’s manufacturing PMI at 49.4% in August

Regarding the PMI data, we have already provided an interpretation in the community, here we only provide the conclusion: the PMI data shows that the Chinese economy is showing signs of recovery. The fundamentals are beginning to support the market.

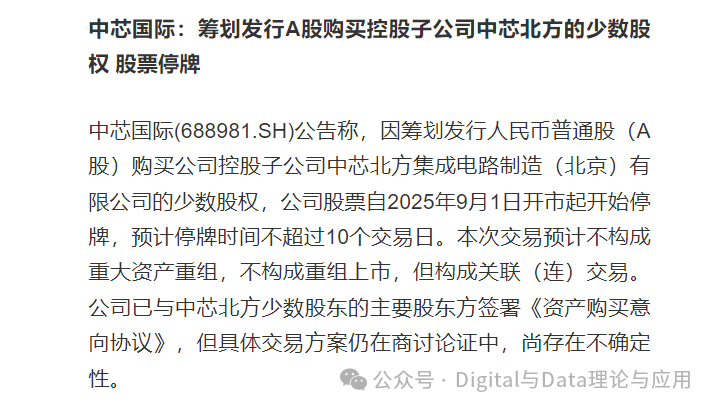

4) SMIC: Planning to issue A-shares to purchase minority stakes in its controlling subsidiary, SMIC North, stock suspended

This move constitutes a significant positive for the semiconductor industry.

There are two ways to issue shares to purchase shares: one is to pay cash consideration, and the other is a share swap operation.

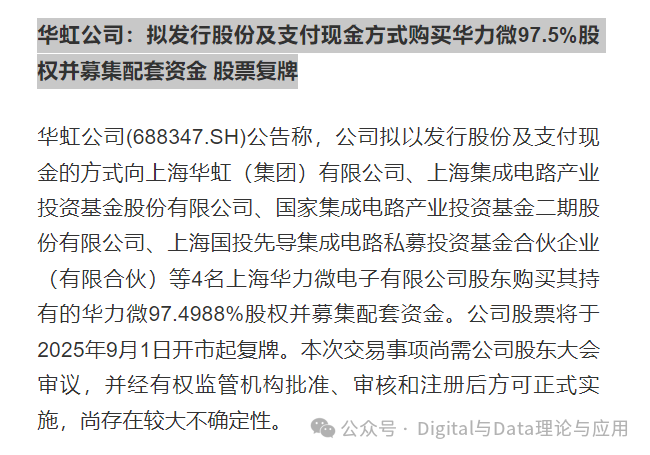

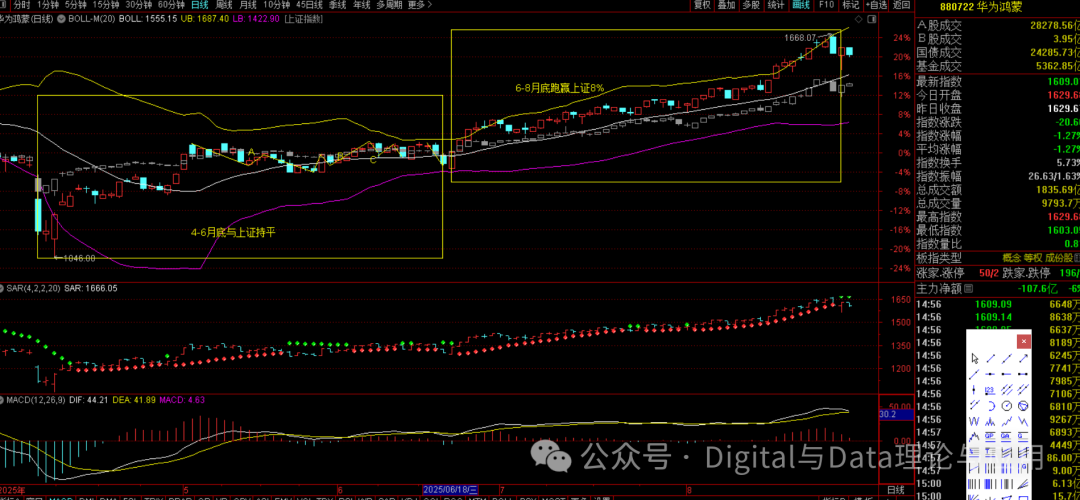

5) Huahong Semiconductor: Plans to issue shares and pay cash to acquire 97.5% of Huawave’s equity and raise matching funds, stock resumes trading

Huahong Semiconductor has confirmed the issuance of shares to pay cash for 97.5% of Huawave’s equity.

