Remember to star the public account ⭐️ to receive notifications promptly.

Source: ContentTranslated fromsemiengineering.

Over the past decade, the data center processor market has undergone two significant transformations.

Previously, all data center computing was based on the x86 architecture, with over 90% coming from Intel. GPUs first appeared in data centers in 2016 (Pascal GPU).

Now, most computing is done on GPUs. AMD is striving to surpass Intel in the x86 market, while Arm-based CPUs are rapidly growing under the push from NVIDIA and hyperscale vendors.

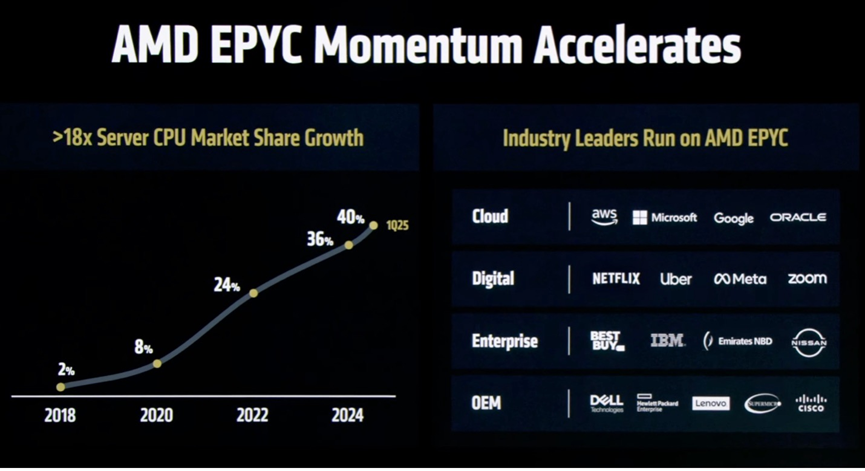

AMD is Replacing Intel in the Data Center CPU Space

AMD is quickly capturing Intel’s market share in the x86 data center processor space.

As shown in the image above, AMD’s share is currently 40%, compared to nearly zero in 2018. This is due to:

1. AMD President and CEO Lisa Su;

2. Lisa Su’s decision to switch to TSMC;

3. The excellent execution of her team;

4. Intel losing its leading position in semiconductor process technology.

These potential factors are unlikely to change quickly, so AMD is likely to become the largest x86 CPU supplier in data centers by 2026. (Intel’s 18A looks feasible on paper, but the company seems to be struggling with scaling nodes and related financial constraints).

AMD’s data center segment revenue for Q1 2025 was $3.7 billion, including CPUs and GPUs. The best estimate is that most of this is from server CPUs, with revenue for Q1 2025 around $2.5 to $3 billion.

In terms of unit numbers, in Q3 2024, the total shipment of server CPUs from AMD and Intel was 5.5 million units. This means an annual shipment of about 22 million units. The top four hyperscale vendors account for about half of this, with each company shipping about 2.5 million units per year. (Note: The average selling price of different CPUs can vary significantly. For example, AMD server CPUs are priced nearly twice that of Intel. Dollar revenue is a better indicator, but to compare with Arm, we only have unit number information.)

Hyperscale Companies Purchased About Half of the x86 Data Center Processors, and They All Use Arm-based CPUs

Mohamed Awad, Senior Vice President and General Manager of Data Center Infrastructure at Arm, stated in March that by the end of 2024, Arm-based CPUs will hold about 15% of the data center market share. However, he expects that by the end of 2025, Arm’s CPU share will grow to nearly 50%—this is roughly based on shipment share. (The following will discuss how Arm’s share may reach 50%, but not until late 2020).

This is due to two other significant transformations. First, hyperscale computing vendors are designing their own CPUs for general applications. Second, NVIDIA is designing its own CPUs for GPU co-processing.

About half of the data center CPU/GPU purchases are made by top hyperscale companies.

Arm’s Mohamed stated that the main motivation for hyperscale computing vendors to build their own CPUs is to optimize for specific workloads, achieving better power/performance. Reducing Intel/AMD’s profit margins is a consideration, but this alone may not justify the shift.

Of course, most workloads run by hyperscale companies are their customers’ software, which is currently primarily optimized for x86. Arm processors will first be used for workloads controlled by hyperscale companies—search, photos, shopping, Facebook, LLMs, etc. But looking at the websites of hyperscale companies, they are heavily promoting their Arm processors, so this situation will change.

