A well-known VC has acquired an 8 billion chip company.

Since the China Securities Regulatory Commission released the “Six Guidelines for Mergers and Acquisitions” on September 24 last year, merger and acquisition transactions across the country have gradually heated up. In the semiconductor field, several notable transactions have emerged.

For example, Shanghai semiconductor company Jingfeng Mingyuan announced that it will acquire control of Yichong Technology. Gelaun Electronics announced its intention to purchase Chengdu Ruicheng Micro’s equity. Recently, the 300 billion market value Haiguang Information initiated a takeover of the 90 billion Zhongke Shuguang. The consolidation of the semiconductor industry chain has entered a phase of multiple blossoming.

Unlike the aforementioned cases, a recent transaction in the industry involved PE/VC using an industrial platform to initiate a merger.

Zhiying Electronics recently announced that its controlling shareholder, Weilang International, and shareholder Win Channel Ltd. signed a “Share Transfer Agreement” to transfer a total of 14.20% of the company’s shares. The share transfer price is 25.677 yuan/share, with a total transaction price of approximately 1.245 billion yuan. After the transaction is completed, the actual controller of the company will change to Zhinen Industrial.

Zhiying Electronics is a leading domestic MCU (Microcontroller Unit) company, with its main products applied in home appliances and other fields. Zhinen Industrial, on the other hand, is a corporate group focused on industrial and automotive chips. The “marriage” of the two companies will expand into the industrial and automotive MCU fields.

However, what is more noteworthy is the “background” of Zhinen Industrial. It is an industrial platform established through cooperation between Shanghai State-owned Assets, Xuzhou State-owned Assets, and Wuyuefeng Science and Technology. Its own industrial business proportion is not high, but under Wuyuefeng’s management, it has continuously acquired and invested in seven semiconductor companies, building a large industrial group. Zhinen Industrial is also seen by some industry insiders as an investment platform.

PE/VC integrating and acquiring through controlling an industrial platform is not common in the current industry. However, we find that Wuyuefeng, Linxin Capital, and others are attempting this. Although the paths vary, these investors share a common inclination: to personally take charge, engage in “entrepreneurship,” and explore the possibilities of chip investment in the second half of the market by becoming long-term operators.

20% Premium Acquisition, 67-Year-Old Founder Cashes Out 1.2 Billion

20% Premium Acquisition, 67-Year-Old Founder Cashes Out 1.2 Billion

Let’s take a look at the transaction between Zhiying Electronics and Zhinen Industrial. We have summarized the key points from their published “Detailed Report on Equity Changes” as follows:

First, Zhiying Electronics’ controlling shareholder Weilang International will hold 31,718,000 shares of the listed company; Win Channel Ltd. will transfer its 16,767,396 shares to Zhinen Industrial. After the completion of this share transfer, Zhinen Industrial will hold 48,485,396 shares of the listed company, accounting for 14.20% of the total shares of the listed company.

Second, the share transfer price is 25.677 yuan/share, with a total share transfer price of 1.245 billion yuan.

Third, Zhinen Industrial will also control an additional 9.2% of Zhiying Electronics’ shares through voting rights entrustment, totaling 23.4% of the voting rights of the company.

Fourth, the controlling shareholder Weilang International is the shareholding platform of Zhiying Electronics’ founder Fu Qiming. After the transaction is completed, the actual controller of the listed company will change from Fu Qiming to Zhinen Industrial. Zhinen Industrial has no actual controller, and Zhiying Electronics will also change to having no actual controller.

From the above points, this transaction is not complicated. The original 67-year-old founder cashes out, and a new actual controlling party enters. The transaction price offers a 20% premium compared to the pre-suspension price of 21.41 yuan/share. The transaction and governance are expected to transition smoothly.

Moreover, for Zhiying Electronics, it may be in urgent need of alliances with external parties.

This company, founded by semiconductor veteran Fu Qiming, has a history of 31 years. Before starting his business, Fu Qiming worked at companies such as United Microelectronics Corporation and Philips. After starting his business in 1994, he targeted the rapidly growing home appliance industry, launching home appliance MCUs and other products; in 2008, he entered the consumer electronics sector, launching the first BMIC (Battery Management Integrated Circuit); after 2016, he expanded into AMOLED (Display Driver ICs), entering the smartphone supply chain.

As a leading company in the MCU field, the company’s stock price reached a record high of 82 yuan/share in November 2021, with a market value once reaching around 25 billion. However, in the past two years, the company’s market value has been shrinking, now only about one-third of its original value, around 8 billion.

The continuous decline in stock price is accompanied by shrinking operational data.