Its performance after resuming trading may have a significant impact on the market, such as determining the performance of SMIC after resuming trading, and we suggest that everyone pay attention to this. The attention here is not to chase the rise and buy in, but to observe its performance.

6) Huawei’s latest performance report: Revenue increased by 3.95% year-on-year, net profit decreased by 32% year-on-year

We do not see the detailed report of Huawei’s performance, with revenue only increasing by 3.95% year-on-year and net profit decreasing by 32% year-on-year, which should be said to far exceed expectations, and may negatively affect the performance of related stocks in the Huawei system.

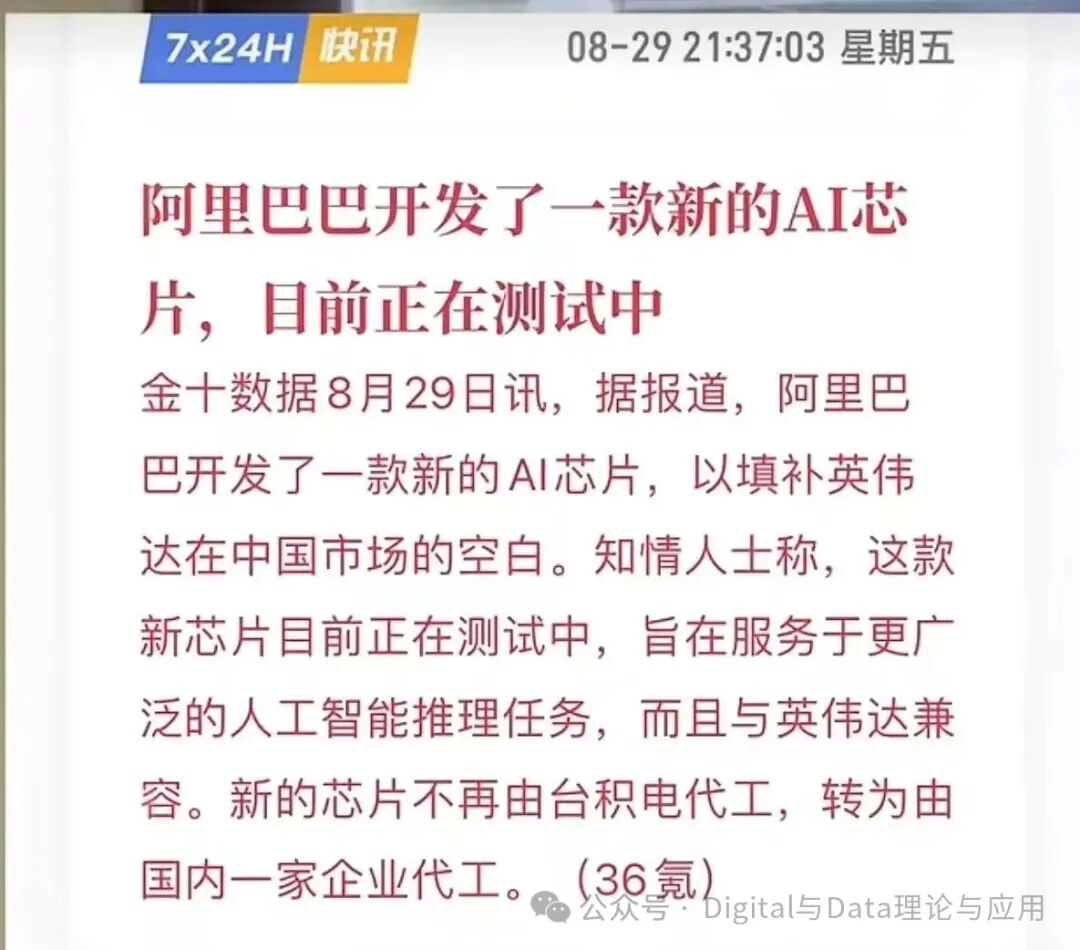

7) 8) Alibaba’s chip breakthrough

Alibaba announced the launch of its chip B plan, with reports indicating that Alibaba has developed a new AI chip that can replace Nvidia, and has chosen domestic companies for foundry, no longer relying on TSMC.

