Recently, the prices of various chemical products, industrial goods, and raw materials have surged, attracting widespread attention in the market. Behind the fluctuating price curves lie three critical questions that the market is most concerned about: What is driving this round of price increases? How long can this upward trend last? Can the performance of upstream and downstream companies in the supply chain seize this opportunity for recovery, and how will it reshape the competitive landscape of the industry?

The price increase is the most sensitive pulse signal in the recovery of the economic context. The Shanghai Securities Journal WeChat account has launched a series of reports titled “Market Exploration of Price Increases”, aimed at highlighting the market vitality and changes in business logic behind this series of price fluctuations. Through the sound of “increase,” we listen to the footsteps of recovery; amidst the ebb and flow, we glimpse a promising future.

Shenghong Technology’s market value has surpassed 200 billion yuan, while the market values of Pengding Holdings, Shengyi Technology, and Huadian Co., Ltd. have all exceeded 100 billion yuan. Additionally, the market values of Shenzhen South Circuit and Dongshan Precision have surpassed 90 billion yuan; since the beginning of the year, there have been as many as 18 A-share PCB concept stocks with price increases exceeding 100%… A small circuit board (PCB) has unleashed astonishing energy in the A-share market, and the driving force behind this is: AI.

Corresponding to the soaring market value is the continuous growth of the performance of leading PCB industry chain companies. Half-year reports show that companies in the PCB industry chain, such as Shengyi Electronics, Tongguan Copper Foil, Helitai, Pengding Holdings, and Shengyi Technology, have all reported good performance growth in the first half of the year, with Shengyi Electronics experiencing a remarkable increase of 452.11% in its performance.

AI has driven strong market demand for related categories, becoming the biggest driving force for the growth of the PCB industry, rapidly boosting the revenue and profits of related companies. Coupled with the insufficient supply and rising prices of upstream copper foil and fiberglass cloth, PCB industry chain companies have recently initiated intensive price increases. The aforementioned PCB leader, Shengyi Electronics, had already raised prices for PCB products in the second quarter.

Looking ahead to industry development trends, several interviewed industry insiders indicated that due to the months-long expansion or product validation required for fiberglass cloth, the current tight supply situation is unlikely to ease in the short term, which will provide certain support for PCB product prices. Furthermore, with the rapid development of emerging industries such as AI and new energy vehicles, the demand for high-end PCBs continues to rise, and the industry’s prosperity is expected to further improve, with product price increases likely to continue until the end of the fourth quarter.

However, it is important to emphasize that this round of PCB price increases is not a universal increase for all products. The aforementioned industry insiders stated that only products related to AI (i.e., AI PCBs) have strong market demand, thus supporting price increases. However, as more manufacturers enter the market and expand production capacity, prices and profit margins are expected to show a downward trend in the long term.

Half-Year Performance is Impressive; AI is the Biggest Driving Force

The peak period for half-year report disclosures has arrived, with data from dozens of companies already outlining the rapid growth of the PCB industry chain and the driving forces behind industry growth.

According to statistics from the Shanghai Securities Journal, as of August 19, a total of 11 companies in the PCB industry chain have released their 2025 half-year reports, all achieving year-on-year growth in operating income, with 10 companies achieving year-on-year growth in net profit attributable to shareholders, and 3 companies achieving a year-on-year growth in net profit attributable to shareholders exceeding 100%.

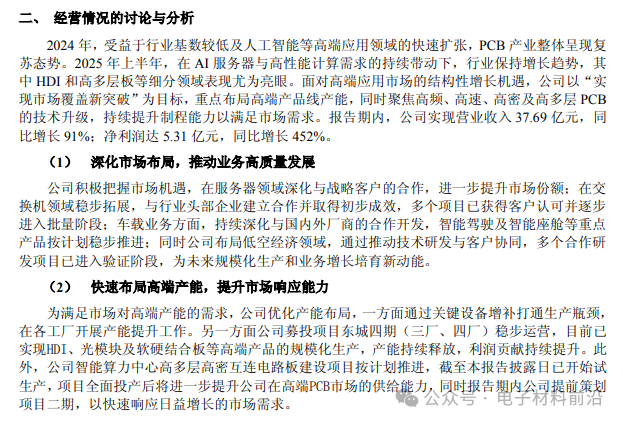

Shengyi Electronics currently ranks first in the PCB industry performance growth rankings. Shengyi Electronics disclosed that the company achieved total operating revenue of 3.769 billion yuan in the first half of the year, a year-on-year increase of 91%; net profit attributable to shareholders reached 531 million yuan, a year-on-year increase of 452.11%. As an upstream copper-clad laminate company, Shengyi Technology achieved total operating revenue of 12.68 billion yuan in the first half of the year, a year-on-year increase of 31.68%; net profit attributable to shareholders reached 1.426 billion yuan, a year-on-year increase of 52.98%.

