The humanoid robot sector has risen by 66% since April.

On September 16, the robot sector led the entire market, hitting the daily limit. This was triggered by statements from Tesla regarding two key points, which directly ignited the domestic robot-related industrial chain.

On September 16, the robot sector led the entire market, hitting the daily limit. This was triggered by statements from Tesla regarding two key points, which directly ignited the domestic robot-related industrial chain.

New positioning, new valuation

On the evening of September 16, Tesla CEO Elon Musk announced plans to conduct a technical assessment of the A15 chip design on Saturday, and will hold a special meeting with various departments next week to focus on discussing artificial intelligence/autonomous driving systems, and the mass production of Optimus robots.

Previously, at the All-In Summit, Musk discussed the latest developments regarding the Optimus robot. He stated that the third version of Optimus currently being designed will address hand flexibility, possess an AI brain, and is expected to achieve mass production. These three advantages are unmatched by any competitors.

The high-profile mass production of AI robots stems from Tesla’s strategic upgrade from an “automobile manufacturer” to a “robot manufacturer.” Emphasizing the potential of humanoid robots, Musk also mentioned that 80% of Tesla’s value will depend on the Optimus robot.

Tesla previously positioned itself as an “electric vehicle and clean energy company,” while the “Master Plan Part Four” marks its official upgrade to an “artificial intelligence and robotics company.”

Expanding from “accelerating the world’s transition to sustainable energy” to achieving a “sustainable affluent society” through AI and robotics.

This means that new energy vehicles and energy are no longer Tesla’s main tasks, practically acknowledging the future competition in hard technology, with the main arena being the AI and robotics sectors.

The support behind the mass production plan exceeding expectations is the maturity of the industrial chain.

Previously, it was rumored that Tesla held a conference call with suppliers, revising the guidance for the third quarter of next year to a weekly production of 1,000 to 10,000 units, corresponding to an annual output of 50,000 to 500,000 units.

In addition to the intensive visits by domestic companies to North America in late August, it is expected that Tesla will come to China for factory inspections in September, and the Gen3 is expected to be released in October-November, with the shareholder meeting also likely to showcase Gen3.

According to an industrial chain order plan estimate:“Customers have three levels of production capacity requirements, namely weekly production of 1,000 units, 5,000 units, and 10,000 units, linked to five-year contracts, with different pricing corresponding to different capacities.”

Weekly production of 1,000 units is expected to start ramping up in August next year, with the Thai factory completing its first batch of capacity construction in Q1 next year, aiming to achieve a capacity of around 5,000 units by the end of next year.

Rough estimates of annual shipment volume:

Rough estimates of domestic supply chain profit elasticity (baseline scenario: weekly production of 5k, shipment of 200,000 units):

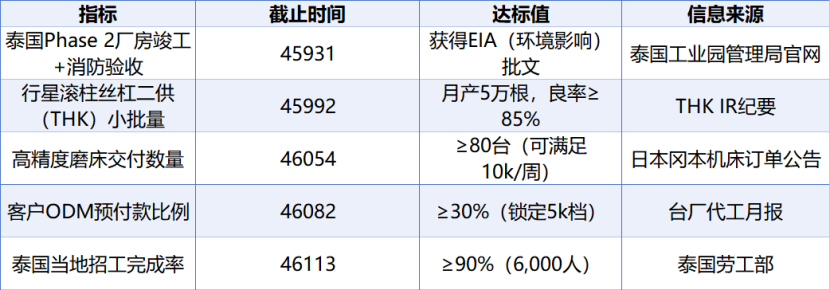

Tracking indicators for achievement probability:

(For each standard met, the “5k achievement probability” can be raised by 10pct; if all standards are met, the probability can increase from 55% to 100%, at which point the model can be directly switched to the “baseline scenario” or even the “optimistic scenario.”)

Assuming only the lower limit of 50,000 is achieved, the target number is also beyond expectations, boosting the industry’s outlook for next year.

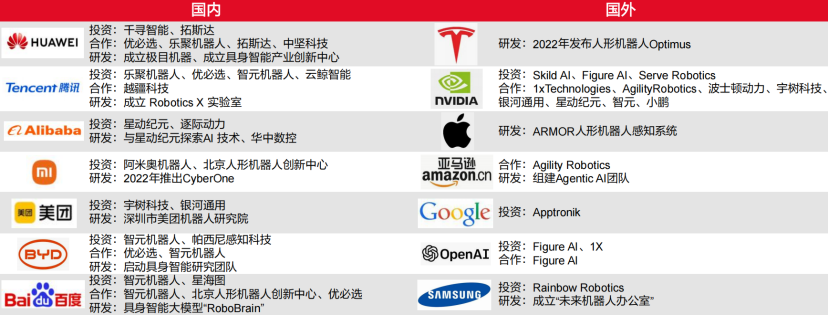

In addition to the above expectations for the industrial chain’s production capacity, progress in various fields of the robotics industry is accelerating.