This move has sparked market speculation about whether there will be another round of semiconductor market similar to the one triggered by DS’s announcement of choosing domestic advanced chips.

We believe that related stocks in the Alibaba system have already performed excellently in August, and the likelihood of a new round may not be large; how they perform after a high opening tomorrow is difficult to judge.

Nevertheless, to meet everyone’s needs, we have also constructed a stock pool related to Alibaba, but I do not recommend chasing high prices.

In fact, it is hard to judge because the market is currently in an emotional phase.

How exactly, the rotation patterns we study below may provide answers.

The solution to the problem is actually quite simple; as the strongest main line cannot peak, if you hold related stocks, just hold them steadily.

2) Foreign Exchange and External Markets

The US stock market has recently been in a narrow range of fluctuations, essentially undergoing a phased three-stage adjustment, due to the unclear prospects for interest rate cuts in September, and the ongoing confrontation between Trump and the Federal Reserve.

Overall, the possibility of an interest rate cut in September seems certain, but the uncertainty lies in how much: is it 25 basis points or 50 basis points?

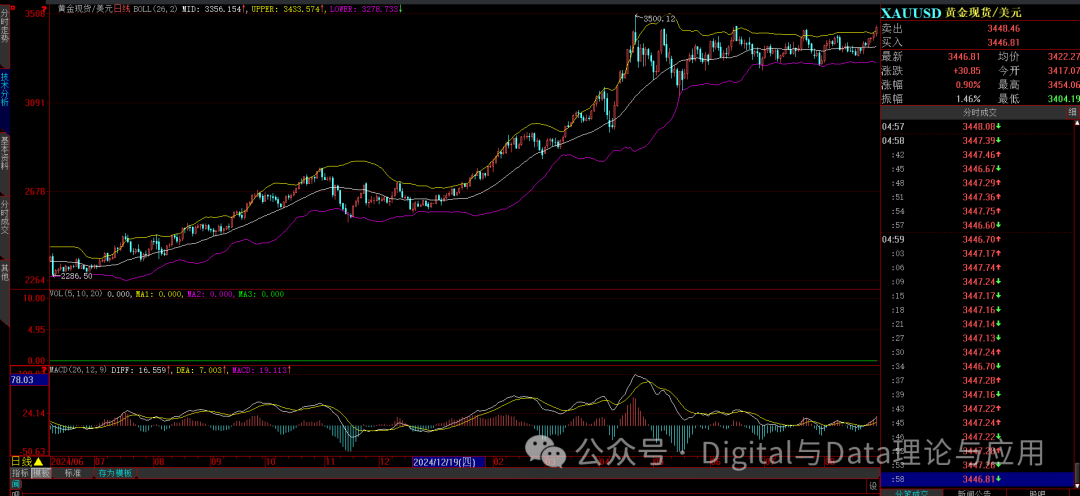

The expectation of an interest rate cut supports the continued depreciation of the US dollar, technically, the US dollar has a requirement for further depreciation.

The expansion of the US dollar’s depreciation is beneficial for US stocks, as well as for gold, non-ferrous metals, and bulk commodities. Therefore, in our September stock allocation, we have increased our allocation to non-ferrous metals, including strategic minerals and energy metals.

At the same time, the signs of recovery indicated by the PMI data also support our increased allocation to strategic minerals and energy metals.

The depreciation of the renminbi indicates a flow of funds towards Chinese assets, which is beneficial for Hong Kong and A-shares.

The depreciation of the US dollar supports gold to break upwards, so September’s allocation may consider gold.

The US stock market may be in the C phase of a phased adjustment, meaning there is a possibility of short-term decline, which is expected not to have a significant impact on A-shares and Hong Kong stocks.

3) Study of Main Line Rotation Patterns Since April

To study the rotation patterns of the main lines since April, we need to push the time back to the early 2025 slow bull market.