Further examination of the half-year reports of Shengyi Electronics and others reveals that the strong market demand driven by AI is the biggest driving force for the growth of the PCB industry.

Shengyi Electronics disclosed that in the first half of 2025, driven by the continuous demand for AI servers and high-performance computing, the industry maintains a growth trend, with sub-sectors such as HDI (High-Density Interconnect) and high-layer boards performing particularly well. The company is focusing on expanding its high-end product line capacity while concentrating on the technological upgrades of high-frequency, high-speed, high-density, and high-multilayer PCBs, continuously enhancing process capabilities to meet market demand.

Tongguan Copper Foil stated that the overall environment of the copper foil market remains challenging in the first half of the year, and the operational situation of copper foil production enterprises is still severe. However, with the rapid global development of AI, the demand for HVLP copper foil, which serves as the substrate for AI servers, is strong and continues to grow.

Benefiting from AI demand, Tongguan Copper Foil’s production of high-end HVLP copper foil in the first half of the year has already exceeded the total output for the entire year of 2024, driving the company’s revenue in the first half of the year to increase by 44.80% year-on-year, and net profit attributable to shareholders to increase by 159.47% year-on-year.

With strong downstream AI demand, industry growth is expected, and the PCB industry chain has also become a favorite among secondary market investors. Since April of this year, the stock prices of multiple companies have entered a continuous upward trend. Among them, Shenghong Technology’s market value has surpassed 200 billion yuan, while the market values of Pengding Holdings, Shengyi Technology, and Huadian Co., Ltd. have all exceeded 100 billion yuan, and the market values of Shenzhen South Circuit and Dongshan Precision have surpassed 90 billion yuan; since the beginning of the year, there have been as many as 18 A-share PCB concept stocks with price increases exceeding 100%.

Fiberglass Cloth in Short Supply; Industry Prosperity May Last Until Year-End

Recently, the news of price increases for copper-clad laminates used in PCBs has become a market hotspot. Companies such as Jiantao, Weilibang, and Hongruixing issued price increase notices on August 15, with price increases ranging from 5 to 10 yuan per copper-clad laminate.

“The most pressing issue now is the delivery time for substrates, and the key problem behind this is the shortage of fiberglass cloth used for substrates.” When discussing the price increase of copper-clad laminates, individuals from chip design companies and substrate companies interviewed stated that due to supply shortages, many PCB companies are urgently validating new fiberglass cloth suppliers such as Lisenor (Shanghai) and Taishan Fiberglass, but this validation process takes several months.

Electronic-grade fiberglass cloth (i.e., fiberglass cloth) is also known as electronic cloth, made from specific specifications of glass fiber yarn, and is an essential raw material for manufacturing core copper foil substrates for electronic products, providing the substrates with excellent electrical properties and mechanical strength. Market information shows that since April, the stock price of A-share fiberglass cloth company Honghe Technology has continuously risen, with a cumulative increase exceeding 316%.

Public information shows that due to rising costs of raw materials such as quartz sand and labor, the demand for AI servers (which require 5 to 8 times the demand of ordinary servers) and the large-scale production of wind turbine blades have driven high-end orders, leading to a rebound in the price of fiberglass cloth globally in the first half of 2025. Nitto Denko raised its product prices by about 20% in August this year.

In terms of production capacity, the global fiberglass cloth industry presents a pattern of “China leading production, high-end Japanese companies in the lead, and Asia-Pacific demand driving”. In high-end products (such as Low-Dk electronic cloth and quartz cloth), companies like Asahi Kasei, Nitto Denko, and AGY from the United States dominate the global market.

“Validating distant water cannot quench the immediate thirst; the tight supply and extended delivery times of raw materials such as fiberglass cloth (which accounts for about 30% of the cost of copper-clad laminates) will lead to continued price increases for copper-clad laminates, coupled with sustained growth in downstream demand, this round of PCB price increases is expected to last until the end of the fourth quarter,” said the aforementioned substrate company personnel, adding that PCB boards have also begun to increase in price.

