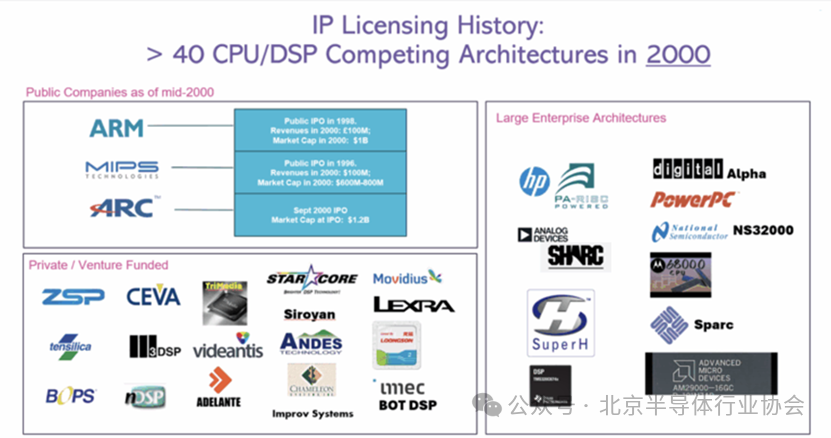

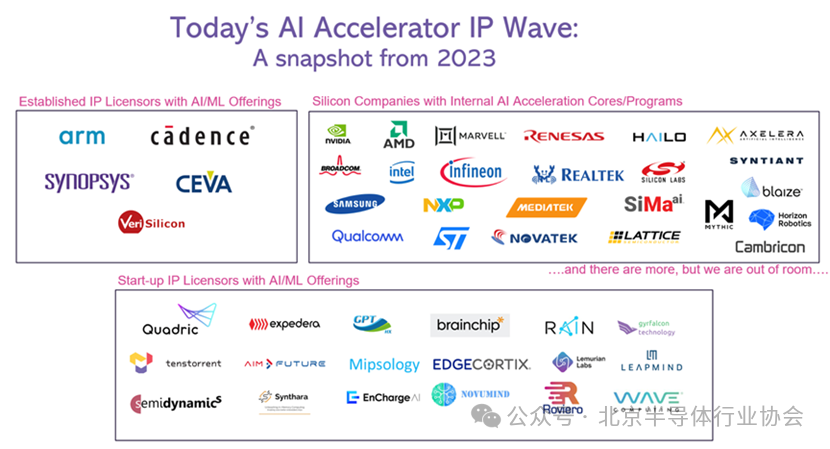

(Source: Quadric)Everyone learns about the cycle of population explosion and inevitable population collapse during their school years in natural or biology classes. Whether it is animals, plants, insects, or bacteria, certain external events trigger a rapid increase in the population of a species, leading to overpopulation and competition for resources (food, space, shelter). Ultimately, either the population explosion depletes the food supply, or the species itself becomes food for other predators, resulting in a significant death toll in the local population. This cycle remains consistent: external triggers, population explosion, resource depletion, and ultimately a collapse back to a population level that can be sustainably maintained in its native habitat.The same boom and bust cycle applies to the businesses created by humans to seize economic opportunities. New housing construction, oil extraction, and even trendy bubble tea businesses witness waves of new enterprises emerging, followed by inevitable market shocks that lead to downsizing, with weaker participants disappearing while stronger competitors survive and thrive. The semiconductor and semiconductor intellectual property industries are no exception, as keen observers can surely recall.The Turbulence of the Intellectual Property IndustryOver the past 25 years, whenever a new interface standard emerges or a new design trend becomes mainstream, we have witnessed the emergence of IP suppliers and chip startups trying to capture market share. In the field of processor IP, we have seen the rise of CPU, DSP, GPU, and even less common categories like packet processors.For example, consider the numerous CPU and DSP architectures that existed in 2000. The following image shows three public processor IP companies at the end of 2000, along with over 40 other companies that either licensed cores or built chips and systems using competing CPUs or DSPs. The semiconductor industry does not need—and cannot support—all 40 architectures. The surge in market participants was due to the onset of the system-on-chip (SoC) design era. SoCs require processors, leading to the birth of many processors or the spin-off of existing technology companies. Within a few years after the peak of the Y2K problem, the number of CPU and DSP licensing companies plummeted to fewer than 10. Most of the names and logos in the above image were no longer in existence by 2005, and some surviving companies (such as Tensilica and Arc) were acquired by larger firms.Referring to the analogy in nature, we cannot help but ask, what “resources” were these CPU/DSP companies lacking? Two main elements were in short supply: investment capital and compiler talent. Investors’ patience is limited, so many companies founded during the explosive growth period from 1998 to 2000 (coinciding with one of the largest stock valuation bubbles in history!) could not sustain themselves after 2005. Meanwhile, architectures that were less competitive and harder to program faced difficulties in hiring enough compiler talent to build advanced tools to compensate for their architectural disadvantages. Most of these companies ran out of time.Today’s NPUs—We’ve Seen This Movie Before!25 years have passed since the peak of CPUs and DSPs, and we are witnessing the same play in the NPU architecture field, albeit with different protagonists. The external trigger is the rapid development of artificial intelligence, with people rushing to integrate AI into various devices, from smartwatches to large data centers. From 2018 to 2024, this wave of opportunity has attracted a significant amount of investment capital.The second image captures a snapshot of some competitive NPU accelerator products (in IP form and embedded in silicon form) at the peak of the NPU wave two years ago.