Overseas: On the evening of September 16, Figure Robotics announced the completion of over $1 billion in Series C financing, with a post-financing valuation of $39 billion. It is worth noting that its Series B financing valuation was only $2.6 billion.

This round of financing will be used to promote the large-scale deployment of humanoid robots in household and commercial scenarios, accelerating the training and simulation of embodied intelligence models.

The company will also initiate the collection of real-world datasets, including human videos and multimodal sensory input data, to enhance the robot’s understanding and operational capabilities in complex, dynamic environments.

Figure AI’s first BotQ automated production line has officially gone into production, currently achieving an annual capacity of 12,000 units. Figure AI aims to increase its annual production capacity to 100,000 units within four years.

Domestic companies such as Zhiyuan and Yushu have also entered the small-batch production stage. It is expected that by 2029, the global humanoid robot market will reach 150 billion yuan.

Domestically: On August 18, Zhiyuan Robotics officially launched three quadruped robot products—D1Pro, focusing on entertainment and education research, D1Edu, and D1Ultra for industrial applications.

Zhiyuan’s six core product lines—Expedition A2 series, Lingxi X2 series, Elf G1, OmniHand dexterous hand series, quadruped robot D1 series, and commercial cleaning C5, are now available for sale on Zhiyuan Mall and JD Mall.

On September 2, Yushu Technology is expected to submit its listing application documents between October and December 2025. In the revenue structure for 2024, quadruped robots, humanoid robots, and component products are expected to account for approximately 65%, 30%, and 5%, respectively, with about 80% of quadruped robots being used in research, education, and consumer fields, while the remaining 20% will be used in industrial fields such as inspection and firefighting, and humanoid robots will be fully utilized in research, education, and consumer fields. As of the end of May 2025, the order backlog (excluding framework agreements) is 2.84 billion yuan, a year-on-year increase of 190%.

The company plans to invest 290 million yuan in R&D in 2024, accounting for 42.6% of revenue, focusing on humanoid robot motion control algorithms and self-developed servo motors; the sales expense ratio is 35.3%, reflecting that the company is in a global market expansion phase.

The company’s operating cash flow is expected to turn positive for the first time in Q1 2025, amounting to 37 million yuan, marking the beginning of a self-sustaining business model.

According to the latest round of financing estimates in the private equity market, Yushu Technology’s current valuation is approximately 8.5 billion yuan, corresponding to 12.5 times its 2024 revenue, significantly higher than the 5-8 times valuation level of industrial robot companies.

On September 3, UBTECH received a procurement contract worth 250 million yuan for embodied intelligent humanoid robot products and solutions from a well-known domestic enterprise, primarily featuring the humanoid robot WalkerS2 (equipped with an autonomous hot-swappable battery system), which will commence delivery within this year. This is currently the largest contract for humanoid robots globally.

The above is just the tip of the iceberg regarding changes in the robotics industry, with progress updates seemingly occurring every few days, while the market gradually becomes “numb.”

The reason is that robots are still some distance away from truly penetrating real life.

People still find performance robots clumsy, delivery robots unattractive, and sanitation robots lagging…

Amidst the novelty, it is still evident that current robots require human supervision and companionship, with concerns about robots going out of control, which seems consistent with the worries people had during the early days of electric vehicles.

However, it is undeniable that current robots cannot truly care for humans in a meaningful way.

So, where exactly are the “dumb” robots lacking?

Or rather, where are the opportunities for the industry to leap forward?

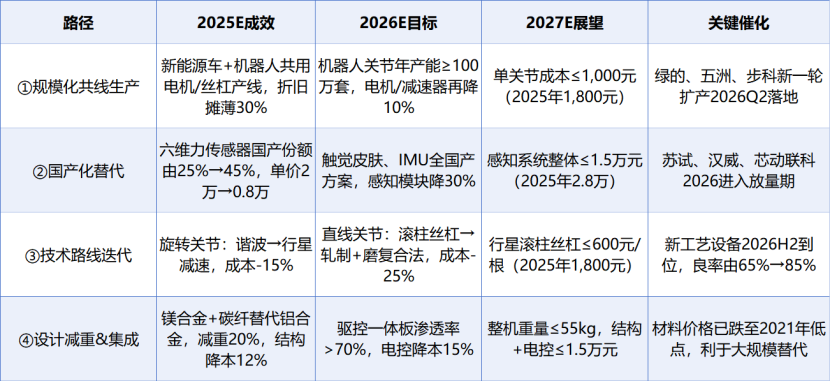

At least two points: reducing hardware costs and enhancing brain efficiency.

Reducing hardware costs is on the way.

In fact, hardware costs have been gradually decreasing with the maturity of the industrial chain, but they have not yet reached the level for large-scale application.