Amazon was the first to adopt Arm architecture CPUs in data centers. The Graviton has entered its fourth generation since 2018. By mid-2024, Amazon had produced over 2 million Gravitons. Assuming 500,000 Gravitons are produced in 2024, this would account for about 20% of total x86 CPU procurement. Graviton is used as standalone compute instances in its cloud and in conjunction with GPUs. Amazon CEO Andy Jassy stated on CNBC on June 30 that Graviton offers 30% to 40% better cost-performance than x86, with lower power consumption.

Google released the Axion processor in April 2024. Google Cloud’s website claims that “Axion provides industry-leading performance and energy efficiency,” specifically stating that “performance is improved by 50% and energy efficiency by 60% compared to current generation x86 instances.”

Microsoft released the Azure Cobalt CPU (along with the Azure Maia AI accelerator) in 2023. Microsoft claims that its performance can save about 30% compared to x86.

While cost savings are important, power will ultimately become the most critical factor. When building increasingly large AI data centers for the Frontier LLM model, power is the biggest challenge.

All these Arm CPUs are available to cloud customers, and if their cost-performance is superior to x86, over time, customers will shift their workloads from x86 to Arm.

Earlier this year, Meta and Arm announced they are developing Arm data center CPUs.

NVIDIA has Shifted to Using Arm CPUs to Control its GPUs

In 2022, NVIDIA developed Grace, its first Arm-based data center CPU. It was initially deployed with the Hopper GPU and will be deployed this year with the Blackwell GPU. NVIDIA does not support the x86 architecture for Blackwell in NVLink72 configurations. Since NVLink72 offers the best performance, most enterprises will choose NVLink72 for deployment.

Comparing the Grace CPU with Intel’s Xeon Platinum 8480+ and AMD EPYC 9654, NVIDIA claims that Grace shows a relative performance improvement of 1.2 to 2.4 times in most non-AI benchmark tests, with energy efficiency improvements of 1.5 to 3.0 times.

JPMorgan expects shipments of Blackwell GPUs to reach 5 million in 2025 (7.5 million Blackwell/Rubin units in 2026). Two Blackwell GPUs are controlled by one Grace CPU, meaning that shipments of Grace CPUs will reach ~2.5 million in 2025. An expert in the data center infrastructure industry stated that for AI workloads, x86 servers are only used to run control plane operations, so for every 100,000 GPUs, 5 to 10 x86 CPU racks will be needed. One CPU rack can hold 42 1U servers, each of which can be equipped with 1 or 2 x86 CPUs. Doing the math, this means that for every 100,000 GPUs, 210 to 840 x86 CPUs are needed, while there are 50,000 Grace CPUs for every 100,000 GPUs. Therefore, for AI workloads, the number of Grace CPUs is 50 to 100 times that of x86.

Previously, we saw that the shipment of x86 data centers was about 22 million units. Considering the 2.5 million Grace CPUs produced by hyperscale vendors and about 1 million Arm-based CPUs, Arm’s market share in 2025 will be about 15%, rather than the nearly 50% predicted by Arm.

By 2030, Arm’s Share Will Increase, but Even So, x86 Seems to Remain Dominant

NVIDIA’s roadmap was released in March at the GTC 2025 conference, showcasing a new Arm processor named Vera, which will pair with the Rubin GPU and the Feynman GPU. Thus, NVIDIA will continue to pursue the Arm+GPU route.

The growth rate of CPUs connected to GPUs will far exceed that of other data center CPUs. Unless AMD’s GPU share grows rapidly (as AMD will connect its GPUs to x86 CPUs), these CPUs will primarily be based on Arm.

The remaining CPUs in data centers that are not directly connected to GPUs are half delivered to hyperscale computing vendors—all of whom are adopting Arm CPUs. These vendors offer better cost-performance and are likely to transition customers to Arm at lower prices.