Data shows that from 2022 to 2024, Zhiying Electronics’ revenue is projected to be 1.602 billion, 1.3 billion, and 1.343 billion, showing an overall downward trend. Looking at the net profit attributable to the parent company, it is projected to be 323 million, 186 million, and 134 million, with year-on-year declines of 12.86%, 42.32%, and 28.01%. In 2024, the company’s gross profit margin is expected to be only 33.6%, the lowest in 17 years. This year, it further dropped to 32.1% in the first quarter.

The decline in both revenue and profit is partly due to the sluggish growth of traditional businesses. Zhiying Electronics’ main revenue comes from industrial MCUs used in white goods, which account for 81% of its revenue, reaching 1.093 billion. Although this business has a market share of 25%, second only to Renesas Electronics in China, it is already in a saturated market, with very limited growth potential. Meanwhile, the BMIC and AMOLED products used in consumer electronics have shrunk due to the weak consumer electronics market.

Another reason is the conservative management strategy of the team, which has led to slow progress in high-end industries and new businesses. The most anticipated new business for Zhiying Electronics is the automotive-grade MCU launched after 2021. However, after three years, it is still in the customer introduction phase, with slow progress.

Therefore, from Zhiying Electronics’ perspective, it needs a new ally that can provide support in the automotive-grade MCU field and open up new opportunities for the company.

Zhinen Industrial, Investing in 7 Semiconductor Companies

Now looking at the buyer, Zhinen Industrial is indeed the bigger highlight of this transaction.

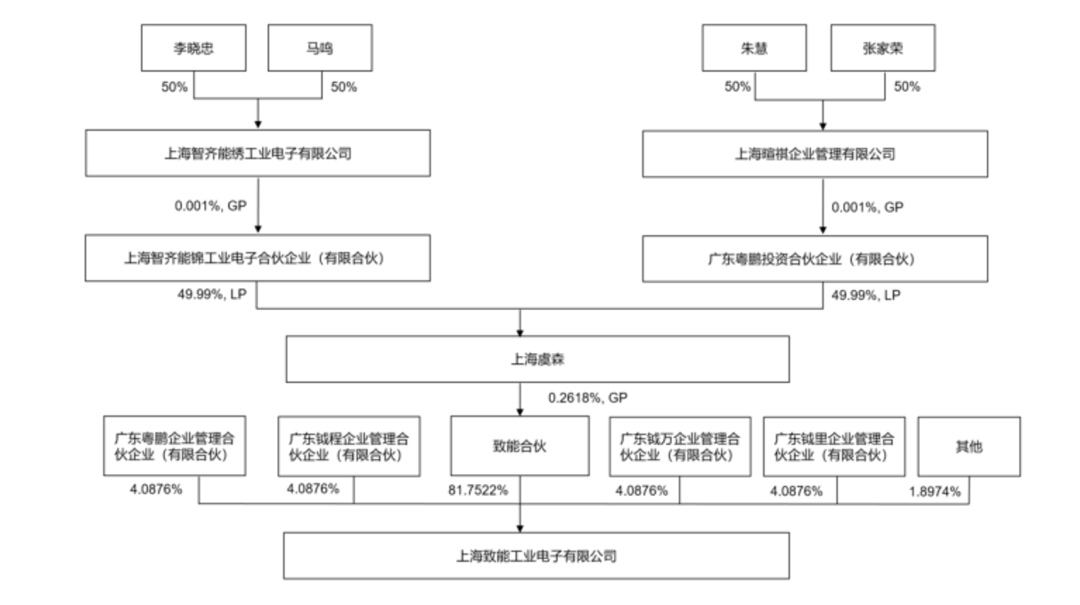

Zhinen Industrial was established in December 2020. The equity structure shows that the largest shareholder is Zhinen Partners, holding 81.75%. Upon further investigation, this partnership was jointly established by Shanghai Venture Capital (50%), Shanghai Wuyuefeng Phase II Integrated Circuit Fund (32.28%), Shanghai Yuxin (8.726%), and Shanghai Qian Can (8.20%).

Zhinen Industrial’s control relationship. Source: Company announcement

Among them, Shanghai Yuxin is a fund under Wuyuefeng; Shanghai Qian Can is a fund established in cooperation between Xuzhou State-owned Assets (Xuzhou Industrial Development Fund, Xuzhou Jinlonghu Industrial Fund) and Wuyuefeng. Thus, as disclosed in Zhiying Electronics’ “Detailed Report on Equity Changes”:

“A high-end intelligent industrial electronics industry platform-level enterprise group established through market-oriented mechanisms, mainly focusing on the layout and industrial ecosystem construction in the industrial and automotive chip fields.”