Taking the Unitree G1 standard version as an example, the launch price in Q1 2024 is 399,000 yuan, while the e-commerce price in July 2025 is expected to be 99,000 yuan (hardware cost ≈ 71,000 yuan), representing a 75% reduction over 18 months; its self-developed joints account for over 80%, with domestic substitutes for hollow cup motors, height reduced to 1.27m, and degrees of freedom reduced to 23. The company’s target price for 2026 is 58,000 yuan, corresponding to a hardware cost of 42,000 yuan, a further 40% reduction.

Looking at the industrial chain, scaling, localization, and technological iteration will all drive down hardware costs:

From the current statements, the proportion of self-produced joint modules is expected to increase:“Self-developed planetary gear reducers and drivers have been mass-produced, and by 2026, motors will also be produced in-house.”Single joint costs are expected to drop from 1,199 yuan to 900 yuan;

Collaboration with Xusheng Group to develop magnesium alloy integrated skeleton, with trial production expected in Q4 2025, reducing shell costs by 30%;

Collaborating with CATL to develop “robot-specific LFP modules,” with mass production expected in 2026, reducing battery pack costs by 20%.

The “ChatGPT” moment for robot brains has not yet arrived.

Understanding real-world data training is crucial for robots; previously, many training methods involved directly placing robots in factories, so those robot manufacturers with automotive factories can obtain training data through repeated practical training.

Tesla, Figure in collaboration with BMW, UBTECH in collaboration with BYD, and Zhiyuan are all examples of this. (Smart readers will have noticed the consistency between the robotics industry chain and the automotive parts industry chain.)

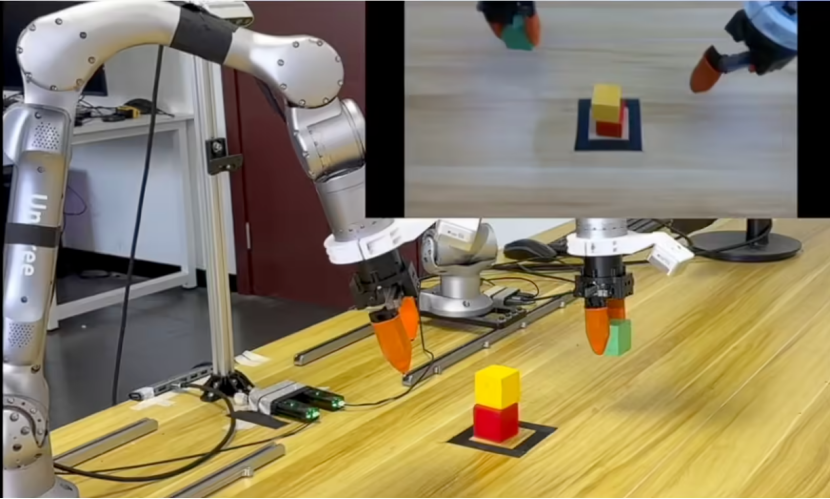

On September 15, Unitree announced the open-sourcing of UnifoLM-WMA-0.UnifoLM-WMA-0 is an open-source world model for various types of robots, designed for general robot learning, with its core component being a world model that understands the physical laws of robot-environment interactions.

(The small window shows the world model’s predictions for future action videos)

The world model has two core functions:

One is the simulation engine (Sim Mode), which uses current images + future action sequences to generate high-fidelity interactive videos in real-time, providing unlimited synthetic data for robot learning.

The second is policy enhancement (Policy Mode), where the world model acts as a “prophet module” connected to the action head, evaluating the consequences of actions in advance and then outputting the optimal control instructions.

In other words, the simulation engine acts like a virtual training ground, generating a large amount of synthetic data for robot learning and training;

policy enhancement can predict the “next step” of robots in real environments, providing reference for decision-making. This allows humanoid robots to become “smarter” without needing to trial and error in real environments every time.

The open-sourcing of UnifoLM-WMA-0 is not only a technical release but also a strategic move by Unitree to define a “general learning base for robots”: to eliminate the bottleneck of “scarcity of real data”; to make “cross-body zero-shot transfer” possible; and to transition the “robot brain” from specialized algorithms to a unified world model.

However, one milestone does not mean the climax of industrial development.

As Unitree Technology founder Wang Xingxing said at the 2025 Inclusion Bund Conference: “Currently, data and models are the challenges for robots, such as how to collect high-quality data for robots and how to truly improve the utilization of data.

Letting AI work is currently a desert in the entire field, with only a few small grasses growing, and we are on the eve of explosive growth.

【Welcome to communicate, contact the assistant via private message】Industry research topic materials;Price-volume-time-space determines buying points;Main force thinking is the trendDetails related to the company are updated daily in the knowledge circle or paid articles, mentioning Mingzhi, JS Leili, Baiwei, and Zhaowei on September 8 and 11.Knowledge Circle. Scan the QR code to join the reading.

Disclaimer

This content is a dynamic compilation of publicly available market information, recorded as personal learning notes, and is for informational reference only. It does not constitute any investment recommendations; you need to make independent investment decisions, and any actions taken based on this are at your own risk. The market has risks, and investment requires caution. Research is not easy, please support with likes!