At the 10th Automotive Electronics Innovation Conference, Zou Guangcai, Deputy Secretary-General of the China Automotive Chip Industry Innovation Strategic Alliance, stated: “The domestic automotive chip industry has caught up with a very good era.”

It is a rare consensus among various parties in the new energy vehicle industry that automotive chips should be self-reliant.

Recently, automotive-grade MCU provider Shanghai Xinwangwei Electronics Technology Co., Ltd. (hereinafter referred to as “Xinwangwei”) has had its IPO accepted on the Sci-Tech Innovation Board, with China Merchants Securities as the sponsor.

As a domestic supplier of self-developed instruction sets and cores, Xinwangwei faces less “bottleneck” risk, but the early exit of shareholders selling shares at a discount and the need to build a development ecosystem add a degree of uncertainty to its prospects amid the intense competition among automotive-grade MCU manufacturers.

01

Net Profit and Cash Flow Divergence

Founded in 2012, Xinwangwei is a specialized integrated circuit design company focused on the research, design, and sales of automotive-grade and industrial-grade MCUs based on its self-developed KungFu instruction set and MCU core.

In its early years, Xinwangwei primarily focused on self-developing MCU instruction sets and cores, successively developing the 8-bit KungFu8 instruction set and core, as well as the 32-bit KungFu32 instruction set and core, and mass-producing industrial-grade MCUs and AIoT MCUs equipped with the KungFu8 core.

The bit width of an MCU refers to the width of binary data processed by the CPU at one time; the higher the bit width, the stronger its computing power and the larger the supported storage space, making it more adaptable to complex application scenarios.

In 2019, Xinwangwei launched the KF8A series automotive-grade MCUs based on the KungFu8 core, primarily used in automotive windows, lighting, seats, panel displays, parking sensors, and water pumps. In 2020, it successively released industrial-grade, AIoT, and automotive-grade MCU products based on the KungFu32 core.

In 2021, Xinwangwei mass-produced the next generation of automotive-grade MCU products, the KF32A156 series, which successfully entered the supply chains of several well-known automotive parts manufacturers, applied in automotive lighting, seats, power motors, BCM, VCU, T-BOX, and new energy vehicle BMS scenarios.

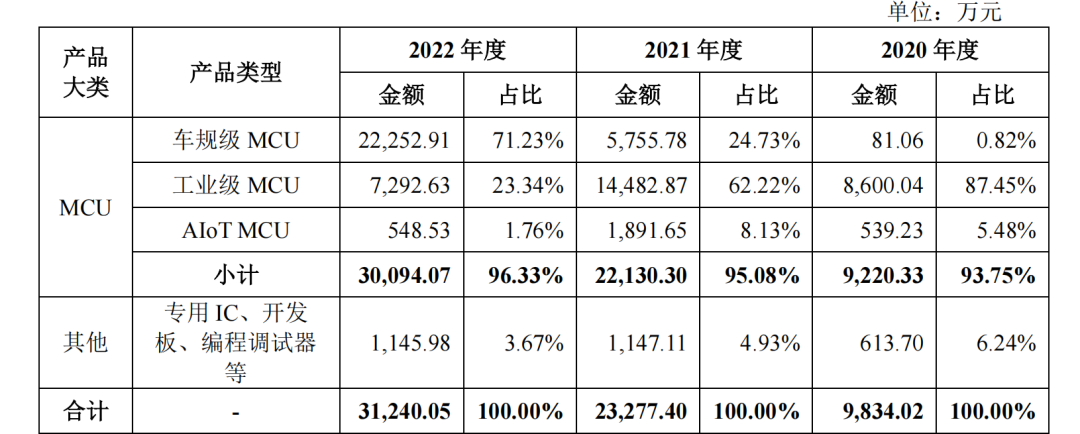

Currently, Xinwangwei’s products are primarily automotive-grade MCUs. From 2020 to 2022 (the “reporting period”), Xinwangwei achieved operating revenues of 98.34 million yuan, 233 million yuan, and 312 million yuan, with 0.82%, 24.73%, and 71.23% of these revenues coming from automotive-grade MCU products, respectively.

Image Source: Xinwangwei Prospectus

During the same period, its net profits were -26.20 million yuan, 51.03 million yuan, and 62.52 million yuan, respectively.

However, the net cash flow from operating activities has remained negative, with -8.51 million yuan, -10.45 million yuan, and -134 million yuan for each period, respectively.

The prospectus indicates that the main reason for the net cash flow from operating activities being lower than net profit in 2021 and 2022 was the increase in inventory, accounts receivable, and prepayments.

The increase in inventory was particularly significant. At the end of each reporting period, the book value of Xinwangwei’s inventory was 25.09 million yuan, 98.01 million yuan, and 253 million yuan, accounting for 18.77%, 17.83%, and 31.49% of current assets at the end of each period, respectively.

Xinwangwei explained that the company’s operational scale has been continuously growing, and the upstream wafer manufacturing sector has experienced capacity constraints. To ensure stable supply, the company has made significant inventory preparations. Coincidentally, in 2022, the global automotive “chip shortage” eased, leading to a significant increase in Xinwangwei’s inventory at that time.