Zhinen Industrial’s profit statement shows that the company’s revenue scale is not large in the industry, with projected revenue of 206 million in 2024. After deducting operating costs and expenses for sales, management, and R&D, the main business is expected to incur a loss of about 81 million, while the company’s other income, investment income, and fair value change income total about 100 million, with fair value change income reaching as high as 88 million. This means that the company’s current profit mainly comes from the appreciation of its investment portfolio.

This also indicates that Zhinen Industrial is still in the layout and construction phase and holds a considerable amount of high-quality assets that continue to appreciate. However, it is worth noting that in 2023, Zhinen Industrial’s investment income was nearly 200 million, which shrank to 72 million in 2024, indicating that the speed of investment portfolio appreciation has slowed down.

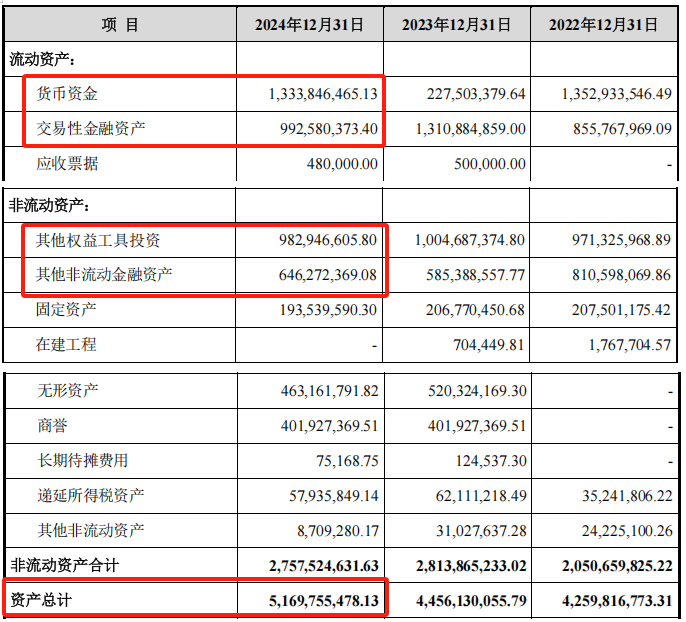

The balance sheet shows that the company has a very high proportion of current assets, with cash and trading financial assets reaching 2.327 billion, generating over 7.5 million in interest income each year. Other equity instrument investments and non-current financial assets total 1.629 billion, accounting for 76.52% of the total assets of 5.17 billion. Combined with the decreasing construction projects year by year, Zhinen Industrial has essentially become an investment institution primarily focused on investments.

From the development history, this judgment is confirmed. After its establishment in 2020, Zhinen Industrial began an intensive investment layout. CVSource data shows that this enterprise has invested in at least 7 companies in the integrated circuit field.

At the beginning of 2021, Zhinen Industrial initiated a takeover of the listed company Broadcom Integrated. It first acquired a total of 6% of the shares from Broadcom’s three old shareholders for 559 million. It then subscribed to Broadcom’s non-public offering, increasing its shareholding to 9.64%, becoming the second-largest shareholder.

In the same year it invested in Broadcom Integrated, Zhinen Industrial also invested in three integrated circuit companies: power semiconductor designer Shanghai Hengtai Ke, automotive semiconductor design company Chipways, and high-performance dedicated MCU chip supplier Taixi Microelectronics.

After 2022, Zhinen Industrial’s industrial layout further expanded. In August 2022, it fully acquired Shaoxin Integrated Circuit. In 2023, it acquired the remaining shares of Shanghai Hengtai Ke, turning it into a wholly-owned subsidiary; by the end of 2023, it participated in a strategic investment in the analog and mixed-signal IC design company Angbao Electronics.

The main application scenarios of these companies are all related to the automotive field. For example, the wholly-owned subsidiary Hengtai Ke is a key supplier for fast charging, energy storage, and motor drive. Taixi Micro specializes in the development of automotive-grade MCU chips.

Moreover, from these investments, Zhinen Industrial often chooses to invest heavily. It either seeks a controlling position or, in minority equity investments like Chipways and Taixi Micro, becomes the second-largest shareholder after the founding team.

If this acquisition of Zhiying Electronics goes smoothly, Zhinen Industrial will control (or hold shares in) 7 semiconductor companies, forming a chip industry group serving the automotive, industrial, and consumer fields. In the MCU segment, Zhinen Industrial will create a product matrix for “home appliances + industrial + automotive” scenarios. Whether in traditional fields like home appliances or emerging fields like smart vehicles, this will greatly enhance its influence. This industrial synergy is seen as a reason to support the 20% premium acquisition.