The semiconductor industry does not need—and cannot support—all 40 architectures. The surge in market participants was due to the onset of the system-on-chip (SoC) design era. SoCs require processors, leading to the birth of many processors or the spin-off of existing technology companies. Within a few years after the peak of the Y2K problem, the number of CPU and DSP licensing companies plummeted to fewer than 10. Most of the names and logos in the above image were no longer in existence by 2005, and some surviving companies (such as Tensilica and Arc) were acquired by larger firms.Referring to the analogy in nature, we cannot help but ask, what “resources” were these CPU/DSP companies lacking? Two main elements were in short supply: investment capital and compiler talent. Investors’ patience is limited, so many companies founded during the explosive growth period from 1998 to 2000 (coinciding with one of the largest stock valuation bubbles in history!) could not sustain themselves after 2005. Meanwhile, architectures that were less competitive and harder to program faced difficulties in hiring enough compiler talent to build advanced tools to compensate for their architectural disadvantages. Most of these companies ran out of time.Today’s NPUs—We’ve Seen This Movie Before!25 years have passed since the peak of CPUs and DSPs, and we are witnessing the same play in the NPU architecture field, albeit with different protagonists. The external trigger is the rapid development of artificial intelligence, with people rushing to integrate AI into various devices, from smartwatches to large data centers. From 2018 to 2024, this wave of opportunity has attracted a significant amount of investment capital.The second image captures a snapshot of some competitive NPU accelerator products (in IP form and embedded in silicon form) at the peak of the NPU wave two years ago. With each rapid transformation in artificial intelligence—such as the emergence of Transformers and then LLMs—waves of fixed-function accelerators have become obsolete, and we have seen some of those names disappear. Today, the resource scarcity that led to the collapse of numerous CPU startups a generation ago is rapidly diminishing the number of AI accelerator startups in the current market. Chip startups either fail or are acquired for their engineers (the latest example being Untether). NPU licensing companies struggle to build complex compilers that map increasingly complex AI algorithms onto unnecessarily complex architectures that combine traditional processors with matrix accelerators. Most ominously, venture capitalists are no longer willing to write large checks for round after round of reckless investment. Instead, they demand to see market attractiveness—either through increased chip output or improved licensing success rates.How Many Will Survive?The world does not need, nor can it support, over 50 NPUs. The world also does not want to see only one survivor—no one likes an 800-pound gorilla dominating the market. The number of NPUs will ultimately shrink to 5 to 10 winners. As the number of competitors decreases, 2025 will become a turning point in the NPU field. The winners will possess the following characteristics: (1) an excellent software toolchain (compiler) capable of handling thousands or tens of thousands of AI models; (2) tools that allow end-users to easily program new AI models onto chips as data scientists continue to innovate rapidly; (3) commercial attractiveness that can attract new capital for continued investment and growth.

With each rapid transformation in artificial intelligence—such as the emergence of Transformers and then LLMs—waves of fixed-function accelerators have become obsolete, and we have seen some of those names disappear. Today, the resource scarcity that led to the collapse of numerous CPU startups a generation ago is rapidly diminishing the number of AI accelerator startups in the current market. Chip startups either fail or are acquired for their engineers (the latest example being Untether). NPU licensing companies struggle to build complex compilers that map increasingly complex AI algorithms onto unnecessarily complex architectures that combine traditional processors with matrix accelerators. Most ominously, venture capitalists are no longer willing to write large checks for round after round of reckless investment. Instead, they demand to see market attractiveness—either through increased chip output or improved licensing success rates.How Many Will Survive?The world does not need, nor can it support, over 50 NPUs. The world also does not want to see only one survivor—no one likes an 800-pound gorilla dominating the market. The number of NPUs will ultimately shrink to 5 to 10 winners. As the number of competitors decreases, 2025 will become a turning point in the NPU field. The winners will possess the following characteristics: (1) an excellent software toolchain (compiler) capable of handling thousands or tens of thousands of AI models; (2) tools that allow end-users to easily program new AI models onto chips as data scientists continue to innovate rapidly; (3) commercial attractiveness that can attract new capital for continued investment and growth.