02

The Era of Intense Competition for Automotive-grade MCUs

On July 19, the State Council Information Office held a press conference to introduce the development of industry and information technology in the first half of 2023. Data from the China Association of Automobile Manufacturers shows that the production of new energy vehicles increased by 42.4% in the first half of the year. Currently, the cumulative production of new energy vehicles in China has surpassed 20 million units.

New energy vehicles are seen as a great opportunity for the Chinese automotive industry to “overtake on a bend,” with both policy and capital leaning towards related industries.

In the trend of increasing intelligence, the development of new energy vehicles has also generated greater demand for MCUs—traditional fuel vehicles typically use dozens of MCUs, while smart vehicles can use over a hundred.

Since 2020, the automotive industry has experienced a chip shortage, leading to a surge in domestic automotive chip industry participants.

According to a report by the Workers’ Daily on July 16, statistics from the China Automotive Chip Industry Innovation Strategic Alliance’s standards working group show that there are currently over 100 companies in China engaged in the development and production of automotive chips, with more than 50 chip companies claiming to have automotive-grade products or mass production applications.

Currently, the domestic MCU market is relatively fragmented. According to statistics from the Forward Industry Research Institute, the market shares of leading domestic MCU companies such as Zhaoyi Innovation, Zhongying Electronics, Espressif Technology, Guomin Technology, and Fudan Microelectronics were 4.4%, 4.1%, 1.5%, 1.8%, and 0.8%, respectively, in terms of MCU business revenue scale in 2021.

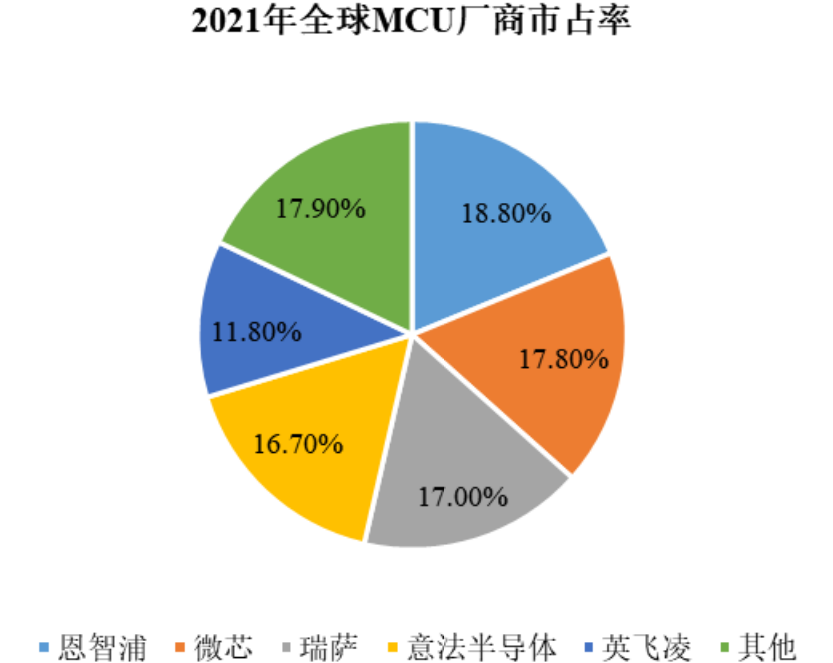

However, the chip industry is one where the strong get stronger; currently, the global MCU market is still dominated by foreign giants such as NXP, Microchip, Renesas, STMicroelectronics, and Infineon, with a CR5 of 82.1% in 2021, making it difficult to shake their position in the short term.

Image Source: Xinwangwei Prospectus

Currently, Xinwangwei’s scale is still relatively small, and the uncertainty will be greater as leading companies emerge and the industry gradually consolidates.

Xinwangwei’s advantage lies in its self-developed instruction set and core, which are not threatened by foreign manufacturers stopping authorization. However, this also presents a disadvantage; once MCUs enter downstream manufacturers, they typically require secondary development (application development) to achieve specific functions in different application fields, meaning the company needs more time and investment to build a development ecosystem. Consequently, the speed of development may be limited.

03

Valuation Exceeds 10 Billion, Shareholders Selling Shares at a Discount

Since 2021, Xinwangwei’s valuation has skyrocketed at a rocket-like pace.

In January 2021, Xinwangwei’s Series A financing raised a total of 80 million yuan from eight investment institutions, with a valuation of approximately 730 million yuan at that time.

In April 2021, Xinwangwei welcomed its Series B financing, with five institutions including Juyuan Development, Wanxiang Qianchao, and Jiaocheng SAIC offering 2.2 billion yuan for an additional registered capital of 934,600 yuan (approximately 8.56% of the total registered capital after the increase), corresponding to a valuation of approximately 2.564 billion yuan.

The Series C financing lineup was even more luxurious. From October 2021 to July 2022, Xinwangwei signed capital increase agreements with eight shareholders including Zhangjiang Ke Investment, Zhongke Xintai, Shanghai Kechuang, and CICC Changde, with a total price of 305 million yuan, bringing Xinwangwei’s valuation to 10 billion yuan.