Semiconductor VC’s Second Half, Answers Provided by Wuyuefeng

Furthermore, although Zhinen Industrial has no actual controller structure, as an investment-oriented industrial platform, the leading party is naturally Wuyuefeng. The legal representative and chairman of Zhinen Industrial, Li Xiaozhong, is one of the core team members of Wuyuefeng.

In the semiconductor investment circle, Wuyuefeng is gaining momentum. In 2009, Wu Ping resigned as CEO of Spreadtrum Communications, and two years later, he co-founded the venture capital firm “Wuyuefeng” with two Tsinghua alumni—former president of Synopsys Asia Pacific Pan Jianyue and founder of Yipin Media Li Feng—dedicated to investing in the integrated circuit field.

Currently, this institution manages over 50 billion yuan in funds and has invested in over 200 companies. Companies like Zhaoyi Innovation, Shanghai Silicon Industry, Rockchip, Guangli Micro, and Huaqin Technology all have its shadow behind them. In the field of semiconductor mergers and acquisitions, Wuyuefeng is a pioneer; it led the Chinese consortium’s acquisition of ISSI in 2015, marking the first successful privatization of a US-based IC design company by Chinese capital.

However, taking the helm of Zhinen Industrial means that Wuyuefeng has chosen not to establish a fund to participate in corporate mergers but to lead investments in a corporate model, which has attracted industry attention for at least three reasons:

First, mergers and acquisitions take a long time; in addition to the transaction itself, long-term management and cultural integration are required. A corporate model has no expiration date, allowing for maximum time cost payment; second, platform companies, in addition to having LP investments, can also generate continuous cash flow through early investments and industrial operations, providing funding guarantees for later mergers; third, the fund’s management fee model may not align the interests of enterprises, GPs, and LPs. However, a corporate model allows fund managers to become entrepreneurs and business owners, focusing more on long-term operations and enterprise cultivation, which is welcomed by state-owned LPs oriented towards industrial cultivation.

Moreover, I have observed that not only Wuyuefeng but also many institutions focused on semiconductor investments are beginning to enter the second half of semiconductor investments through the operation of industrial platforms.

For example, at the end of 2021, Lin Yajun, who leads Linxin Investment, became the second-largest shareholder of Chongqing Road and Bridge by acquiring shares held by Tongfang Guoxin. Soon after, Lin Yajun became the general manager of Chongqing Road and Bridge, using this platform to drive semiconductor mergers.

At that time, Lin Yajun explained the benefits of this approach: on one hand, Chongqing Road and Bridge has good cash flow, which can provide capital support for merger transactions. On the other hand, the Chongqing side also supports the transformation and upgrading of traditional enterprises, helping Linxin to strengthen the integrated circuit industry in Chongqing.

In 2024, Chongqing Road and Bridge initiated a takeover of Lanzi Electronics, planning to acquire no more than 15.01% of Lanzi Electronics through capital increase + old stock transfer. Although this transaction was ultimately terminated, Lin Yajun remains the general manager of Chongqing Road and Bridge, and efforts to promote semiconductor mergers have not ceased.

Another semiconductor investment institution, Xingcheng Capital, has established Yuehai Integrated in Zengcheng, Guangzhou, utilizing its industrial resources in the semiconductor field. Unlike the previous two, it is not investment-led but has chosen to create a “manufacturing + packaging” core industrial company. This company has already built high-end sensor 8-inch/12-inch TSV packaging projects and has received funding from Guangzhou Industrial Investment and Zengcheng Industrial Investment.

The approaches of these three institutions naturally differ: Wuyuefeng has established an investment platform in partnership with state-owned assets; Linxin Investment controls (or leads) a listed company to promote semiconductor project participation and mergers; Xingcheng Capital is creating an industry by attracting previous LPs or state-owned funds to participate. The challenges they face are also different: Linxin Investment first needs to integrate internally within the listed company; Xingcheng Capital must fight within the industry; Wuyuefeng’s path appears lighter, but coordinating and merging multiple companies is not easy either.

However, regardless of the differences, the attempts of these investment institutions all exhibit the characteristics of a “founder model”: taking charge personally, engaging in “entrepreneurship,” and raising the expectations of investors.

Looking at the resume of Li Xiaozhong, chairman of Zhinen Industrial, you can see that he previously served as president of Xiaxing Electronics (600057), later joined Wuyuefeng Science and Technology as an investment partner, and represented Wuyuefeng in the preparation and financing of Shanghai Silicon Industry’s listing, making him a veteran adept in both operations and investments in the semiconductor sector. Now, investors are becoming entrepreneurs and long-term operators, which may be their answer for the second half of investment.

*Disclaimer: This article is the original work of the author. The content reflects their personal views, and our reposting is solely for sharing and discussion purposes, not representing our endorsement or agreement. If there are any objections, please contact us.