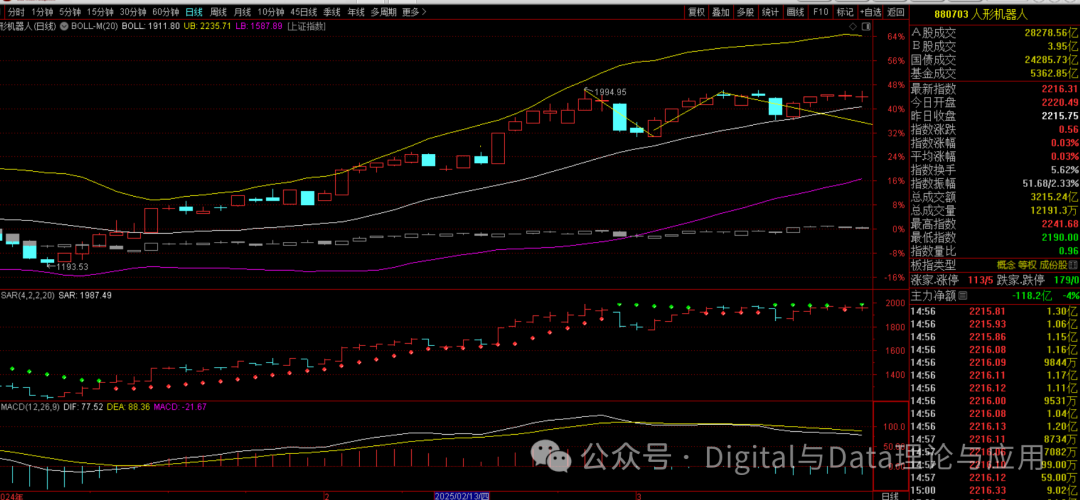

1) The strongest main line in the first quarter: the performance of humanoid robots and Huawei’s HarmonyOS after the hype

In the slow bull market from January to March, humanoid robots outperformed the Shanghai Composite Index by 45%.

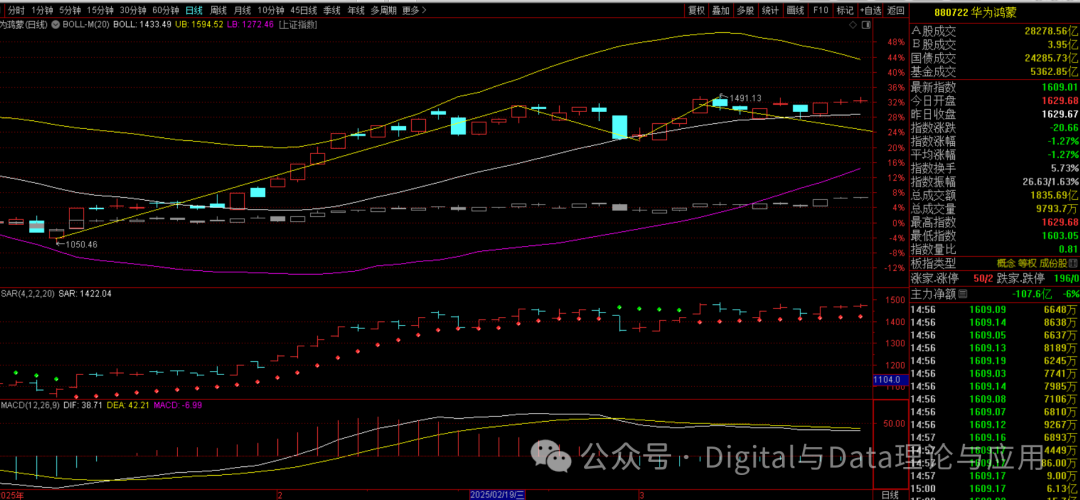

In the slow bull market from January to March, Huawei’s HarmonyOS outperformed the Shanghai Composite Index by 28%, close to 30%.

Humanoid robots and Huawei’s HarmonyOS were the strongest main lines in the market from January to March.

At that time, various grand narratives were supporting these two directions, one was DS’s disruption of US AI, and the other was the first year of commercialization for humanoid robots.