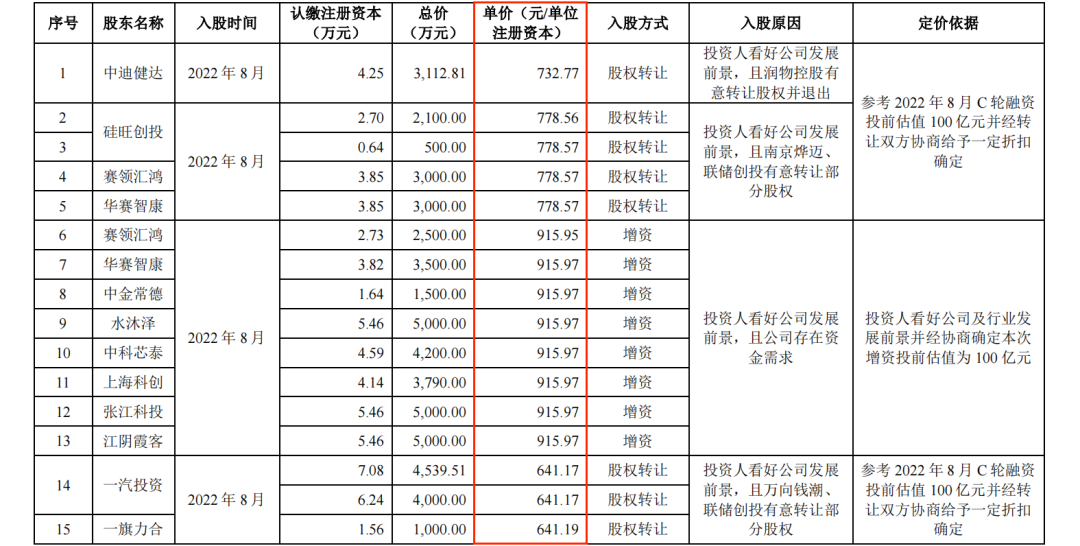

However, at the same time, some original shareholders also sold shares at a discount. In August 2022, Runwu Holdings, Nanjing Yema, and Lianchuang Venture Capital sold equity to Zhongdi Jianda and Silicon Wang Venture Capital at a price that was 20% and 15% lower, respectively.

In August 2022, FAW Investment and Yiqi Lihe acquired shares through equity transfer, with Wanxiang Qianchao and Lianchuang Venture Capital offering a “super low discount” of 30%, transferring 1.18% and 0.41% of Xinwangwei’s shares for 85.395 million yuan and 10 million yuan, respectively.

Image Source: Xinwangwei Prospectus

As of the date of signing the prospectus, Ding Xiaobing and the Ding brothers collectively hold 60.32% of Xinwangwei’s shares, directly and indirectly controlling 64.19% of the voting rights corresponding to Xinwangwei through Shanghai Xintao, Shanghai Xuexin, and Nanjing Yema, making them the company’s common actual controllers.

SAIC Group’s Jiaocheng SAIC and Shangqi Qifeng hold 1.89% and 1.82% of the shares, respectively, while FAW Group’s wholly-owned subsidiary FAW Investment and FAW Capital Holdings Co., Ltd. hold 1.18% and 0.14% of the shares, respectively, ranking as the 11th, 12th, and 15th and 35th largest shareholders of Xinwangwei.

Recommended Reading:

Yunzhisheng’s Move to the Hong Kong Stock Exchange: “Big Model” Hype Cannot Conceal the Truth of “Blood Loss”

Battery Complaints Due to Sudden Power Loss, Yugu Technology Targets Millions of Delivery Riders’ Electric Vehicles for IPO

Land Use Rights for Fundraising Projects Not Yet Approved, Changguang Chuangxin Eager to Rush for Sci-Tech Innovation Board IPO, What for?

Low Capacity Utilization, Rising Inventory Year by Year, Is the IPO of Shuangdeng Co., Ltd. for Lithium-ion Battery Projects Necessary?

Sales Data “Changing Faces”, Complex Acquisition Moves, Yanzhiwu’s IPO is More Unpredictable than Bird’s Nest Effects

Fuxin Technology’s Rush for Sci-Tech Innovation Board IPO: 99% Reliant on Major Clients, Still Accumulating Uncompensated Losses, No Dividends in Sight

Gaojing Solar Perfectly Demonstrates “Photovoltaic Wealth Creation”, IPO Valuation of 20 Billion After 3 Years

Can We Make Big Models Without Trillions of Parameters? Out the Door Asking Questions for Hong Kong IPO All Relying on “Annoying” AI Dubbing?

China Run Guang Energy’s GEM IPO Accepted: Performance Fluctuates Greatly, Asset-Liability Ratio Far Higher than Comparable Peers

Weak Blood Generation Ability, Heavily Dependent on Major Clients, Is Maichuang Co., Ltd. Providing After-sales Outsourcing Services to Xiaomi and Lenovo Also Going for IPO?

Now Available on Platforms