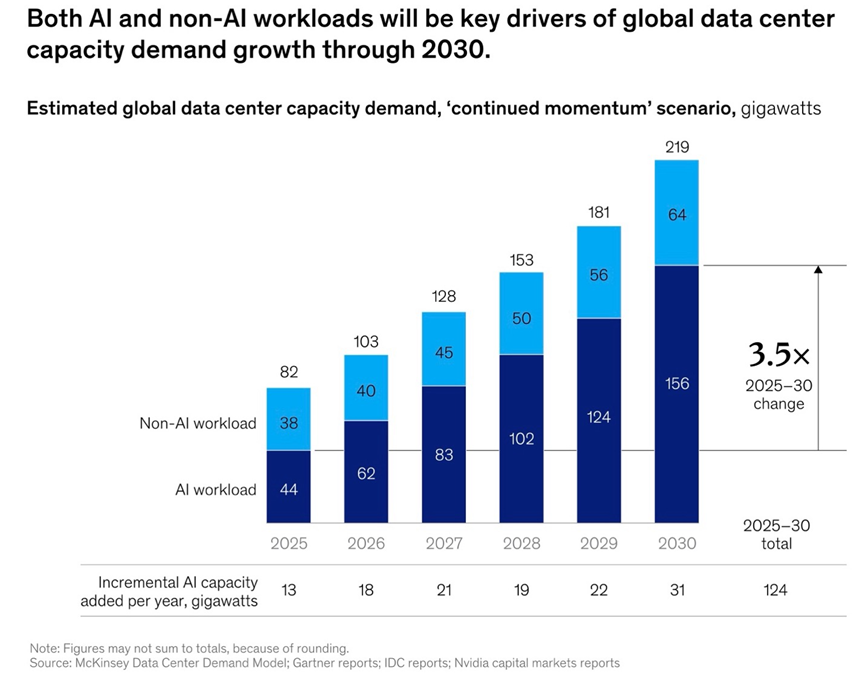

McKinsey released a forecast for data center growth in 2030 earlier this April.

By 2030, AI workloads measured in watts will grow 3.5 times. Non-AI workloads will grow 1.7 times.

If in 2025, non-AI workloads are handled by about 22 million x86 CPUs and about 1 million Arm CPUs, and the growth rate of compute units is as fast as GW (gigabytes) (rough estimate), then the number of compute units in 2030 will be about 37 million x86 CPUs and about 2 million Arm CPUs. Currently, we assume that hyperscale computing companies will not shift their CPU configurations to Arm. If the top four hyperscale computing companies (which account for about half) shift 50% of their CPUs to Arm, then by 2030, the number of compute units will be about 29 million x86 CPUs and about 1 million Arm CPUs. Considering the investments from hyperscale computing companies and their promotional efforts on their websites, the latter scenario seems more likely to occur.

If in 2025, non-AI workloads are handled by about 5 million GPUs, then by 2030, this demand will expand to about 18 million GPUs, requiring about 9 million Arm CPUs. (Depending on how GPUs are computed, the actual number of Arm CPUs may be lower).

Thus, by 2030, the total number of data center CPUs will reach about 48 million, with Arm’s share reaching up to 19 million. While these numbers are rough, they are sufficient to indicate that Arm will undoubtedly challenge the dominance of data center CPUs in the next decade. The two main factors driving this trend are: 1) Hyperscale companies will shift cloud workloads from x86 to Arm; 2) The number of Arm CPUs used in NVIDIA-based AI data centers will be 50 to 100 times that of x86.

Dollar share is more important, but we do not have average selling price data for Arm. The dollar share of x86 is likely to be higher than its shipment share, but the trend is still towards a steady increase in Arm’s share over time. AMD’s significant share acquisition in the AI field from NVIDIA will slow Arm’s share growth, as AMD is likely to use x86 rather than Arm for GPU co-processing.

Reference Link

https://semiengineering.com/data-center-cpu-dominance-is-shifting-to-amd-and-arm/

*Disclaimer: This article is original by the author. The content reflects the author’s personal views, and Semiconductor Industry Observation reproduces it solely to convey a different perspective, which does not represent Semiconductor Industry Observation’s endorsement or support of this view. If there are any objections, please feel free to contact Semiconductor Industry Observation.

END

This is the 4096th content shared by “Semiconductor Industry Observation”. Welcome to follow.

Recommended Reading

★A Chip That Changed the World

★U.S. Secretary of Commerce: Huawei’s Chips Are Not That Advanced

★“ASML’s New Lithography Machine, Too Expensive!”

★NVIDIA’s Quietly Rising New Competitor

★Chip Prices Plummeting, All Blame Trump

★New Solutions Announced to Replace EUV Lithography!

★Semi Equipment Giants, Salaries Soar by 40%

★Foreign Media: The U.S. Will Propose Banning Software and Hardware Made in China for Cars

Star the public account ⭐️ to receive notifications promptly, the small account to prevent loss

Like this post

Share this post

Recommend this post