The situation at that time is similar to the current semiconductor sector. If someone had reminded you to sell Huawei, HarmonyOS, or humanoid robots, you probably would not have accepted it.

We had previously reminded to realize profits on humanoid robots and Huawei’s HarmonyOS stocks, specifically, it should have been on March 20, when humanoid robots and Huawei’s HarmonyOS broke below the middle track of the Bollinger Bands.

Looking at what happened afterward, the humanoid robots underwent a round of adjustment that lasted until the end of July.

The same situation also occurred with Huawei’s HarmonyOS, with a round of adjustment lasting until the end of July.

What does this indicate? First, any round of the strongest main line’s hype is related to grand narratives; the hype of humanoid robots and Huawei’s HarmonyOS from January to March was related to DS and the commercialization year of humanoid robots.

In comparison to the current chips, semiconductors represent the strongest logic to replace Nvidia, opening up your infinite imagination.

In March, the market was not worried about the trade war, so the trade war was not the reason for the adjustment; it was the adjustment requirement brought about by the excessive short-term rise.

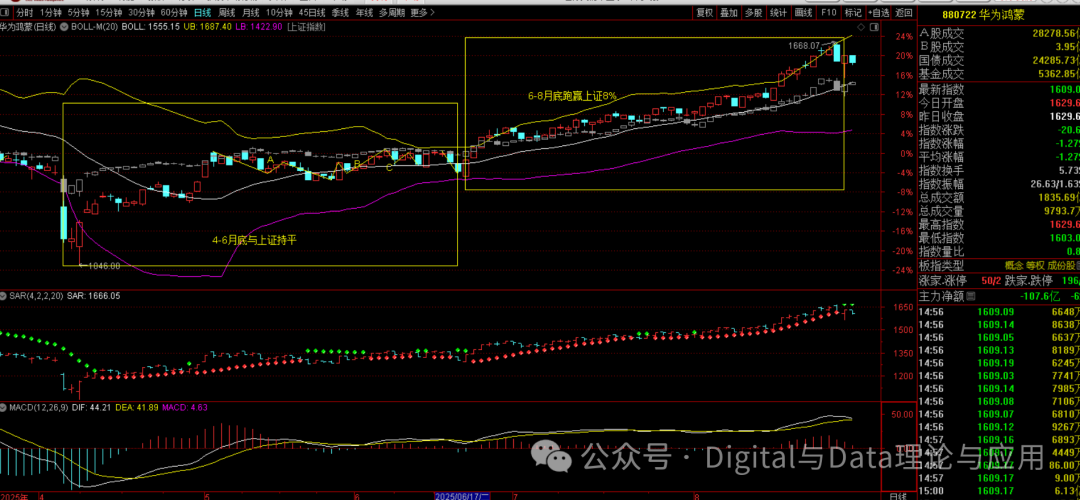

Looking at their performance after April.

Huawei’s HarmonyOS from April to the end of June was basically on par with the Shanghai Composite Index, and from July to August, it began to rise, only outperforming the Shanghai Composite Index by less than 10 percentage points.

Similarly, humanoid robots from April to mid-July were basically on par with the Shanghai Composite Index, and after mid-July, they outperformed the Shanghai Composite Index by less than 10 percentage points.

This indicates one issue: after the hype of the strongest main line, its adjustment may not be large. However, the duration of the adjustment is quite long.

Similarly, under the background of a bull market, will the semiconductor chips enter a relatively long adjustment or sideways movement after the hype? It is worth noting that, although we are still confident in their performance in this round of super bull market.

2) The strongest main line from April to July: banks and high-dividend stocks: the bear market change in mid-July

The strongest main line from April to July was undoubtedly high-dividend and dividend assets, but after mid-July, they have become bear stocks in the bull market.

This also indicates that even after a bull market hype, there will be adjustments, even adjustments that change the nature of the market.

We see that small and medium-sized banks underperformed the Shanghai Composite Index from January to March, with the underperformance reaching nearly 10 percentage points.

From April to mid-July, they outperformed the Shanghai Composite Index, reaching nearly 15 percentage points, becoming the strongest main line in the market from April to mid-July.