It is understood that although China has a huge PCB production capacity, both substrates and fiberglass cloth are weaknesses in the domestic PCB industry chain. In terms of PCB substrates, only a few companies such as Shenzhen South Circuit and Xingsen Technology have some supply capabilities. In the fiberglass cloth sector, China National Materials Technology (its wholly-owned subsidiary Taishan Fiberglass) is a leader in domestic Low-Dk electronic cloth, with its first-generation products already in volume production, and the second-generation product development is accelerating, while quartz cloth is entering the customer certification stage.

In addition, the rise in copper prices has also become one of the driving forces behind the price increases of copper-clad laminates. China Galaxy Securities pointed out that although we are still in the off-season for copper demand, the demand in the power grid and new energy sectors remains resilient, and domestic social inventories are still at low levels compared to the same period last year, maintaining a premium structure in the spot market, which continues to support copper prices. With supply constraints at the mining end, the Federal Reserve likely restarting interest rate cuts in September, and the demand peak season of “Golden September and Silver October,” copper prices are expected to continue to rise steadily.

Strong AI Demand; Leading Companies Actively Expand Production

Looking ahead to the development trends of the PCB industry, Shengyi Electronics stated that the rapid development of the AI industry is sufficient to support the growth of the PCB market, with the global PCB market value expected to grow by 7.6% to reach 79.128 billion USD by 2025. From a medium to long-term perspective, it is predicted that by 2029, the global PCB market value will reach 94.661 billion USD, with a compound annual growth rate of 5.2% from 2024 to 2029, still showing a stable growth trend.

Shengyi Technology disclosed that according to Prismark’s forecast, servers, AI servers, and data centers have become the core driving forces for market growth, while the demand for HDI in laptops and gaming consoles is also showing good growth trends, particularly in the automotive sector, where the smart driving field is performing exceptionally well, thus driving rapid growth in related PCB demand, with the growth rate of 18+ high-multilayer boards expected to reach 41.7%, and HDI boards expected to grow by 12.9% year-on-year by 2025.

Under the strong market demand, companies in the PCB industry chain are actively initiating expansion plans.

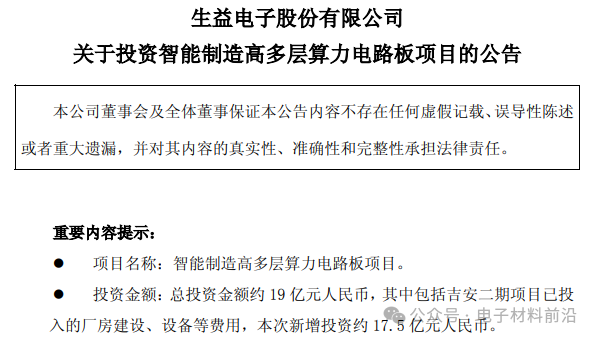

For example, Shengyi Electronics disclosed on August 16 that to meet the demand of the mid-to-high-end market for servers, high-multilayer network communication, and rapidly developing AI computing power, the company has decided to invest in the intelligent manufacturing high-multilayer circuit board project in part of the existing factory floors of the second phase project in Ji’an, with a total planned investment of approximately 1.9 billion yuan, aiming for an annual production of 700,000 square meters of printed circuit boards, with each phase producing 350,000 square meters annually.

“Due to the rise of the AI server and switch market, our first-generation low-dielectric electronic cloth products that we have reserved will start volume production in the second half of 2023, with accelerated volume production in the second half of 2024, currently in a situation of supply exceeding demand,” said China National Materials Technology during an institutional survey, adding that to make Taishan Fiberglass an indispensable supplier in the AI field, the company plans to establish China National Materials Special Fiber (Shandong) Co., Ltd. in Taian, Shandong, with an investment of 1.302 billion yuan to build a “special fiberglass cloth project with an annual output of 26 million meters” by October 2024.

The increase in production capacity has also become one of the highlights disclosed in the half-year reports of many companies. For instance, Shengyi Technology disclosed that the second phase project of Jiangxi Shengyi Technology Co., Ltd. began phased production in June this year, and once fully operational, it will achieve an additional annual production capacity of 18 million square meters of copper-clad laminates and 34 million meters of commercial adhesive sheets.

Source: Shanghai Securities Journal; Author: Li Xingcai