What happened next? We made accurate predictions at that time, constantly reminding everyone not to join in when the market was down; everyone saw the market sentiment, and no one would believe that bank stocks would adjust.

The situation at that time was completely consistent with the market sentiment of Huawei’s HarmonyOS, humanoid robots, and the current semiconductor sector, CPO, and PCB.

At that time, we also saw voices in the group inducing me to make the decision to join in when the market was down, but I did not do so, because in my view, bank stocks were severely overvalued, and after the hype, there would definitely be adjustments.

From mid-July to the end of August, bank stocks had underperformed the Shanghai Composite Index by nearly 10 percentage points, forming a rare bear stock in a bull market.

The above analysis and comparison indicate two issues: first, the strongest main line in a phase often starts from underperforming the market, that is, starting from poor performance; second, like humanoid robots and Huawei’s HarmonyOS from January to March, after the hype, there will be significant long-term adjustments. The adjustment of small and medium-sized banks or bank stocks has exceeded 50 days, and it is no longer of a mid-term nature.

Thus, everyone should consider whether chips, semiconductors, PCBs, and CPOs can soar? Especially against the backdrop of a flurry of positive news this weekend, how will they perform tomorrow, next week, and in September?

If in July, at the peak of banks and dividend stocks, one chose to join in when the market was down, what kind of mentality would that be now? At that time, their mentality was disbelief that banks would adjust, disbelief that dividend stocks would adjust; joining in a day late was more painful than death.

Isn’t this similar to the current market perception of chips, semiconductors, CPOs, and PCBs?

3) Chips, CPOs, and semiconductors: will they continue to soar?

The comparison shows that the patterns of Huawei’s HarmonyOS, humanoid robots, and bank stocks are consistent; at their peak, no one believed they would soar, and no one believed they would adjust, or undergo mid-term adjustments or even turn bearish.

In comparison to the current cluster of positive news in the semiconductor sector, the market faces the judgment: will it continue to soar? Or will it peak and decline, falling into adjustment?

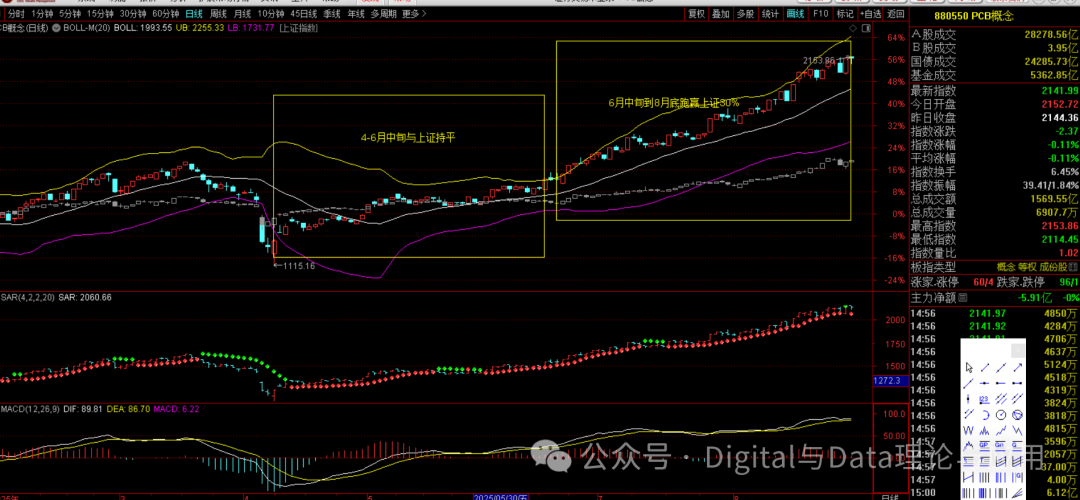

Chips outperformed the market slightly from January to March, were on par with the Shanghai Composite Index from April to June, and after the end of June, they began a magnificent upward movement, becoming the strongest main line in the market, outperforming the Shanghai Composite Index by over 20%.

CPO was on par with the Shanghai Composite Index from January to March, underperformed the Shanghai Composite Index from April to June, and after June, it began a magnificent upward movement, outperforming the Shanghai Composite Index by over 50 percentage points.

PCB slightly outperformed the Shanghai Composite Index from January to March, was basically on par with the Shanghai Composite Index from April to June, and after late June, it began a magnificent upward movement, outperforming the Shanghai Composite Index by nearly 40 percentage points.

The comparison shows that their performance before becoming the market’s main line was not outstanding, either underperforming or on par with the Shanghai Composite Index, which is consistent with the performance of bank stocks before their launch.

Currently, they have all significantly outperformed the Shanghai Composite Index, at least by over 20 percentage points, and at most nearly 50 percentage points.

So the question arises: have we reached the peak? How much upward space is left in the wave?

Technically, no peak signal has been issued, so we believe there is still upward space; however, due to the significant outperformance, the upward space may be limited.

If you hold related stocks, you can continue to hold; if not, chasing high prices may not be a wise choice.

5) Innovative drugs: after the hype, the adjustment trend is very obvious

From the above chart, it can be seen that before the launch of innovative drugs, from January to mid-May, their performance was basically on par with the Shanghai Composite Index, and after mid-May until the end of July, they began a magnificent upward trend, with maximum gains exceeding 30% and approaching 40%.

What happened afterward? Since August, the adjustment trend has become very obvious, breaking below the middle track of the Bollinger Bands, with SAR issuing sell signals, and MACD continuing to decline; the adjustment is still not over.

The trend of innovative drugs may serve as a very good hint for chips, semiconductors, CPOs, and PCBs: any thematic speculation and the strongest main line will ultimately face the requirement and fate of mid-term adjustments.

The trend of innovative drugs is consistent with that of humanoid robots and Huawei’s HarmonyOS after March, as well as with banks after mid-July: after reaching a peak, they will face mid-term or longer adjustments.

4) September Main Line Selection: Low Position, Undervalued, Cycle Reversal

According to the rotation patterns, the market faces a high degree of switching, but it should not be random switching; it must comply with: 1) support from industrial policies, upward industry cycles, and low technical and valuation levels.

1) Main Line Rotation Logic: Supplementary Rise and New Cycle

A bull market is a cycle, and the rotation of the main line is also a cycle.

The strongest main line in this bull market started with humanoid robots and Huawei’s HarmonyOS; once they have adjusted sufficiently and begun an upward trend, they may attract funds to sell high and buy low, or attract outside funds to buy in.

We may not choose Huawei’s HarmonyOS, as its revenue and profit have decreased by 32% year-on-year, which may negatively affect the performance of the industry chain.

The adjustment is sufficient, and humanoid robots have the potential for an outbreak.

Similar includes low-altitude economy, AI glasses, etc.

The above aligns with the AI+ action plan supported by the Central Committee and the State Council, which conforms to industrial policies and national strategies.

2) Strategic Minerals: Scarce Resources

The trend of scarce resources has just shown an accelerating trend, with important main line signals including tungsten, antimony, germanium, zirconium, as well as low-position varieties of rare earth permanent magnets.

3) Anti-involution, US dollar depreciation, and cycle reversal

Anti-involution may lead to a cycle reversal, and the depreciation of the US dollar supports non-ferrous and scarce resources, mainly lithium battery materials, including lithium ore, lithium batteries, and anode materials.

4) Computing power infrastructure and energy storage

Support for lithium ore, lithium batteries, etc.

5) Solid-state batteries

Demand for humanoid robots, drones, and new energy vehicles is expanding.

6) Controlled nuclear fusion

Is the focus of competition between China and the US

7) Others

Such as technically low positions or undervalued CPOs, PCBs, and chips.

5) Recommendations

Since we are facing a super bull market, as long as you hold main line varieties, including the recently hot CPOs, PCBs, chips, etc., you can hold them steadily until clear adjustment signals are issued.

The September allocation plan is a forward-looking layout; do not rush to complete it in one step, as the market is full of variables and adjustments may occur at any time.

A basic principle remains unchanged: new productive forces, strategic minerals, anti-involution and cycle reversal, and innovative drugs are the main lines that do not change; their rotation exists, but accurately grasping it is difficult. Low buying and not chasing high, preparing to realize profits on overheated varieties and looking for new main lines is the basic operation.

The above represents personal views and does not constitute investment advice, for reference only.